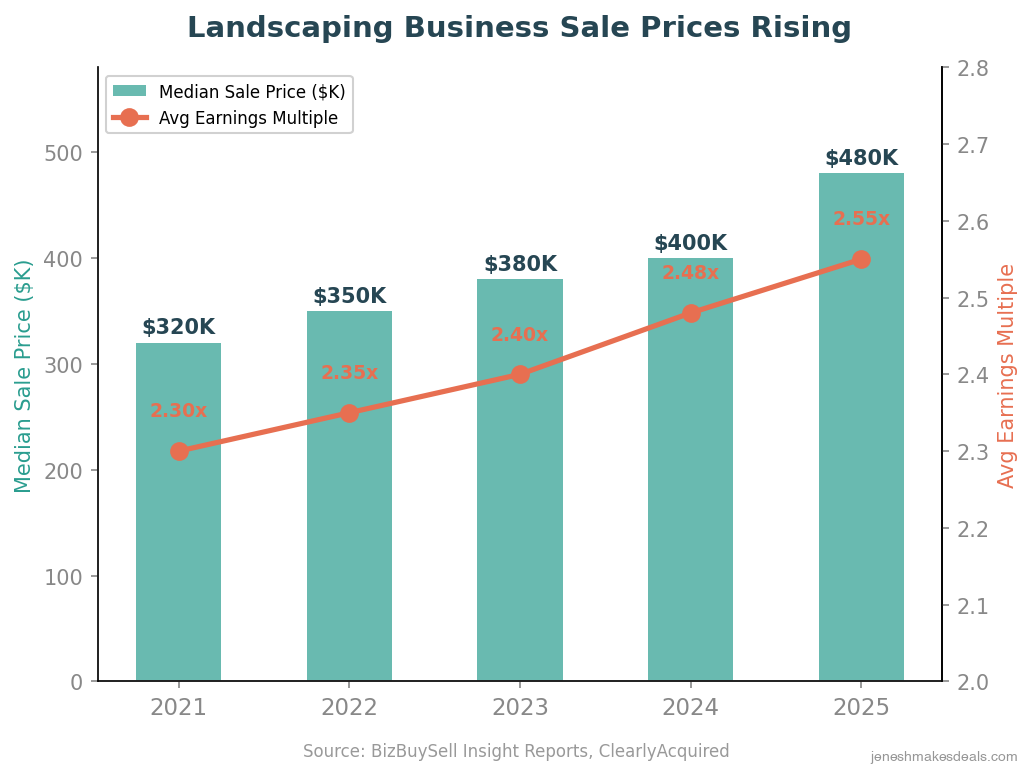

Private equity firms closed over 100 landscaping deals in 2025. The median sale price hit $480,000, up 20% from the previous year. Average earnings multiples climbed from 2.3 in 2021 to 2.55 in 2025. If you own a landscaping business and you've been thinking about selling, the numbers are saying now.

But a strong market doesn't mean every seller gets a strong outcome. The difference between a landscaping company that sells for $2.5 million and one that sells for $1.2 million on the same revenue usually comes down to preparation, timing, and knowing what buyers actually want.

This is the tactical guide. I'll walk you through the exact steps to sell your landscaping business at peak value in 2026, from when to list, to what multiples look like across business types, to the full PE deal landscape, to a month by month pre sale playbook. If you're 12 to 24 months from a sale, this is your roadmap.

