Six months. That's the timeline most sellers hope for when they decide it's time to sell their business. And I'll tell you upfront: it's achievable, but most sellers aren't ready for what it actually requires.

The average small business takes 9 to 12 months to sell from the moment it hits the market. Some take 18 months or longer. The ones that close in 6 months share a specific set of characteristics, and they don't get there by luck. They get there by doing the work before they list, not after.

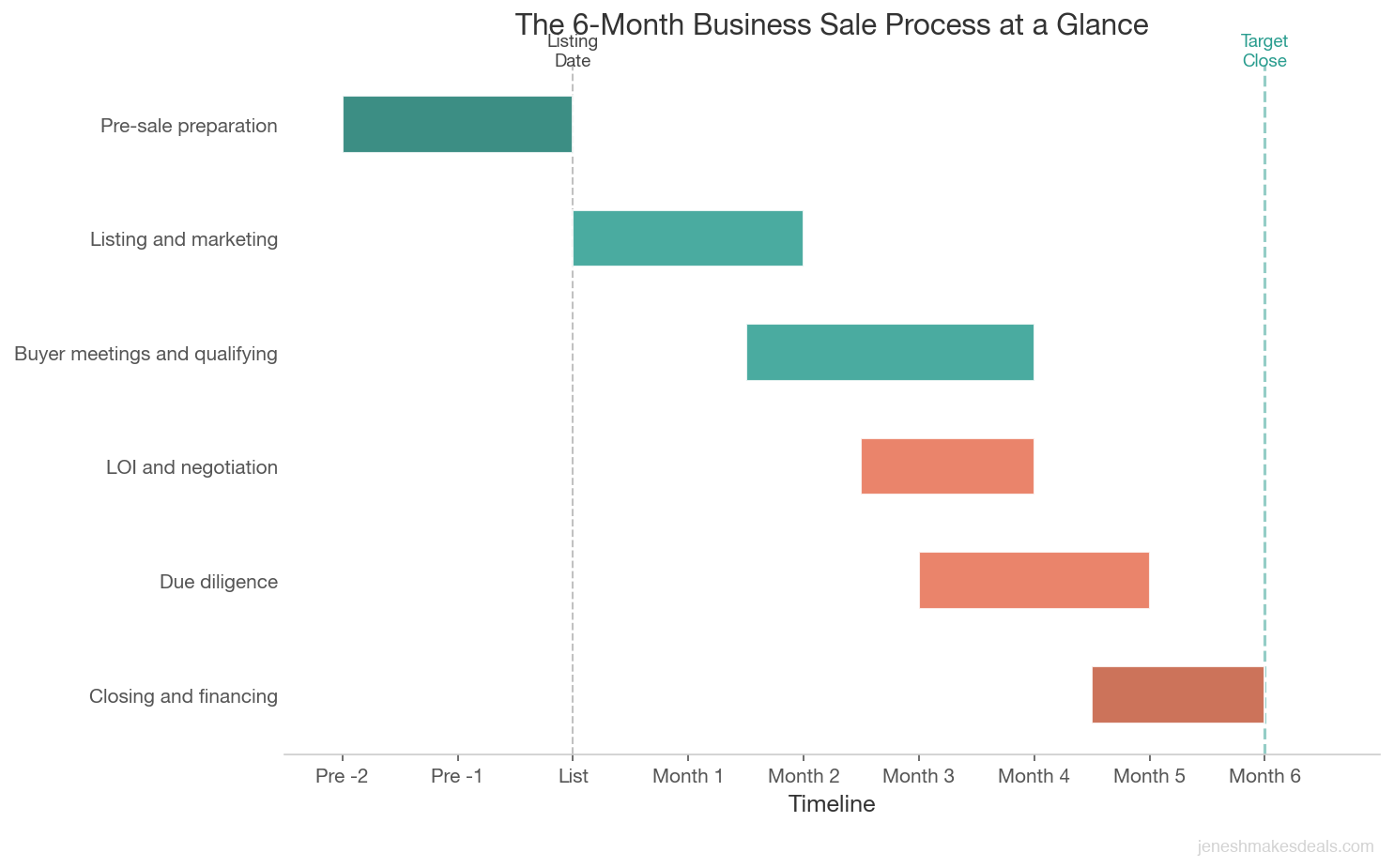

Here's the real story of what a 6 month sale looks like.

