What Is Seller's Discretionary Earnings (SDE) and How to Calculate It

When you're buying or selling a small business, one number drives everything: seller's discretionary earnings, or SDE.

Not revenue. Not net profit. Not gross margin. SDE.

If you've spent any time looking at business listings or talking to brokers, you've probably seen SDE thrown around constantly. Businesses are priced as "a multiple of SDE." Buyers calculate what they can pay based on SDE. Sellers try to maximize their SDE before going to market. It's the central metric of small business valuation, and if you don't understand it, you're at a serious disadvantage on either side of a deal.

Let me break down exactly what SDE is, how to calculate it, and where most sellers go wrong.

What SDE Is and Why It Matters More Than Net Profit

Net profit is the number left over after you've paid all the business expenses, including the owner's salary. For large companies with professional management, net profit makes sense as a valuation basis. But for small businesses where the owner is also the operator, net profit dramatically understates what the business is actually generating.

Here's why. A business owner might pay themselves a $120,000 salary. That salary is an expense on the income statement, which reduces net profit. But a buyer who acquires that business will also be the operator. They don't have to pay someone else $120,000 to do that job. So from a buyer's perspective, that $120,000 is money available to them, not a true business cost.

SDE adds that back. It starts with net profit and then adds back the owner's compensation, owner perks, and any other expenses that were discretionary to this particular owner and won't necessarily be costs for the next owner. The result is a cleaner picture of what the business actually generates for whoever owns and operates it.

SDE is the total financial benefit available to a single owner/operator. It answers the most important question in small business valuation: "How much does this business actually put in the owner's pocket?"

For small businesses under about $5 million in revenue, SDE is the standard valuation metric. Above that size, EBITDA tends to be used instead. The difference matters.

The SDE Formula

SDE is calculated using this formula:

Net Income + Owner's Compensation + Add-Backs = SDE

Each component needs to be defined carefully:

Net Income is the bottom line from the business's income statement, after all expenses including the owner's salary and any taxes.

Owner's Compensation includes W-2 salary, distributions, and any other compensation the owner took from the business. This gets added back in full.

Add-Backs are expenses that appeared on the income statement but that a new owner would not incur, or that were discretionary to the current owner. These include things like the owner's health insurance, personal vehicle expenses run through the business, personal travel, rent paid to a related landlord at above market rates, and one-time expenses that won't recur.

The total is SDE: the true earning power available to a working owner.

What Qualifies as an Add-Back

Add-backs are where sellers most often get tripped up, in both directions. Some sellers miss legitimate add-backs that cost them money at closing. Others try to add back things that aren't defensible, which causes buyers and lenders to discount the whole SDE calculation.

Here are the main categories of legitimate add-backs:

Owner's Compensation and Benefits

Everything the owner received from the business gets added back. This includes:

- W-2 wages and salary

- Owner distributions (profit distributions from an S corp or LLC)

- Health insurance premiums paid by the business for the owner and their family

- Retirement contributions the business made on behalf of the owner

- Owner's life insurance premiums paid through the business

- Any auto allowances or vehicle lease payments for the owner's personal vehicle

Personal Expenses Run Through the Business

Many small business owners run personal expenses through the business. These are legitimate add-backs if they're documented:

- Meals, entertainment, or travel that were personal in nature

- Cell phone or home internet paid by the business for personal use

- Memberships (gym, clubs, subscriptions) that were personal

- Home office deductions if they don't reflect a real business expense

- Clothing and personal items categorized as business expenses

One-Time or Non-Recurring Expenses

Expenses that happened this year but won't happen again:

- Legal fees for a dispute that has been resolved

- Equipment repairs that were exceptional, not routine maintenance

- Costs related to a one-time expansion project

- Consulting fees for a specific project that's complete

- Insurance settlement payments

- Costs from a natural disaster or other unusual event

Non-Cash Charges

These reduce accounting profit without affecting cash:

- Depreciation on equipment and assets

- Amortization of intangibles (if applicable)

- Owner's share of cost basis adjustments in pass-through entities

Excessive or Inflated Expenses

Sometimes an owner pays more than market rate for something that benefits them personally:

- Rent paid to a related party above market rate (the difference between what was paid and market rent is the add-back)

- Compensation paid to family members who don't actually work in the business, or who are paid above market for work they do

Each add-back needs to be documented with proof. Not just a verbal claim. An actual expense record that shows what was paid and why it qualifies as discretionary.

