If I could give every business owner one piece of advice about selling, it would be this: start preparing at least 12 months before you want to go to market. Not 3 months. Not 6 months. Twelve months minimum.

I know that feels like a long time. But every seller I've worked with who started early ended up with a higher sale price, a smoother transaction, and far less stress than those who rushed to market. The ones who tried to sell with 90 days of preparation? They almost always left money on the table, dealt with surprises during due diligence, or had deals fall apart because something wasn't ready.

Preparing a business for sale is like preparing a house for sale. You could list it tomorrow with dishes in the sink and paint peeling off the walls. Or you could spend a few months fixing it up and staging it properly. The second approach costs more upfront but brings a significantly higher return.

Sellers who start preparing 12 months out consistently achieve higher sale prices, smoother transactions, and far fewer deal failures than those who rush to market with 90 days of preparation.

Before diving into the checklist, take our exit readiness assessment to see where your business stands today and which areas need the most attention.

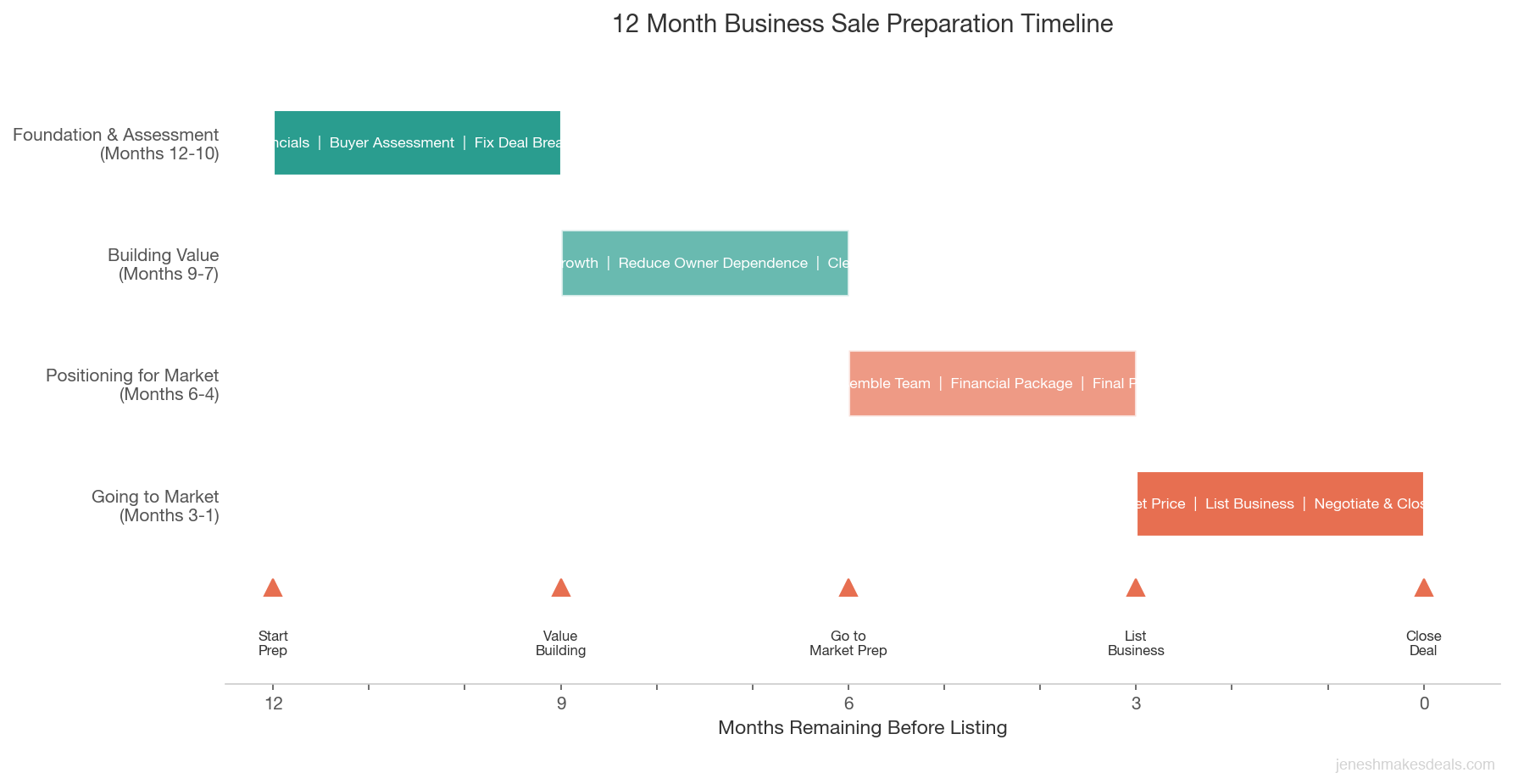

Here's your month by month checklist for the 12 months leading up to listing your business.

