I've covered what earnouts are and whether you should accept one in a separate post. If you haven't read that yet, start there. It explains the basics: what an earnout is, why buyers propose them, the control problem, and when it makes sense to accept one.

This post is different. This is about the mechanics. You've already decided an earnout will be part of your deal. Now you need to structure it so both sides feel protected, the terms are enforceable, and you don't end up in litigation 18 months from now arguing about how to calculate EBITDA.

I've brokered deals where a well structured earnout saved a transaction that would have died over a valuation gap. I've also seen deals where a sloppy earnout turned two reasonable people into adversaries. The difference almost always comes down to how carefully the terms were built.

Choosing the Right Performance Metric

The metric you tie the earnout to is the single most important structural decision. Get this wrong and everything else in the agreement is noise.

There are four common metrics. Each has real tradeoffs.

| Metric | Best For | Pros | Cons |

|---|---|---|---|

| Gross Revenue | Service businesses, agencies, SaaS | Hardest to manipulate, simplest to verify, minimal accounting judgment | Ignores profitability; seller gets paid even if margins collapse |

| Gross Profit | Retail, distribution, manufacturing | Captures margin quality, harder to game than EBITDA | Requires agreed upon cost of goods definitions; some room for allocation games |

| EBITDA | Larger deals ($2M+), PE acquisitions | Reflects true business performance, aligns with standard valuation methods | Highly susceptible to expense manipulation by buyer; complex accounting definitions |

| SDE | Owner operated businesses under $2M | Matches how the business was valued at sale | Requires agreement on add backs; buyer may argue different add back treatment |

Here's my rule of thumb. If you're the seller, push for gross revenue. It's the cleanest metric. The buyer can't reduce your payout by hiring extra staff, raising executive salaries, or reclassifying expenses. Revenue either came in or it didn't.

If you're the buyer, you probably want EBITDA or gross profit because you don't want to pay an earnout on revenue that doesn't produce profit. That's a fair concern. The compromise I recommend most often is gross profit with a clearly defined cost of goods schedule attached as an exhibit to the purchase agreement.

One thing both sides should agree on: never use net income as an earnout metric. There are too many variables, including interest, taxes, depreciation schedules, and amortization of goodwill, that make net income unreliable and easy to dispute.

The metric you choose determines who controls the outcome. Revenue is the seller's friend because it's nearly impossible for a buyer to suppress top line numbers without obviously damaging the business. EBITDA is the buyer's friend because they control the expense side. Pick the metric that reflects the trust level between both parties.

Setting Realistic Targets Based on Historical Performance

The earnout target needs to be grounded in what the business has actually done, not what either party hopes it will do.

I see this mistake constantly. A buyer proposes an earnout target that requires 20% revenue growth when the business has grown 5% per year for the past three years. The seller signs it thinking "the business has momentum." Then reality kicks in and the seller earns nothing.

Here's how to set targets that are fair to both sides.

Start with the trailing three year average. If the business generated $1.8 million, $1.9 million, and $2.0 million in revenue over the past three years, your baseline is about $1.9 million. Any target at or below $1.9 million is essentially asking the business to maintain performance. Anything above is asking for growth.

Cap the growth expectation. If historical growth has been 5% to 7% annually, an earnout target requiring 15% growth is unreasonable. I generally tell sellers not to accept targets that require growth more than 1.5 times the historical rate. So if growth has been 6%, don't accept a target that requires more than 9%.

Use trailing twelve month (TTM) data, not annual fiscal year. Fiscal year data can be distorted by seasonality, one time events, or timing issues. TTM data from the twelve months immediately before closing gives you a cleaner picture.

Agree on adjustments for known changes. If a major customer contract is expiring, or the business just landed a large new account, both parties should agree on how to treat these in the baseline. Don't leave this to interpretation later.

