The moment a buyer gets serious about your business, they ask for financials. Not a brochure. Not a tour. Financials.

And here's the thing: most small business owners are not ready for that moment. Their books have years of mixed personal and business expenses. Their tax returns tell a different story than their P&Ls. Their add-backs are scattered across spreadsheets nobody else can follow. What looks profitable in their heads becomes impossible to verify on paper.

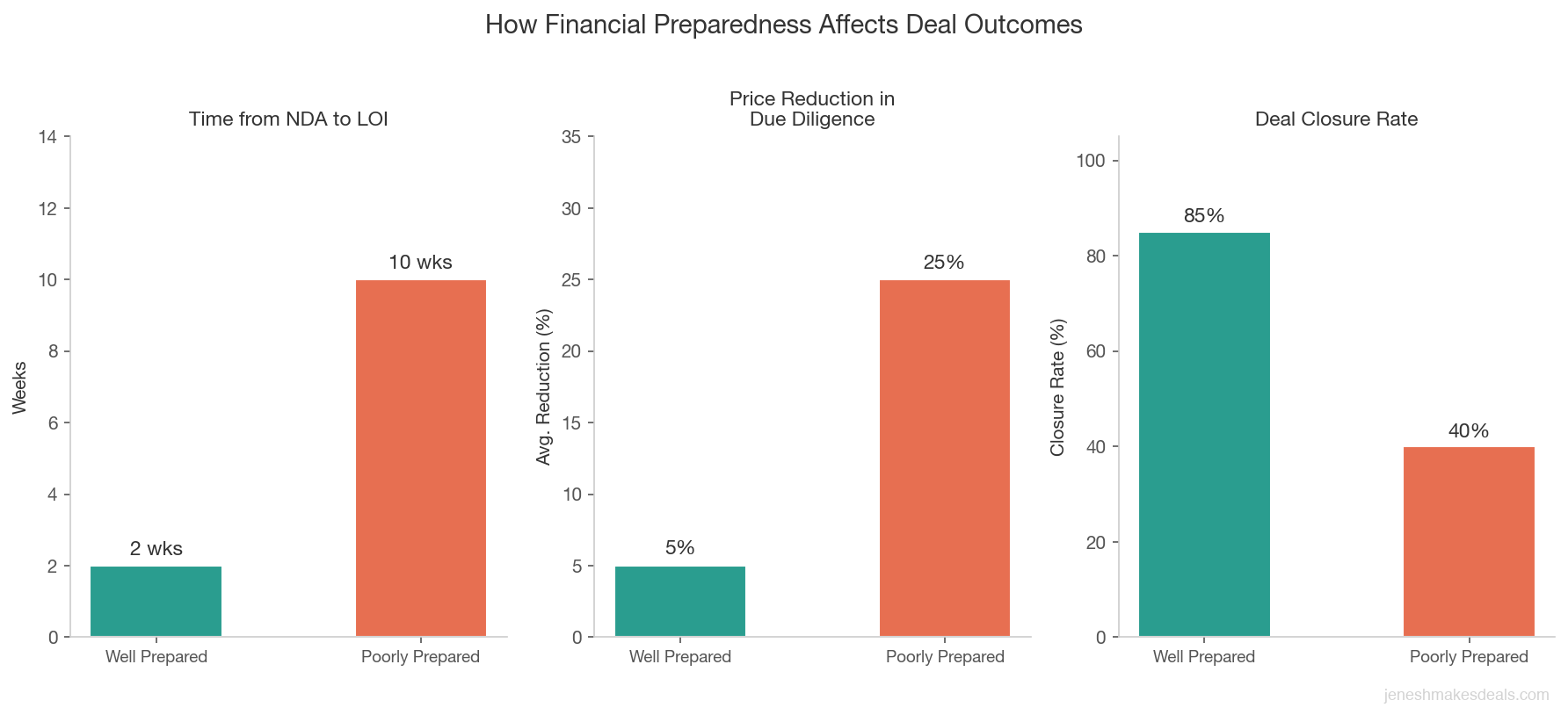

I've watched deals fall apart, prices get cut by 20 to 30%, and closings get delayed by months, all because a seller's financials weren't prepared properly. The business was good. The numbers just couldn't prove it.

This guide will walk you through exactly what to do to get your financials sale-ready, whether you're going to market in six months or three years from now.

