Getting multiple offers on your business sounds like a dream. And it is, if you handle it right. But I've seen sellers pick the highest price offer only to have it fall apart three months later. The buyer couldn't get financing, the contingencies piled up, and the seller ended up starting over with nothing to show for it but lost time and a business that now looks stale on the market.

The best offer isn't always the highest number. I've closed deals where the seller accepted $50,000 less than the top offer and walked away happier, faster, and with more cash in hand at closing. A sure close at a fair price beats a risky close at a great price every single time.

If you're sitting on multiple offers, here's exactly how to evaluate them, compare them, and pick the one that actually gets you to the closing table.

Why Multiple Offers Happen in the First Place

Multiple offers don't happen by accident. They happen because you did several things right, or because market conditions are working in your favor.

The most common reasons I see multiple offers come in:

You priced it correctly. A $900,000 business listed at $850,000 will attract more serious buyers than the same business listed at $1.1 million. The lower list price creates urgency and competition. The inflated price creates silence.

Your business is strong. Consistent revenue growth, clean financials, a diversified customer base, and a business that doesn't require the owner to work 70 hours a week. Those are the businesses that attract five to eight inquiries in the first two weeks.

Your marketing was done well. A strong Confidential Information Memorandum (CIM), professional photos, and targeted outreach to qualified buyers matter. A two page listing with blurry photos will get fewer looks than a 20 page CIM that tells a clear story.

Your industry is hot. Right now, home services businesses (HVAC, plumbing, landscaping), healthcare adjacent businesses, and anything with recurring revenue are drawing significant buyer attention. If you're in a hot sector, expect competing offers.

Timing. Listing in Q1 or early Q2 generates more interest because buyers who secured financing at the start of the year are actively looking. List in late November and most buyers are waiting until January.

What to Look at Beyond the Price

When you get two or three offers, the temptation is to line them up by price and pick the highest one. Don't do that. Price is one of at least six factors that determine which offer is actually the best for you.

Here's what I evaluate with every offer that comes across my desk:

Down payment percentage. A buyer offering $800,000 with 30% down ($240,000) is in a fundamentally different position than a buyer offering $800,000 with 10% down ($80,000). The larger down payment means more skin in the game, higher likelihood of loan approval, and less risk that the deal collapses during underwriting. I want to see at least 15% to 20% down on SBA deals and 25% or more on conventional deals.

Financing type. How the buyer plans to pay matters enormously. The main options are:

- All cash. Fastest close, fewest contingencies. But cash buyers typically offer 10% to 15% less than financed buyers.

- SBA loan. Most common for businesses between $250,000 and $5 million. SBA deals take 60 to 90 days to close and come with lender requirements. But SBA buyers often pay full price or close to it.

- Seller financing. The buyer asks you to carry part of the note. This can be fine in small amounts (10% to 20% of the deal), but if a buyer wants you to finance 50% of the purchase price, that's a sign they can't get bank financing and you're taking on significant risk.

- Combination. Many deals are structured as SBA loan plus a small seller note. This is normal and often the best structure for both sides.

Contingencies. Every contingency in an offer is a potential exit ramp for the buyer. Common contingencies include financing approval, satisfactory due diligence, landlord lease approval, and franchisor approval (for franchise businesses). Fewer contingencies means a higher probability of closing. An offer with six contingencies and a 120 day timeline is much riskier than an offer with two contingencies and a 60 day timeline.

Timeline to close. How quickly can this buyer get to the closing table? A cash buyer might close in 30 days. An SBA buyer needs 60 to 90 days. A buyer who says "I need six months" is either not ready or has other complications you should investigate.

Buyer qualifications. Has this person run a business before? Do they have industry experience? Have they been pre-approved for financing? A buyer with a pre-approval letter from a reputable SBA lender is dramatically more likely to close than a buyer who says "I'm planning to apply for a loan."

Earnout or seller note terms. If part of the purchase price is deferred through an earnout or seller note, you need to evaluate the terms carefully. A $900,000 offer with $200,000 as a two year earnout tied to revenue targets is really a $700,000 guaranteed offer with $200,000 in maybe money.