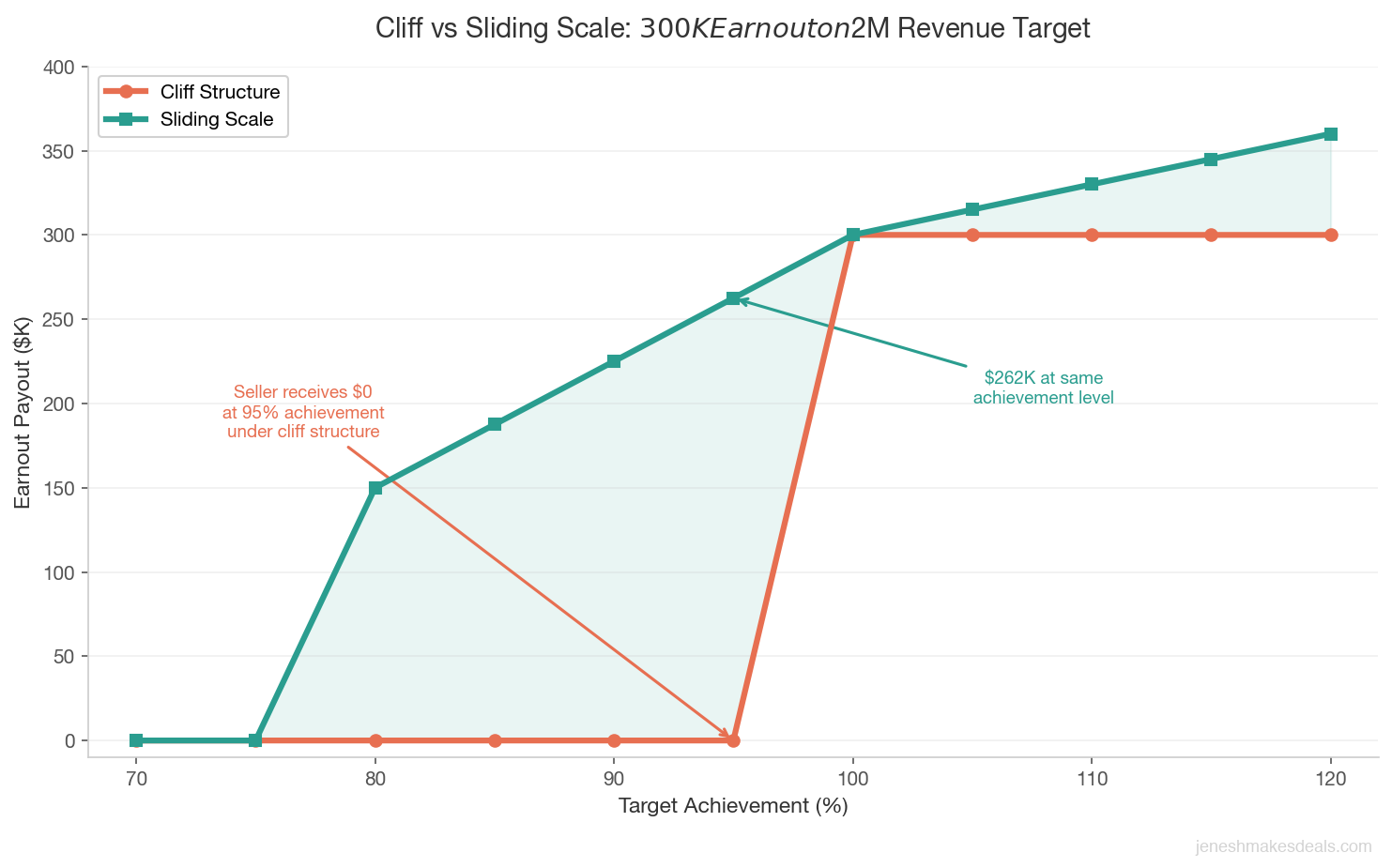

Build a sliding scale, not a cliff. This is critical. A cliff structure pays nothing unless the seller hits 100% of target. A sliding scale pays proportionally. Here's how the math works for a $300,000 earnout with a $2 million revenue target:

| Achievement | Cliff Structure Payout | Sliding Scale Payout |

|---|---|---|

| 80% ($1.6M) | $0 | $150,000 |

| 85% ($1.7M) | $0 | $187,500 |

| 90% ($1.8M) | $0 | $225,000 |

| 95% ($1.9M) | $0 | $262,500 |

| 100% ($2.0M) | $300,000 | $300,000 |

| 110% ($2.2M) | $300,000 | $330,000 (with cap at $360,000) |

The sliding scale starts at 50% payout for 80% achievement, then scales linearly. Notice I also included upside: if the seller exceeds the target, they earn more, up to a cap. This is fair to both parties. The seller gets rewarded for outperformance, and the buyer knows their maximum exposure.