The five categories of legitimate add-backs are owner compensation, personal expenses run through the business, one time costs, non cash charges, and above market related party expenses. If an expense does not fit cleanly into one of these categories, it probably is not a defensible add-back.

Step by Step SDE Calculation with a Real Example

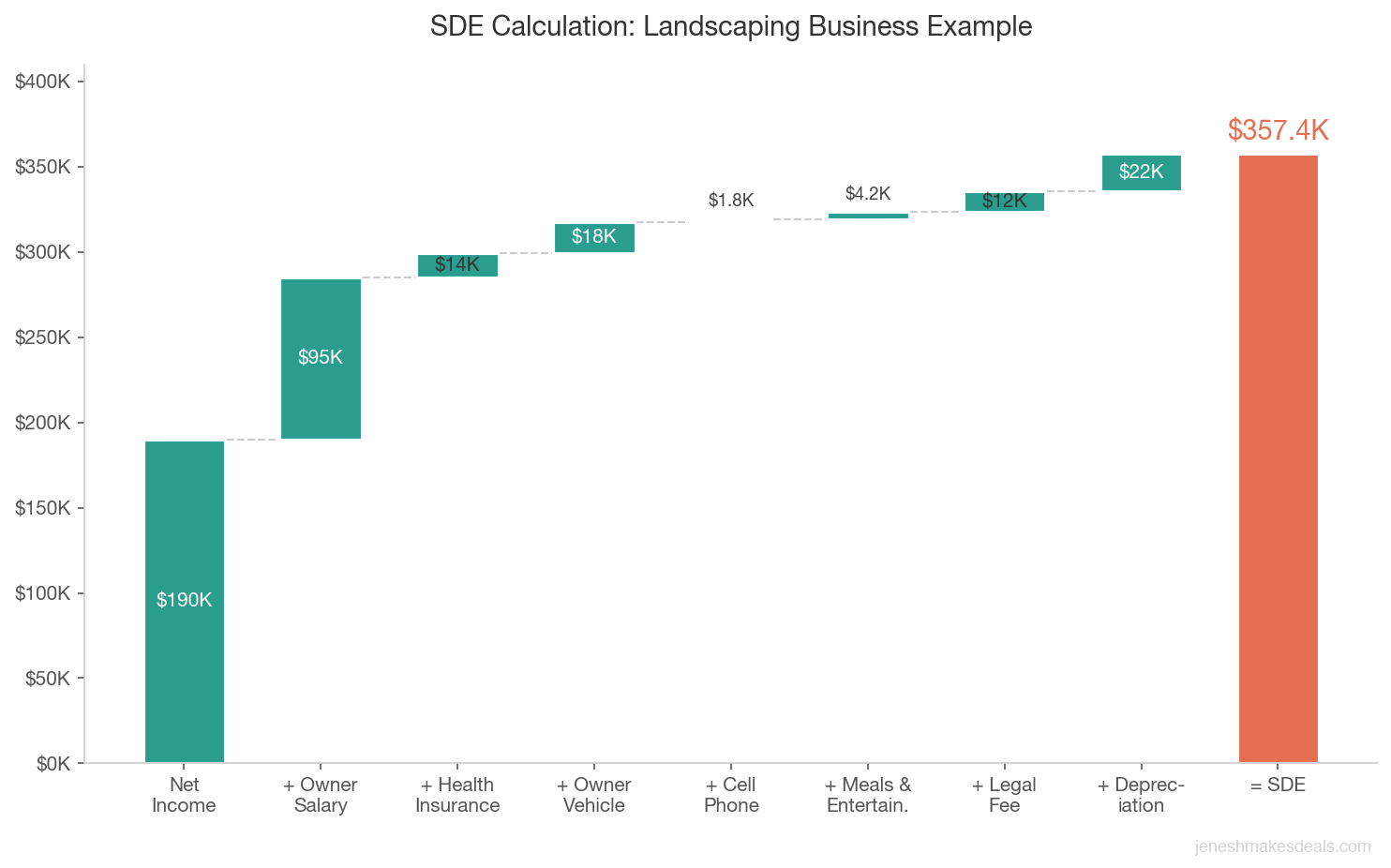

Let me walk through a real calculation. Say you're selling a landscaping business. Here are the numbers from last year's tax return and bookkeeping. Knowing how to read business tax returns before buying helps verify these add-backs are legitimate:

Income Statement:

- Revenue: $1,450,000

- Cost of goods sold: $720,000

- Gross profit: $730,000

- Operating expenses: $540,000 (includes everything below)

- Net income: $190,000

Now the add-backs from that $540,000 in operating expenses:

| Item | Amount |

|---|---|

| Owner W-2 salary | $95,000 |

| Owner health insurance | $14,400 |

| Owner vehicle (personal truck) | $18,000 |

| Owner cell phone | $1,800 |

| Personal meals/entertainment | $4,200 |

| One-time legal fee (resolved) | $12,000 |

| Depreciation (non-cash) | $22,000 |

| Total Add-Backs | $167,400 |

SDE Calculation:

- Net income: $190,000

- Plus add-backs: $167,400

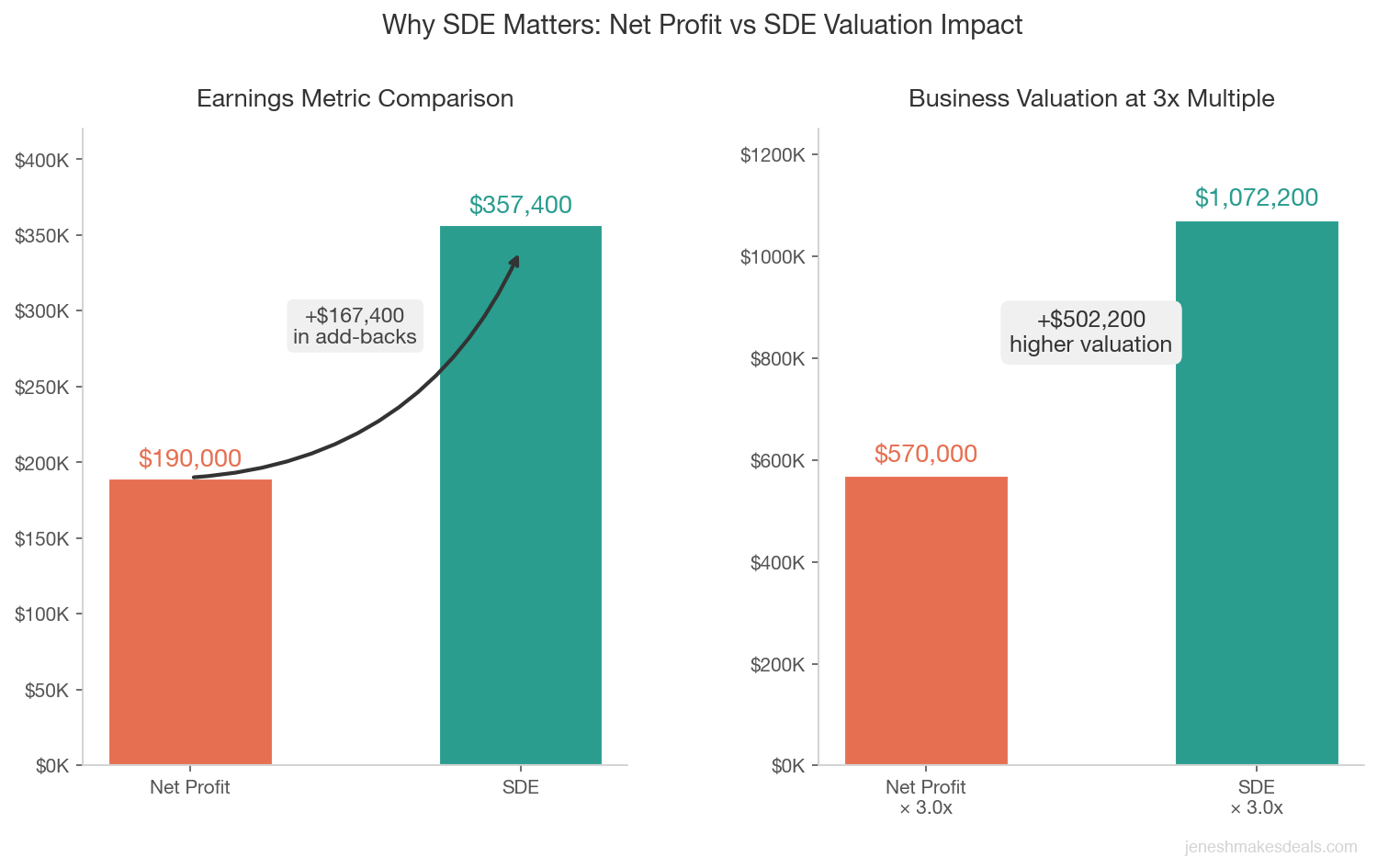

- SDE: $357,400

That's a dramatically different number than the $190,000 net income. A buyer looking at only net profit and applying a 3x multiple would value this business at $570,000. With SDE at $357,400 and the same 3x multiple, the value is $1,072,200.

The difference is real money. This is why understanding add-backs matters so much in any business transaction.

Using net profit instead of SDE to value a small business can understate the true value by 40% or more. In this example, the difference is over $500,000.

Use our business valuation calculator to see how SDE multiples translate to business value for your specific situation. Our listing price estimator can also help you figure out a realistic asking price based on your SDE.

SDE vs. EBITDA: When to Use Each

SDE and EBITDA (earnings before interest, taxes, depreciation, and amortization) measure similar things but are used in different contexts. Understanding which metric applies to your situation is important. For a full breakdown of EBITDA, see what EBITDA means and how buyers use it.