When I sit down with a seller to review offers, I always ask the same question: "If this buyer's financing falls through on day 60, how would you feel about starting over?" That gut check tells you more about which offer to accept than any spreadsheet. The offer that lets you sleep at night is usually the right one.

How to Compare Offers Side by Side

I use a scoring matrix with my clients. It's simple, and it works. Here's the framework.

Rate each offer on a 1 to 5 scale across six categories:

| Factor | Weight | Offer A | Offer B | Offer C |

|---|---|---|---|---|

| Purchase price | 25% | ? | ? | ? |

| Terms and structure | 20% | ? | ? | ? |

| Buyer financial strength | 20% | ? | ? | ? |

| Closing probability | 15% | ? | ? | ? |

| Timeline | 10% | ? | ? | ? |

| Contingencies | 10% | ? | ? | ? |

Multiply each score by the weight and add them up. The offer with the highest weighted score is usually the right choice.

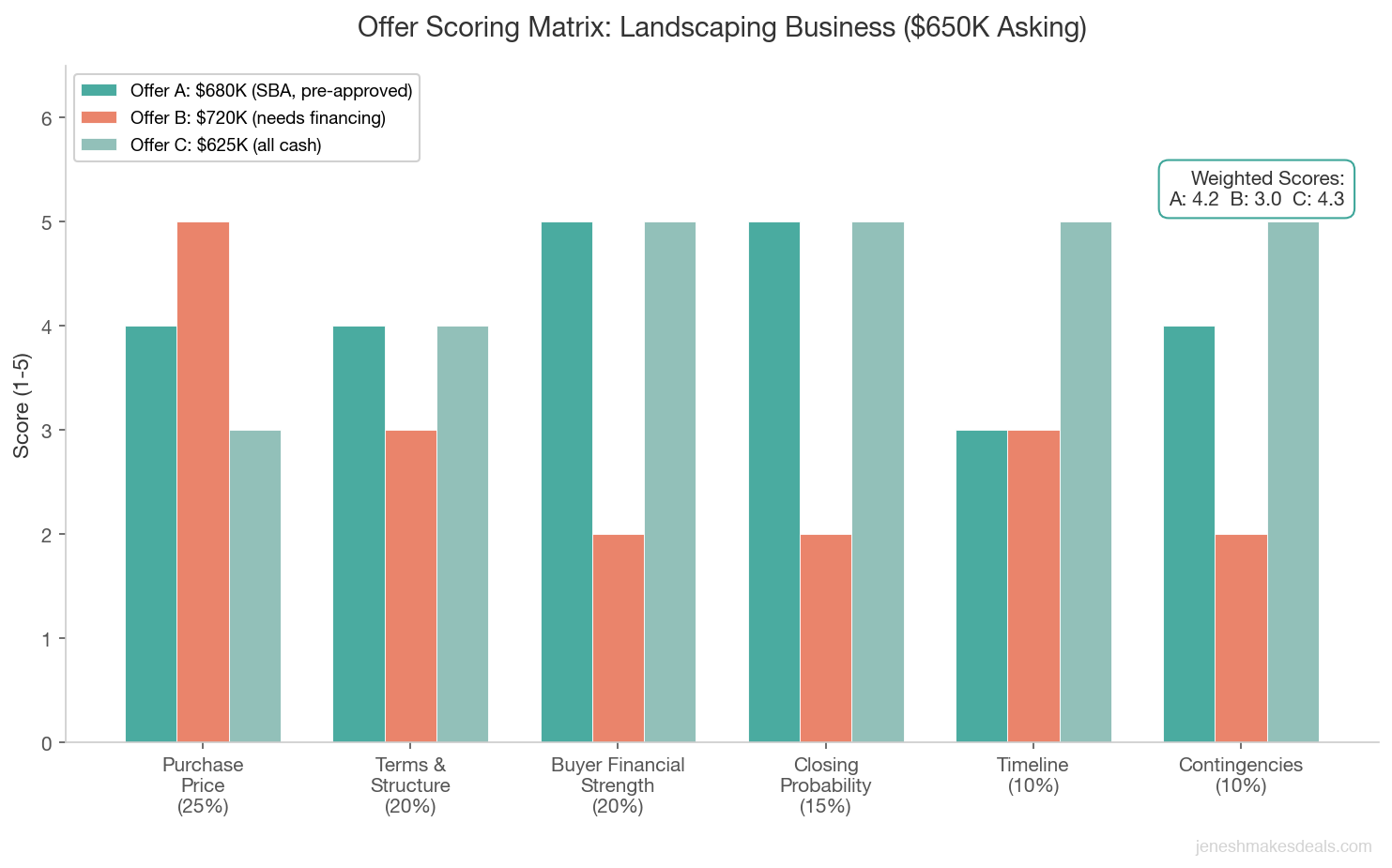

Let me walk through a real example. Say you're selling a landscaping business for $650,000 and you receive three offers:

Offer A: $680,000, SBA financed, 20% down ($136,000), pre-approved buyer with industry experience, 75 day close, standard contingencies.

Offer B: $720,000, 10% down ($72,000), buyer needs to secure financing, no industry experience, 90 day close, wants extended due diligence period.

Offer C: $625,000, all cash, experienced buyer, 30 day close, minimal contingencies.

Most sellers look at this and want Offer B because $720,000 is the biggest number. But when you score it:

- Offer A scores highest on buyer strength, closing probability, and terms

- Offer B scores highest on price but lowest on buyer strength and closing probability

- Offer C scores highest on timeline and contingencies but lowest on price

In my experience, Offer A is the best choice about 70% of the time. It balances a strong price with a qualified buyer who can actually close. Offer B has a 40% to 50% chance of falling apart during underwriting. Offer C is the safe choice if you need speed, but you're leaving $55,000 on the table.

Not sure how to value the offers you're receiving? Use our free business valuation calculator to see where the numbers land.

