You spent years building your business. You finally got an offer you're happy with. Then your accountant tells you what you actually owe in taxes, and suddenly that number doesn't look so great anymore.

I see this happen all the time. A business owner sells for $1.2 million and expects to walk away with most of it. After federal capital gains taxes, state income taxes, depreciation recapture, and the net investment income tax, they're left with somewhere between $720,000 and $840,000. That's a 30% to 40% haircut they didn't plan for.

Use our seller net proceeds calculator to estimate your actual take home based on your sale price and tax situation.

The good news is that the tax outcome isn't fixed. How you structure the deal, when you sell, and what kind of entity you're selling all affect how much you keep. The difference between a well planned sale and a poorly planned one can be six figures.

Important disclaimer: Everything in this post is general educational information. I'm a business broker, not a CPA or tax attorney. Your specific tax situation depends on dozens of variables I can't account for here. Please work with a qualified tax professional before making any decisions about selling your business.

The Tax Surprise Most Sellers Don't See Coming

Most business owners I talk to focus on one number: the sale price. They want to know what their business is worth, so they look at their seller's discretionary earnings or EBITDA, apply a multiple, and land on a figure.

But the sale price is the gross number. What matters is the net, and taxes are the single biggest line item between the two. On a $1 million sale, the federal tax alone can range from $150,000 to $370,000 depending on how the deal is structured.

Here's what makes it tricky. The IRS doesn't treat a business sale as one transaction. It breaks the sale apart into individual asset categories, and each one gets taxed at a different rate. Goodwill gets treated differently than inventory, which gets treated differently than equipment, which gets treated differently than a non compete agreement.

The structure of the deal, whether it's an asset sale or stock sale, how the purchase price is allocated, and whether you take a lump sum or installments, all change the tax picture dramatically.

Capital Gains vs Ordinary Income: How the Sale Gets Taxed

When you sell a business, different parts of the sale get taxed at different rates. The two big buckets are capital gains (lower rates) and ordinary income (higher rates).

Capital gains treatment (lower taxes):

- Goodwill and going concern value

- Customer lists and other intangible assets held more than one year

- Real estate (if held more than one year)

Ordinary income treatment (higher taxes):

- Inventory

- Accounts receivable

- Non compete agreements (the IRS treats these as ordinary income to the seller)