Why Your Financials Are the First Thing Buyers Scrutinize

Buyers are not buying your story. They're buying a financial asset. Everything they want to know about your business, whether it's actually profitable, whether the revenue is real, whether there are hidden risks, flows through the financial statements.

In my experience, buyers who walk away from a deal they were excited about almost always cite financial issues. Sometimes it's outright problems, like revenue that dropped unexpectedly or undisclosed liabilities. More often, it's just messiness. Books that don't reconcile. Expenses that can't be explained. Tax returns that don't match QuickBooks. Buyers interpret messiness as risk. Risk kills deals or drives prices down.

The inverse is also true. When a seller presents clean, organized, well-documented financials with a clear add-back schedule and three years of consistent trends, buyers gain confidence. That confidence translates directly into price. I've seen buyers stretch on valuation for sellers with excellent books because the clean financials reduced the buyer's perception of risk.

Prepare your financials as if every number will be challenged by a skeptical CPA, because it will be.

Buyers interpret messy financials as risk. Risk kills deals or drives prices down by 20 to 30%. Clean books signal confidence, and confidence translates directly into a higher sale price.

Three Years of Clean P&Ls: What "Clean" Actually Means

Every buyer will ask for three years of profit and loss statements. Not one year. Not a summary. Three full years, month by month if possible.

"Clean" means specific things. It doesn't just mean "organized." Here's what buyers and their CPAs are looking for:

Revenue Is Documented and Consistent

Clean revenue means every sale is recorded, every payment is deposited, and the total ties to your bank statements and tax returns. There should be no material cash sales that appear in your books but not on your returns. No revenue being counted in multiple periods. No large "other income" categories with no explanation.

Buyers will look at revenue trends across all three years. Growing revenue tells a story. Volatile revenue raises questions. Declining revenue requires a strong explanation. Understand your own trend before a buyer asks about it.

Expenses Are Categorized Properly

Every expense should be categorized in a way that makes logical sense. Payroll in payroll. Rent in rent. Marketing in marketing. When expenses are miscategorized or dumped into catch-all accounts like "general and administrative," buyers have to go through every transaction to understand what the business actually costs to run. That's time and effort they view as risk.

If your bookkeeping software has categories set up from years ago that don't make sense anymore, clean them up before you go to market. It's worth the time.

There Are No Unexplained Swings

A month where revenue doubles with no explanation is a red flag. An expense that appears once for $80,000 and never again needs an explanation. Unusual items should be noted and explained in writing as part of your financial package.

Getting Your Tax Returns in Order

Your tax returns are the most credible financial document you have. They're prepared by a professional, filed with the government, and carry legal weight. Buyers and SBA lenders put significant weight on them, specifically because they're harder to manipulate than internal bookkeeping.

The problem is that many small business owners optimize their tax returns for minimum tax liability, which often means showing as little income as possible. That's completely legitimate for tax purposes. But when you go to sell, the IRS-reported income is used to validate your SDE and your asking price.

The Returns Have to Match the P&Ls

This is where a lot of sellers get into trouble. Their P&L shows $400,000 SDE, but their tax return shows $60,000 in net income. The gap is explainable through add-backs, but if those add-backs aren't clearly documented and reconcilable, the buyer's lender will use the tax return number. Suddenly your business is worth much less.

The solution is a formal SDE reconstruction that bridges your tax return to your claimed SDE. Every add-back is listed, the dollar amount is specified, and the source document is referenced. Start here before you do anything else.

Your tax returns are the single most credible financial document in a deal. If your P&L shows $400,000 in SDE but your tax return shows $60,000 in net income, you need a formal SDE reconstruction that bridges that gap with documented add-backs, or the lender will use the tax return number.

Use the Same Accountant for Business and Personal if Possible

When the business tax returns and owner's personal returns are prepared by the same accountant, the compensation flow is easier to trace and verify. Buyers and lenders can see exactly what the owner took out of the business in each form, salary, distributions, and benefits.

If your tax returns are prepared by someone who doesn't fully understand the business, consider switching to a CPA who specializes in small businesses before you go to market.

File Amended Returns if There Are Errors

Some sellers discover errors in prior returns during the financial preparation process. File amended returns before you go to market. Errors that come out during due diligence create serious doubt about everything else in the financials.

