Strategic Buyer vs Financial Buyer: Which Is Right for Your Business Sale?

When you sell your business, the type of buyer sitting across the table changes everything. I'm not talking about personality or negotiation style. I'm talking about how they calculate your company's worth, how they structure the deal, and how much cash you walk away with at closing.

In my work as a business broker, I've seen the same $2 million revenue company get a $3.5 million offer from one buyer and a $6.2 million offer from another. The difference? One was a financial buyer running a spreadsheet model. The other was a strategic buyer who saw the acquisition as a shortcut to 18 months of organic growth.

The type of buyer determines the math. Strategic buyers pay for what the business becomes inside their operation. Financial buyers pay for what it produces on its own.

Understanding the difference between strategic buyers and financial buyers affects your pricing, your marketing, your deal timeline, and the terms you'll negotiate. Let me break it all down.

What Is a Strategic Buyer?

A strategic buyer is a company that acquires your business because it fits into their existing operations. They're not just buying your revenue. They're buying access to your customers, your geography, your technology, your team, or your supply chain.

A strategic buyer already operates in your industry or an adjacent one. They look at your business and see ways to combine it with what they already have. The result is a company worth more together than the two pieces separately. That's what people in M&A call "combined value."

Here are some real world examples I've seen:

- A regional HVAC company with $4 million in revenue gets acquired by a national home services platform. The buyer wanted their 2,300 customer contracts and three licensed technicians in a market they hadn't entered yet.

- A $1.5 million ecommerce brand selling pet supplements gets bought by a larger pet products company. The buyer wanted the brand's 180,000 social media followers and its Amazon ranking for 40+ keywords.

- A $900,000 revenue accounting firm gets acquired by a mid size CPA firm expanding into a new state. The buyer wanted the seller's 200+ recurring tax clients.

In each case, the buyer paid a premium over what the business was "worth" on a pure cash flow basis. That premium exists because the buyer can extract value that a standalone owner can't.

What Drives Strategic Buyers

Strategic buyers are motivated by growth that would take too long or cost too much to build organically:

- Market expansion. Entering a new city, state, or region through acquisition instead of building from scratch.

- Customer acquisition. Buying an established customer base is faster than marketing for 2 to 3 years.

- Vertical integration. A manufacturer buying a distributor to control more of the supply chain.

- Technology or IP. Acquiring proprietary software, patents, or processes rather than developing them internally.

- Eliminating competition. Buying a competitor to consolidate market share and reduce pricing pressure.

What Is a Financial Buyer?

A financial buyer acquires your business primarily as an investment. They're focused on the returns the business can generate over a defined holding period, typically 3 to 7 years. The business needs to stand on its own and produce predictable cash flow.

Financial buyers come in several forms:

- Private equity firms. From lower middle market PE funds (acquiring businesses with $1 million to $5 million in EBITDA) to large funds targeting $50 million+ deals.

- Search funds. Typically one or two MBA graduates who raise capital to find and buy a single business in the $500,000 to $3 million SDE range.

- Individual buyers. High net worth individuals looking to replace their W2 income with a business producing $200,000 to $1 million in annual owner earnings.

- Family offices. Wealth management entities buying businesses for long term cash flow, often with longer hold periods than traditional PE.

What Drives Financial Buyers

Financial buyers care about one thing above all else: return on invested capital. Their key concerns include:

- Cash flow stability. Consistent, predictable earnings over 3+ years. Lumpy revenue scares them.

- Owner dependence. If the business can't run without you, a financial buyer sees risk.

- Debt capacity. Most use SBA loans, seller financing, or fund level debt to amplify returns. The business needs to service that debt comfortably.

- Exit opportunity. PE firms are already thinking about who they'll sell to in 5 years when they buy it today.

How Each Buyer Type Values Your Business

This is where the difference gets real. Strategic and financial buyers use fundamentally different math to arrive at a price.