Is 6 Months Realistic? The Honest Answer

Yes, six months is realistic for the right business with the right preparation. No, it's not the average experience, and it's not automatic.

Businesses that sell in 6 months or less typically have several things in common: clean financials, reasonable pricing, low owner dependence, no pending legal issues, and a clear lease or real estate situation. They also tend to be in markets with active buyer demand.

Businesses that take 12 to 18 months are usually fighting one or more of these same issues: overpricing, financial disorganization, complicated ownership structure, lease problems, or declining revenue. These aren't always fatal issues, but they slow deals down significantly.

The honest answer to "can I sell in 6 months?" depends on where your business is today. A well run, profitably priced service business with three years of clean financials can likely close in 6 months. A business with inconsistent records, an asking price above what the market will bear, and an owner who is the entire customer relationship team will probably take much longer.

Before you set a timeline, get a real valuation conversation so you're working from an accurate starting point, not an optimistic one. It's also worth reflecting on how to know when to sell your business, because timing your exit well is just as important as executing the sale quickly. You can also use our business sale timeline estimator to see whether 6 months is realistic for your specific business.

The businesses that sell in 6 months or less aren't lucky. They're prepared. Clean financials, realistic pricing, and low owner dependence are the three factors that separate a 6 month sale from an 18 month one.

The Pre Sale Preparation That Must Happen Before You List

This is where most sellers lose the 6 month race before it starts. They decide to sell, immediately list, and then spend months scrambling to produce documents that should have been ready on day one.

Pre sale preparation is not optional if you want a fast sale. Here's what needs to be done before the business goes to market:

Financial cleanup. Three years of clean profit and loss statements, balance sheets, and tax returns, all reconciled and consistent with each other. Adjusted financials (adding back personal expenses and one time costs) prepared and clearly documented. For a full guide to doing this right, see how to prepare your business financials for sale. If your bookkeeping is a mess, hire a CPA to organize it before listing. This alone can take 4 to 8 weeks and is not something you do while buyers are already asking questions.

Asset list. A detailed inventory of all assets included in the sale: equipment, vehicles, furniture, fixtures, software licenses, intellectual property, and inventory. Buyers need this and you need to produce it quickly once they ask.

Lease review. If you have a commercial lease, confirm that it can be assigned to a buyer, know how much time is left on it, and understand your landlord's assignment requirements. Lease problems discovered mid deal kill timelines. Discover them early.

Legal review. Any pending litigation, pending regulatory matters, or unresolved contract disputes need to be surfaced and either resolved or prepared for disclosure. Surprises during due diligence extend timelines by weeks or months.

Confidential Information Memorandum. Your CIM is the detailed business overview document that serious buyers review before making an offer. A broker typically helps create this, but it requires your input on operations, customer relationships, staff, and competitive position. Having a solid CIM ready at launch shortens your time to first offer.

Proper pricing. Pricing is one of the most common timeline killers. If you list at 1.5x above market value, you'll spend months attracting no one or attracting buyers who make low offers and walk when you don't negotiate. Price right from the start based on actual comparable sales, not what you'd like the business to be worth.

Pre Sale Preparation Checklist and Timeframes

| Task | Typical Timeframe | Why It Matters |

|---|---|---|

| Financial cleanup (3 years of P&L, balance sheets, tax returns) | 4 to 8 weeks | Buyers walk when numbers don't reconcile |

| Asset inventory (equipment, IP, licenses) | 1 to 2 weeks | Delays buyer questions if not ready on day one |

| Lease review and landlord coordination | 2 to 4 weeks | Lease assignment issues kill deals mid process |

| Legal review (litigation, contracts, compliance) | 2 to 4 weeks | Surprises in due diligence add months |

| Confidential Information Memorandum (CIM) | 2 to 3 weeks | Shortens time to first qualified offer |

| Market based pricing and valuation | 1 to 2 weeks | Overpricing is the number one timeline killer |

Month 1 to 2: Listing, Marketing, and First Buyer Inquiries

Once your preparation is complete and your business is listed, the first two months are about generating buyer interest and making initial contact with prospective buyers.

A well marketed listing generates most of its qualified inquiries in the first 30 to 60 days. If you're working with a broker, they'll push the listing to their buyer network, relevant online marketplaces, and targeted outreach to strategic acquirers. If you're selling yourself, you're managing this marketing effort directly.