If you're a seller being offered a cliff structure, push back. Hard. Cliff earnouts are the single biggest source of $0 payouts in small business deals.

I've seen sellers walk away from hundreds of thousands of dollars because their earnout missed the target by 3%. A sliding scale starting at 80% achievement would have paid them the majority of what they earned. If a buyer insists on a cliff structure, that tells you something about their intentions. Treat it as a red flag.

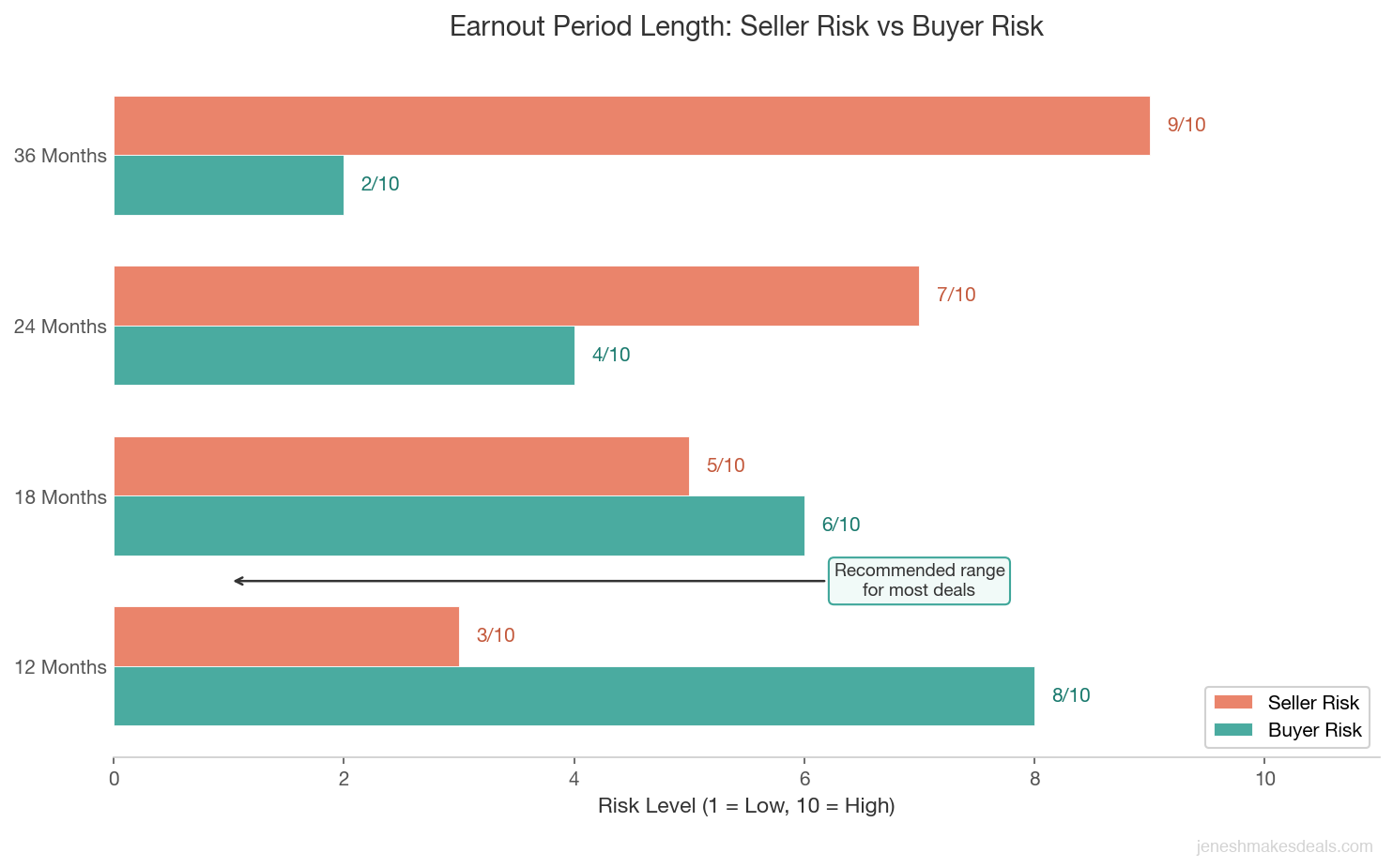

Determining the Earnout Period

The length of the earnout period affects risk, measurement accuracy, and the seller's ability to move on. There's no perfect length, but there are clear tradeoffs.

| Period | Seller Risk | Buyer Risk | Best For |

|---|---|---|---|

| 12 months | Lower; less time for buyer to change operations | Higher; short runway to prove sustainability | Revenue based earnouts, strong historical performance |

| 18 months | Moderate | Moderate | Compromise position; covers seasonal cycles |

| 24 months | Higher; significant post sale commitment | Lower; more data points, more confidence | Businesses with long sales cycles or annual contracts |

| 36 months | Highest; seller tied to business for years | Lowest; maximum downside protection | Only justified for very large earnout components or businesses with major concentration risk |

My recommendation: push for 12 months if you're the seller. Accept 18 to 24 months only if the earnout represents a large percentage of total deal value (over 25%) and the buyer has legitimate reasons for needing more time, such as a business with annual contract renewals that need to be tested.

I almost never recommend 36 month earnouts. Three years is a long time. The buyer will make dozens of operational decisions that affect your numbers. Management transitions, technology changes, market shifts. By year three, the business barely resembles what you sold.

One structural option that works well: split the earnout into annual measurement periods. Instead of one $300,000 earnout measured after 24 months, structure it as two $150,000 earnouts measured after 12 months and 24 months respectively. This gives the seller earlier payouts and creates natural checkpoints.

Payment Schedules and Timing

When and how the earnout money moves matters almost as much as how much it is.

Measurement windows. Define exactly when the measurement period starts and ends. I recommend the measurement period begin on the first day of the month following closing. If you close on March 15th, the 12 month measurement period runs April 1st through March 31st of the following year. This avoids partial month complications.