Financial Buyer Valuation

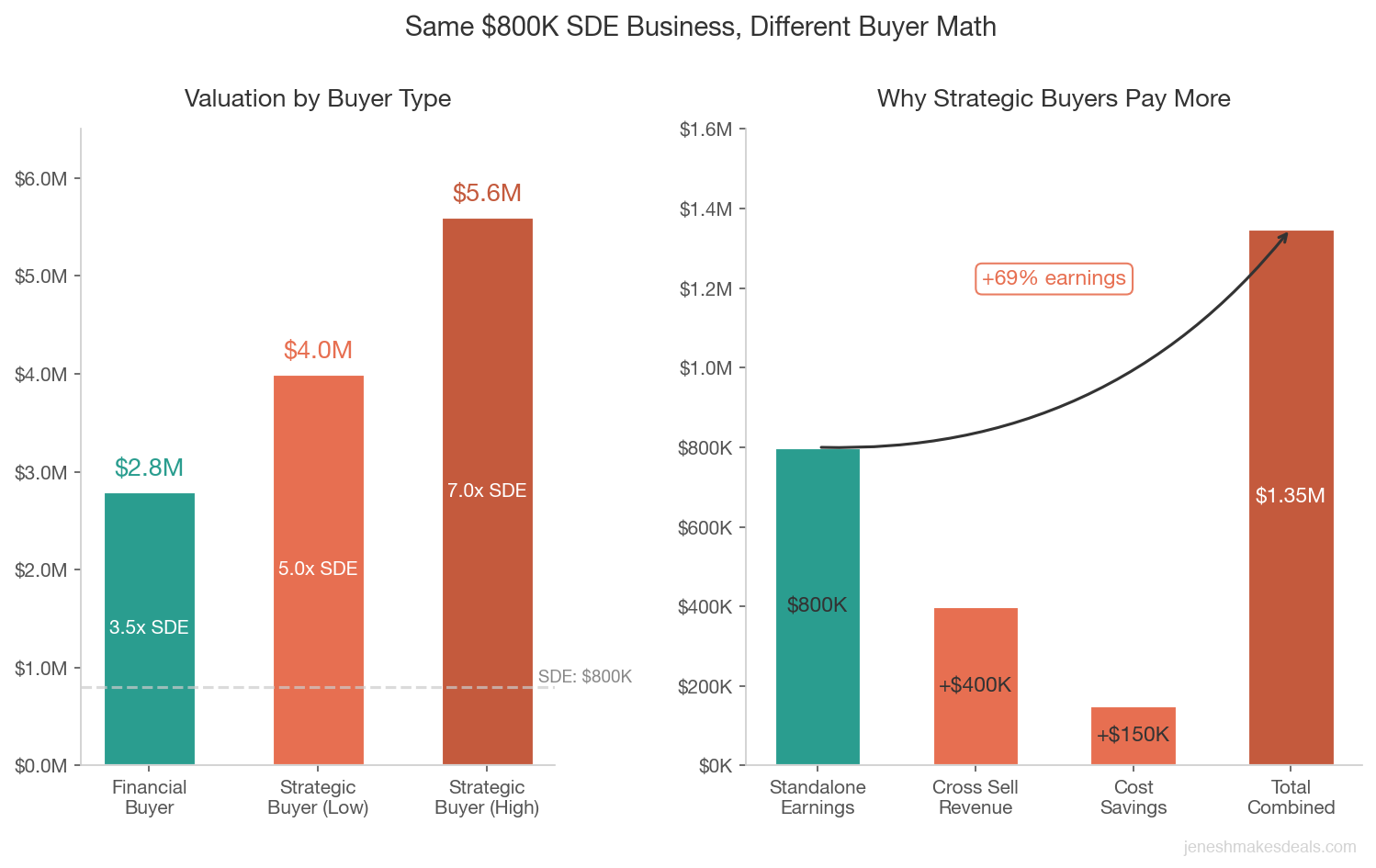

Financial buyers start with your seller's discretionary earnings (SDE) or EBITDA and apply a market multiple. For most small businesses with $500,000 to $3 million in SDE, you're looking at 2.5x to 4.5x SDE. Larger businesses with $3 million+ EBITDA might command 5x to 7x.