Separating Personal Expenses from Business Expenses

This is the most common financial problem I see in small business sales, and it's also the most avoidable. Business owners, especially sole proprietors and single-member LLC owners, routinely pay personal expenses through the business. Cell phones, vehicle payments, health insurance, meals, even home expenses run through the business account.

This is fine from a tax perspective if it's done correctly. But for a sale, it creates two problems. First, it makes your P&L look messier than it needs to be. Second, it muddies the water on which expenses are real business costs and which are owner perks.

Separating Before You List

Ideally, start separating personal and business expenses 12 to 24 months before you list. Open a dedicated personal account for personal expenses. Pay yourself a W-2 salary and use that for personal spending. Keep the business accounts strictly for business expenses.

The cleanest P&L possible is one where every expense line item is a genuine cost of running the business, with owner compensation appearing as a single, clearly labeled salary line. That's easy for a buyer to understand and verify.

If you can't separate cleanly before you sell, at minimum document every personal expense in your books with a note flagging it as an add-back. "Cell phone (personal use, add-back)" labeled right in the bookkeeping system.

Start separating personal and business expenses 12 to 24 months before you list. The cleanest P&L is one where every expense line item is a genuine cost of running the business, with owner compensation appearing as a single, clearly labeled salary line.

Want a realistic sense of what your business is worth right now? Try our free valuation calculator based on your current SDE.

Documenting Add-Backs Properly

Add-backs are legitimate adjustments that represent expenses specific to the current owner's situation, not the cost of running the business under new ownership. But they have to be documented. Claims without documentation don't survive due diligence.