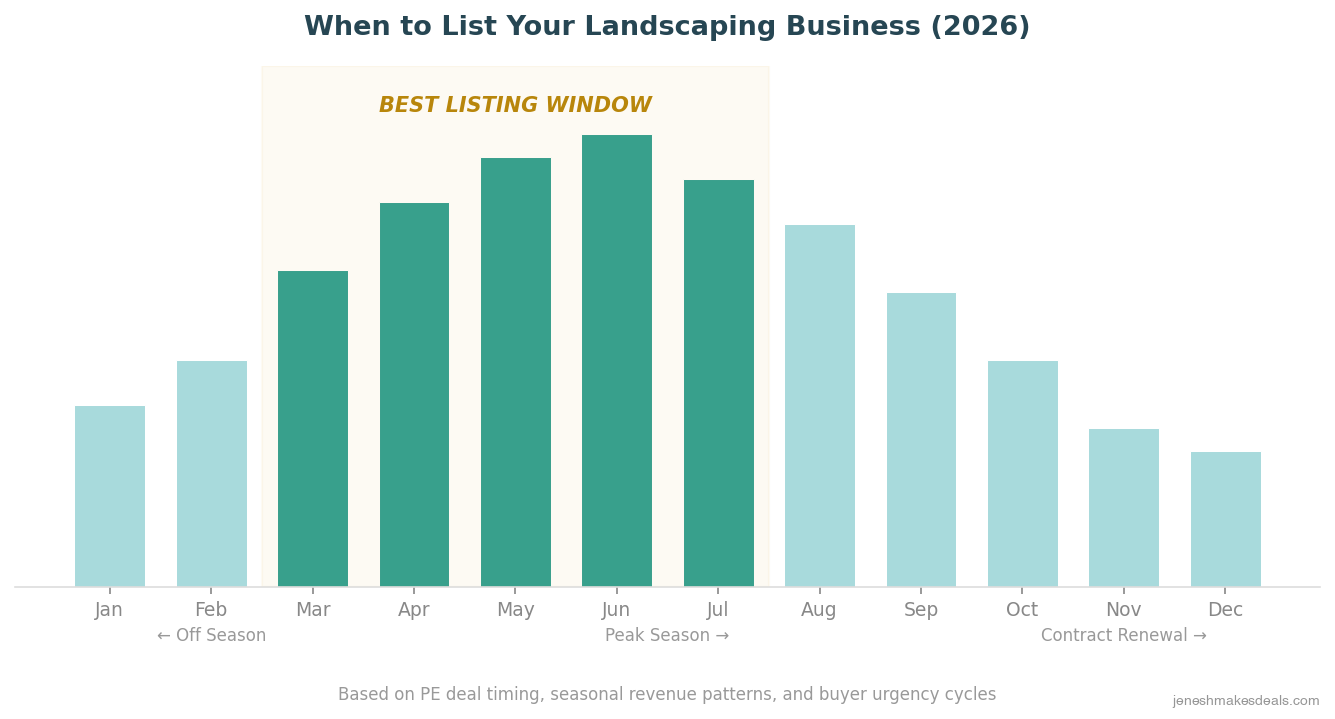

When to List: The 2026 Timing Window

Timing your listing isn't about picking a random date. It's about aligning your financials, buyer activity, and seasonal dynamics to create the strongest possible position.

Late Q1 through early Q3 2026 is the sweet spot. Here's why. Your trailing twelve month financials at that point include a full peak season from April through September. That means your SDE and EBITDA numbers reflect your best revenue months. Buyers see the strongest version of your business.

Buyer urgency peaks in spring and summer too. PE firms operate on annual deployment calendars and push hard to close before year end portfolio deadlines. Listing in Q2 means you're in front of active buyers with allocated capital and a ticking clock.

There's also a contract renewal angle. If your maintenance contracts renew between October and December, those renewals demonstrate forward revenue to prospective buyers. A book of signed contracts going into next season is one of the strongest signals you can send during due diligence.

The market data supports moving quickly. The median landscaping business now sells in 149 days on market, the fastest pace since 2017. Among owners surveyed, 55% believe they can get their desired price right now, but 60% worry that waiting could yield the same or a lower result. The market is telling sellers to act while conditions are strong.

Want to know what your landscaping business is worth today? Use our free landscaping valuation calculator to get an estimate based on your SDE and business profile.

What Landscaping Businesses Are Actually Selling For

Valuation in landscaping is not one number. It depends heavily on your revenue mix, business size, and what kind of buyer you're selling to. Here's how the multiples break down.

SDE Multiples by Business Type

| Business Type | SDE Multiple Range | What Drives It |

|---|---|---|

| Recurring maintenance contracts | 3.5x to 5.0x | Predictable cash flow, low churn |

| Balanced maintenance + project work | 3.0x to 4.5x | Revenue stability with upside |

| Hardscape and project only | 2.0x to 3.5x | Lower predictability, higher risk |

| Small residential (owner operated) | ~2.46x | Owner dependency, limited scalability |

The overall SDE multiple range for landscaping businesses sits at 2.76x to 3.21x according to Peak Business Valuation. Revenue multiples run 0.67x to 0.89x.