What typically happens in this phase:

- The listing goes live on BizBuySell, industry specific platforms, and your broker's buyer network

- Initial inquiries come in, ranging from genuinely interested buyers to tire kickers

- NDAs go out to interested parties

- The broker or you conduct initial screening calls

- Qualified buyers receive the CIM

In a well functioning 6 month sale, you're aiming to have 3 to 5 genuinely qualified buyers engaged by the end of month two. "Qualified" means they've signed the NDA, reviewed basic information, demonstrated financial capacity, and had an initial conversation that confirms they're serious.

Don't panic if the first few inquiries go nowhere. Screening out unqualified buyers quickly is the goal at this stage, not converting every inquiry.

Month 2 to 4: Buyer Meetings, NDAs, and Qualifying Serious Buyers

This is the deepest and most intensive phase of the process. You're moving from a general pool of interested parties down to one or two serious buyers who might actually make an offer.

During this phase, you're:

Conducting management meetings. These are in person or video calls where you meet qualified buyers, answer detailed questions about operations, and assess whether they're the right person to take over the business. Plan for two to four of these meetings with different buyers.

Providing detailed financials. Qualified buyers who have cleared initial screening get access to detailed financial statements, customer information (under strict confidentiality), and any other materials needed to develop an offer.

Answering due diligence questions. Even before an offer is made, serious buyers ask operational questions. How does your customer acquisition work? What are the key employee roles? What does your peak season look like? Be responsive. Buyers who wait days or weeks for answers lose confidence and often move on to other opportunities.

Building rapport. This sounds soft, but it matters. Sellers who help buyers understand and get excited about the business get better offers. Sellers who are guarded or transactional in every interaction often watch interested buyers cool off.

The goal exiting month four is a signed Letter of Intent. In a 6 month sale, getting to LOI by month four or early month five is the target. If you're approaching month five without an LOI, the 6 month timeline is in jeopardy.

Month 3 to 5: LOI, Negotiation, and Due Diligence

The Letter of Intent is not the finish line. It's the starting gun for the most intensive part of the sale. If you relax after signing an LOI, you will lose weeks you can't get back.

Once you have a signed LOI, you typically have a 30 to 60 day exclusivity period during which the buyer conducts formal due diligence. During this time, you owe that buyer your full cooperation, and the clock on your timeline is running hard.

LOI negotiation. Before signing, negotiate the key terms: purchase price, payment structure, seller financing if any, earnout if any, transition period, and exclusivity window. Don't rush past this. An LOI signed under poor terms is hard to undo.

Due diligence period. The buyer's attorney and accountant will request documents covering financials, contracts, leases, employee agreements, IP, and regulatory compliance. Responding to these requests quickly and thoroughly is one of the most important things you can do to maintain timeline. Sellers who take two weeks to produce documents that should take two days add a month to their closing date.

Issues and resolution. Due diligence almost always surfaces something. A mismatched tax return line, a lease with an unusual clause, a contract that needs an assignment approval. Most of these issues are manageable. What determines whether they kill the deal or get resolved is how both parties approach them. Come to the table with problem solving intent, not defensiveness.

For a detailed checklist of what buyers look for during due diligence, see our due diligence checklist for business buyers.

Month 5 to 6: Closing, Financing, and Final Paperwork

The closing phase is where the deal either crosses the line or falls apart waiting for one more document.

What happens in this phase:

Financing finalization. If the buyer is using SBA financing, this is typically the longest variable. SBA loan processing can take 45 to 90 days from application. For a 6 month timeline to work with SBA financing, the buyer needs to have submitted their loan application no later than month three. If your buyer is using conventional financing or cash, this phase is faster.

Purchase agreement. Your attorneys negotiate and finalize the purchase agreement, which is more detailed and binding than the LOI. Budget 2 to 4 weeks for this process once the due diligence period closes.

Third party approvals. Landlord consent to lease assignment, franchisor approval if applicable, and any regulatory transfer requirements. These need to be initiated early because third parties don't move on your timeline.

Pre closing checklist. Inventory counts, employee notifications (often timed for a few days before closing), utility transfer arrangements, and any other operational handoffs.

Closing day. Documents signed, funds transferred, keys handed over. If everything went right, this happens on or around the six month mark from when you listed.