When to Use SDE

SDE is the right metric for businesses where:

- Revenue is under $5 million (typically)

- The owner actively works in the business and is compensated through it

- The business is being sold to an individual buyer who will be the operator

- Comparing businesses in small business marketplaces

SDE answers the question: "What does this business earn for a working owner?"

When to Use EBITDA

EBITDA is the standard for larger businesses where:

- Revenue is $5 million or more

- Professional management is (or will be) in place

- The buyer is a financial buyer (private equity) or larger company

- The business is large enough that management is a separate cost from ownership

EBITDA answers the question: "What does this business earn for an investor who isn't working in it?"

| Factor | Use SDE | Use EBITDA |

|---|---|---|

| Business revenue | Under $5M | Over $5M |

| Buyer type | Individual operator | Investor or strategic buyer |

| Owner role | Actively working | Not involved in operations |

| Market context | Small business marketplace | Middle market / M&A |

| Owner's comp adjustment | Fully added back | Not added back (replaced by a manager at market wages) |

If you're selling a small business to an individual buyer, use SDE. If you're selling a business large enough to have professional management, use EBITDA. Mixing these up is a common mistake that leads to mispriced deals.

The simplest rule: if the owner works in the business and the buyer will too, use SDE. If the business has (or will have) a paid management team running day to day operations, use EBITDA.

For a deeper look at valuation methods, see my guide on how to value a business.