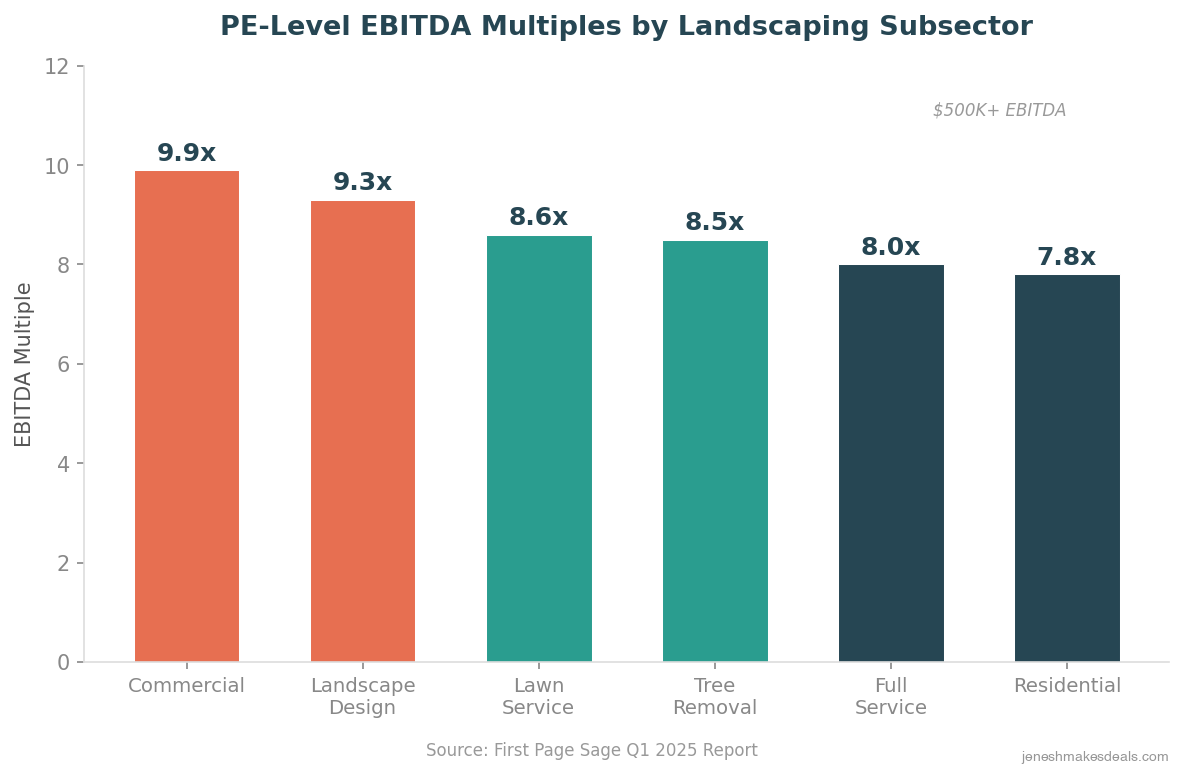

EBITDA Multiples (PE Level Deals)

For larger businesses attracting private equity buyers, EBITDA multiples run considerably higher.