Months 12 to 10: Foundation and Assessment

This first quarter is about understanding where you stand and setting yourself up for success. No one knows you're selling yet, and that's intentional.

Month 12: Get Your Financial House in Order

Review your last three years of financials. Pull your tax returns, profit and loss statements, and balance sheets. Look at them through a buyer's eyes. Are they clean? Are they consistent? Do they tell a story of a profitable, well managed business?

Identify and document all add backs. These are personal expenses running through the business that inflate costs: your car, phone, family members on payroll, personal travel, one time expenses. Create a clear schedule showing each add back, the amount, and supporting documentation.

Start working with a CPA experienced in business sales. Not just any CPA. You need someone who has been through M&A transactions and understands how buyers and lenders will evaluate your financials. If your current accountant has never worked on a business sale, it's time to add one to your team who has.

Calculate your adjusted earnings. Using your add back schedule, figure out your true SDE (seller's discretionary earnings) or EBITDA. This number will be the foundation of your valuation. If you don't like what you see, you have time to improve it.

Need help understanding your numbers? Use our free business valuation calculator to see what your adjusted earnings translate to in terms of business value.

Month 11: Assess Your Business Through a Buyer's Eyes

Walk through your business as if you were buying it. What would concern you? What looks dated or neglected? What would impress you? Make a list.

Evaluate your team. Who are your key employees? Would they stay after a sale? Are there any positions that are understaffed? Any roles where only one person has critical knowledge? Start addressing gaps now.

Review your customer concentration. Look at your top 10 customers by revenue. If any single customer represents more than 15% of your total revenue, start working to diversify. You have time, but you need to start now.

Assess your lease situation. When does your lease expire? What are the renewal terms? A business with a lease expiring in 6 months is a tough sell. You'll want at least 3 to 5 years of remaining lease term, preferably with renewal options.

Document your operations. Start creating or updating your operations manual. This should cover everything a new owner needs to know: daily routines, vendor contacts, employee procedures, customer management processes, and equipment maintenance schedules.

Month 10: Address the Big Issues

Fix anything that could be a deal breaker. Pending lawsuits, environmental issues, tax problems, compliance gaps. These things don't go away during a sale. They get worse. Address them now while you have time and bargaining power.

Resolve any partner or shareholder issues. If you have co owners, make sure everyone agrees on selling and on the terms. Partnership disputes during a sale process can kill deals and add months of delay.

Update your legal documents. Review your business entity documents, operating agreements, key contracts, insurance policies, and any intellectual property registrations. Make sure everything is current and in order. Our seller due diligence checklist walks you through every document category buyers will request so nothing falls through the cracks.

Get a preliminary valuation. Work with a broker or business appraiser to understand what your business is currently worth. This gives you a baseline and helps you identify which improvements will have the biggest impact on value.

Months 9 to 7: Building Value

Now that you know where you stand, this quarter is about making strategic improvements that increase your business value.

Month 9: Strengthen Your Revenue

Diversify your customer base. If you identified concentration risk in month 11, you should be actively pursuing new customers. Every new customer you add reduces concentration and increases the perceived stability of your revenue.

Lock in key customers with contracts. Move your best customers to service agreements, annual contracts, or subscription models where possible. Contracted revenue is worth more than transactional revenue in the eyes of a buyer.

Review your pricing. Many business owners haven't raised prices in years. If you're below market, implement gradual price increases now. You want at least 6 months of results at the new pricing to show buyers that the higher margins are sustainable.

Focus on recurring revenue. Any revenue you can make predictable and recurring increases your valuation multiple. Maintenance contracts, retainer agreements, subscription services, and automatic reorders all count.

Month 8: Reduce Owner Dependence

Delegate key responsibilities. Start handing off tasks that only you currently do. Sales calls, vendor negotiations, employee management, customer relationship management. If it requires your personal involvement, start training someone else to do it.

Hire or promote a manager. If you don't have someone who can run the day to day without you, now is the time to make that hire. A buyer needs to see that the business can operate without the previous owner.