Calculation period. After the measurement period ends, the buyer needs time to compile financials. Give them 60 days. No more. Some buyers try for 90 or 120 days, which means the seller doesn't know their payout for months after the earnout period ends. Sixty days is sufficient.

Payment timing. The earnout should be paid within 30 days after the calculation period closes. So for a 12 month earnout starting April 1st, the timeline looks like this:

- April 1, 2026 to March 31, 2027: Measurement period

- April 1 to May 31, 2027: Buyer prepares earnout calculation

- June 1, 2027: Buyer delivers calculation to seller

- June 30, 2027: Earnout payment due if calculation is undisputed

Interim payments. For longer earnout periods, I strongly recommend quarterly or semi annual interim payments. If the earnout is based on annual revenue, pay out earned amounts quarterly based on actual revenue to date. This reduces the seller's credit exposure and keeps both sides aligned.

Escrow. The gold standard is placing the maximum earnout amount in third party escrow at closing. Funds are released to the seller as targets are met, or returned to the buyer if not. Buyers resist escrow because it ties up capital, but from a seller's perspective, an unescrowed earnout is just a promise.

Ready to figure out how deal structure affects your total proceeds? Use our business valuation calculator to model different scenarios.

Protecting the Seller with Operating Covenants

Operating covenants are the clauses that restrict what the buyer can do during the earnout period. They exist to prevent the buyer, intentionally or not, from making decisions that tank the seller's earnout.

Without these protections, the earnout is essentially a bet on a stranger's management skills. Here are the covenants I recommend for sellers.

Maintain consistent accounting methods. The buyer must use the same revenue recognition, expense classification, and accounting standards that were in place at closing. No switching from accrual to cash basis. No changing how deferred revenue is recognized. This single covenant prevents the most common earnout disputes.

No customer redirection. If the buyer operates other businesses, they cannot move customers or revenue from the acquired entity to other operations. This is especially important in roll up acquisitions where the buyer is consolidating multiple businesses.