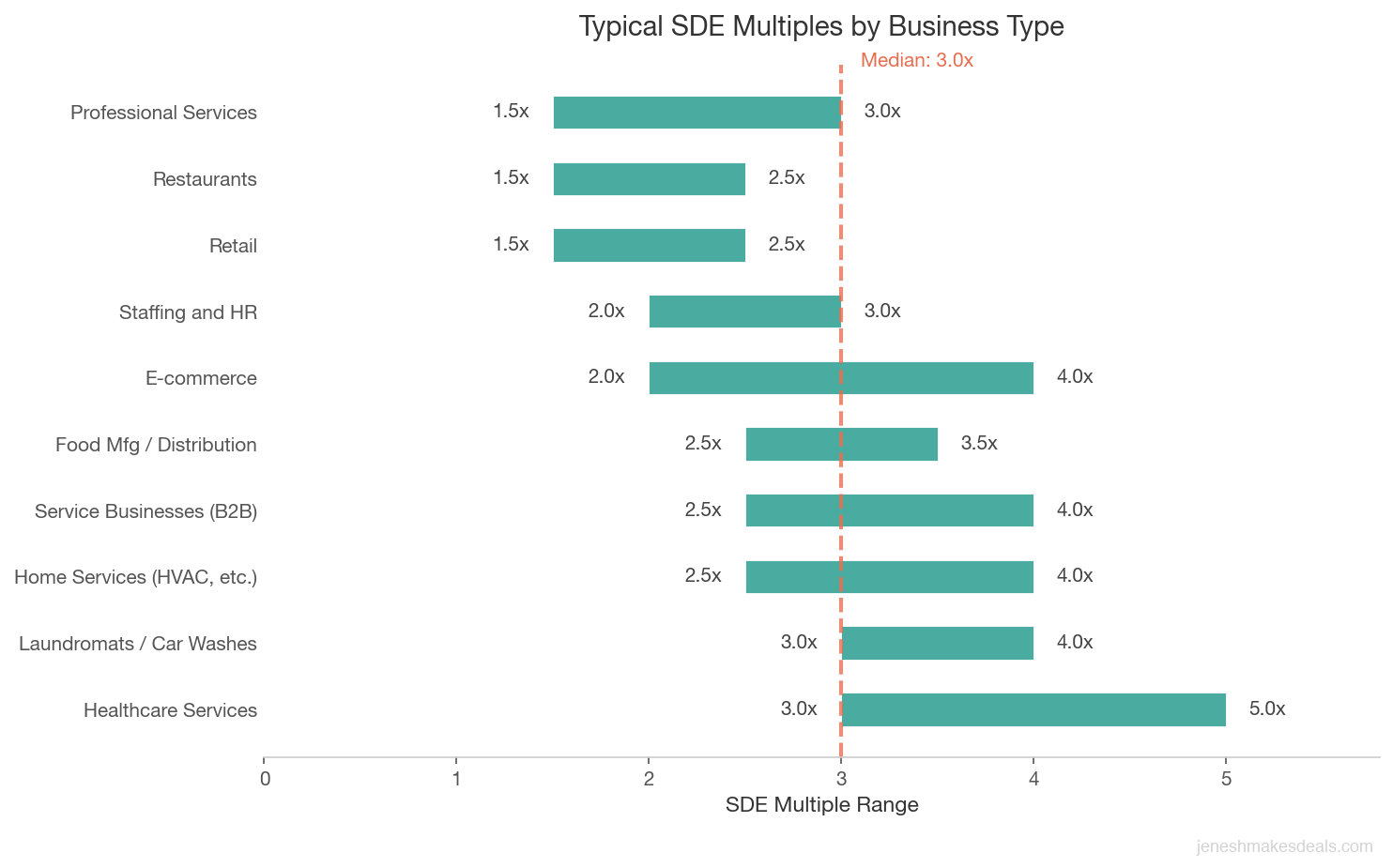

SDE Multiples by Business Type

Once you have SDE calculated, you apply a multiple to get to a valuation. The multiple varies by industry, business stability, growth trend, and risk factors. Here's a general reference:

| Business Type | Typical SDE Multiple | Notes |

|---|---|---|

| Service businesses (B2B) | 2.5x to 4x | Higher end for recurring contracts |

| Professional services (law, accounting, consulting) | 1.5x to 3x | Lower due to key person risk |

| Retail | 1.5x to 2.5x | Heavily dependent on lease terms |

| Restaurants | 1.5x to 2.5x | Higher end for well established, loyal customer base |

| Food manufacturing / distribution | 2.5x to 3.5x | |

| Healthcare services | 3x to 5x | High demand, recurring revenue |

| E-commerce | 2x to 4x | Depends heavily on traffic source reliability |

| Home services (HVAC, plumbing, landscaping) | 2.5x to 4x | Higher for businesses with service contracts |

| Laundromats / car washes | 3x to 4x | Strong for turnkey, stable cash flow |

| Staffing and HR | 2x to 3x | Client concentration matters a lot |

These are ranges, not fixed numbers. A service business at the bottom of its range might trade for 2.5x SDE because it's owner dependent and has no contracts. The same type of business with recurring revenues, multiple employees, and strong customer retention might trade at 4x or above.

For current multiples in your specific industry, read my guide on 2026 business valuation multiples by industry.