Example: your business generates $800,000 in SDE. A financial buyer applies a 3.5x multiple based on comparable transactions. That gives you a valuation of $2.8 million. They then work backward from their return target, staying disciplined about not overpaying.

For a deeper look at how these multiples work, check out my post on business valuation methods explained.

Strategic Buyer Valuation

Strategic buyers start with the same baseline, then add combined value on top.

Using that same $800,000 SDE business, a strategic buyer sees that acquiring your customer base will add $400,000 in annual revenue within 12 months through cross selling. They also expect to save $150,000 per year by eliminating duplicate overhead like office space and insurance.

Now they're not just valuing $800,000 in earnings. They're valuing a combined operation that generates an additional $550,000 per year. That same business might get a 5x to 7x multiple from a strategic buyer, resulting in $4 million to $5.6 million. That's 43% to 100% more than the financial buyer's offer.

Side by Side Comparison

| Factor | Financial Buyer | Strategic Buyer |

|---|---|---|

| Valuation basis | Standalone cash flow (SDE/EBITDA) | Cash flow + combined value |

| Typical multiple (small biz) | 2.5x to 4.5x SDE | 4x to 7x+ SDE |

| Typical multiple (mid market) | 4x to 7x EBITDA | 6x to 12x+ EBITDA |

| Premium over market | At or near market value | 20% to 100%+ premium |

| What they're buying | Cash flow and growth potential | Customers, market share, technology, talent |

Which Buyer Type Pays More (and When)?

On average, strategic buyers pay 20% to 50% more than financial buyers for the same business. But "more" isn't always "better."

Strategic buyers pay the highest premiums when your business has something they can't easily replicate, such as proprietary technology, exclusive contracts, or a brand with real customer loyalty. If they'd need 2 to 3 years and $2 million in marketing spend to build what you've already built, they'll pay handsomely to skip that. Premiums also spike when consolidation is happening in your industry and multiple acquirers compete for the same targets.

Financial buyers might actually be the right choice when you want a clean exit with more cash at closing. SBA backed individual buyers often put 70% to 90% of the price in cash at close, while strategic buyers sometimes pay 40% to 60% in stock, earnouts, or deferred payments. Individual buyers and search fund operators also tend to preserve your existing team and culture, whereas a strategic buyer might consolidate operations within 6 months.

A $6 million offer with $2.5 million in earnouts is not a $6 million deal. Always evaluate offers based on guaranteed cash at closing, not headline price.

Which Buyer Is Right for Your Situation?

| Your Priority | Best Fit | Why |

|---|---|---|

| Maximum total price | Strategic buyer | Combined value premiums of 20% to 100%+ |

| Most cash at closing | Financial buyer | 70% to 90% cash vs 40% to 60% from strategic |

| Clean, fast exit | Financial buyer (individual) | SBA deals close in 60 to 90 days |

| Preserving team and culture | Financial buyer (search fund) | They typically keep existing staff |

| Highest price, willing to stay involved | Strategic buyer with earnout | Earn more if you hit performance targets |

| Second bite of the apple | PE firm with equity rollover | Roll 10% to 20%, cash out again at higher valuation |

Wondering what your business might be worth to each type of buyer? Try our free valuation calculator to get a baseline estimate.