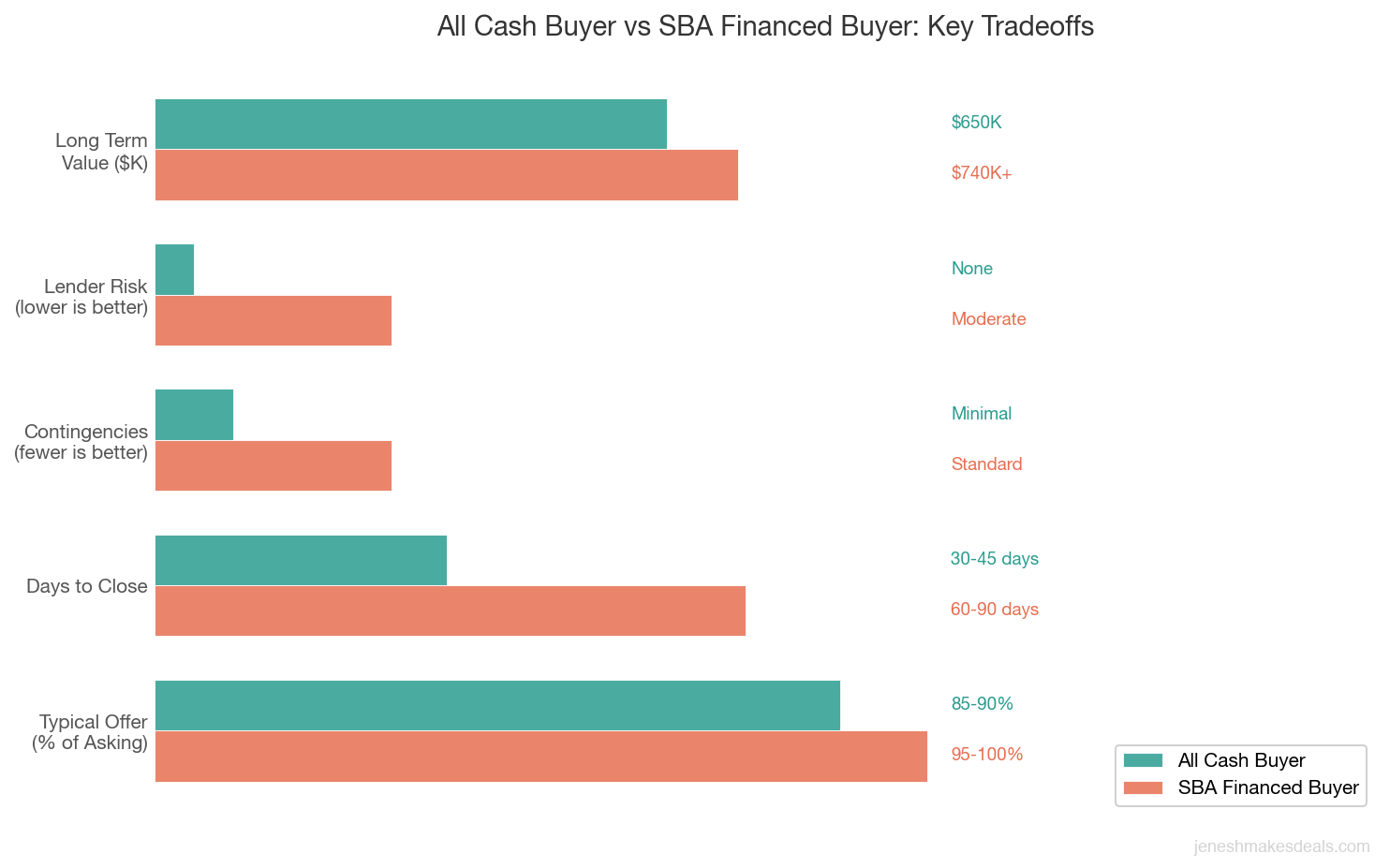

The All Cash Buyer vs. the SBA Buyer

This comes up in almost every multiple offer situation, so let's break it down specifically.

The all cash buyer:

- Closes in 30 to 45 days

- No financing contingency (the biggest deal killer removed)

- No lender appraisal requirement

- No SBA paperwork, no bank underwriting delays

- Typically offers 10% to 15% below asking price

- May want a bigger discount specifically because they're paying cash

The SBA buyer:

- Closes in 60 to 90 days

- Must get loan approval (lender will scrutinize the business's financials, tax returns, and lease)

- Lender may require an independent business appraisal

- Typically pays full price or within 5% of asking

- Deal can fall apart if the lender doesn't approve the loan

Here's the math that matters. On a $750,000 business:

- Cash buyer offers $650,000 (13% below asking). You net $650,000 at closing, minus broker fees and closing costs.

- SBA buyer offers $740,000 with you carrying a $75,000 seller note at 6% over five years. You get $665,000 at closing, but you'll collect another $86,400 over five years if the buyer makes all payments.

The total value of the SBA deal is higher, but it takes five years to fully realize, and you're carrying risk on that seller note. The cash deal puts $650,000 in your pocket in 30 days with no ongoing risk. There's no universal right answer. It depends on your priorities, your timeline, and how much risk you're willing to accept after the sale.

Red Flags in Offers

Not every offer deserves your attention. Some offers are warning signs that a buyer isn't serious, isn't qualified, or is going to waste your time. Here's what to watch for.

Low earnest money. Earnest money (also called a good faith deposit) should be 3% to 5% of the purchase price. On a $500,000 deal, that's $15,000 to $25,000. If a buyer offers $2,000 in earnest money on a $500,000 business, they're not committed. The earnest money is their skin in the game. If it's too low, they can walk away with almost nothing at stake.

Too many contingencies. Standard contingencies include financing, due diligence, and lease assignment. That's normal. But when a buyer adds contingencies for things like "satisfactory review by buyer's uncle who owns a similar business" or "approval of buyer's spouse who has not yet been informed of this purchase," those are signals that this buyer has unresolved issues that will delay or kill the deal.