Step away for test periods. Take a week off without checking in. Then take two weeks. How did the business perform? What problems came up? These test runs reveal the gaps in your management structure that need to be filled before going to market.

Document your personal processes. All those things you do by instinct, how you handle difficult customers, how you price custom jobs, how you decide which suppliers to use, write them down. Turn your personal knowledge into company knowledge.

A business that runs without its owner is worth significantly more than one that depends on a single person. If you can take two weeks off and the business doesn't skip a beat, you've built something a buyer will pay a premium for.

Month 7: Clean Up Operations

Address deferred maintenance. Fix the leaky roof, replace the aging HVAC system, repair the parking lot. These things will come up during due diligence and will either reduce your sale price or give the buyer negotiating power.

Update technology. If you're running your business on spreadsheets and post it notes, invest in proper systems. A modern POS system, CRM, accounting software, or scheduling platform makes the business easier to evaluate and operate.

Organize your files. Create a well organized digital file system with all important documents: contracts, leases, insurance policies, employee records, vendor agreements, permits, and licenses. Buyers will request all of this during due diligence.

Review and update your insurance. Make sure all policies are current and adequate. Check for any gaps in coverage that could be an issue during the sale process.

Ready to start the selling process? Contact us for a free consultation and we'll help you create a customized preparation plan.

Months 6 to 4: Positioning for Market

You're halfway there. This quarter is about polishing the business and getting ready to go to market.

Month 6: Assemble Your Team

Select your business broker. If you haven't already, interview at least three brokers and choose one who specializes in your industry. The broker will guide you through the rest of the process, but having them on board at the 6 month mark gives them time to learn your business and develop a marketing strategy.

Engage your attorney. You need a business attorney experienced in M&A transactions, not your general counsel who handles contracts and employment issues. Your M&A attorney will review the listing agreement, prepare for due diligence, and eventually negotiate the purchase agreement.

Brief your CPA. Let your accountant know you're moving forward. They'll need to prepare specific financial documents and may need to recast your financials to show adjusted earnings. Having your CPA ready to respond quickly to buyer inquiries is important.

Consider a sell side quality of earnings report. For businesses valued over $2 million, commissioning your own QofE can accelerate the process and strengthen your negotiating position. Now is the time to start that process if you're going to do it.

Your Advisory Team at a Glance

| Team Member | Primary Role | When to Engage | What to Look For |

|---|---|---|---|

| Business Broker | Marketing, buyer screening, deal management | Month 6 | Industry specialization, recent comparable sales |

| M&A Attorney | Contract review, due diligence, closing docs | Month 6 | M&A transaction experience, not just general counsel |

| CPA | Financial recasting, tax planning, add back documentation | Month 12 | Prior experience with business sale transactions |

| Wealth Advisor | Post sale tax strategy, proceeds management | Month 6 to 4 | Experience with business exit planning |

Your advisory team, a broker, M&A attorney, and experienced CPA, is the single biggest factor in protecting your sale price and avoiding deal killing surprises during due diligence.

Month 5: Financial Preparation

Prepare your financial package. Working with your broker and CPA, put together the documents buyers will want: three to five years of tax returns, profit and loss statements, balance sheets, equipment lists, customer lists (anonymized initially), and your add back schedule with documentation.

Create a confidential information memorandum (CIM). Your broker will typically prepare this, but you'll need to provide the information. The CIM is the marketing document that presents your business to potential buyers. It covers your history, operations, financials, growth opportunities, and everything a buyer needs to evaluate the opportunity.

Forecast the current year. Provide a credible projection for the current fiscal year. Buyers want to see that current performance is tracking with or above historical results.

Address any financial red flags. Declining margins, increasing debt, rising costs. If there are negative trends, develop explanations and, where possible, corrective actions. It's better to proactively address these in your CIM than to have a buyer discover them during diligence.

Month 4: Final Preparations

Verify all licenses and permits. Make sure every license, permit, and certification your business requires is current and transferable. Expired or non transferable licenses can delay or kill a deal.

Confirm your lease transfer process. Talk to your landlord's representative (or have your attorney do it) to understand what's required to assign or transfer your lease. Some landlords require financial qualification of the buyer. Others have first refusal rights. Know the process before a buyer asks about it.

Prepare employee transition plans. You don't want to tell employees yet, but you should have a plan for when and how you'll communicate the sale. Identify key employees who'll be critical to the transition and think about retention incentives.

Take care of any last cosmetic improvements. Deep clean the facility, update signage, fix anything that creates a negative first impression. You want the business to look its best when buyers start visiting.