| Segment | EBITDA Multiple |

|---|---|

| Commercial Landscaping | 9.9x |

| Landscape Design | 9.3x |

| Lawn Service | 8.6x |

| Tree Removal | 8.5x |

| Full Service | 8.0x |

| Residential | 7.8x |

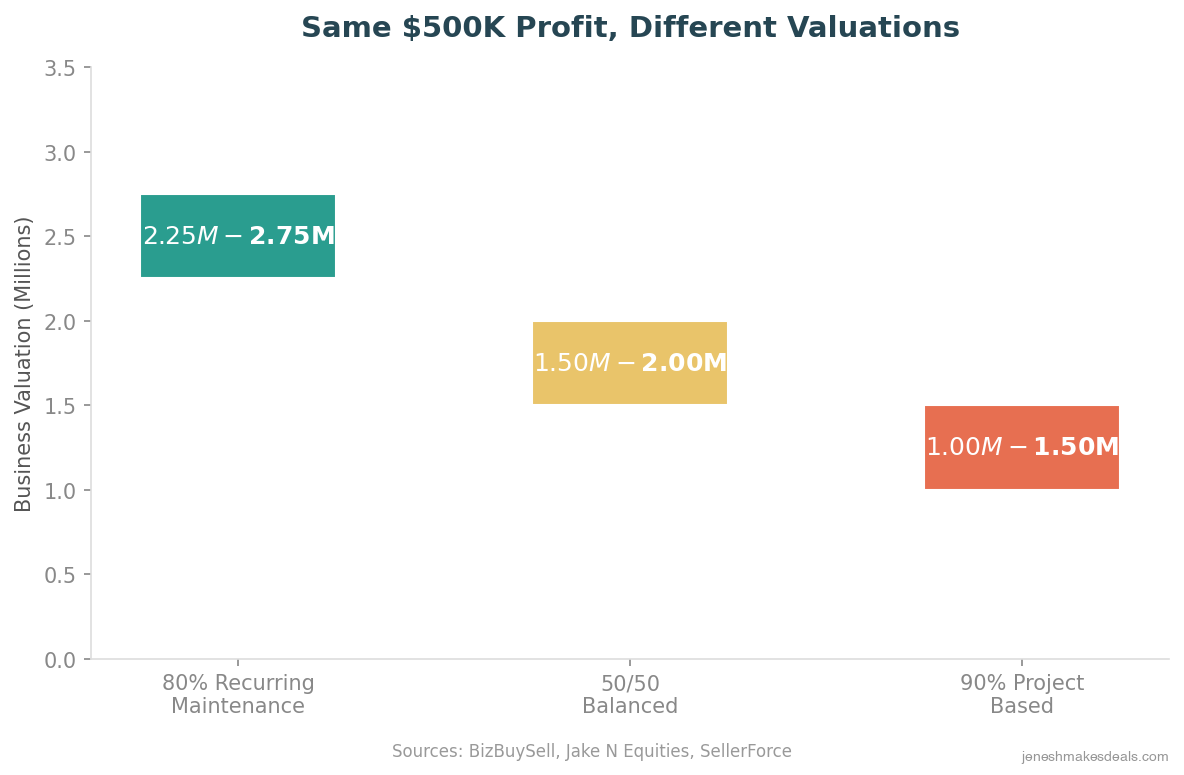

The Recurring Revenue Premium

This is the single most important thing to understand about landscaping valuations. Buyers value recurring revenue 2 to 3 times more than project revenue. The gap shows up clearly in real numbers.

A landscaping business with 80% recurring revenue and $500,000 in profit can sell for $2.25 to $2.75 million. A business with 90% project revenue and the same $500,000 profit fetches only $1.0 to $1.5 million. Same earnings. Dramatically different outcomes. That's the recurring revenue premium in action.

If you're currently project heavy, shifting your revenue mix toward recurring maintenance is the single highest ROI move you can make before listing. Even moving from 30% recurring to 50% recurring can add hundreds of thousands to your sale price. I go deeper on this in the pre sale playbook section below.

Curious what a buyer would pay for your specific business? Get a free valuation consultation and we'll walk through your numbers, revenue mix, and buyer fit.

The PE Deal Landscape: Who's Buying and Why

Private equity is the dominant force in landscaping M&A right now. Deal volume surged from 22 transactions in 2023 to 65 in 2024 to over 100 in 2025, averaging nine deals per month. PE firms now account for 76% of all landscaping transaction volume. The market split is roughly 60/40 between financial and strategic buyers.

Here's the full picture of major PE activity in the space.

| PE Firm (AUM) | Target Company | Date | Details |

|---|---|---|---|

| Ares Management ($546B AUM) | Landscape Workshop | May 2025 | Majority stake, 38 locations across the Southeast |

| Wind Point Partners ($7B AUM) | ExperiGreen Lawn Care | Jan 2025 | Platform acquisition from Huron Capital, 19 add ons drove 10x EBITDA growth |

| Wind Point Partners | Turf Masters + ExperiGreen merger | Dec 2025 | Combined entity: 1,800 employees, 400K customers, 16 states, 2 Canadian provinces |

| Sterling Group Foundation Fund | Russell Landscape Group | 2024 to 2025 | 5 acquisitions since investment, 16 regional ops, first Texas entry |

| Comvest Private Equity | Bland Landscaping (now C.S.S.) | 2025 | 14 branches across the Southeast, expanding into Florida |

| Align Capital Partners | Strata Landscape Services | May 2025 | Western US platform, 350+ commercial clients in CA and UT |

| Century Park Capital | Green Summit Landscape Group | Nov 2025 | Newly formed national platform |

| Harvest Partners / Neuberger Berman | Yellowstone Landscape | Dec 2024 | Ranked #4 on Lawn & Landscape Top 100 |

| CI Capital | Mariani Premier Group | Ongoing | 24th acquisition completed Jan 2025 |

| KKR / One Rock Capital | BrightView Holdings | 2023 to 2025 | One Rock invested $500M convertible preferred; KKR sold $174M in shares |