Unrealistic timelines. An offer that says "closing in 14 days" on a deal that requires SBA financing isn't realistic. SBA loans take 60 to 90 days minimum. The buyer either doesn't understand the process or is making promises they can't keep.

No proof of funds. A serious buyer should be able to provide, at minimum, a letter from their bank or financial advisor confirming they have the liquidity for the down payment. If they can't produce this within 48 hours of making an offer, something is off.

Vague financing plans. "I plan to get a loan" is not a financing plan. "I've been pre-approved by Live Oak Bank for up to $600,000 with 15% down" is a financing plan. The difference between these two statements is the difference between a deal that closes and a deal that collapses in month three.

Lowball with escalation language. Some buyers submit a low offer and say "but I'm willing to go higher if needed." This is a negotiation tactic to anchor you to a low number. If they're willing to go higher, they should submit the higher offer.

How to Use Multiple Offers Ethically

You have a responsibility to handle competing offers honestly. Lying about other offers, fabricating interest that doesn't exist, or creating artificial urgency is unethical and can create legal liability. But that doesn't mean you have to be passive.

Here's what's appropriate:

You can disclose that you have competing interest. Telling a buyer "we have received other offers and are evaluating all of them this week" is factual and fair. It lets them know they need to put their best foot forward.

You can set a deadline for best and final offers. Telling all parties "we're accepting final offers by Friday at 5:00 PM" creates a fair and transparent process.

You can share general terms without specific numbers. Telling a buyer "we have a competing offer with more favorable terms" is acceptable. I generally don't share specific competing offer amounts because it can create an artificial bidding war that leads to a buyer overextending.

You cannot fabricate offers. Telling a buyer you have three other offers when you have zero is fraud. Don't do it.

You cannot share one buyer's proprietary information with another. Buyer A's financial qualifications and offer terms are confidential. Don't share them with Buyer B.

Counter Offer Strategy

When you have multiple offers, you have two basic strategic approaches.

Option 1: Counter one buyer directly. If one offer is clearly the strongest but has one or two terms you want to improve, counter that buyer directly. For example, if Offer A is $650,000 but you want $675,000, and the buyer is well qualified with SBA pre-approval, counter at $675,000 and keep the other buyers informed that you're in active negotiations but haven't accepted an offer yet.

This approach works best when one offer is clearly superior and you don't want to risk losing that buyer by asking everyone to resubmit.

Option 2: Ask all buyers for best and final. If the offers are close in quality, invite all parties to submit their best and final offer by a specific deadline. Something like: "We've received multiple competitive offers and are asking all interested parties to submit their best and final terms by [date]. Please include your highest purchase price, proposed terms, and any changes to contingencies or timeline."

This approach works best when you have three or more competitive offers and want to maximize both price and terms.

A few rules for counter offers:

- Don't counter so aggressively that you scare off a good buyer. A counter that adds $100,000 to the price and demands a 30 day close will make most buyers walk away.

- Be specific. "We'd like to see $25,000 more on the purchase price and a 60 day close instead of 90" is a clear counter. "We need better terms" is vague and unproductive.

- Respond to all offers in a timely manner, even if you're not interested. A simple "we've decided to move forward with another buyer" keeps the door open for a backup.

Ready to put your business on the market and attract competing offers? Get a free consultation to discuss your sale strategy.

Why You Should Always Have a Backup Offer

This is something I preach to every seller I work with. Always keep a backup buyer in the loop. Always.

Deals fall through. The numbers vary by source, but in my experience, about 25% to 30% of accepted offers in small business sales don't make it to closing. The reasons are predictable: financing falls apart, due diligence reveals something the buyer can't accept, the landlord won't assign the lease, or the buyer simply gets cold feet.

If your deal falls apart and you have no backup buyer, you're starting the entire process over. You re-list the business (which now looks like "something must be wrong with it because it was under contract and came back"), you wait for new inquiries, you screen new buyers, and you've lost three to four months minimum.

