You agreed on a $1.2 million sale price. You shook hands. You signed a letter of intent. Then three weeks before closing, your buyer's attorney sends over the purchase agreement, and buried in section 7 is something about a "working capital peg" of $165,000.

You call your broker. "What is this? I thought the price was $1.2 million."

It still is. But now you're learning that you need to leave $165,000 worth of current assets in the business at closing. And if the actual working capital falls short of that peg, the difference comes out of your proceeds.

I've watched this scenario play out dozens of times. Sellers who thought they understood the deal suddenly realize the number on the LOI is not the number that hits their bank account. Working capital adjustments are one of the most poorly understood parts of selling a business, and they can swing the final proceeds by $50,000 to $200,000 in either direction.

Let me explain how this works so you're not caught off guard.

What Working Capital Actually Is

Working capital is a simple formula:

Working Capital = Current Assets minus Current Liabilities

Current assets are the things your business owns that can be converted to cash within 12 months. That includes cash in the bank, accounts receivable, inventory, and prepaid expenses. Current liabilities are the obligations due within 12 months: accounts payable, accrued wages, sales tax payable, and short term debt.

Here's a quick example. Say your business has:

- Cash: $80,000

- Accounts receivable: $95,000

- Inventory: $60,000

- Prepaid expenses: $15,000

- Total current assets: $250,000

And on the liability side:

- Accounts payable: $55,000

- Accrued expenses: $20,000

- Sales tax payable: $10,000

- Short term loan balance: $15,000

- Total current liabilities: $100,000

Your net working capital is $150,000. That's the cash the business needs in the system to keep the lights on, pay vendors, carry inventory, and collect from customers. It's the operational fuel that makes the business run day to day.

If you want a deeper look at how this number plays into a buyer's calculations, see working capital from a buyer's perspective.

Why Buyers Require a Working Capital Peg

Put yourself in the buyer's shoes for a moment. They're paying you $1.2 million for a business that generates, say, $300,000 in seller's discretionary earnings. They've probably put 10% to 20% down and financed the rest through an SBA loan. Their cash reserves are thin.

Now imagine closing day arrives and you've pulled out all the cash, collected every receivable, and sold off extra inventory. The buyer walks in on Monday morning and the business has $12,000 in the bank, zero receivables coming in, and not enough inventory to fill the next week's orders. Payroll is due Friday. Vendor invoices are stacking up.

The business technically still exists, but it can't function. The buyer would need to inject $100,000 or more of their own money just to get through the first month. That's not what they agreed to pay for.

This is why virtually every business acquisition includes a working capital requirement. The buyer expects to receive a business that can operate normally from day one. The working capital peg establishes what "normal" looks like, and the seller is expected to deliver the business with at least that much working capital at closing.

How the Working Capital Peg Is Calculated

The most common approach is to calculate the average net working capital over the trailing 12 months. You take a snapshot of working capital at the end of each of the last 12 months, add them up, and divide by 12. That average becomes the peg.

Some deals use a 6 month average if the business has been growing or contracting significantly, and the parties agree that recent months better reflect the go forward reality. I've also seen 3 month averages in fast moving businesses where the 12 month lookback doesn't make sense.

Here's where it gets negotiated. Buyers want to include everything that keeps the business running. Sellers want to exclude items that inflate the peg, because a higher peg means more assets they need to leave behind. Common negotiation points include:

- Cash: Many deals exclude operating cash from the working capital calculation. The seller keeps the cash, and working capital is calculated on a "cash free, debt free" basis. This is standard in most small business transactions.

- Inventory: Almost always included. The buyer needs product to sell.

- Accounts receivable: Usually included, but sometimes the seller retains receivables and collects them post closing. This depends on the deal structure.

- Prepaid expenses: Included if they benefit the buyer (like prepaid rent or insurance that extends past closing).

The key is that whatever methodology is used, it needs to be spelled out clearly in the purchase agreement. Vague language around working capital is where disputes start. If you're preparing your financials for sale, make sure your monthly balance sheets are clean enough to support this calculation.

The True Up Mechanism

Here's how the peg actually works at closing. The purchase agreement establishes a target working capital number, let's say $150,000. At closing, you deliver the business with whatever working capital happens to be there on that specific date.

But here's the catch: you don't know the exact working capital on closing day until after the books are closed for that period. So most deals use an estimated working capital at closing, with a "true up" that happens 60 to 90 days later.