How Buyers Use SDE to Calculate Their Offer

When a buyer looks at a business, they're asking one core question: "Does this business generate enough money to pay my debt service, pay me a reasonable salary, and still leave a return on my investment?"

Here's how a buyer typically works through the math.

Starting with SDE of $357,400 (from our example above):

| Line Item | Annual Amount |

|---|---|

| SDE (total available to owner) | $357,400 |

| Minus: debt service ($1,072,200 at 6% for 10 years) | ($143,000) |

| Minus: buyer's replacement salary | ($80,000) |

| Remaining cash flow (return on investment) | $134,400 |

That $134,400 represents the buyer's return on their equity investment. Divided by the down payment (roughly $107,000 at 10%), that's a strong return.

If the SDE were inflated through questionable add-backs, the debt service would stay the same but the buyer would realize they can't actually service the debt and pay themselves. That's when deals collapse after closing, which is why sophisticated buyers scrutinize every add-back.

How SDE Affects Deal Economics at Different Levels

| SDE | Valuation (3x) | Annual Debt Service | Buyer Salary | Remaining Cash Flow |

|---|---|---|---|---|

| $200,000 | $600,000 | $80,000 | $65,000 | $55,000 |

| $300,000 | $900,000 | $120,000 | $75,000 | $105,000 |

| $357,400 | $1,072,200 | $143,000 | $80,000 | $134,400 |

| $500,000 | $1,500,000 | $200,000 | $90,000 | $210,000 |

Assumes 10% down, 6% interest, 10 year term. Buyer salary varies by deal size.

Thinking about financing your acquisition? Explore SBA and alternative loan options here to understand what loan structures are available for different deal sizes.

Why Inflated Add-Backs Kill Deals

This is the most important practical point in this entire post. Sellers who inflate their add-backs to pump up SDE almost always hurt themselves.

Here's what happens. The seller presents an inflated SDE. The business gets priced based on that number. A buyer makes an offer. Due diligence begins. The buyer's CPA reviews every add-back against actual expense records and tax returns. Buyers who have learned to read a P&L statement catch these discrepancies quickly. Savvy buyers know exactly what to look for in a small business, and verifying every add-back against tax returns is near the top of that list. Some of the claimed add-backs aren't documented. Some don't qualify. The real SDE comes out 20% lower than presented.

Now the buyer either walks away, comes back with a significantly lower offer, or demands a price reduction. The deal renegotiation is painful for everyone. Sellers who were honest from the start avoid this entirely.

SBA lenders add another layer. When you apply for an SBA loan, the lender does their own SDE analysis against your tax returns. If your SDE presentation doesn't match what the tax returns support, the lender's number wins. A deal that was priced at $1 million SDE might get financed only to $700,000 worth of transaction because the lender's SDE is lower.

Be honest about your add-backs. Document everything. Present only what you can prove. Sellers who do this close faster and with fewer headaches.

Every add-back you claim needs a paper trail. If you cannot prove it with a receipt, invoice, or tax return, assume the buyer's CPA will disallow it entirely.

Common Mistakes Sellers Make When Calculating SDE

Adding back the owner's entire compensation without separating salary from distributions. Only actual compensation (salary, guaranteed payments, and similar items) should be added back. Pure investment returns that the owner took as distributions are more complex and require CPA guidance.

Double-counting expenses. Some sellers add back depreciation and also add back the lease on a piece of equipment, when the lease is already reflected in the expense line. Make sure each add-back represents a real, non-duplicative expense.

Adding back recurring expenses as "one-time." If the same legal firm bills the business every year for ongoing compliance, that's not a one-time expense. It belongs in operating costs.

Normalizing rent paid to a related party without a real market analysis. If you own the building and the business pays you rent, you need an actual market comparison to determine what portion is above market. Claiming the entire rent payment as an add-back isn't appropriate.

Not removing the adjustment for an owner who will stay on. If the previous owner is staying on in a paid role post-closing, the add-back for their compensation should be partial, not full. The buyer is still paying someone to do that work.

Missing legitimate add-backs. On the other side, sellers sometimes forget to add back depreciation, the owner's retirement contributions, or personal auto expenses that were clearly business expenses. Leave money on the table by being too conservative.