If you have a backup buyer, you make a phone call. "The previous offer didn't work out. Are you still interested?" About half the time, the backup buyer is still interested and you can restart the process immediately.

Here's how to manage a backup offer:

- When you accept Offer A, call Offer B and say: "We've accepted another offer, but if anything changes, you're our first call. Are you comfortable being in a backup position?"

- Most buyers will say yes. They've already done their initial evaluation.

- Keep the backup buyer updated every two to three weeks with a simple "still in due diligence with the other buyer."

- If the primary deal falls apart, contact the backup buyer within 24 hours.

I've saved deals with this approach more times than I can count. One seller had a $1.2 million deal collapse after 67 days when the buyer's SBA lender pulled out. We called the backup buyer on day 68, re-negotiated terms in a week, and closed 45 days later. Without the backup, that seller would have been looking at another four to six months minimum.

A business that comes back on the market after a failed deal carries a stigma. Buyers wonder what the first buyer found during due diligence. Keeping a backup buyer warm costs you nothing but a brief phone call every two weeks, and it can save you months of lost time and a significant price discount if your primary deal falls apart.

Managing Buyer Emotions Through the Process

When you have multiple offers, you're dealing with multiple people who are emotionally invested in buying your business. How you manage those emotions matters for the outcome.

Buyers who feel jerked around, lied to, or disrespected will walk away even if the deal makes financial sense for them. Buying a business is personal. People are putting their savings, their career, and sometimes their family's future on the line. Treat every buyer with respect, even the ones you don't choose.

Be transparent about your process. Tell buyers upfront: "We're reviewing all offers this week and will respond by Friday." Then actually respond by Friday.

Don't ghost buyers. If you're moving forward with someone else, tell the other buyers. A 60 second phone call is all it takes. "We've decided to move forward with another buyer. If anything changes, we'll be in touch."

Don't create a bidding war for sport. Going back to buyers three and four times asking for "just a little more" is exhausting for everyone and usually results in buyers walking away. One round of best and final is standard. Two rounds is the max before buyers lose trust.

Be honest about timelines. If you need a week to decide, say that. Buyers are far more patient with honest delays than with silence.

When to Accept Less Money for Better Terms

This is the part where most sellers struggle, because it feels counterintuitive to accept a lower offer. But sometimes the lower offer is the better deal.

Here are situations where I've advised clients to take less money:

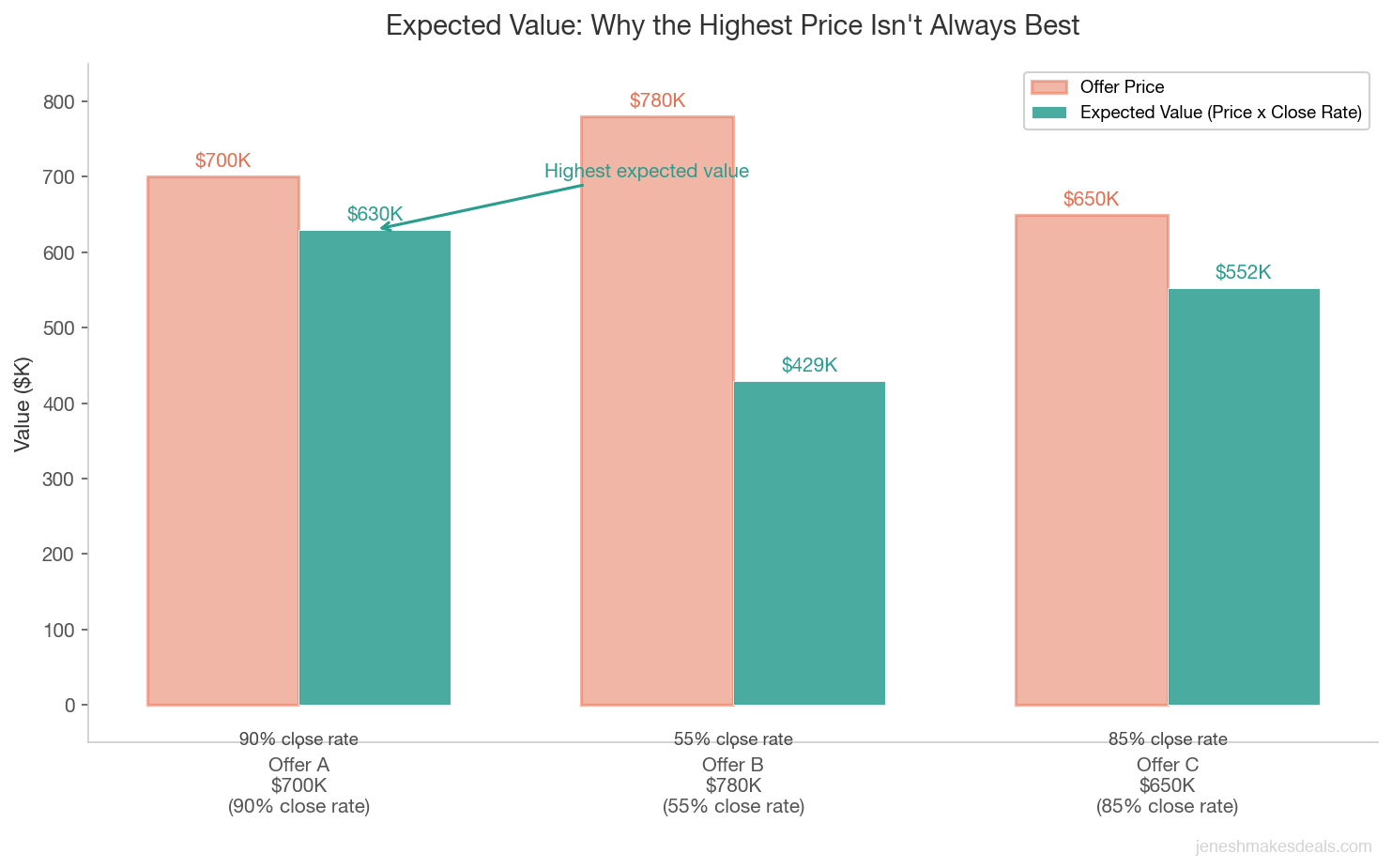

The higher offer has shaky financing. A $700,000 offer from a buyer with marginal credit, no pre-approval, and 10% down is worth less than a $650,000 offer from a buyer with 25% down, an SBA pre-approval letter, and 780 credit. The first offer has maybe a 50% chance of closing. The second has an 85% chance. Expected value math: $700,000 x 50% = $350,000. $650,000 x 85% = $552,500. The lower offer has a higher expected value.

You need to close quickly. If you're relocating, dealing with health issues, or need liquidity for another investment, a fast close at a lower price may serve your needs better than waiting three to four months for a higher price that might not materialize. Time has a real cost.

The higher offer comes with a large earnout. A $800,000 offer with a $200,000 earnout based on 12 months of post sale revenue is really a $600,000 guaranteed offer. If the alternative is a $725,000 offer with no earnout, take the $725,000.

The higher offer has seller financing you're uncomfortable with. A $750,000 offer where you carry a $250,000 note at 5% for seven years means you're a lender for seven years. If the buyer defaults, you may have to pursue legal action. A $680,000 all cash offer eliminates that risk. Sometimes sleeping well at night is worth $70,000.

I tell every seller the same thing: multiply the offer price by the probability it actually closes. A $700,000 offer with a 90% chance of closing is worth more than a $780,000 offer with a 55% chance. Run the expected value math before you fall in love with a big number.

Curious what your business is really worth? Run the numbers with our valuation calculator to make sure any offer you're considering is in the right range.

The Role of Your Broker in Managing Multiple Offers

If you're working with a business broker (and you should be when multiple offers are in play), here's what your broker should be doing:

Qualifying every buyer before presenting offers. Your broker should verify financial capability and ensure every buyer who submits an offer is capable of closing. You shouldn't be reviewing offers from unqualified buyers.