Months 3 to 1: Going to Market

The final quarter is when the business officially goes on the market and you start interacting with potential buyers.

Month 3: Launch

Finalize your asking price. Working with your broker, set a realistic asking price based on your adjusted earnings, comparable sales, and current market conditions. Price it right from the start. Overpricing leads to sitting on the market and eventually selling for less than you would have with a fair initial price.

List the business. Your broker will launch the marketing campaign across their platforms, buyer databases, and targeted outreach channels. The business should be presented confidentially, without identifying information available to unqualified browsers.

Establish a showing protocol. Decide how buyer visits will work. Will they happen after hours? During slow periods? Will you be present? Your broker should manage the logistics, but you need to be available and flexible.

Prepare for buyer questions. Buyers will ask tough questions about everything from customer retention to why you're selling. Work with your broker to prepare honest, compelling answers to the most common questions.

Month 2: Buyer Management

Respond promptly to information requests. Speed matters in deal making. When buyers or their advisors request documents or information, get it to them within 24 to 48 hours. Delays signal disorganization or that you're hiding something.

Maintain business performance. This is critical. Many sellers mentally check out once they decide to sell. Don't let revenue slip, don't cut back on marketing, and don't let maintenance slide. Buyers are watching current performance closely, and any decline will raise red flags.

Be available for meetings and calls. Buyers who are seriously interested will want to meet you, tour the facility, and ask detailed questions. Make time for this. Your enthusiasm and cooperation signals that you're a serious seller.

Start due diligence preparation. Even before receiving an offer, start organizing all the documents a buyer will request during due diligence. Your broker can give you a typical due diligence checklist. Having everything ready shortens the timeline from offer to close.

Month 1: Closing Stretch

Evaluate offers carefully. Don't just look at the price. Consider the terms: financing contingencies, due diligence period, transition requirements, earnout provisions, and non compete terms. Sometimes a slightly lower price with cleaner terms is the better deal.

Negotiate with your endgame in mind. Know what your minimum acceptable terms are before negotiations start. Be willing to compromise on things that don't matter as much to protect what does.

Support the due diligence process. Once you accept an offer, the buyer will begin formal due diligence. Your job is to be responsive, transparent, and organized. The faster due diligence goes, the more likely the deal closes.

Plan your transition. Start thinking practically about how you'll hand over the business. Most deals include a 30 to 90 day transition period where you help the new owner learn the business. Plan what that looks like.

The Complete Checklist: Quick Reference

Here's the full 12 month checklist in a format you can print and track.

| Month | Key Actions |

|---|---|

| 12 | Review 3 year financials, document add backs, engage M&A experienced CPA |

| 11 | Customer concentration analysis, lease review, start operations manual |

| 10 | Fix deal breakers, resolve partner issues, get preliminary valuation |

| 9 | Diversify customers, lock in contracts, review pricing, build recurring revenue |

| 8 | Delegate responsibilities, hire/promote manager, test stepping away |

| 7 | Deferred maintenance, technology updates, organize files |

| 6 | Select broker, engage M&A attorney, consider sell side QofE |

| 5 | Prepare financial package, create CIM, forecast current year |

| 4 | Verify licenses, confirm lease transfer, plan employee transition |

| 3 | Set asking price, list business, establish showing protocol |

| 2 | Respond to buyer inquiries, maintain performance, prepare for due diligence |