SDE Calculation Quick Reference

| Do This | Do Not Do This |

|---|---|

| Add back all documented owner compensation (W-2, distributions) | Add back investment returns or passive income as "compensation" |

| Include depreciation and amortization as non cash add-backs | Double count depreciation and a lease on the same equipment |

| Add back one time legal fees that have concluded | Classify recurring annual legal costs as "one time" |

| Use a real market rent analysis for related party rent | Claim the entire rent payment to a related party as an add-back |

| Reduce the owner salary add-back if the owner stays after the sale | Add back the full salary when the owner will remain in a paid role |

| Provide receipts, invoices, and tax returns for every add-back | Present verbal explanations without supporting documentation |

The most expensive mistake sellers make is not double counting or inflating add-backs. It is missing legitimate ones entirely. Forgotten depreciation, retirement contributions, and personal auto expenses can leave tens of thousands of dollars on the table.

How to Document Your Add-Backs for Buyers

Every add-back you claim needs documentation. Not a verbal explanation. A paper trail.

Prepare an add-back schedule that lists each item, the dollar amount, and the supporting evidence. For each line:

- Owner salary: Copy of W-2 or payroll records

- Owner health insurance: Insurance invoice and business payment record

- Owner vehicle: Auto expense from the books matched to a specific vehicle registered personally to the owner

- Personal expenses: Credit card or expense report showing the item and its personal nature

- One-time legal fees: Invoice from the law firm and explanation of the matter that has concluded

- Depreciation: From the depreciation schedule on the tax return

Package this as a single document with supporting exhibits. When buyers and lenders ask for your SDE breakdown, you hand them this package. Every item is accounted for. Every claim is supported. This signals professionalism and speeds up the due diligence process considerably.

Sellers who can't produce documentation for their add-backs should expect buyers to discount or disallow them entirely.

Ready to prepare your business for sale? Before you go to market, take the time to prepare your financials properly. Clean, well documented books make every part of the sale process faster. Contact me here for a consultation on how to present your financials in the strongest possible way.

Next Steps

If you're a seller, start by pulling three years of tax returns and P&Ls and calculating SDE for each year using this methodology. Consistency across years is important. Buyers will want to see the trend.

If you're a buyer, the first thing to do with any business you're evaluating seriously is reconstruct the SDE yourself from the underlying financials. Don't just accept the seller's number. Go through every add-back with your CPA and verify it against actual records.

Both buyers and sellers benefit from having a qualified CPA involved in the SDE analysis before any serious negotiations begin. The accountant who does your personal taxes is probably fine for basic bookkeeping. A CPA who specializes in business transactions and can prepare a quality of earnings report is worth the investment.

Frequently Asked Questions

Is SDE the same as owner's benefit?

Essentially yes. "Owner's benefit," "owner's cash flow," and "seller's discretionary earnings" all refer to the same concept: total financial benefit to the owner/operator. The terms are used interchangeably in small business transactions.

Does SDE include the buyer's salary?

No. The owner's compensation is added back to reflect that the new owner will be the operator. The buyer's expected salary is then factored into debt service analysis, but it's not part of the SDE number itself.

Should I calculate SDE before or after taxes?

SDE is calculated before income taxes, using net income (or pre-tax income) as the starting point. Federal and state income taxes on business income are typically added back as part of the SDE analysis for pass-through entities.

What if the business has multiple owners?

Add back all working owners' compensation. If two partners each take $80,000, you add back $160,000. If one partner is a silent investor and doesn't work in the business, their distributions aren't typically added back as compensation.

Can SDE be negative?

Yes. If the business is losing money and the add-backs don't overcome the losses, SDE can be negative. This doesn't necessarily mean the business is worthless, but it means it can't be valued on an SDE multiple basis. The valuation would need to look at asset value, turnaround potential, or other factors.

What's the difference between SDE and cash flow?

SDE is a normalized earnings figure. Actual cash flow can differ due to working capital changes, capital expenditures, and debt payments. SDE tells you the earnings power. Free cash flow to equity tells you the actual cash available after reinvestment and debt service. Both numbers matter in evaluating an acquisition.

Planning to sell? Download our free Complete Guide to Selling Your Business in 2026 for a step by step walkthrough of the entire process, from valuation to closing.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.