Staffing minimums. The buyer must maintain key positions (sales manager, account managers, operations lead) throughout the earnout period. If a critical employee leaves, the buyer must fill the position within 60 days. You can tie this to specific named individuals or to role requirements.

Pricing floors. The buyer cannot reduce pricing by more than a defined percentage (I recommend 10%) without the seller's written consent. This prevents a buyer from slashing prices to drive volume at the expense of margin, which destroys EBITDA based earnouts.

Marketing spend minimums. If the business relies on paid marketing, require the buyer to maintain at least 80% of the trailing twelve month marketing spend. A buyer who cuts the marketing budget will see leads drop, which drops revenue, which drops your earnout.

No entity restructuring. The buyer cannot merge, dissolve, or reorganize the acquired entity during the earnout period. If the business gets folded into a larger operation, it becomes impossible to track standalone performance.

Operate in good faith. This is the catch all. The buyer must operate the business in a manner consistent with past practice and not take actions whose primary purpose is to reduce the earnout obligation. Courts have upheld this kind of language, but it's stronger when paired with the specific covenants above.

Operating covenants are the difference between an earnout that works and one that ends in litigation. I tell every seller: if the buyer pushes back on reasonable covenants, ask yourself why. A buyer who plans to run the business honestly has no reason to resist protections that simply require them to keep doing what the business was already doing.

What the Buyer Should Require

Earnout structuring isn't just about protecting sellers. Buyers have legitimate interests too, and a well structured earnout accounts for both sides.

Seller transition commitment. Require the seller to stay involved for 6 to 12 months full time, with a consulting arrangement for the remainder. If the seller doesn't honor transition obligations, the buyer should have the right to reduce the earnout proportionally.

Non compete and non solicitation. The seller should be restricted from competing or soliciting customers and employees during the earnout period. If you're the seller, this is reasonable. You can't take your customers and then complain the target wasn't met.

Cap on earnout exposure. Set a hard cap on total payout. If the earnout includes an upside kicker, cap it at 120% of the base amount. On a $300,000 earnout, the buyer's maximum exposure would be $360,000.

Knowledge transfer schedule. Build specific milestones for handing off customer relationships, vendor contacts, and operating procedures. The seller must also cooperate with reasonable reporting requests during the measurement period.

Thinking about how to structure your next deal? Contact us for a confidential conversation about your situation.

Dispute Resolution Mechanisms

Even a well drafted earnout will occasionally produce disagreements. The resolution process needs to be defined in advance. Trying to figure this out after a dispute starts is expensive and adversarial.

Here's the three tier process I recommend.

Tier 1: Direct negotiation (30 days). When the buyer delivers the earnout calculation, the seller has 30 days to review and either accept or deliver a written objection. If the seller objects, both parties have 30 days to negotiate directly and attempt to resolve the disagreement. Most disputes that get resolved do so at this stage.

Tier 2: Independent accountant (30 to 60 days). If direct negotiation fails, an independent CPA firm reviews the disputed calculation. Both parties submit their positions. The accountant issues a binding determination that must fall within the range of the two positions. The cost gets allocated based on the outcome: whoever's position was further from the final number pays. This incentivizes both sides to be reasonable.

Tier 3: Arbitration. For disputes that can't be resolved by an accountant (such as allegations of covenant violations or bad faith), the agreement should provide for binding arbitration with a single arbitrator experienced in M&A disputes. Arbitration is faster and less expensive than litigation, and it's private. Specify the arbitration rules (AAA or JAMS) and the venue.

What to avoid. Don't leave dispute resolution to general litigation in state court. Business sale disputes that end up in court take 18 to 36 months, cost $50,000 to $200,000 in legal fees per side, and produce unpredictable results. An accountant determination and arbitration process costs a fraction of that.

Acceleration and Kill Clauses

These are the clauses that address what happens when the earnout is going off the rails, either because the seller is overperforming or because the buyer has fundamentally changed the business.

Acceleration Clauses (Seller Protection)

An acceleration clause allows the seller to receive the full remaining earnout immediately if certain trigger events occur.