- Depreciation recapture on equipment

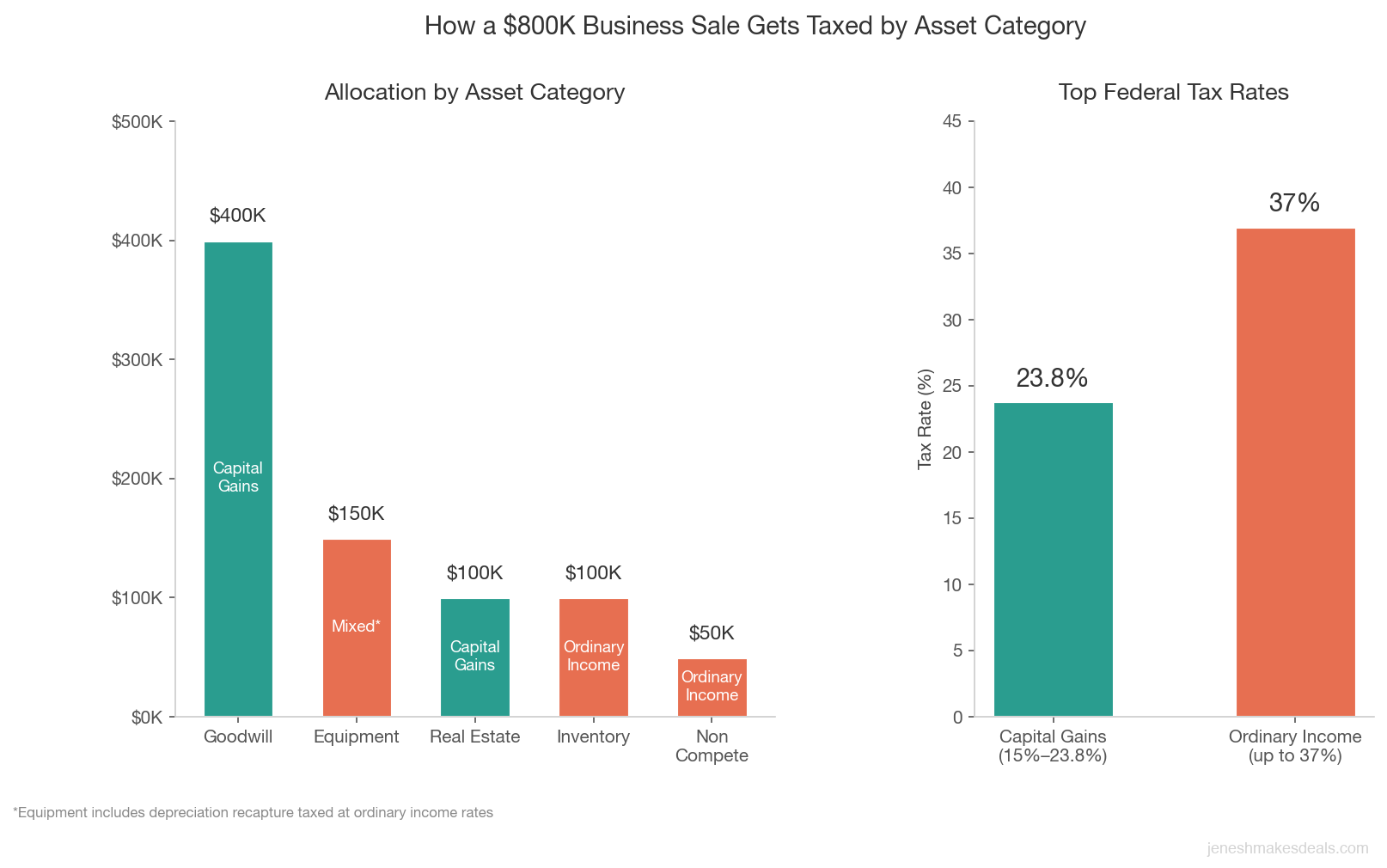

Here's a real example. Say you sell your business for $800,000 and the purchase price allocation breaks down like this:

- Goodwill: $400,000 (capital gains rate, 15% to 23.8%)

- Equipment: $150,000 with $100,000 of depreciation recapture (ordinary income rate on the recapture)

- Inventory: $100,000 (ordinary income rate)

- Non compete agreement: $50,000 (ordinary income rate)

- Real estate: $100,000 (capital gains rate)

The $400,000 in goodwill gets taxed at the long term capital gains rate. But that $100,000 in depreciation recapture and $100,000 in inventory? Those get taxed at your ordinary income rate, which could be 32% or 37% at the federal level.

This is why the purchase price allocation in your sale agreement is one of the most important tax documents you'll sign. It determines which bucket each dollar falls into.

The purchase price allocation is the single most negotiable tax document in your entire deal. Every dollar you shift from ordinary income categories to goodwill saves you 13 percentage points in federal tax.

Asset Sale vs Stock Sale: The Tax Tug of War

The biggest structural decision in any business sale is whether it's an asset sale vs stock sale. This single choice can swing the seller's tax bill by tens of thousands of dollars.

Asset sale: The buyer purchases individual assets (equipment, inventory, goodwill, customer list, etc.). Each asset class gets taxed at its own rate. The buyer gets to "step up" the basis of those assets and depreciate them, which gives the buyer a tax benefit.

Stock sale: The buyer purchases the ownership shares of the entity. The seller typically pays long term capital gains on the entire profit, which is usually more favorable. The buyer inherits the existing tax basis of the assets, which is usually less favorable for them.