The true up works like this:

Step 1: At closing, both parties agree on an estimated working capital number. Let's say it's $155,000.

Step 2: The buyer's accountant prepares a closing date balance sheet within 60 to 90 days after closing. They calculate the actual working capital as of the closing date.

Step 3: If actual working capital was $170,000 (above the $150,000 peg), the buyer owes the seller the $20,000 difference. The seller gets a check.

Step 4: If actual working capital was $130,000 (below the $150,000 peg), the seller owes the buyer $20,000. This typically comes out of an escrow holdback.

Most purchase agreements include a "collar" or threshold, usually $5,000 to $15,000, where no adjustment is made. If working capital is within $10,000 of the peg in either direction, both parties just leave it alone. This prevents disputes over minor fluctuations.

The true up is where a lot of post closing tension lives. The seller thinks they left the business in great shape. The buyer's accountant finds $25,000 in accrued liabilities that weren't on the estimated balance sheet. Now someone owes someone money. Clear documentation and a well drafted purchase agreement prevent most of these fights.

How Working Capital Affects Your Net Proceeds

Let me walk through a real example so you can see how this hits your bottom line.

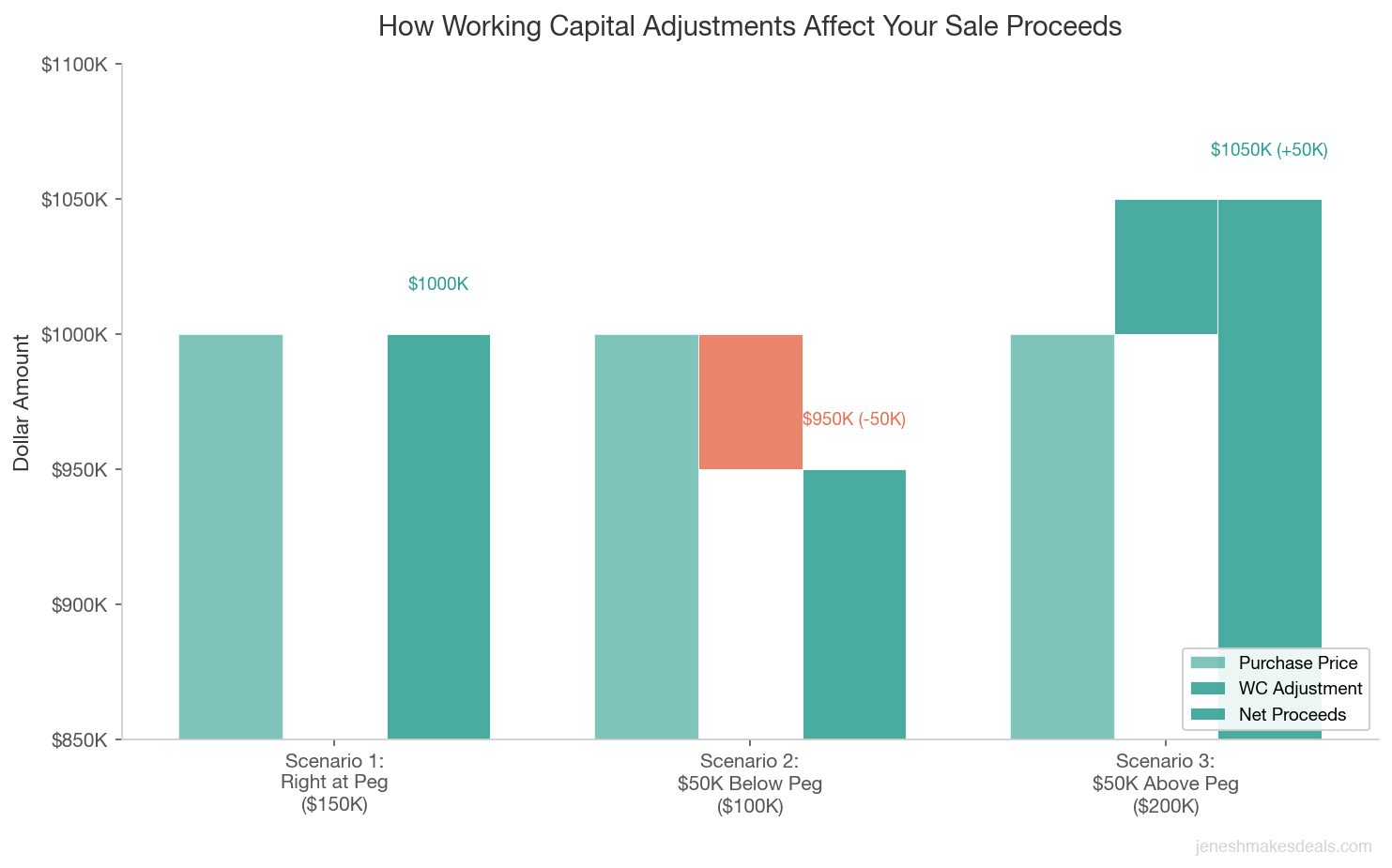

The deal: Your business sells for $1,000,000. The working capital peg, based on a 12 month trailing average, is $150,000.

Scenario 1: Working capital at closing is $150,000 (right at the peg)

You receive the full $1,000,000 purchase price. No adjustment. This is the cleanest outcome.

Scenario 2: Working capital at closing is $100,000 ($50,000 below the peg)

The purchase price is reduced by $50,000. Your effective proceeds are $950,000. That $50,000 shortfall typically happened because you collected receivables aggressively before closing, ran down inventory, or delayed payables to boost cash.

Scenario 3: Working capital at closing is $200,000 ($50,000 above the peg)

You receive the $1,000,000 purchase price plus an additional $50,000 for the excess working capital. Your total proceeds are $1,050,000. This happens when a seller leaves the business flush with inventory or has a strong receivables month heading into closing.

See the pattern? The working capital peg is essentially a second price negotiation. The headline number is important, but the peg determines how much of that number you actually keep. On a $1 million deal, I've seen working capital adjustments range from $30,000 in the seller's favor to $80,000 against the seller.

Need help figuring out what your business is worth? Use our free business valuation calculator to get a quick estimate.