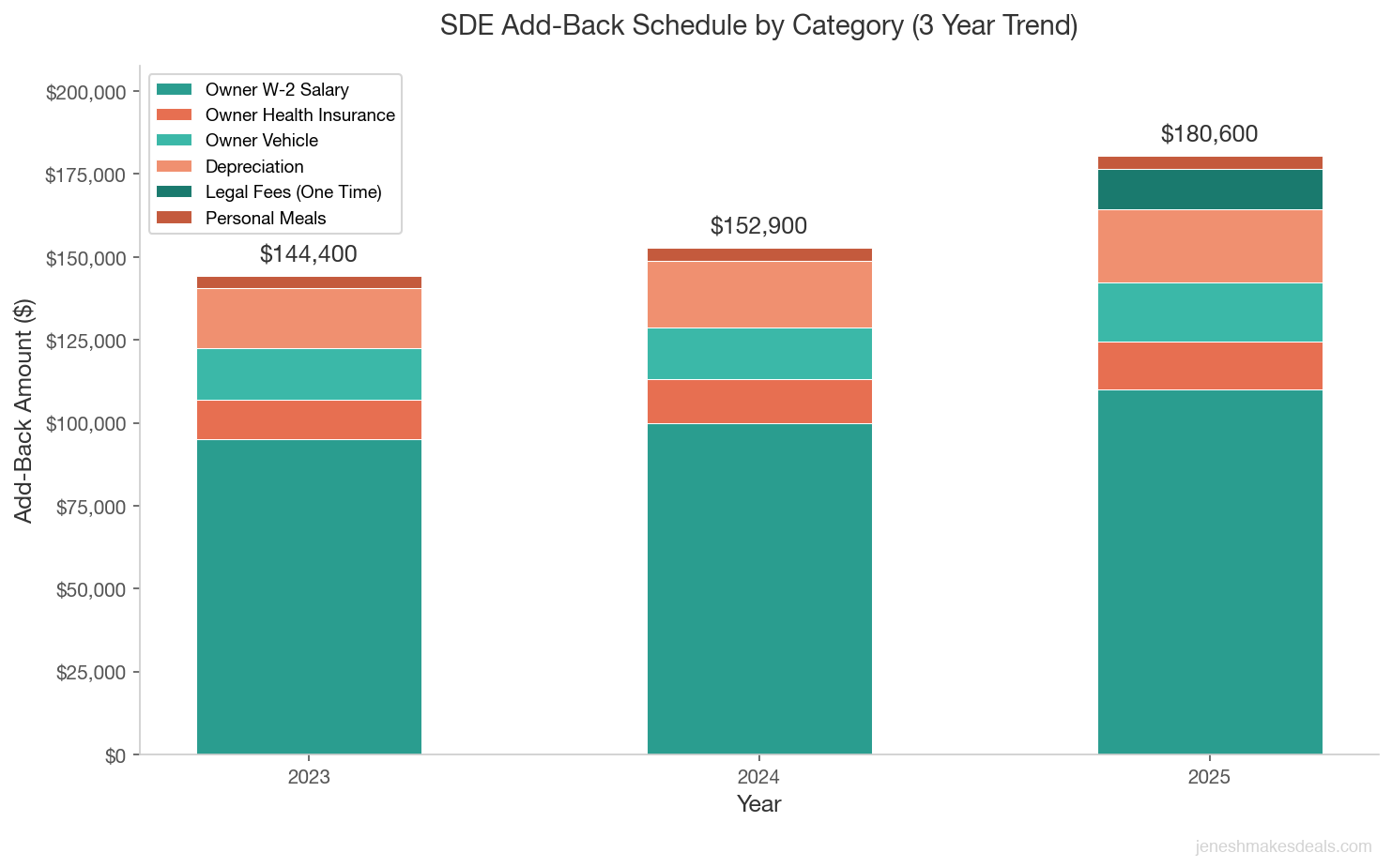

The Add-Back Template

Prepare a separate add-back schedule using this format:

| Item | Description | 2023 | 2024 | 2025 | Documentation |

|---|---|---|---|---|---|

| Owner W-2 salary | Annual compensation per W-2 | $95,000 | $100,000 | $110,000 | W-2 / Payroll records |

| Owner health insurance | Health/dental premiums paid by business | $12,000 | $13,200 | $14,400 | Insurance invoices |

| Owner vehicle | Personal vehicle lease on books | $15,600 | $15,600 | $18,000 | Lease agreement, vehicle registration |

| Depreciation | Non-cash charge per tax return | $18,000 | $20,000 | $22,000 | Tax return schedule |

| Legal fees (one-time) | Dispute with contractor, now resolved | $0 | $0 | $12,000 | Invoice, resolution docs |

| Personal meals/entertainment | Owner personal meals on business card | $3,800 | $4,100 | $4,200 | Expense detail |

| Total Add-Backs | $144,400 | $152,900 | $180,600 |

This kind of organized schedule tells buyers and lenders exactly what you're claiming and where to find the proof. Without it, add-backs become a negotiation that slows down the deal and often ends with buyers discounting your SDE.

Every add-back needs a paper trail. "Trust me, that was personal" does not survive due diligence. List the item, the dollar amount, and the source document for every single adjustment.

For more detail on SDE and the add-back methodology, read my post on what SDE is and how to calculate it.

Balance Sheet Cleanup: What Buyers Look at Beyond Income

Most sellers focus entirely on the income statement when preparing financials. But buyers and lenders also look hard at the balance sheet, and what's there can affect the deal significantly.

Clean Up the Balance Sheet Before Listing

Walk through every line on your balance sheet. Here is what to check and fix for each item:

| Balance Sheet Item | What to Check | Action Before Listing |

|---|---|---|

| Cash | Balances reconcile to bank statements | Reconcile all accounts, resolve discrepancies |

| Accounts Receivable | Only amounts actually owed to you | Write off uncollectible receivables (anything 120+ days old) |

| Equipment & Fixed Assets | Assets on books actually exist and work | Remove fully depreciated or unused assets |

| Intangibles | Goodwill, customer lists are explainable | Document what each represents and how it was valued |

| Accounts Payable | Reflects what you actually owe | Clear old payables already paid but not removed from books |

| Owner Loans | Owner borrowing or lending to business | Document and resolve all intercompany or owner loan balances |

| Deferred Revenue | Advance payments for undelivered services | Correctly reflect as a liability |

Showing $200,000 in receivables when $80,000 is more than 120 days old and effectively uncollectible misleads buyers about working capital. Buyers will do a walk-through and compare the asset list to what they see. Buyer's lenders will flag unresolved intercompany or owner loan balances. Make sure every line is accurate and explainable.

Accounts Receivable and Payable: What Your Aging Report Reveals

The accounts receivable aging report shows how old each outstanding invoice is. It tells a story about your collection practices and the health of your customer relationships.