Change of control. If the buyer sells the business to a third party during the earnout period, the seller's remaining earnout should accelerate and be paid in full at closing of the subsequent sale. The logic: the seller agreed to earn out based on this buyer's management. A new buyer changes the equation entirely.

Material breach of operating covenants. If the buyer violates the staffing minimums, redirects customers, or changes accounting methods in violation of the agreement, the seller should have the right to accelerate the full earnout. This is the enforcement mechanism that gives covenants teeth.

Business dissolution or bankruptcy. If the buyer's entity files for bankruptcy or ceases operations during the earnout period, the remaining earnout accelerates and becomes a priority claim.

Kill Clauses (Buyer Protection)

A kill clause allows the buyer to terminate the earnout obligation under specific circumstances.

Seller breach of non compete. If the seller competes with the business during the earnout period, the buyer should have the right to terminate the remaining earnout obligation entirely.

Seller failure to perform transition duties. If the seller agreed to stay involved and fails to fulfill their transition obligations (walks away, becomes unresponsive, refuses to make introductions), the buyer should have the right to reduce or eliminate the remaining earnout.

Force majeure. A pandemic, natural disaster, or regulatory change that fundamentally disrupts the business's ability to perform should give both parties the right to renegotiate the earnout terms. This clause got a lot of attention after 2020 for obvious reasons.