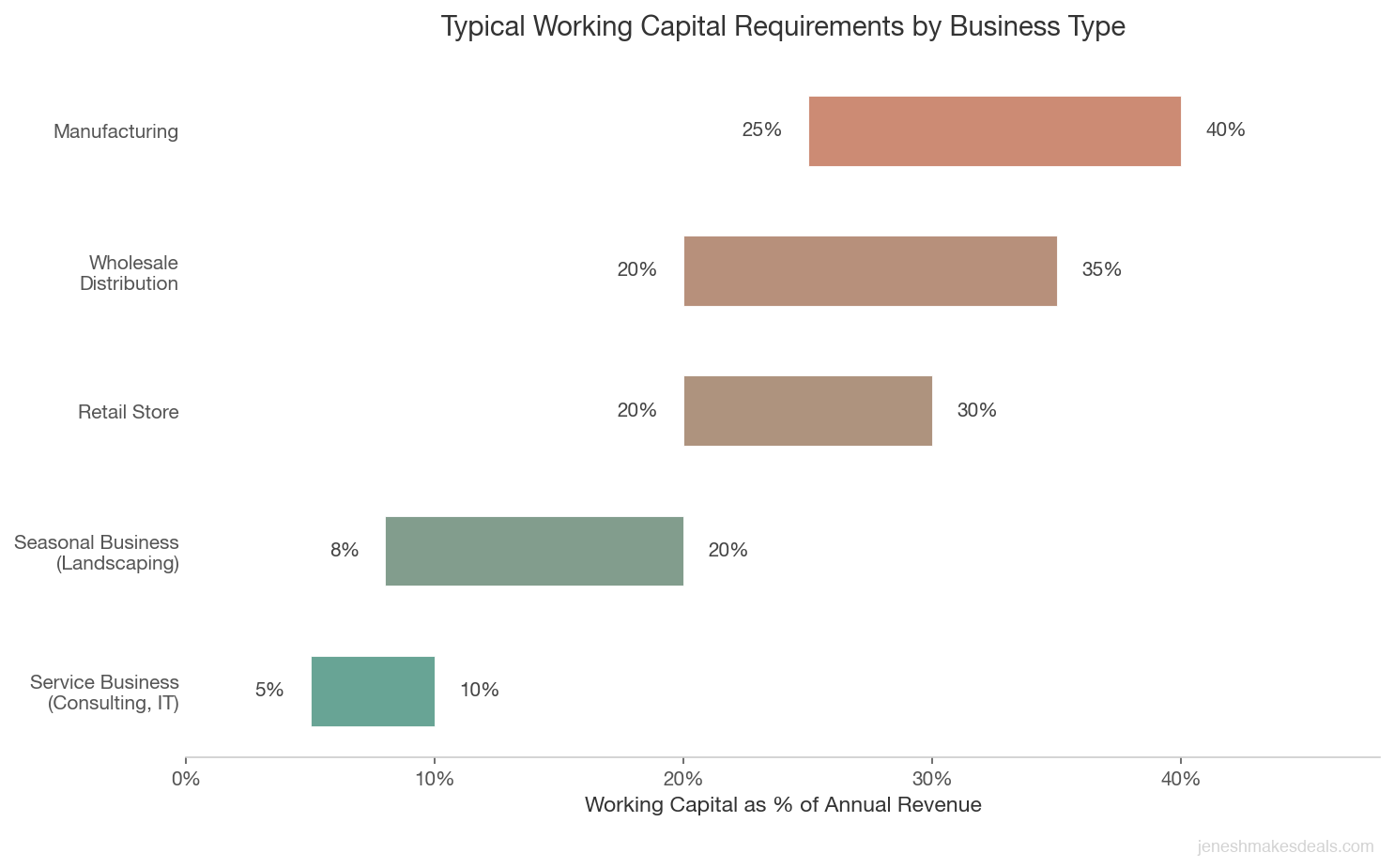

Working Capital in Different Types of Businesses

Not all businesses carry the same working capital. The type of business you're selling dramatically affects how big the working capital peg will be and how much it affects your proceeds.

Service Businesses

Service businesses typically have low working capital requirements. If you run a consulting firm, an IT services company, or a marketing agency, your current assets are mostly cash and receivables. You don't carry inventory. Your working capital peg might be 5% to 10% of annual revenue.

On a $500,000 service business sale, the working capital peg might be $25,000 to $50,000. It's a factor, but it's not going to reshape the economics of the deal.

Retail and Distribution

Retail businesses carry inventory, and inventory is the biggest driver of working capital. A retail store with $400,000 in annual revenue might carry $80,000 to $120,000 in inventory at any given time. Add in receivables if you sell on terms, and the working capital peg can easily reach 20% to 30% of revenue.

On a $1 million retail business sale, a working capital peg of $200,000 to $300,000 is common. That's real money.

Manufacturing

Manufacturing businesses often have the highest working capital needs. You're carrying raw materials, work in process, finished goods, and often sizable accounts receivable because your customers are other businesses that pay on 30 to 60 day terms. Working capital as a percentage of revenue can hit 25% to 40%.

I worked with a manufacturing seller whose business sold for $2.5 million. The working capital peg was $625,000. That was a bigger number than his SBA down payment would have been if he were the buyer. He wasn't prepared for it, and it caused real tension in the final weeks before closing.