What Buyers Look For in AR Aging

Buyers want to see most receivables collected within 30 to 45 days. If a significant portion of your AR is over 90 days, it signals collection problems or customers in financial trouble. Either way, it affects what portion of receivables buyers will count toward working capital.

| AR Aging Bucket | Buyer Perception | Impact on Deal |

|---|---|---|

| 0 to 30 days | Healthy, normal collection cycle | Counted at full value toward working capital |

| 31 to 60 days | Acceptable but worth monitoring | Usually counted at full value |

| 61 to 90 days | Raises questions about collection practices | May be discounted 10 to 25% |

| 91 to 120 days | Signals collection problems | Often discounted 50% or more |

| 120+ days | Likely uncollectible | Usually excluded from working capital entirely |

Before you go to market:

- Send overdue notices and actively collect past due accounts

- Write off or provision for any receivables you know are uncollectible

- Document your collection process so buyers can see it's systematic

What Your AP Aging Reveals

The accounts payable aging shows how quickly you pay your vendors. Slow payment may indicate cash flow stress. Very fast payment may indicate poor cash management. Either can raise questions.

Make sure you're paying vendors on roughly normal terms and that any significantly overdue payables are resolved or explained before you list.

Inventory Valuation: How to Handle It

If your business carries inventory, how it's valued on the balance sheet matters to buyers. Inventory is typically included in the sale, and the purchase agreement will specify how the final inventory count and value gets determined.

Common Inventory Issues

Obsolete or slow moving inventory. Buyers don't want to pay full price for inventory that won't sell. Write down or write off inventory that's clearly obsolete before you list. A buyer who finds a warehouse full of unsellable goods after closing is a unhappy buyer.

Inconsistent valuation method. Make sure you've been valuing inventory consistently, whether FIFO, LIFO, or weighted average. Changing methods in the year before a sale creates confusion and looks like manipulation.

Consigned inventory. If you hold inventory on consignment, make sure it's clearly separated from owned inventory in your accounting.

Most deals for product businesses include a provision for a physical inventory count at or just before closing, with the purchase price adjusted based on the actual value of inventory on hand. Know how your inventory is valued so you can explain the methodology clearly.

When to Hire a CPA or Financial Advisor to Help

If your financials are clean and your bookkeeping is current, you may not need extensive help beyond your regular accountant. But in many situations, hiring a CPA with business transaction experience before you go to market is worth every dollar.

Consider bringing in specialized financial help if:

- Your books have years of personal expenses mixed in that need to be sorted

- There are significant discrepancies between your tax returns and your QuickBooks or other accounting software

- Your business has multiple entities, related party transactions, or complex ownership structures

- Revenue has been volatile and needs a narrative that explains the trend

- You want a quality of earnings report to preempt buyer due diligence

A quality of earnings report, prepared by an independent CPA, is an analysis of your financials that validates your SDE and add-backs before the buyer's CPA does it. It's proactive, it speeds up due diligence, and it signals to buyers and lenders that you're confident in your numbers.

| Level of Financial Help | Typical Cost | When You Need It | What You Get |

|---|---|---|---|

| Regular accountant cleanup | $1,000 to $3,000 | Books are mostly clean, minor personal expense sorting | Reconciled P&Ls, corrected categories, clean balance sheet |

| CPA financial review | $3,000 to $8,000 | Material discrepancies between books and tax returns | Reviewed statements, SDE bridge, reconciliation report |

| Quality of earnings report | $5,000 to $25,000 | Complex business, multiple entities, or buyer requires it | Independent validation of SDE, add-backs, and revenue quality |

Before you bring in a CPA, use our seller due diligence checklist to assess which financial areas need the most attention.

Ready to think through your financial preparation plan? Talk to me directly and I'll tell you honestly what level of financial cleanup you need before listing.

The Financial Package Buyers Expect When You List

When you go to market, you should be ready to provide the following on request to serious buyers after an NDA is signed:

The Standard Seller Financial Package

- Three years of profit and loss statements (monthly detail, not just annual)

- Three years of business tax returns (all schedules)

- Most recent year-to-date P&L if you're listing mid-year

- Balance sheet as of the most recent month end

- Add-back schedule with documentation

- Any large contracts with customers or vendors

- Accounts receivable aging report

- Accounts payable aging report

- Inventory valuation (if applicable)

- List of equipment and fixed assets

The cleaner and more organized this package is, the faster buyers move. I've seen well-prepared sellers go from signed NDA to letter of intent in under two weeks. Sellers who are scrambling to pull together basic financials can spend months just getting to the due diligence stage.