See the tension? Buyers generally prefer asset sales because they get bigger depreciation deductions going forward. Sellers generally prefer stock sales because the entire gain is taxed at the lower capital gains rate.

| Factor | Asset Sale | Stock Sale |

|---|---|---|

| Seller tax treatment | Each asset taxed at its own rate | Entire gain taxed at capital gains rate |

| Buyer tax benefit | Step up in basis, larger depreciation | Inherits existing basis |

| Who prefers it | Buyers (tax deductions) | Sellers (lower tax rate) |

| Common entity types | Sole proprietorships, LLCs | C corporations |

| Typical deal size | Under $5 million | Over $5 million |

In practice, most small business sales (under $5 million) are structured as asset sales. If you're selling a sole proprietorship or LLC, it's almost always an asset sale by default. Stock sales are more common with C corporations and larger transactions.

If the buyer insists on an asset sale but you'd benefit from stock sale treatment, this is a negotiation point. Some sellers accept a slightly lower purchase price in exchange for stock sale treatment because the after tax proceeds end up being higher.

Ready to talk about selling? Contact us for a free consultation and we'll walk you through your options.

Federal Capital Gains Tax Rates in 2026

For 2026, the federal long term capital gains rates are:

- 0% for single filers with taxable income up to approximately $48,350 (married filing jointly up to $96,700)

- 15% for single filers from $48,350 to $533,400 (married filing jointly from $96,700 to $600,050)

- 20% for income above those thresholds

On top of those rates, there's the 3.8% Net Investment Income Tax (NIIT) that applies to individuals with modified adjusted gross income above $200,000 (single) or $250,000 (married filing jointly). These NIIT thresholds have never been adjusted for inflation since they were introduced in 2013, so they catch more sellers every year.

For most business owners selling a business worth $500,000 or more, the effective federal capital gains rate is 23.8% (the 20% top rate plus the 3.8% NIIT).

One thing to watch in 2026: the Tax Cuts and Jobs Act provisions are set to sunset at the end of 2025 unless Congress extends them. This could affect ordinary income tax brackets for the portions of your sale taxed as ordinary income. If your sale includes significant inventory, non compete payments, or depreciation recapture, changes to the ordinary income brackets matter. Talk to your CPA about the current status of any tax legislation.

Depreciation Recapture: The Hidden Tax Trap

If your business owns equipment, vehicles, or other depreciable assets, depreciation recapture is probably the most misunderstood tax issue in a business sale.

Here's how it works. Over the years, you've been deducting depreciation on your equipment. Those deductions reduced your ordinary income and saved you taxes at your marginal rate. When you sell the business, the IRS wants some of that back.

Section 1245 property (equipment, vehicles, machinery, furniture): The gain attributable to prior depreciation deductions is taxed as ordinary income, up to a maximum rate of 37%. Only the gain above the original cost gets capital gains treatment.

Section 1250 property (real estate): Depreciation recapture on real property is taxed at a maximum rate of 25%, which is higher than the standard capital gains rate but lower than ordinary income rates.

Let me show you a concrete example.

You bought a piece of equipment for $200,000 five years ago. You've taken $160,000 in depreciation deductions, so your adjusted basis is $40,000. You sell the business, and this equipment is valued at $120,000 in the purchase price allocation.

Your total gain is $80,000 ($120,000 sale price minus $40,000 basis). But here's how it breaks down:

- Depreciation recapture: $80,000 of the gain is recaptured at ordinary income rates (because the sale price doesn't exceed the original $200,000 cost). At a 37% federal rate, that's $29,600 in tax on this single piece of equipment.

If you'd been taxed at the capital gains rate of 23.8%, the tax would have been $19,040. That's a $10,560 difference on just one asset.

Now multiply that across all your depreciated equipment. If you took advantage of bonus depreciation or Section 179 expensing in prior years (which accelerated your deductions), the recapture bill can be substantial.