Two things stand out from this table. First, new platforms are still being formed. Century Park Capital launched Green Summit as a brand new national platform in November 2025. That means there's continued demand for well run businesses to serve as foundation acquisitions. Second, the buy and build strategy dominates. ExperiGreen's story is the playbook: Huron Capital's 19 add on acquisitions drove a 10x increase in EBITDA before the platform was sold to Wind Point Partners.

The BrightView story is worth understanding too. The industry's largest player paused acquisitions for 11 consecutive quarters, choosing instead to buy back its own stock at 7.5x rather than paying 8 to 9x for acquisitions. That pricing discipline from the biggest strategic buyer means PE firms have been filling the gap aggressively.

Here's the structural opportunity: the top 50 landscaping companies control only 20% of market share. The remaining 80% is fragmented across hundreds of thousands of smaller operators. This fragmentation is exactly what PE roll up strategies target. If you're a well run business in a strategic geography, you're what these firms are looking for.

For a deeper look at how the retirement wave intersects with PE consolidation, read my post on why retiring landscaping owners should sell now.

The Pre Sale Playbook: 18 to 24 Months Out

The owners who get top dollar don't wake up one morning and decide to sell. They prepare methodically. Here's the timeline I recommend, broken into the key areas buyers evaluate.

Shift Your Revenue Mix

Target at least 50% recurring revenue before listing. 60% or more puts you in the premium multiple range. Here's how to get there.

Convert informal customer relationships into written, multi year contracts with auto renewal clauses. Start this process 12 to 24 months before listing. Auto renew terms mean your contract book grows passively. During due diligence, buyers want to see signed agreements, not handshake deals.

Diversify your service lines to keep revenue flowing year round. Add snow removal, holiday lighting, irrigation management, and overseeding programs. Seasonal layering reduces buyer risk and demonstrates a business that generates cash in every quarter.

Keep single client concentration below 15 to 20% of revenue. If one commercial account represents 30% of your billings, that's a red flag buyers will price into their offer. Spread the risk. Track customer retention rates by segment for at least 2 years before listing.

Build Route Density

This one is overlooked by most sellers but heavily evaluated by buyers. The ideal target is 8 to 12 residential accounts per day per crew, clustered in tight geographic zones. Dense routes create a 15 to 20% labor cost advantage compared to crews driving across town between jobs.

Buyers specifically request route maps during due diligence. They want to see that your crews are running efficient territory patterns, not crisscrossing the service area. If your routes are loose, spend the next 12 months tightening them. Drop unprofitable outlier accounts and replace them with clients closer to your core zones.

Adopt Technology Early

Technology adoption signals operational sophistication to buyers. It also generates the data that strengthens due diligence narratives. Right now, 93% of landscaping businesses use digital software in daily operations, but only 17% use AI. That gap is your opportunity.

AI route optimization delivers 20 to 35% reduction in drive time, up to 70% reduction in admin scheduling, and 15 to 25% more daily jobs per crew. ROI hits within 12 to 18 months. GPS fleet tracking alone can cut travel time by up to 25%.

Smart irrigation is an emerging value driver. Rock Hill Capital invested in Weathermatic in December 2025. Husqvarna acquired Orbit Irrigation for approximately $480 million in early 2026. Smart irrigation systems deliver 20 to 50% water savings and create a new recurring revenue stream through connected monitoring and management. This is a service line that barely existed three years ago and now has major capital behind it.

For a deeper look at robotic mowers, AI scheduling, and how they're reshaping landscaping valuations, read my post on robotic mowers and AI in landscaping.

Hire a Broker

I know this sounds self serving, but the data backs it up. Landscaping businesses sold with broker representation achieve 25% higher prices on average than those sold without. Brokers also save owners 30 or more hours per week during the sales process by managing buyer communications, due diligence requests, and deal negotiations.

A good broker runs a competitive process with multiple qualified buyers. The first offer is rarely the best. When you have three PE firms and two strategic acquirers at the table, the bidding dynamic changes entirely.

Thinking about selling but not sure where to start? Schedule a free consultation and I'll give you an honest assessment of your readiness and timeline.