Seasonal Businesses

If your business is seasonal, the month you close matters enormously. A landscaping company that closes in March might have $20,000 in working capital. The same company closing in July might have $90,000. The trailing 12 month average accounts for some of this, but the actual working capital at closing can still swing wildly depending on timing.

Common Working Capital Disputes

Working capital disagreements are the number one source of post closing disputes in business sales. Here are the issues I see most often.

What Counts as "Current"

The standard definition of current assets and liabilities uses a 12 month cutoff. But gray areas exist. Is a deposit on a piece of equipment that won't arrive for 14 months a current asset? What about a customer retainer that's partially earned? Both sides will interpret these in their favor.

Cash vs. Non Cash Working Capital

In many deals, working capital is calculated on a "cash free" basis, meaning operating cash is excluded. But then the question becomes: what's "operating cash" versus "excess cash"? If your business keeps $200,000 in the bank but only needs $50,000 to operate, is the other $150,000 excess cash that the seller keeps? This needs to be defined precisely.

Prepaid Expenses

Sellers sometimes prepay expenses before closing, like six months of insurance or a year of software licenses. Those prepaid amounts show up as current assets, which inflates working capital. Buyers will argue those prepayments were made specifically to manipulate the peg. Sellers will argue they were normal business operations. Again, clarity in the purchase agreement prevents this.