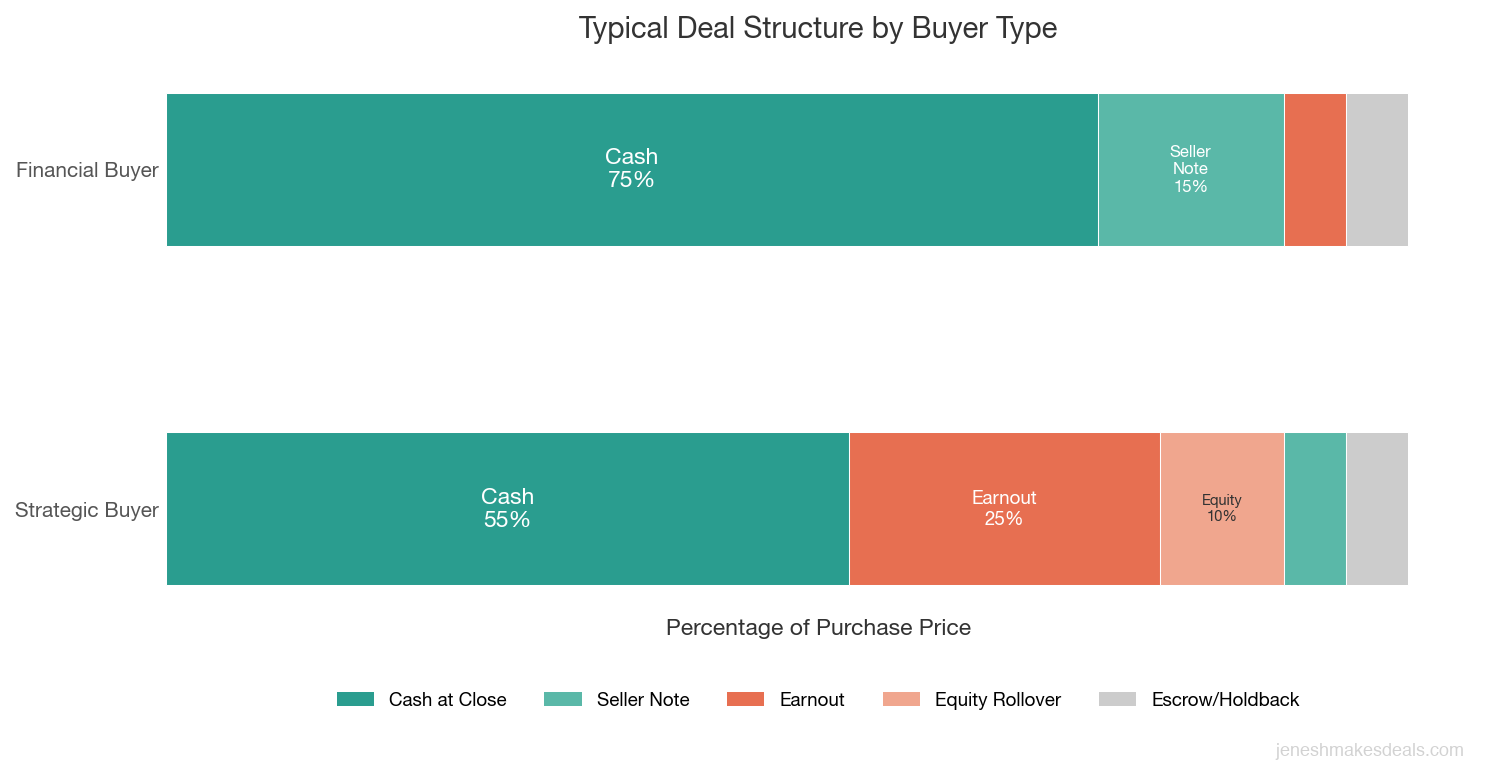

Deal Structure Differences

The purchase price is just one number. How that price gets paid matters just as much.

| Deal Term | Financial Buyer | Strategic Buyer |

|---|---|---|

| Cash at closing | 60% to 90% of purchase price | 40% to 80% of purchase price |

| Seller financing | Common (10% to 30% of deal) | Less common |

| Earnout component | Less common (10% to 20% of deals) | Very common (30% to 50% of deals) |

| Equity rollover | Sometimes (PE offers 10% to 20%) | Common with large private buyers |

| Escrow/holdback | 5% to 10% for 12 to 18 months | 10% to 15% for 12 to 24 months |

| Non compete term | 2 to 3 years, narrow scope | 3 to 5 years, broader scope |

| Due diligence timeline | 30 to 60 days | 60 to 120 days |

| Total close timeline | 60 to 120 days | 90 to 180 days |

The Earnout Factor

Earnouts deserve special attention when selling to strategic buyers. An earnout is a portion of your purchase price contingent on the business hitting certain targets after the sale closes. You might get $4 million at closing plus $1.5 million if the business hits $2 million in revenue in each of the next two years.