Transition Management Away from Yourself

Owner dependency is one of the biggest value destroyers in landscaping sales. If you're still running crews, meeting with clients, and approving every purchase order, your business is worth less than it should be. Buyers pay a 25 to 30% valuation premium for businesses with professional management teams and documented SOPs.

Start transitioning now. Hire or promote a crew leader to an operations manager role. Document your processes for scheduling, billing, customer onboarding, and crew management. The goal is simple: the business should be able to run without you for at least two weeks without any problems. If it can't, you haven't built a business. You've built a job.

Clean Your Financials

PE buyers don't take your word for it. They conduct a Quality of Earnings (QoE) analysis that scrutinizes every line item in your books. Here's what they expect.

Three years of clean, well documented financial statements. GAAP aligned is best. At minimum, have professionally prepared statements that show consistent revenue, margins, and expense categories. Inconsistent or messy books kill deals faster than almost anything.

EBITDA margins between 12 and 20%. Gross profit margins between 35 and 50%. If your margins are below these ranges, work with your CPA to identify and document legitimate add backs. Personal vehicle expenses, one time equipment purchases, above market owner compensation. These all get added back to adjust your true earnings. But they need to be documented cleanly.

Document every add back. PE firms expect a detailed add back schedule with supporting documentation. "Trust me, I run personal expenses through the business" doesn't fly. You need receipts, explanations, and a CPA who understands business sale financials.

Work with an accountant who has experience in business sales, not just tax prep. The difference matters. A sale oriented CPA structures your financials to present the strongest defensible earnings picture. A tax oriented CPA structures them to minimize your tax bill. Those two goals often conflict.

Need help finding the right financial advisor? Reach out for a free consultation and we'll connect you with professionals who specialize in landscaping business sales.

Platform vs. Add On: Know What You Are

Understanding how PE firms categorize your business changes your entire negotiation strategy.

Platform companies are the foundation acquisitions. PE firms buy them first, then use them as a base for rolling up smaller operators. Platforms typically have $3 million or more in EBITDA, multi state or large regional operations, professional management teams, technology infrastructure, and strong brand recognition. Platforms command the highest multiples and the most favorable deal structures.

Add on acquisitions are smaller businesses purchased to bolt onto an existing platform. Add ons trade at lower multiples but still benefit from the PE premium. If you're a $500,000 to $2 million EBITDA business, you're likely an add on candidate. That's not a bad thing. It means there are funded platforms actively looking to acquire businesses like yours in specific geographies.

The key question is: which platforms are expanding in your region? Look at the deal table above. If you're in the Southeast, Landscape Workshop (Ares Management), C.S.S. (Comvest), and Russell Landscape Group (Sterling Group) are all active. In the West, Strata Landscape Services (Align Capital) is building. If you're in lawn care specifically, the ExperiGreen and Turf Masters combined entity under Wind Point covers 16 states and is likely still acquiring.

A broker with PE relationships can position your business to multiple platform buyers simultaneously. That competition is how you get the best price.

Revenue Optimization Tactics That Move the Needle

Beyond the strategic shifts in the pre sale playbook, here are specific tactical moves that increase your valuation.

Formalize Everything

If you have 200 residential customers and 150 of them are on informal arrangements with no written contracts, you don't have recurring revenue. You have customers who could leave tomorrow. Formalize every relationship. Minimum 12 month terms. Auto renewal clauses. Written scope of work. This takes effort, but it directly increases the multiple buyers will pay.

Layer Seasonal Services

A landscaping business that generates revenue only from April to October is worth less than one that bills 12 months a year. Layer in snow removal for winter, holiday lighting for November and December, irrigation maintenance for spring, and overseeding and aeration for fall. Each service line you add reduces buyer risk perception and adds revenue without proportionally adding overhead.

Invest in Smart Irrigation

This is the emerging play that most landscaping owners haven't made yet. Smart irrigation creates a monthly monitoring and management fee that stacks on top of the initial installation. It's pure recurring revenue with high margins. The capital flowing into this space (Rock Hill Capital into Weathermatic, Husqvarna's $480 million Orbit acquisition) tells you exactly where the market is heading.

Track and Prove Retention

Buyers want to see customer retention data segmented by service type and client tenure. If you can show that your maintenance clients stick around for an average of 4 to 5 years with less than 10% annual churn, that's a powerful number. Start tracking this now even if you haven't been. Two years of retention data by segment is the minimum buyers want to see.