Accounts Receivable Quality

Not all receivables are equal. If your AR includes $40,000 that's 120 days past due and unlikely to be collected, is it really a current asset? Buyers will push to exclude aged receivables or apply a discount. Sellers will argue that slow paying customers always pay eventually. The deal should specify aging thresholds, typically excluding anything over 90 days.

Accrued Liabilities the Seller Didn't Book

This is the one that creates the most anger. After closing, the buyer's accountant discovers accrued liabilities that weren't on the seller's balance sheet. Unpaid vacation time. Unreported sales tax. Warranty obligations. These increase current liabilities, which reduces working capital below the peg, which triggers a payment from the seller. If you're a seller, make sure your accruals are complete and accurate before closing.

How Sellers Can Protect Themselves

Working capital doesn't have to be a trap. If you understand how it works and plan for it, you can protect your proceeds and avoid post closing disputes.

Negotiate the Peg Carefully

Don't just accept whatever trailing 12 month average the buyer proposes. Look at what's included in the calculation. If certain months were anomalies (a big inventory build for a one time order, or a seasonal spike that won't repeat), argue for excluding them or using a methodology that reflects normal operations.

Understand What's Included and Excluded

Before you sign the purchase agreement, get a line by line breakdown of what goes into the working capital calculation. Which specific accounts are included? What's the treatment of cash? How are aged receivables handled? This is not a detail to leave to the attorneys. You need to understand it.

Don't Strip Cash Before Closing

This is the biggest mistake I see sellers make. In the months leading up to closing, they start pulling cash out of the business. They take extra distributions. They delay vendor payments to keep cash in their personal accounts. They collect receivables aggressively and don't reinvest.

All of this reduces working capital below the peg, which reduces your proceeds dollar for dollar. Every $1 you pull out above normal distributions is $1 that comes off your sale price. It's a zero sum game.

Keep Operations Normal

Run the business the same way you've been running it. Don't change your ordering patterns, collection practices, or payment timing. Buyers and their advisors will compare your closing date working capital to the trailing average, and if it looks like you manipulated things, it creates distrust that can derail the entire deal.

Get Clarity in the Purchase Agreement

The working capital section of your purchase agreement should be several pages long with a detailed schedule showing exactly which accounts are included, the methodology for calculating the peg, the true up timeline, the dispute resolution process, and the collar amount. If it's one vague paragraph, you're setting yourself up for a fight.

Ready to talk about selling? Contact us for a free consultation and we'll walk you through your options.