Presenting all offers fairly. Your broker presents every qualified offer with a clear summary of price, terms, contingencies, buyer strength, and their assessment of closing probability. The decision is yours, but your broker's experience in evaluating offer quality is one of the most valuable things they bring to the table.

Managing communication with all buyers. Your broker is the single point of contact. This prevents buyers from contacting you directly and ensures consistent messaging. When one buyer asks "are there other offers?", your broker handles it.

Negotiating counter offers. A good broker can squeeze an extra $20,000 to $50,000 out of a deal without alienating the buyer, because they know where the real limits are.

Managing the backup buyer relationship. Your broker keeps the backup buyer warm and is ready to pivot if the primary deal falls apart.

Keeping you emotionally grounded. Selling your business is emotional. A good broker has seen this dozens of times and can help you make a clear, rational decision instead of second guessing yourself.

Don't have a broker yet? If you're expecting multiple offers, now is the time to get professional help. Schedule a free consultation to discuss your options.

Common Mistakes Sellers Make with Multiple Offers

I've been doing this long enough to see the same mistakes repeated. Here are the ones that cost sellers the most money and time.

Chasing the highest number. The highest price means nothing if the buyer can't close. I had a client who chose an $880,000 offer over an $820,000 offer. The $880,000 buyer couldn't get financing. Four months later, the $820,000 buyer had purchased a different business. My client eventually sold for $790,000. Chasing the extra $60,000 cost them $30,000 and four months.

Taking too long to decide. When you have multiple offers, the clock is ticking. Buyers have other businesses they're looking at. If you take three weeks to evaluate offers, some of those buyers will move on. I tell my clients to make a decision within five to seven business days of receiving the last offer. Urgency is your friend.

Negotiating with everyone simultaneously. Pick your top choice and negotiate with them. If those negotiations fail, move to your second choice. Trying to negotiate with three buyers at once is confusing, time consuming, and often backfires when buyers find out (and they sometimes do) that you're playing them against each other.

Ignoring buyer qualifications. A buyer who says "I'll figure out financing later" is not a qualified buyer. Don't let the excitement of a high offer blind you to the reality that this person may not be able to close.

Failing to get offers in writing. Verbal offers mean nothing. Every offer should be in writing with specific terms: purchase price, down payment, financing method, contingencies, proposed closing date, and earnest money. If a buyer won't put it in writing, they're not serious.

Making Your Final Decision

When it comes down to it, the decision about which offer to accept comes back to three questions:

-

Which buyer is most likely to actually close? Look at their financial strength, their pre-approval status, their experience, and the structure of their offer. A 90% chance of closing at $700,000 is better than a 60% chance of closing at $780,000.

-

Which offer gives you the best overall value? This means price, terms, risk, and timeline combined. Not just the number on the first line.

-

Which timeline and structure fits your life? If you need to close by September because you're moving, a cash buyer who can close in 30 days might be better than an SBA buyer who needs 90 days but offers $40,000 more. Your personal situation matters.

Getting multiple offers is the result of doing things right. Don't waste that advantage by grabbing the shiniest offer without looking underneath it. Evaluate every offer on the full picture. Use the scoring matrix. Keep a backup buyer. And trust the process.

Thinking about selling and want to make sure you're positioned for multiple offers? Reach out for a free consultation and let's talk about your business, your timeline, and your goals.

Related Articles

April 16, 2026

Preparing Your Business for Sale: The 12 Month Checklist

The best time to start preparing your business for sale is 12 months out. Here's exactly what to do each quarter.

April 9, 2026

Best Time of Year to List Your Business for Sale

Timing your listing right can mean more buyers, better offers, and a faster close. Here's what the data says about when to go to market.

April 3, 2026

How to Handle the Transition After Selling Your Business

The 30 to 90 days after closing can make or break the deal. Here's how to handle the transition smoothly.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.