Strategic buyers love earnouts because they reduce risk. If the synergies don't materialize, they pay less. From your side, earnouts introduce uncertainty. You're giving up control but still depending on performance for part of your payout.

I've written a detailed breakdown of how earnouts work. Read it here: What Is an Earnout in a Business Sale?

The Equity Rollover

PE firms sometimes ask sellers to "roll over" 10% to 20% of their equity into the new ownership structure. When the PE firm sells the business again in 5 to 7 years at a higher valuation, your stake is worth more.

I've seen sellers who rolled over 15% of a $3 million deal end up with a second payout of $1.2 million when the PE firm exited 4 years later. But if the PE firm doesn't grow the business as planned, your rollover equity could be worth less than what you gave up.

How to Position Your Business for Each Buyer Type

Positioning for Strategic Buyers

Highlight your customer base. Document your customer count, retention rate, average revenue per customer, and geographic distribution. If you have 500 recurring commercial clients in a metro area the buyer hasn't entered, that's your headline.

Quantify the combination potential. Don't make the buyer guess. Show how your 2,300 residential customers represent $460,000 in annual cross sell opportunity for a buyer with complementary services.

Protect your IP and contracts. Make sure proprietary processes, software, or exclusive agreements are properly documented and legally assigned to the business entity.

Reduce transition risk. Build a management team that can operate without you. If you are the entire platform, the integration risk is too high to justify a premium price.

Positioning for Financial Buyers

Clean up your financials. Eliminate personal expenses running through the business. Reconcile any discrepancies in 3 to 5 years of tax returns, P&Ls, and balance sheets.

Prove recurring revenue. A business with 70% recurring revenue gets a meaningfully higher multiple than one dependent on new sales every month.

Document your systems. Create SOPs for key functions. Financial buyers need to know the business runs without the current owner.

Show a growth runway. Identify 2 to 3 specific growth opportunities you haven't pursued, and be honest about why.

Minimize customer concentration. If one customer accounts for more than 15% of revenue, that's a red flag. Diversify before going to market.

For guidance on evaluating buyers, read my post on how to screen buyers for your business.

Need help figuring out if your business is ready to go to market? Schedule a free consultation to discuss your options.

Common Mistakes Sellers Make

Mistakes With Strategic Buyers

Accepting the first offer without creating competition. Running a process with 3 to 5 strategic prospects creates competitive tension. I've seen this single tactic add 15% to 30% to the final price.

Not quantifying combined value. If you don't help the buyer see the added benefits, they won't price them in. Show how your $3 million revenue business combined with their $20 million operation creates $1 million in new revenue or $500,000 in cost savings within 18 months.

Ignoring the earnout structure. A $6 million offer with $2.5 million in earnouts is not a $6 million deal. It's a $3.5 million deal with a chance to earn more. Always evaluate offers based on guaranteed cash at closing.

Giving away confidential information too early. Strategic buyers are often competitors. Make sure you have a strong NDA in place and that the buyer has demonstrated serious intent before sharing customer lists or trade secrets.

Mistakes With Financial Buyers

Overvaluing based on strategic comps. Just because a competitor sold for 6x EBITDA to a strategic acquirer doesn't mean your business is worth 6x to a financial buyer. Financial buyers don't get that combined premium.

Not preparing for SBA requirements. About 60% of small business acquisitions involve SBA financing. If your financials are messy or your lease isn't transferable, the lender will flag it.

Being inflexible on seller financing. Financial buyers often need the seller to carry 10% to 20% of the purchase price. A $200,000 seller note on a $2 million deal, paid back over 3 years at 6% interest, can be a smart way to close while earning a return.

Underestimating management team importance. A business that can't function without the owner is worth 20% to 30% less to a financial buyer. Build a team before you sell.