State Taxes: Where You Live Matters More Than You Think

Federal taxes are only part of the picture. State taxes on a business sale vary wildly.

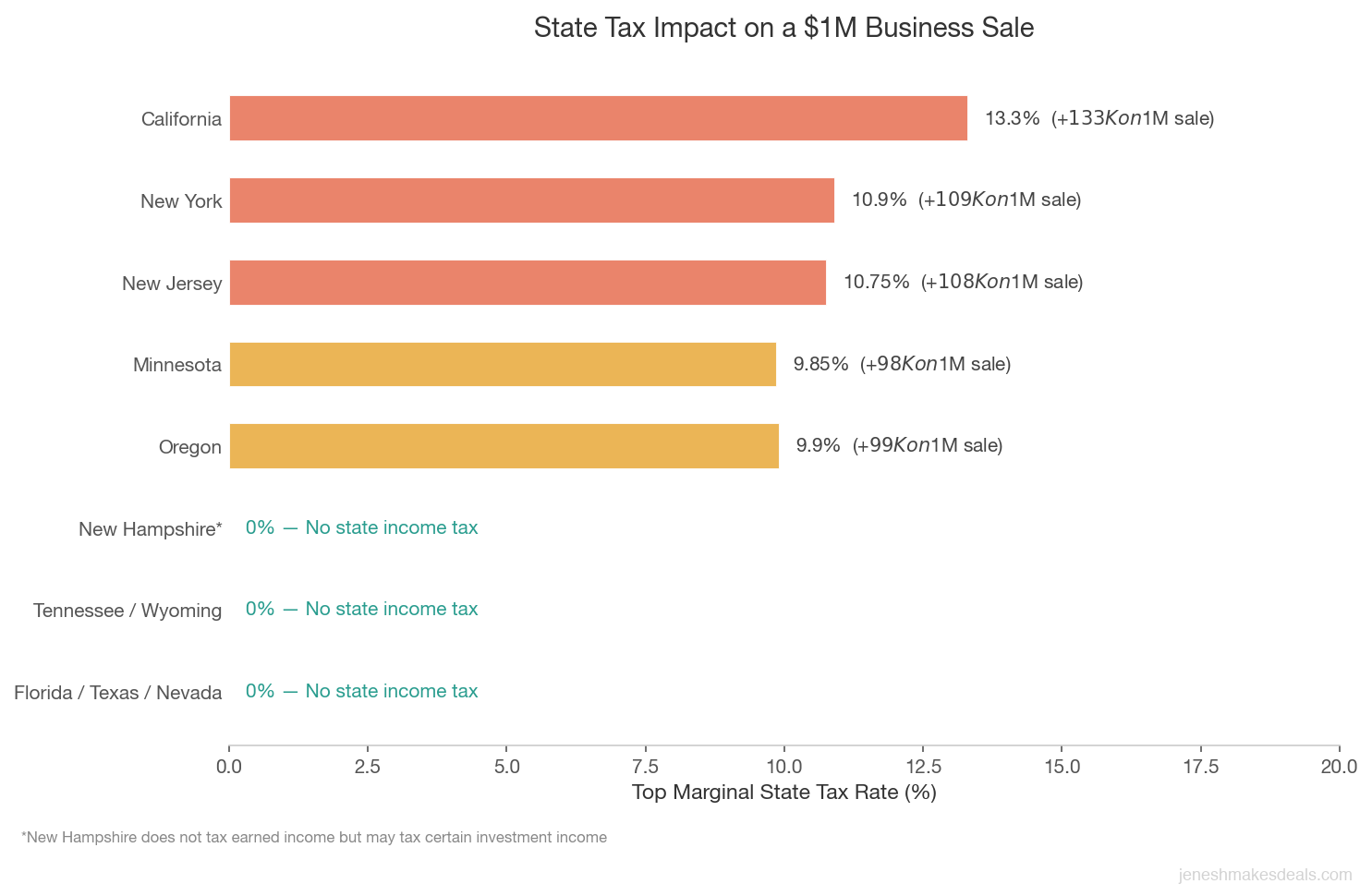

States with no income tax (and therefore no state tax on business sale gains): Alaska, Florida, Nevada, New Hampshire (on earned income), South Dakota, Tennessee, Texas, Washington, Wyoming.