Want to understand how these tactics would impact your specific valuation? Check out our landscaping valuation page for industry benchmarks, or use the calculator for a quick estimate.

Common Mistakes That Cost Sellers Real Money

I've seen these patterns repeatedly in landscaping business sales. Every one of them leaves money on the table.

Not knowing what recurring revenue really means. Having long term customers is not the same as having recurring revenue contracts. Buyers define recurring revenue as contracted, auto renewing agreements with defined scope. A customer who's used you for 10 years but could cancel with a phone call is not recurring revenue. Formalize the relationship.

Overvaluing equipment. Your fleet of trucks, mowers, and trailers matters less than you think. Buyers care about earnings, recurring revenue, and management depth. Equipment is a depreciating asset they can replace. A common mistake is pricing the business based on replacement cost of equipment plus some premium. That's not how buyers calculate value.

Hiding owner perks in the financials. Running personal expenses through the business is common, but undocumented perks create a credibility problem during due diligence. If the buyer's QoE team finds expenses you didn't disclose as add backs, they start questioning everything else. Transparency is better than surprises.

Skipping the broker to save on commission. Yes, brokers charge 8 to 12% on most landscaping deals. But the 25% higher sale price they typically achieve more than covers the fee. You also get your time back. Selling a business while running it is a full time job on top of a full time job. Without a broker, the business often suffers during the sale process, which then hurts the valuation. It's a negative spiral.

Listing at the wrong time. Listing in Q4 means your trailing twelve months start with the slow winter season and your peak season numbers are 6 to 9 months old. Listing in Q2 or early Q3 puts your best financial quarter front and center. Timing is not everything, but it's something, and it's free.

Ignoring route density. A buyer looking at two businesses with identical revenue will pay more for the one with tighter routes. Dense routes mean lower fuel costs, more jobs per crew per day, and easier scaling. Loose routes mean waste. If your route maps look like a plate of spaghetti, fix them before listing.

Waiting for one more good year. This is the most expensive mistake of all. The owners who keep saying "I'll sell after next season" often end up selling 3 to 5 years later at a lower multiple in a worse market. The current cycle won't last forever. PE capital allocations shift. Interest rates fluctuate. The best time to sell is when buyers are aggressive and your numbers are strong. That window is open right now.

What to Do Next

The landscaping M&A market in 2026 is the strongest it's ever been for prepared sellers. PE deal volume is at record levels. New platforms are still being formed. Multiples for businesses with recurring revenue, technology, and management depth are at or near historical highs.

But "the market is strong" and "your business will sell for a premium" are two different statements. The gap between them is preparation.

Here's your action plan.

-

Get a current valuation. Stop guessing what your business is worth. Use our free landscaping business valuation calculator for a quick estimate, or contact us for a detailed analysis that factors in your revenue mix, route density, contracts, and team.

-

Audit your recurring revenue. What percentage is under formal contract with auto renewal terms? If it's below 50%, that's your first priority. Start converting informal relationships to written agreements immediately.

-

Assess your owner dependency. Can the business operate without you for two weeks? If not, you need to invest in management depth before you list. Buyers discount owner dependent businesses by 25 to 30%.

-

Clean up your financials. Engage a CPA experienced in business sales. Get three years of clean statements, document all add backs, and prepare for a Quality of Earnings analysis.

-

Invest in technology. AI route optimization, GPS tracking, and smart irrigation are the three highest ROI technology investments for pre sale landscaping businesses. Most pay for themselves in 12 to 18 months and signal operational maturity to buyers.

-

Talk to a broker. Even if you're 18 to 24 months out, understanding the market, identifying which PE platforms are active in your geography, and starting the preparation process now puts you in a dramatically better position than waiting until you're ready to list.

The landscaping businesses that sell for 4x to 5x SDE in 2026 are the ones whose owners started this process a year or two ago. You can't change when you start, but you can start today. The window is open. The buyers are active. The multiples are favorable. What happens next is up to you.

Ready to talk about your exit? Schedule a free, confidential consultation and I'll walk you through where your business stands, what buyers in your market are paying, and what it would take to maximize your sale price.

Need capital to invest in technology, equipment, or growth before selling? Our unsecured funding programs provide up to $500,000 with no collateral required, perfect for pre sale improvements that pay for themselves at closing.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.