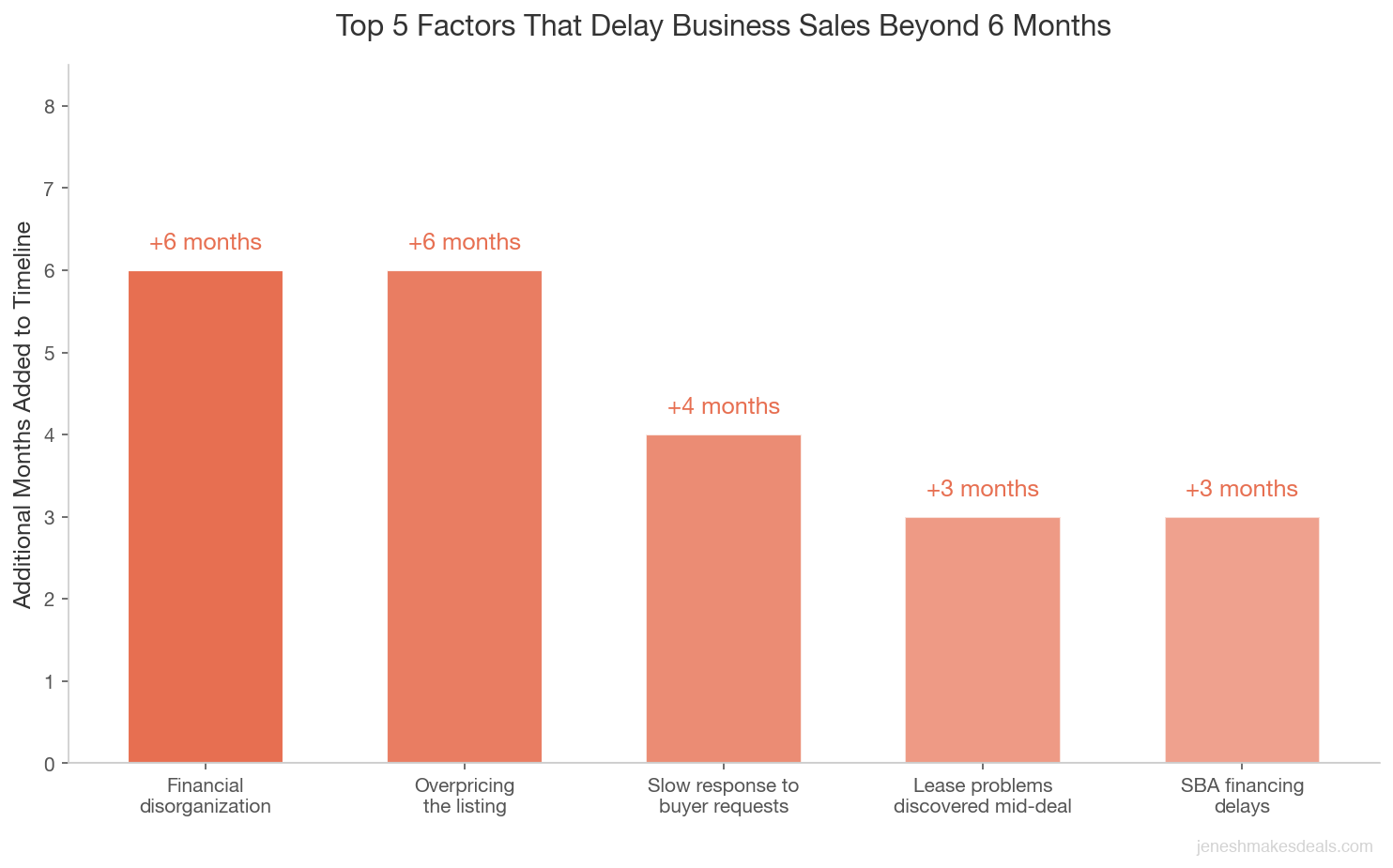

The 5 Things That Delay Sales Beyond 6 Months (and How to Avoid Each)

1. Financial disorganization. Buyers ask for three years of statements and you spend six weeks pulling together records that don't reconcile. Fix: complete financial cleanup before listing, not after.

2. Overpricing. You list at $1.5 million, get no offers for three months, drop to $1.2 million, get an offer, and lose another three months. Fix: price accurately from the start based on actual market comps, not hope.

3. Slow response to buyer requests. Every week you take to respond to a due diligence request is a week off the end of your timeline. Fix: designate dedicated time each week to the sale process and treat buyer requests as the priority they are.

4. Lease problems discovered mid deal. Your lease has four months left and the landlord won't cooperate on assignment. Fix: review your lease before listing and resolve issues proactively.