Real World Examples

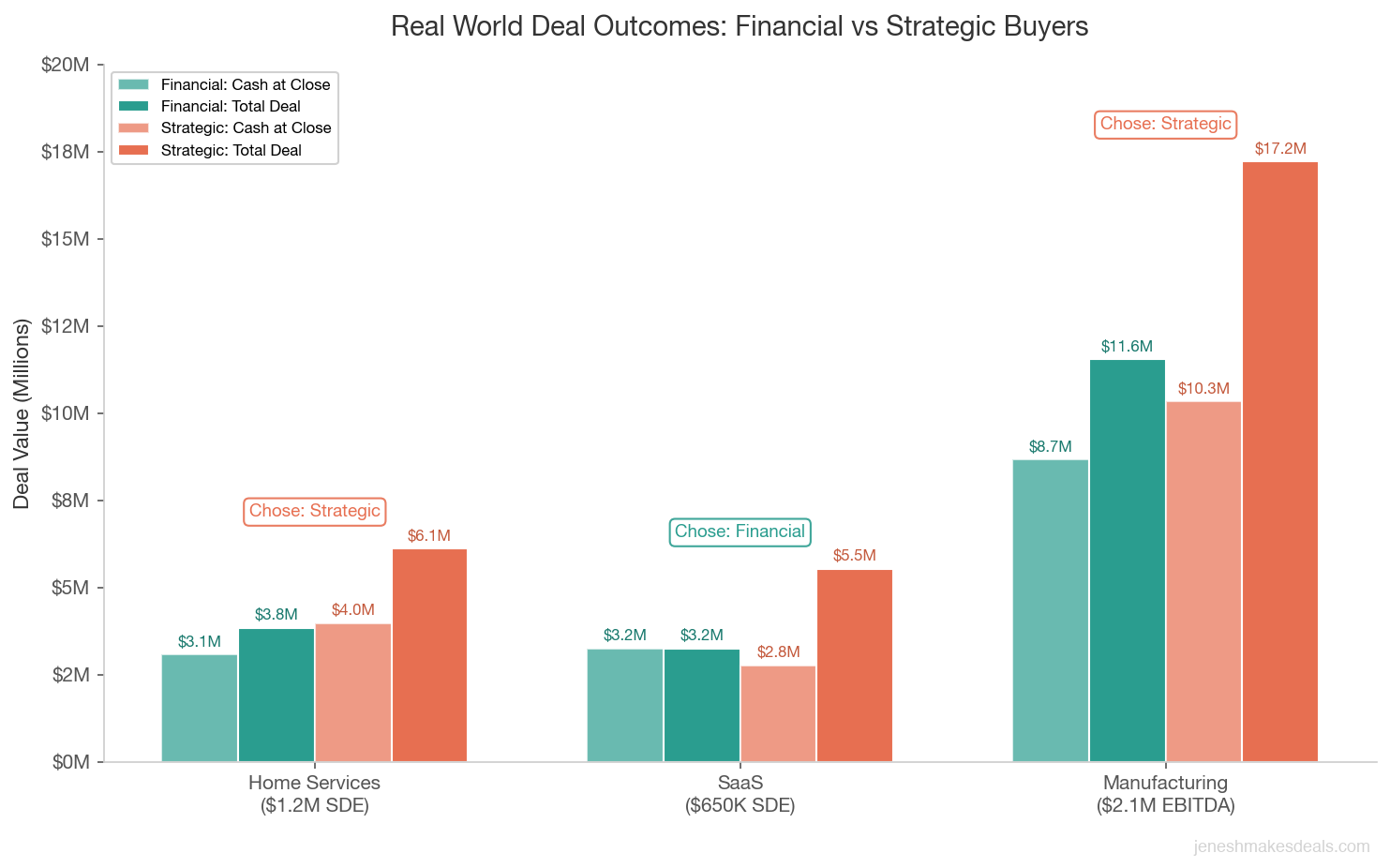

Example 1: Home Services Company

A residential plumbing company with $1.2 million in SDE and $3.8 million in revenue.