High tax states:

- California: up to 13.3% (no distinction between ordinary income and capital gains)

- New York: up to 10.9%

- New Jersey: up to 10.75%

- Oregon: up to 9.9%

- Minnesota: up to 9.85%

If you live in California and sell a business for $1 million in profit, you could owe an additional $133,000 in state taxes on top of your federal bill. That's a meaningful amount of money.

| State | Top Tax Rate | Additional Tax on $1M Sale |

|---|---|---|

| Florida, Texas, Nevada | 0% | $0 |

| South Dakota, Wyoming | 0% | $0 |

| Oregon | 9.9% | $99,000 |

| Minnesota | 9.85% | $98,500 |

| New Jersey | 10.75% | $107,500 |

| New York | 10.9% | $109,000 |

| California | 13.3% | $133,000 |

A few things to know about state taxes and business sales:

Your state of residence matters. Most states tax you based on where you live, not where the business operates. If you live in California but the business is in Nevada, California still wants their cut.

Moving before the sale. Some sellers consider relocating to a no income tax state before selling. This can work, but you need to do it right. Most states have "clawback" rules. California, for example, can tax you on gains if you were a resident when the business appreciated in value, and they look back at residency changes that happen close to a sale. You typically need to establish genuine residency in the new state 12 to 18 months before the sale for this to work.

Multistate businesses. If your business operates in multiple states, the gain may need to be apportioned across those states. This gets complicated fast and is another reason to work with a tax professional.

Need help figuring out what your business is worth? Use our free business valuation calculator to get a quick estimate.

Installment Sales and Tax Deferral

If you're offering seller financing as part of the deal, there's a potential tax benefit: the installment sale method under IRC Section 453.

With an installment sale, you report the gain proportionally as you receive payments rather than all at once in the year of sale. This can spread the tax liability over several years and potentially keep you in lower tax brackets each year.

Here's an example. You sell your business for $1 million with $300,000 down and $700,000 in seller financing paid over seven years. Your basis in the business is $200,000, so your total gain is $800,000. Your gross profit percentage is 80% ($800,000 gain divided by $1,000,000 sale price).

In the year of sale, you receive $300,000. Of that, 80% ($240,000) is taxable gain. The remaining $60,000 is return of basis. Over the next seven years, 80% of each annual payment is taxable gain.

Instead of reporting $800,000 in gains in one year (pushing you into the highest brackets), you're reporting smaller amounts each year. Depending on your other income, this could keep you in the 15% capital gains bracket instead of the 20% bracket, saving you 5% on hundreds of thousands of dollars.

When installment sales make sense:

- When you're okay with seller financing and the buyer is creditworthy

- When reporting all the gain in one year would push you into significantly higher brackets

- When you want to reduce your exposure to the 3.8% NIIT

When they don't make sense:

- When you need all the cash immediately

- When the buyer's credit risk is high (you're deferring taxes on income you might not collect)

- When tax rates are expected to increase significantly in future years

Spreading a $800,000 gain over seven years through an installment sale could keep you in the 15% capital gains bracket instead of 20%, saving you 5% on hundreds of thousands of dollars. But depreciation recapture is always due in year one.

One gotcha: depreciation recapture is recognized in the year of sale regardless of whether you use the installment method. You can't defer that portion.

Qualified Small Business Stock (QSBS) Exclusion

Section 1202 of the tax code offers one of the most generous tax benefits available: the potential to exclude up to $10 million in capital gains (or 10 times your basis, whichever is greater) from the sale of qualified small business stock.

If you qualify, this could mean paying zero federal capital gains tax on your business sale. That's a massive benefit.