| 1 | Evaluate offers, negotiate terms, support due diligence, plan transition |

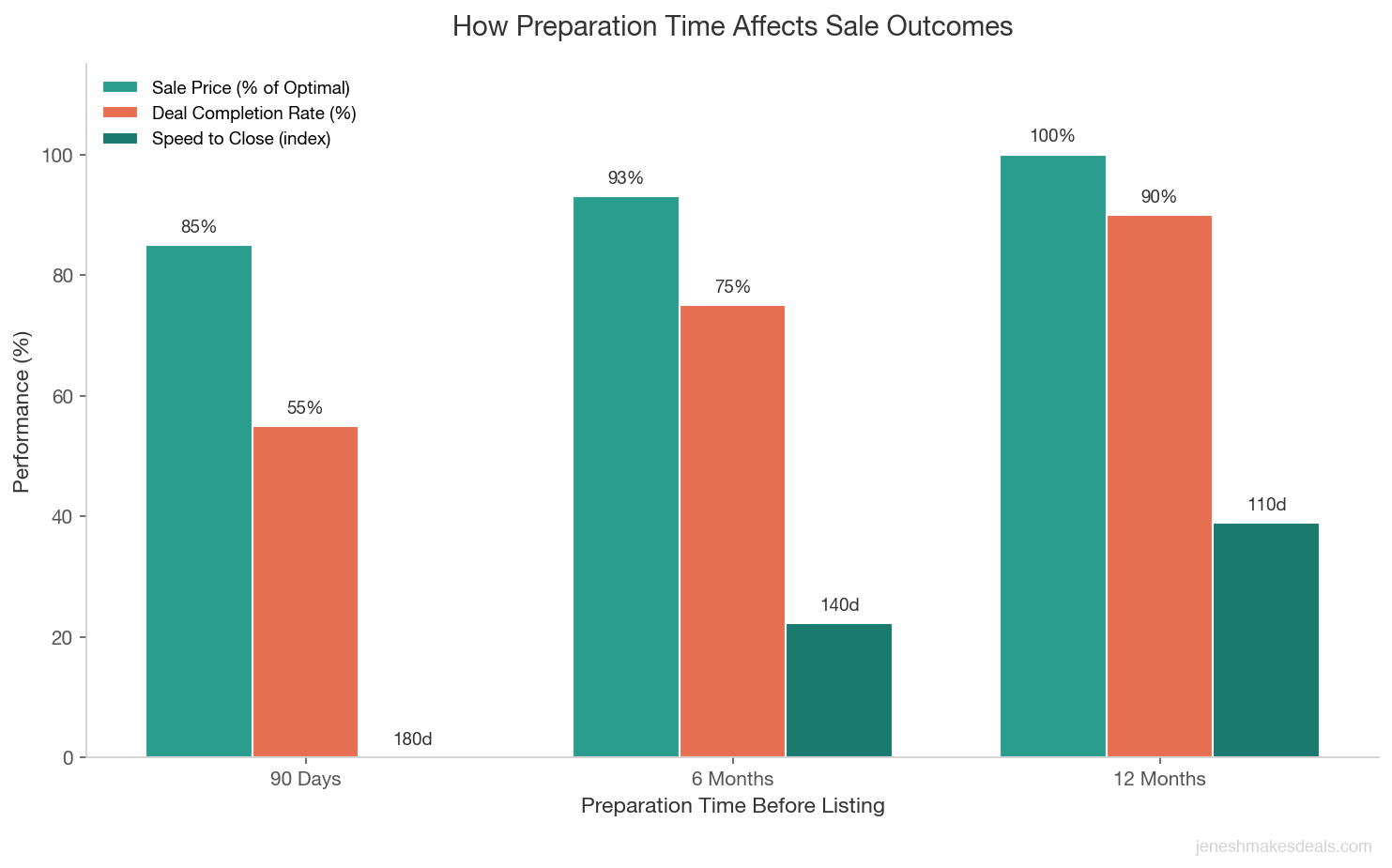

How Preparation Time Affects Your Outcome

The data is clear: more preparation time leads to better results across every metric that matters to sellers.

| Preparation Time | Typical Sale Price | Deal Completion Rate | Average Days to Close |

|---|---|---|---|

| 90 days | 85% of optimal value | 55% | 180 days |

| 6 months | 93% of optimal value | 75% | 140 days |

| 12 months | 100% of optimal value | 90% | 110 days |

What If You Don't Have 12 Months?

I know not everyone has the luxury of a full year to prepare. Sometimes circumstances force a quicker timeline: health issues, partnership problems, burnout, or a buyer approaching you unexpectedly.

If you have 6 months, focus on the financial preparation (months 12 to 10 actions), the most impactful value building activities (months 9 to 7), and assembling your team (month 6). Skip the cosmetic improvements and focus on substance.

If you have 3 months, prioritize clean financials, a realistic valuation, an experienced broker, and honest presentation of your business as is. You may not get the highest possible price, but you can still get a fair deal with good preparation.

If a buyer approaches you tomorrow, don't panic. Slow the process down enough to get an attorney and broker involved, understand what your business is actually worth, and protect your interests in negotiations. Even a week of preparation is better than none.