5. Financing delays. The buyer's SBA loan application was submitted too late. Fix: when you qualify buyers, confirm they've already been pre qualified by a lender. If they haven't, encourage them to do it immediately.

Want to talk through the specific bottlenecks in your situation? Contact us for a consultation.

Should You Hire a Broker to Sell Faster? (Yes, Here's Why)

For most businesses, the answer is yes, a broker significantly speeds up the process.

Here's the specific impact on timeline:

Faster buyer sourcing. A broker's existing buyer network can generate qualified inquiries in weeks rather than months. Building an audience from scratch when you list without a broker takes longer.

Pre qualified buyer pool. Good brokers don't forward every inquiry to sellers. They screen for financial qualification, intent, and fit before you ever take a meeting. This means you spend less time on conversations that go nowhere.

Faster document preparation. Experienced brokers know exactly what buyers will ask for and can help you prepare it in advance. No scrambling once buyers start requesting documents.

Deal momentum management. Brokers stay on buyers during slow periods, push responses, and keep deals moving. Without a broker, deals stall when no one is actively managing the momentum.

Issue navigation. When problems surface in due diligence (and they always do), experienced brokers have seen the same issues many times and know how to address them efficiently. First time sellers reinvent the wheel.

Selling With a Broker vs. Without: Timeline and Effort Comparison

| Factor | With a Broker | Without a Broker |

|---|---|---|

| Time to first qualified buyer | 2 to 4 weeks | 6 to 12 weeks |

| Buyer screening | Broker filters before you meet anyone | You handle every inquiry personally |

| Document preparation | Broker guides you on exactly what to prepare | Trial and error as buyers ask for things |

| Deal momentum | Broker follows up and pushes the process forward | Deals stall when you're busy running the business |

| Due diligence issues | Broker has seen similar issues and knows how to resolve them | You figure it out as problems arise |

| Cost | 8% to 12% commission on businesses under $1 million | No commission, but your time has a cost |

| Typical total timeline | 6 to 9 months | 9 to 18 months |

The tradeoff is commission, typically 8% to 12% for businesses under $1 million. Whether the math works depends on your specific situation. But the time savings alone are often worth it, especially if your time is valuable and you're still running the business during the sale. If you're still weighing the decision, our post on whether you should use a broker to sell your business walks through the tradeoffs in detail.

What You Sacrifice When You Rush a Sale

Six months is a fast sale. Chasing it in four months is a different story.

Buyers know when a seller is in a hurry. Urgency is a negotiating concession. A 6 month sale where buyers compete is always better than a 4 month sale where you accepted the first acceptable offer.

When you artificially accelerate a timeline, the usual casualties are price and terms. Buyers know when a seller is in a hurry. Urgency is a negotiating concession. If you accept the first offer quickly, skip full market exposure, or rush due diligence, you are almost certainly leaving money on the table.

A 6 month sale where you've given buyers enough time to compete is better than a 4 month sale where you accepted the first acceptable offer. Speed is a priority, but not at the cost of running a process that generates competitive interest.

The other sacrifice is due diligence quality. Sellers who push to close quickly sometimes encourage buyers to skip certain verifications. This can come back to hurt both parties after closing, through disputes about representations and warranties or claims about what was disclosed.

Six months is fast enough. Four months at the cost of price and proper process is rarely the right tradeoff.

The Businesses That Actually Sell in 6 Months (What They Have in Common)

I've closed deals in under 6 months and I've watched others drag on for 18 months with the same buyer quality. The pattern in the fast closing businesses is consistent.

Clean, consistent financials. Three years of statements that match tax returns, with add backs clearly documented. No surprises in the numbers.

Realistic pricing. The business is listed within 10% to 15% of where comparable businesses have recently sold. Not at "what I need to retire," but at "what the market will actually pay."

Low owner dependence. The business has systems, trained staff, and customer relationships that extend beyond the owner personally. Buyers can see a path to running it without the seller within a reasonable transition period.

Active seller participation in the process. The seller is responsive, organized, and engaged throughout. They return calls, answer questions quickly, and make decisions without excessive delay.

No critical open issues. No pending litigation, no lease about to expire, no regulatory violations in progress. Clean enough that due diligence is verification, not excavation.

Right buyer, right fit. They found a buyer who has the capital, the experience, and the genuine interest in this specific business.