The requirements are strict:

- C corporation only. The business must be organized as a C corp. S corps, LLCs, partnerships, and sole proprietorships don't qualify.

- Original issuance. You must have acquired the stock at original issuance (not purchased from another shareholder).

- Five year holding period. You must have held the stock for at least five years.

- Active business requirement. At least 80% of the corporation's assets must be used in an active trade or business. Certain industries are excluded, including professional services (law, accounting, consulting, health), banking, insurance, farming, and hospitality.

- Aggregate gross assets. The corporation's aggregate gross assets must not have exceeded $50 million at the time the stock was issued and immediately after.

Here's the reality: most small business owners I work with don't qualify for QSBS. Many are structured as S corps or LLCs, which disqualifies them immediately. Others are in excluded industries. And the five year holding requirement means you can't just convert to a C corp right before selling.

But if you're early in your business journey and think you might sell someday, it's worth talking to a tax attorney about whether QSBS planning makes sense. The tax savings can be enormous.

Opportunity Zones and 1031 Exchanges

Two other tax deferral strategies come up frequently in business sale conversations: 1031 exchanges and Opportunity Zone investments.

1031 Exchanges

A 1031 exchange lets you defer capital gains taxes by reinvesting the proceeds into "like kind" property. But there's a catch for business sellers: 1031 exchanges only apply to real property (real estate). You can't do a 1031 exchange on goodwill, equipment, inventory, or other business assets.

If your business sale includes real estate (like you own the building the business operates in), you may be able to do a 1031 exchange on the real estate portion. The rest of the sale proceeds would still be taxable. This requires careful structuring. The real estate needs to be separated from the business sale, and you need to follow strict timelines (45 days to identify replacement property, 180 days to close).

Opportunity Zone Investments

After selling your business, you can defer and potentially reduce capital gains by investing in a Qualified Opportunity Fund (QOF) within 180 days of realizing the gain. The original tax law offered a step up in basis for investments held 5 or 7 years, but those deadlines have largely passed for new investments in 2026.

The remaining benefit is that if you hold the Opportunity Zone investment for at least 10 years, any appreciation on the new investment is tax free. This can be attractive if you're looking to reinvest sale proceeds into real estate or business ventures in designated Opportunity Zones.

The risk is that Opportunity Zone investments are illiquid and tied to specific geographic areas. You're making a 10 year commitment to get the full benefit. Don't let the tax tail wag the investment dog.

Tax Planning Strategies Before the Sale

The biggest mistake I see sellers make is waiting until the deal is almost done to think about taxes. By then, your options are limited. The best tax outcomes come from planning 12 to 24 months before the sale.

Here's what to think about ahead of time:

1. Entity structure review. If you're currently an LLC or S corp, converting to a C corp might make sense for QSBS treatment, but only if you can meet the five year holding period. For most sellers, this ship has sailed. But your current entity structure still affects how the sale is taxed, so understand the implications.

2. Purchase price allocation negotiation. The allocation of the purchase price across asset categories directly determines your tax bill. Sellers generally want more allocated to goodwill (capital gains) and less to inventory and non competes (ordinary income). Work with your CPA to model different allocation scenarios before you negotiate with the buyer.

3. Timing of the sale. If you have a low income year, selling in that year could keep more of your gain in lower tax brackets. Conversely, if you're expecting a windfall from another source, you might want to time the sale differently.

4. Installment sale planning. If spreading the gain over multiple years makes sense, structure the seller financing terms to optimize your tax brackets in each year.

5. Charitable giving strategies. If you're charitably inclined, a Charitable Remainder Trust (CRT) can let you sell appreciated business assets, defer the capital gains tax, receive an income stream, and get a charitable deduction. This is complex and requires specialized legal help, but the tax benefits can be significant.