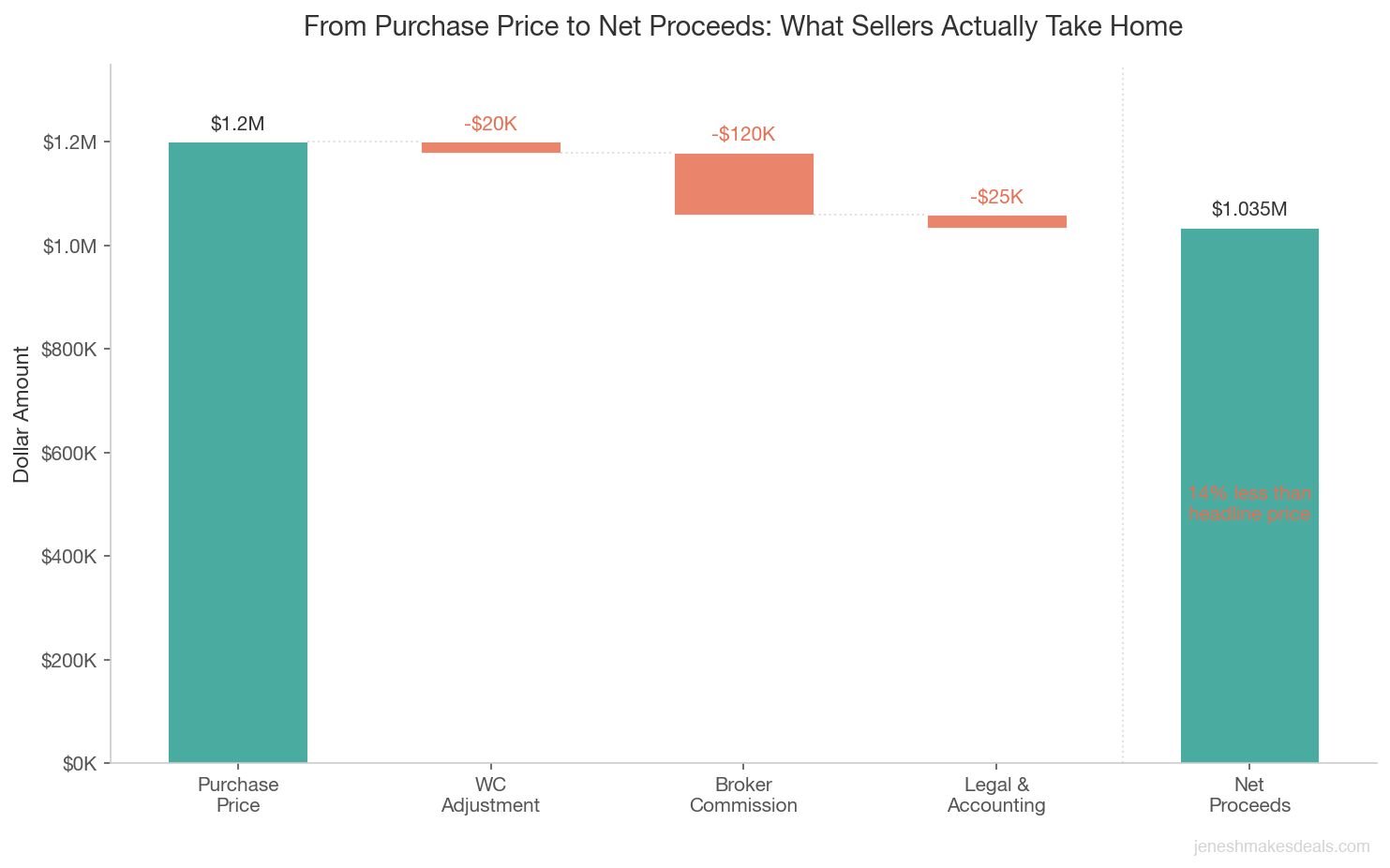

Working Capital vs. the Purchase Price

Here's the mental model I want you to walk away with. When you see a purchase price of $1.2 million in a letter of intent, don't think of that as the money you're going to receive. Think of it as the enterprise value, which then gets adjusted for working capital.

Your actual proceeds look like this:

Net Proceeds = Purchase Price +/- Working Capital Adjustment - Transaction Costs

If the working capital peg is $150,000 and you deliver $150,000, the adjustment is zero. If you deliver $120,000, you lose $30,000. If you deliver $180,000, you gain $30,000.

This is why I tell every seller to model their net proceeds before they agree to a deal. Knowing your EBITDA and SDE is critical for the headline price, but understanding working capital is what tells you what you'll actually take home.

Here's a framework:

| Component | Amount |

|---|---|

| Purchase price (enterprise value) | $1,200,000 |

| Working capital peg | $150,000 |

| Estimated WC at closing | $130,000 |

| Working capital adjustment | -$20,000 |

| Broker commission (10%) | -$120,000 |

| Legal and accounting | -$25,000 |

| Estimated net proceeds | $1,035,000 |

That $1.2 million headline becomes $1.035 million after working capital and transaction costs. Still a great outcome, but it's 14% less than the number you shook hands on. If you haven't planned for this, it can feel like you're being taken advantage of. You're not. This is how every deal works. You just need to plan for it from the beginning.

What to Do Right Now If You're Thinking About Selling

Start tracking your monthly working capital. Pull a balance sheet at the end of each month and calculate current assets minus current liabilities. Do this for 12 consecutive months so you have a trailing average ready when you need it.

Look at the composition of your working capital. Is it mostly inventory? Receivables? Cash? The composition tells you what's going to be negotiated hardest in the deal. Heavy inventory businesses face the toughest working capital negotiations because inventory values are subjective.

Talk to your accountant about accrued liabilities. Make sure everything that should be on your balance sheet is actually there. Unpaid vacation, deferred revenue, warranty reserves. These are current liabilities that reduce your working capital, and it's much better to deal with them now than to have them discovered during the true up.

And most importantly, don't treat the working capital discussion as an afterthought. It should be part of your deal negotiations from day one, right alongside the purchase price and terms. The sellers who get the best outcomes are the ones who understand every number in the deal, not just the headline.

Planning to sell your business? Reach out for a confidential conversation about what your deal might look like, including working capital, net proceeds, and timeline.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.