Financial buyer offer: 3.2x SDE = $3.84 million. Individual buyer using SBA financing. Structure: 80% cash at close ($3.07 million), 10% seller note ($384,000 over 3 years), 10% escrow.

Strategic buyer offer: 5.1x SDE = $6.12 million. PE backed home services roll up wanting 1,800 customer contracts and 8 licensed plumbers. Structure: 65% cash ($3.98 million), 20% earnout tied to customer retention ($1.22 million over 2 years), 15% equity rollover.

Result: The seller chose the strategic buyer. Guaranteed cash at close was $910,000 higher, plus the earnout and rollover upside. Both earnout targets were hit, and the seller received approximately $5.6 million total.

Example 2: SaaS Business

A B2B SaaS product for dental practices with $650,000 in SDE, $1.4 million in ARR, and 92% gross margin.

Financial buyer offer: 5x SDE = $3.25 million. PE firm focused on vertical SaaS. All cash at close.

Strategic buyer offer: 8.5x SDE = $5.53 million. Large dental supply company. Structure: 50% cash ($2.76 million), 30% earnout tied to ARR growth over 3 years, 20% stock in parent company.

Result: The seller chose the financial buyer. All cash meant $3.25 million guaranteed vs only $2.76 million at close from the strategic offer. The seller didn't want to stay involved for 3 years, and the stock was illiquid. Sometimes the "lower" offer is the better deal.

Example 3: Manufacturing Business

A specialty food manufacturer with $2.1 million in EBITDA, $9.5 million in revenue, FDA certifications, and two proprietary formulations.

Financial buyer offer: 5.5x EBITDA = $11.55 million from a PE fund. Structure: 75% cash, 15% equity rollover, 10% seller note.

Strategic buyer offer: 8.2x EBITDA = $17.22 million from a national food brand. Structure: 60% cash ($10.33 million), 25% stock, 15% earnout.

Result: The seller negotiated the strategic buyer up from 7x to 8.2x by creating competitive tension between two strategic bidders. Even at 60% cash, the guaranteed close amount ($10.33 million) exceeded the financial buyer's total offer. The earnout paid out in full.

Ready to explore what your business could be worth? Use our valuation tools to start running the numbers.

How to Attract Both Buyer Types

The best outcomes happen when sellers market to both buyer types simultaneously.

Build a CIM that speaks to both audiences. Include the clean financial data financial buyers want, plus sections on market position, customer characteristics, and combination potential that strategic buyers care about.

Build a targeted buyer list. Work with your broker to identify 5 to 10 financial buyers (PE firms, search funds, individuals) and 5 to 10 strategic buyers (competitors, adjacent companies, roll up platforms).

Compare offers on total value, not headline price. Score each offer on guaranteed cash at closing, probability weighted earnout value (discount by 30% to 50%), equity component (discounted for illiquidity), transition requirements, tax implications, and non compete restrictions.

Don't rush to accept. Counter offers, competitive pressure, and creative structuring can add 10% to 25% to total proceeds if you're patient.

Running a competitive process with 3 to 5 prospects from each buyer type creates the tension that drives the best offers. The smartest sellers never pick one path upfront.

The Bottom Line

Strategic buyers and financial buyers aren't better or worse. They're different tools for different situations. Strategic buyers typically pay more, but their deals take longer and often include earnout risk. Financial buyers offer cleaner deals with more cash at closing, but at lower headline prices.

The smartest sellers I work with don't pick one or the other upfront. They prepare their business to appeal to both types, run a competitive process, and let the offers tell them which path produces the best outcome.

The preparation you do before going to market, from cleaning up financials to documenting processes to identifying potential strategic acquirers, determines which buyers show up and how much they're willing to pay.

Want to figure out the right buyer strategy for your business? Reach out for a free, confidential conversation about your goals and timeline. I'll help you understand your options and build a plan to get the best deal possible.

If you want a full overview of what selling looks like from start to finish, grab our free Complete Guide to Selling Your Business in 2026.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.