Fast Close vs. Slow Close: What Makes the Difference

| Factor | Sells in 6 Months | Takes 12 to 18+ Months |

|---|---|---|

| Financials | 3 years of clean, reconciled statements matching tax returns | Incomplete records, inconsistencies between P&L and tax filings |

| Pricing | Listed within 10% to 15% of recent comparable sales | Priced based on owner's retirement needs, not market data |

| Owner dependence | Systems and trained staff in place, business runs without owner daily | Owner is the primary customer relationship and revenue driver |

| Seller responsiveness | Returns calls and documents within 24 to 48 hours | Takes 1 to 2 weeks to respond to buyer requests |

| Legal and lease status | No pending litigation, lease is assignable | Lease about to expire, unresolved legal matters surface mid deal |

| Buyer qualification | Buyers pre qualified by a lender before LOI | Buyer financing falls through after months of due diligence |

None of these are accidents. They're the result of preparation and realistic decision making. The 6 month sellers aren't lucky. They're ready.

Common Mistakes That Slow Down Sales

Every week of delay costs you twice: once in lost momentum with your buyer, and again in the mental toll of a sale that drags on longer than it should. The sellers who close on time are the ones who treat the sale process like a second job from day one.

Starting the process before you're actually ready. Sellers who list without having financials organized, legal issues resolved, or a realistic price end up starting over after months of failed conversations.

Negotiating every point to the limit. There's a difference between getting a fair deal and fighting so hard on every term that you exhaust your buyer. Some negotiation is appropriate. Grinding the buyer on every minor provision loses goodwill and time.

Disappearing during due diligence. Some sellers check out emotionally once the LOI is signed. They respond slowly, lose focus, and make the buyer feel like they're chasing. This creates doubt and extends timelines.

Letting the process distract from operations. If your business underperforms during the sale period because you're distracted, buyers notice. Declining performance during due diligence is a major red flag and a reason for buyers to retrade.

Your Next Steps

If a 6 month sale is your goal, here's the prep list you need to start today:

- Get your financials in order. Hire a CPA if you haven't maintained clean books.

- Get a realistic business valuation from someone who works in business sales, not a ballpark from a multiple calculator.

- Review your lease and any pending legal matters.

- Reduce any obvious owner dependence issues over the next 3 to 6 months.

- Talk to a broker about the process and timeline for your specific situation.

The sooner you start the prep, the sooner you can list, and the faster the whole process moves.

Ready to get started? Contact us for a free consultation to talk through your specific situation and timeline.

Ready to start the process? Explore selling your business.

Want to get a ballpark on value first? Use our business valuation calculator.

Frequently Asked Questions

Is 6 months realistic for a first time seller?

Yes, if the business is well prepared and properly priced. First time sellers often underestimate how long due diligence and closing paperwork take, so working with an experienced broker is especially valuable for keeping the process moving efficiently.

Does business size affect how long a sale takes?

Generally yes. Businesses under $500,000 in sale price often move faster because they attract more buyers and financing is simpler. Businesses over $2 million involve more complex due diligence, more sophisticated financing, and often more buyers who need time to make decisions.

What if my buyer's financing falls through near closing?

This is one of the most frustrating delays in business sales. If you're three months into a process and your buyer's bank declines their loan, you're essentially starting over with the next buyer. Ways to reduce this risk: require proof of pre qualification before you accept an LOI, and consider buyers who have alternative financing sources or more cash available.

Can I sell without a broker in 6 months?

Possible but harder. You'll need to manage marketing, buyer screening, due diligence coordination, and deal momentum yourself while still running your business. Some sellers pull it off. Most end up taking longer without a broker than with one.

What happens if I get a great offer in month 2?

Take it seriously. A great early offer is often a sign that you priced correctly and the business is genuinely attractive to buyers. The risk of waiting for "a better offer" is that you lose the motivated buyer you have and spend more time searching for the hypothetical one.

Related Articles

April 16, 2026

Preparing Your Business for Sale: The 12 Month Checklist

The best time to start preparing your business for sale is 12 months out. Here's exactly what to do each quarter.

April 12, 2026

How to Handle Multiple Offers on Your Business

Multiple offers are a great problem to have. But picking the wrong one can cost you months and thousands. Here's how to evaluate them.

April 9, 2026

Best Time of Year to List Your Business for Sale

Timing your listing right can mean more buyers, better offers, and a faster close. Here's what the data says about when to go to market.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.