Well prepared sellers go from signed NDA to letter of intent in under two weeks. Sellers scrambling to pull together financials can spend months just getting to the due diligence stage. Your financial package is the single biggest factor in deal velocity.

Some sellers also prepare a seller's discretionary earnings summary, a one or two page document that shows the SDE calculation clearly with line item add-backs. This is not required, but it orients buyers quickly and reduces back-and-forth questions.

Next Steps for Sellers

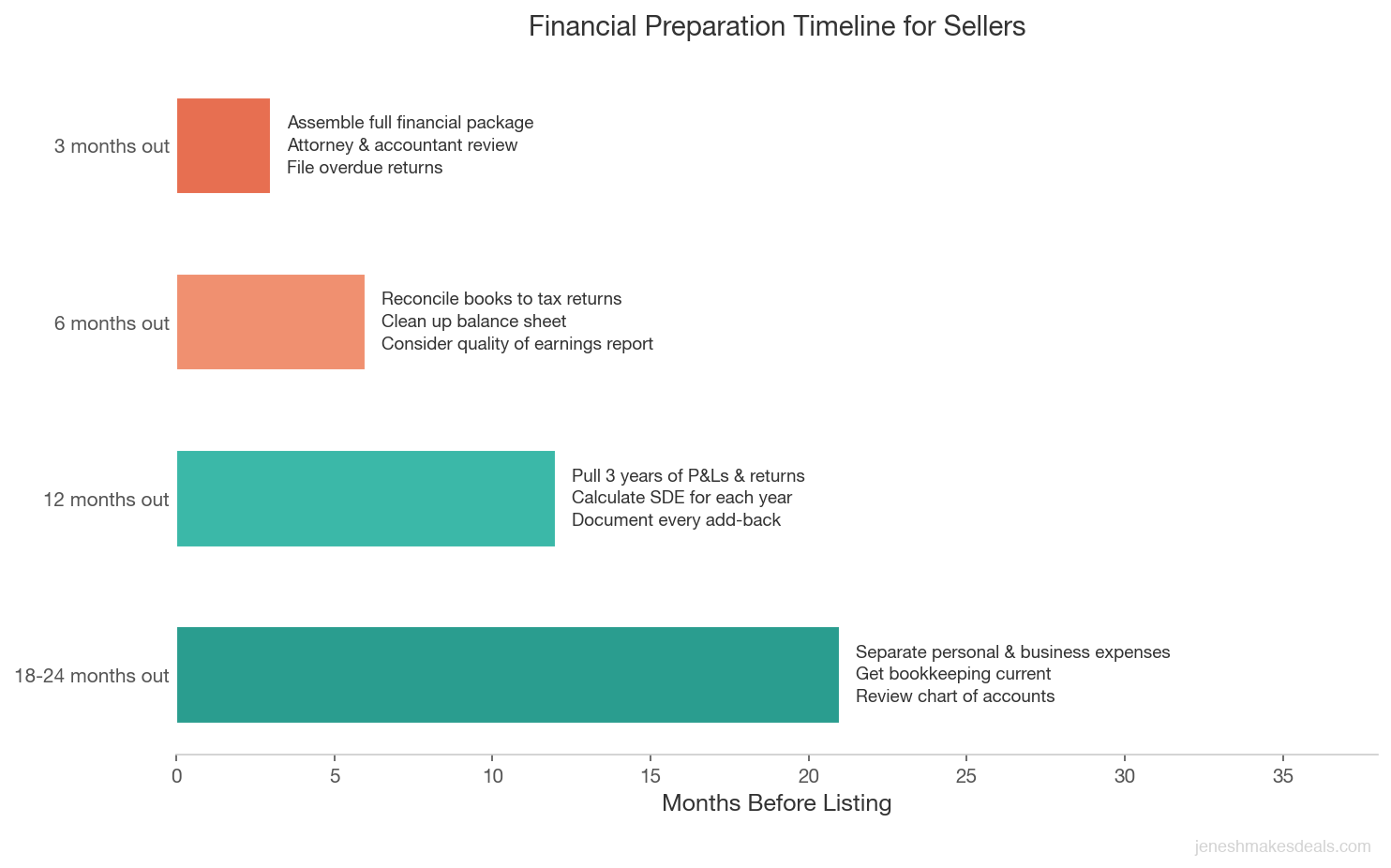

The time to prepare your financials is not when you've already decided to list. It's 12 to 24 months before you think you want to sell.