6. Increase your basis. Any capital improvements or investments you make in the business before the sale increase your cost basis and reduce your taxable gain. If you've been putting off equipment purchases or building improvements, doing them before the sale can serve double duty: they increase the business value and reduce your tax liability. Focus on increasing your business value in ways that also boost your basis.

7. State residency planning. If you're in a high tax state and the sale is a year or more away, consider whether relocating makes financial sense. This is a big life decision that shouldn't be made solely for tax reasons, but the savings can be substantial. A $2 million sale in California could cost you $266,000 in state taxes that you'd avoid in Florida or Texas.

Ready to talk about selling? Contact us for a free consultation and we'll walk you through your options.

Putting It All Together: A Real World Example

Let me walk through a simplified example that ties everything together.

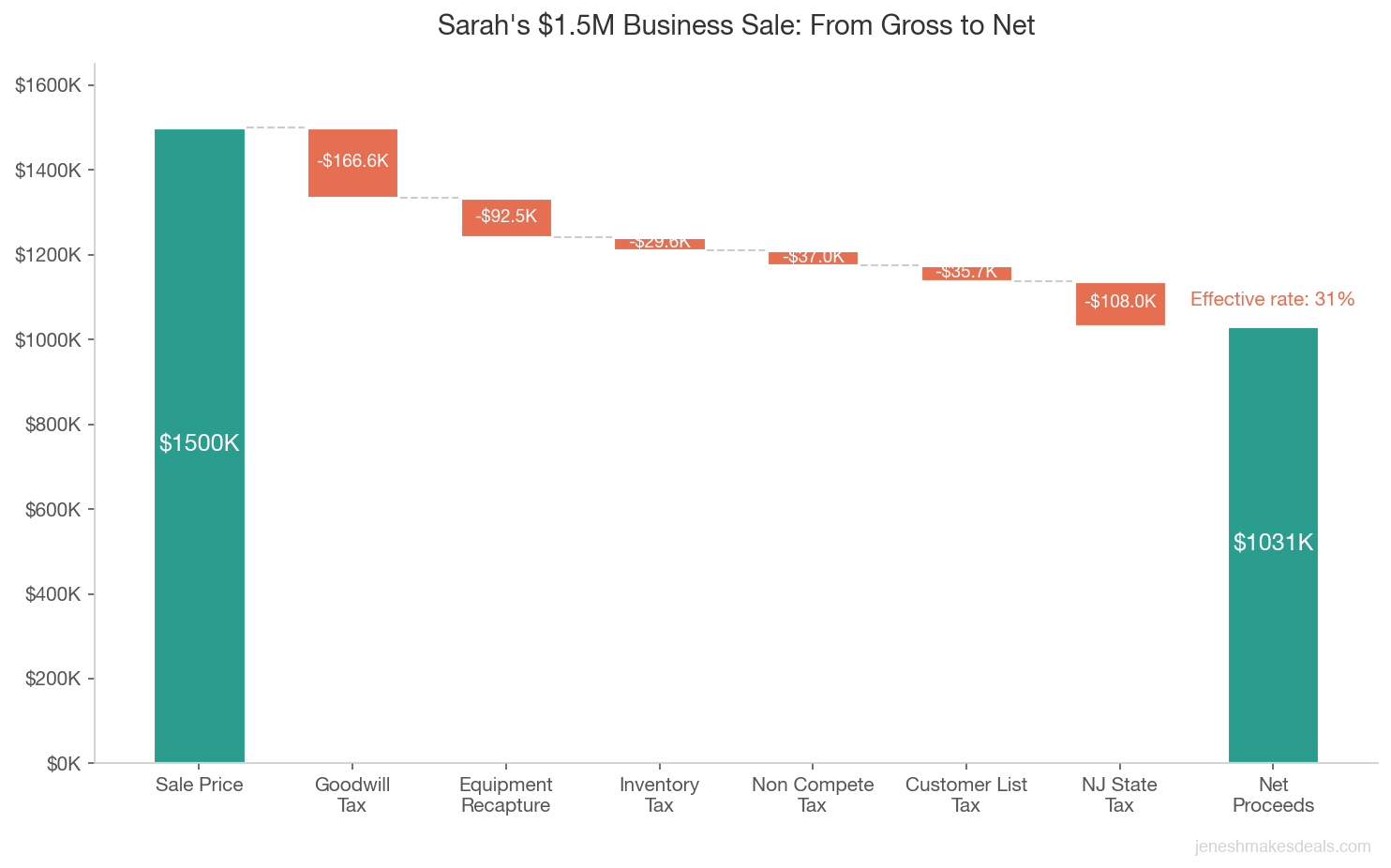

Sarah owns a manufacturing business in New Jersey. She's been running it for 12 years. She's organized as an S corp. A buyer offers $1.5 million as an asset sale.

Purchase price allocation:

- Goodwill: $700,000

- Equipment: $350,000 (original cost $500,000, accumulated depreciation $400,000, adjusted basis $100,000)

- Inventory: $200,000

- Non compete agreement: $100,000

- Customer list: $150,000

Federal tax calculation:

Goodwill ($700,000): Long term capital gains. Assuming 23.8% rate (20% + 3.8% NIIT) = $166,600.

Equipment ($350,000): Gain is $250,000 ($350,000 minus $100,000 basis). Of that, $250,000 is depreciation recapture taxed at ordinary income rates. At 37% = $92,500. (The sale price doesn't exceed the original $500,000 cost, so it's all recapture.)

Inventory ($200,000): Ordinary income. Assuming cost basis of $120,000, gain is $80,000. At 37% = $29,600.

Non compete ($100,000): Ordinary income. At 37% = $37,000.

Customer list ($150,000): Long term capital gains at 23.8% = $35,700.

Total federal tax: approximately $361,400

New Jersey state tax: New Jersey taxes capital gains as ordinary income at rates up to 10.75%. On the total gain (roughly $1,080,000 after adjusting for basis), the state tax could be approximately $100,000 to $116,000.

Total estimated tax: approximately $461,000 to $477,000