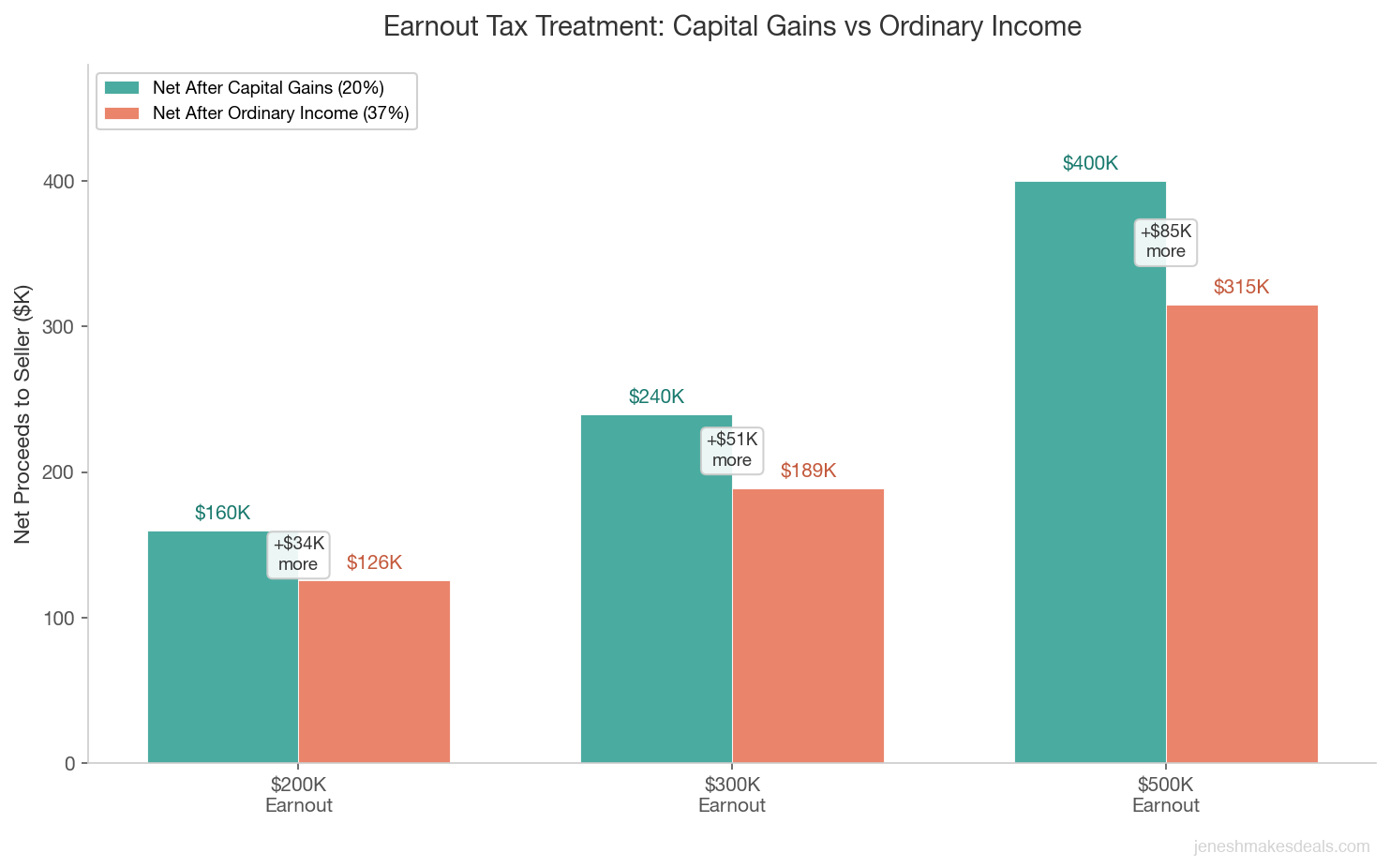

Tax Treatment of Earnouts

Taxes are one of the most overlooked aspects of earnout structuring, and they can meaningfully change how much the seller actually keeps.

For sellers. Earnout payments can be taxed as capital gains or ordinary income depending on how the purchase agreement characterizes them. If the earnout is structured as additional purchase price, it's typically taxed at long term capital gains rates (currently 20% federal for high earners). If it's structured as compensation for services (like a consulting arrangement), it's taxed at ordinary income rates (up to 37% federal).

The difference on a $300,000 earnout is significant:

| Tax Treatment | Federal Rate | Tax on $300,000 | Net to Seller |

|---|---|---|---|

| Capital gains | 20% | $60,000 | $240,000 |

| Ordinary income | 37% | $111,000 | $189,000 |

That's $51,000 more in the seller's pocket from capital gains treatment. State taxes add another layer.

For buyers. Buyers generally prefer to characterize earnout payments as compensation because it's deductible as a business expense. Capital gains treatment for the seller means the buyer doesn't get to deduct the payment.

This creates a natural tension. The purchase agreement needs to explicitly state the tax characterization, and both parties' tax advisors need to review it before signing.

Other tax considerations. The IRS may allow installment sale reporting, where you report gain as you receive payments rather than all at closing. If payments are deferred more than one year, the IRS may also impute interest, converting part of your capital gains into ordinary income. Don't finalize any earnout without having your tax advisor model the specific numbers. For a broader view, this guide on tax implications of selling a business covers the major areas.

Worked Examples: Two Earnout Structures Compared

Let me walk through two scenarios so you can see how structural choices produce different outcomes.

Example 1: Revenue Earnout (Service Business)

Deal: Seller sells a digital marketing agency for $1.5 million. Buyer pays $1.15 million at closing.

Earnout: $350,000 tied to gross revenue over 12 months.

- Target: $1.2 million (matches TTM revenue, no growth required)

- Scale: Linear from 80% ($960,000) to 110% ($1.32 million)

- Floor payout at 80%: $175,000. Cap at 110%: $385,000

- Quarterly installments. $350,000 in escrow

If revenue hits $1.08 million (90%): Seller receives $262,500. Revenue is clean and hard to manipulate. The 12 month period limits exposure. Escrow eliminates credit risk.

Example 2: EBITDA Earnout with Protections (Manufacturing)

Deal: Seller sells a light manufacturing company for $4.2 million. PE buyer pays $3.0 million at closing.

Earnout: $1.2 million tied to adjusted EBITDA over 24 months, measured annually.

- Year 1 target: $850,000 EBITDA. Year 2 target: $900,000

- $600,000 per year. Scale: Linear from 80% to 120%

- "Adjusted EBITDA" defined in a 4 page exhibit with every add back, expense category, and accounting method specified

- Covenants: maintain production staff, no facility relocation, marketing spend within 15% of trailing average, no management fees or intercompany charges, no customer transfers

- Acceleration: full payout if buyer sells entity or breaches material covenants

- Named CPA firm for dispute resolution within 45 days

If Year 1 EBITDA is $790,000 (93%) and Year 2 is $870,000 (97%): Total earnout is $1,042,500 out of $1.2 million. The covenant package restricts expense manipulation, and the named CPA firm means disputes get resolved fast.