Here's a practical timeline:

18 to 24 months out: Start separating personal and business expenses completely. Get your bookkeeping current and on a consistent system. Review your chart of accounts.

12 months out: Pull three years of P&Ls and tax returns. Calculate SDE for each year. Identify and document every add-back. Note anything that will need explanation to a buyer.

6 months out: Reconcile your books to your tax returns. Clean up the balance sheet. Consider hiring a CPA for a financial review or quality of earnings report.

3 months out: Assemble the full financial package. Have your attorney and accountant review everything. Make sure your most recent returns are filed and any overdue issues are resolved.

Being financially prepared before you list puts you in a position of strength. You control the narrative. You know your numbers cold. And you close faster at a higher price.

For more on preparing your business for sale overall, read my guide on maximizing business value before selling. You should also understand what buyers will be looking for when they review your financials so you can present the right picture.

Want help thinking through your financial preparation timeline? Contact me here for a free consultation. I'll walk you through what buyers and lenders will look at and help you prepare in advance. Ready to start the process? Learn more about selling with us.

Get the complete seller playbook. Our free Complete Guide to Selling Your Business in 2026 covers everything from financials to negotiation to tax planning.

Common Mistakes Sellers Make with Financials

| Mistake | Why It Hurts | How to Avoid It |

|---|---|---|

| Waiting until after deciding to sell | Cleaning up 3 years of messy books in 30 days creates errors and looks rushed | Start financial cleanup 12 to 24 months before listing |

| Claiming add-backs without documentation | "Trust me, that was personal" gets cut in due diligence every time | Attach source documents (W-2s, invoices, receipts) to every add-back |

| Not reconciling QuickBooks to tax returns | A $400,000 gap between bookkeeping and returns raises serious red flags | Reconcile quarterly and resolve discrepancies before going to market |

| Overstating normalized EBITDA or SDE | Buyers adjust their offer downward after due diligence uncovers inflated numbers | Be conservative with add-backs, let buyers discover upside rather than downside |

| Not preparing the most recent year | Buyers want 2023, 2024, and 2025 financials, missing data stalls the deal | Close your books promptly each year, have year-to-date statements ready |

| Forgetting about trends | A single strong year doesn't overcome two years of decline | Present all three years honestly and explain what changed |

Frequently Asked Questions

Do I need audited financials to sell my business?

Most small business sales don't require audited financials. Reviewed or compiled financials, or CPA-prepared tax returns with internal P&Ls, are usually sufficient. Larger transactions over $5 million may require reviewed or audited statements, especially if institutional buyers or lenders are involved.

What if my tax returns show very low income to minimize taxes?

This is common and doesn't prevent you from selling. The SDE add-back process exists specifically to bridge this gap. But you'll need to clearly document every add-back and be prepared for your lender to use the tax return number as their baseline. Work with a CPA to build a solid bridge.

Should I have my books prepared by a new accountant before listing?

Not necessarily. Changing accountants right before a sale can raise questions. If your current accountant is competent, have them prepare a cleaned-up three year summary. If the books are in bad shape, bringing in a specialist for a financial cleanup project makes sense, while keeping your regular accountant for ongoing filings.

What happens if buyers find something in due diligence that I didn't disclose?

It depends on what they find and whether it was material. Minor discrepancies get negotiated into a price adjustment. Material issues can kill the deal or lead to legal claims under the representations and warranties in your purchase agreement. Disclose proactively and your attorney can help you document it in a way that minimizes liability.

How far back do buyers look at financials?

Standard practice is three years. For businesses with unusual history (a big year, a bad year, pandemic disruption), buyers may want to look further back to understand the baseline. SBA lenders also look at three years of business tax returns plus two years of personal returns for the owner.

Can I sell if one year was bad?

Yes. One bad year in three is explainable. Two bad years out of three is harder. Three declining years requires a very compelling story about what changed and why the trend reversed. Be honest about the history and present the most recent 12 months in detail if they're stronger than the prior years.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.