Sarah sells for $1.5 million and keeps roughly $1,023,000 to $1,039,000. That's a 31% to 32% effective tax rate on the total sale price.

If Sarah had structured this differently (stock sale, installment payments, better purchase price allocation), she might have kept an additional $50,000 to $100,000. That's real money.

On a $1.5 million sale, the difference between a well structured deal and a poorly structured one is $50,000 to $100,000 in after tax proceeds. That's the cost of not planning ahead.

Note: This example is simplified for illustration. Actual tax calculations involve many more variables. Please work with a CPA for your specific situation.

What to Do Next

Tax planning for a business sale isn't something you figure out on closing day. The sellers who keep the most money are the ones who start planning a year or two before they list.

Here's my recommendation:

-

Get a valuation. You can't plan for taxes on a sale until you know roughly what the business is worth. That gives you a starting point for modeling different scenarios.

-

Talk to a CPA and tax attorney. Not a general practitioner. Find someone who specializes in business sales and transactions. The fee for good tax planning is tiny compared to the tax savings.

-

Talk to a business broker. I can help you understand how deal structure affects your after tax proceeds and work with your tax team to structure the sale in the most favorable way.

-

Start early. Some strategies (QSBS, state residency changes, entity restructuring) require years of lead time. Even strategies that don't require as much time, like purchase price allocation planning, work better when you're not under deadline pressure.

The tax code is complicated, but the core principle is simple: plan ahead, structure smartly, and get good professional advice. The difference between a well planned sale and an unplanned one can easily be six figures. To see how taxes, broker fees, and legal costs add up for your deal, model your total transaction costs here.

Ready to start planning your exit? Contact us for a free consultation. I'll help you think through the deal structure and connect you with tax professionals who specialize in business sales. For a full overview of every step in the selling process, including deal structure and negotiation, download our free Complete Guide to Selling Your Business in 2026.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.