Want to model how an earnout affects your deal value? Try our valuation calculators to run the numbers.

Common Structuring Mistakes That Lead to Litigation

I've seen these patterns produce lawsuits, arbitration claims, and destroyed relationships between buyers and sellers. Avoid all of them.

Undefined accounting terms. The agreement says "revenue" without specifying cash basis, accrual, or GAAP. The buyer switches methods and $150,000 in recognized revenue disappears. Lawsuit.

No restriction on related party transactions. The buyer charges "management fees" to their holding company. EBITDA drops. The seller gets a smaller earnout. Arbitration.

Earnout measured on a combined entity. The buyer merges the business into their existing operation. No separate P&L exists anymore. Nobody can agree which revenue belongs where. Litigation.

No interim reporting. The seller sees no financial data until the final calculation 14 months after closing. The numbers don't match expectations, but the seller has no records to challenge them.

Vague good faith language without specific covenants. The agreement says "good faith" but doesn't define it. The buyer makes aggressive cost cuts. The court says buyer's actions were within their discretion. Seller loses.

No acceleration on change of control. The buyer sells the business 8 months in. The new owner has no obligation under the earnout. The seller's remaining payout becomes unenforceable.

Oral side agreements. Buyer and seller verbally agree to terms that never make it into the written contract. The integration clause supersedes everything. Seller has no recourse.

Every one of these mistakes is preventable with proper drafting. An experienced M&A attorney should review every earnout agreement before it's signed.

Your Earnout Structuring Checklist

Before you sign, make sure you've addressed every item on this list.

- Metric defined in precise detail with exhibit attached

- Target based on historical performance with sliding scale

- Measurement period start and end dates specified

- Payment timing with calculation delivery date and payment due date

- Escrow or alternative credit protection for the seller

- Operating covenants covering accounting, staffing, pricing, and customer redirection

- Seller obligations with clear transition duties and reasonable non compete

- Acceleration triggers on change of control or material covenant breach

- Kill clauses protecting the buyer if the seller competes or abandons duties

- Dispute resolution with three tier process: negotiation, accountant, arbitration

- Tax treatment reviewed by both parties' advisors and stated in the agreement

If the answer to any of these is "no" or "I'm not sure," you're not ready to sign.

Need help evaluating or structuring an earnout? Get in touch for a free consultation. I'll walk you through the numbers and help you understand what you're actually agreeing to.

Frequently Asked Questions

Should the seller or buyer propose the earnout structure?

The buyer usually proposes the initial structure in their offer or letter of intent. The seller then negotiates. I recommend sellers prepare a counter structure in advance with their preferred metric, target range, measurement period, and required covenants. Being prepared gives you a significant advantage over reacting to the buyer's terms.

Can earnout terms be renegotiated after signing the LOI?

Yes. The LOI typically outlines the earnout in general terms, but the detailed provisions get negotiated during the definitive purchase agreement phase. That's where the metric exhibit, operating covenants, dispute resolution, and acceleration clauses are finalized. Push for as much specificity in the LOI as possible so there are fewer surprises later.

How do earnouts work with SBA loans?

SBA lenders treat earnout payments as part of the purchase price, but because they're contingent, the SBA may not count the full earnout when sizing the loan. The seller might need to accept a lower base price or the buyer might need more equity. If SBA financing is involved, get the lender's input on the earnout structure early.

Is an earnout better than seller financing for bridging a valuation gap?

For sellers, seller financing is almost always preferable. A seller note is a debt obligation owed regardless of business performance. An earnout is contingent on hitting targets. If you have a choice between a $300,000 seller note at 6% interest and a $300,000 revenue earnout, the note is safer. The exception: when you genuinely believe the business will outperform and an uncapped earnout gives you more upside.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

April 20, 2026

Strategic Buyer vs Financial Buyer: Which Is Right for Your Business Sale?

Strategic and financial buyers value businesses differently. Here's how to decide which type of buyer gets you the best deal.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.