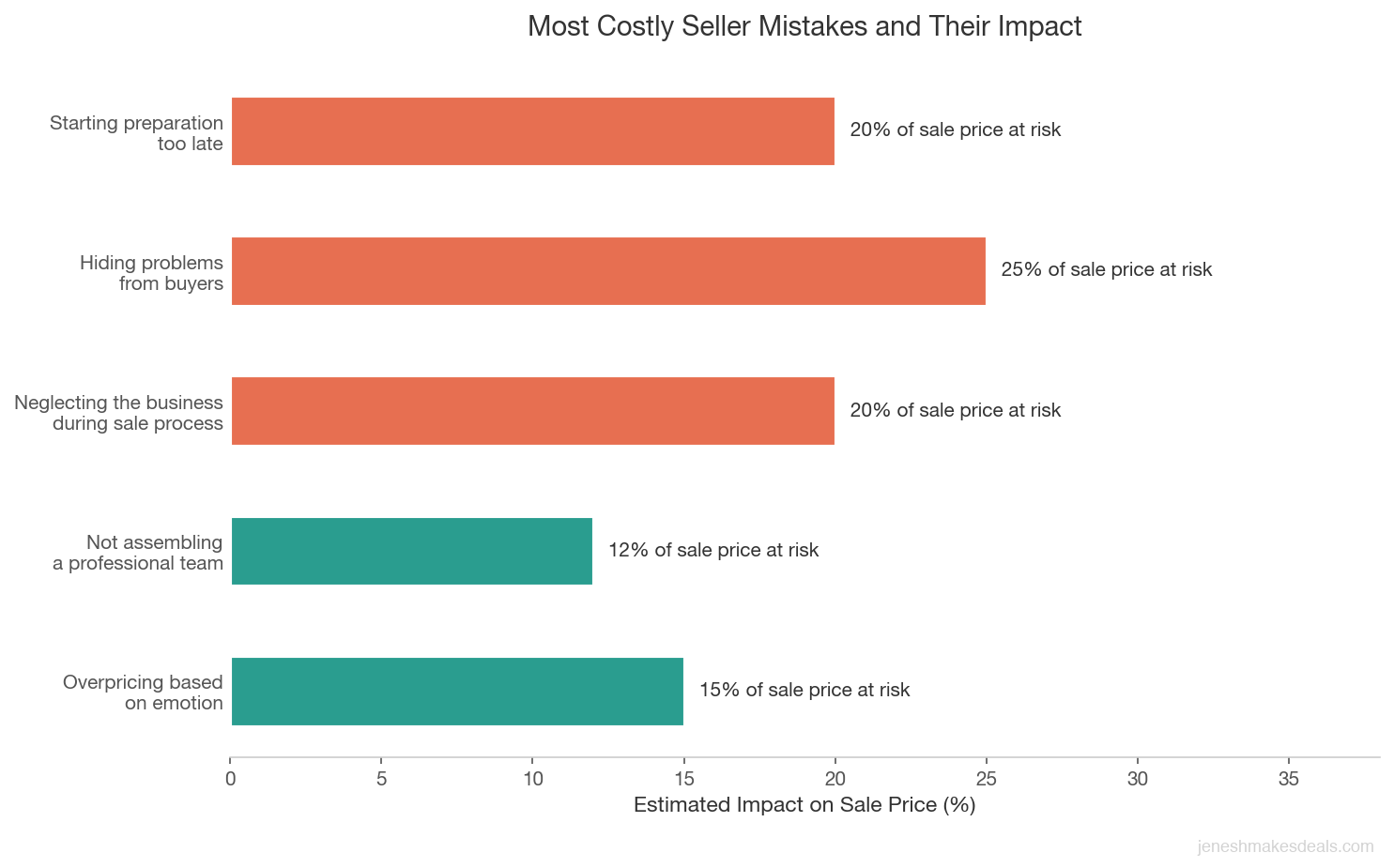

The Biggest Preparation Mistakes I See

After working with dozens of sellers, these are the mistakes that cost people the most money and cause the most deal failures.

Starting too late. By far the most common mistake. Sellers decide they want to sell and expect to close within 90 days. The average small business sale takes 6 to 12 months from listing to closing, and that's after preparation.

Hiding problems. Every business has issues. Trying to hide them doesn't make them go away, it makes them emerge during due diligence when they do maximum damage to your credibility and sale price. Disclose early, address what you can, and be honest about what you can't.

Neglecting the business during the sale process. Buyers evaluate the business as it is today, not as it was when you decided to sell. A revenue decline during the marketing period can tank a deal. Keep running the business like you plan to own it forever.

Not assembling a team. Trying to sell a business without a broker, attorney, and CPA experienced in M&A is like performing surgery on yourself. You might survive, but the outcome will be worse than if you'd hired professionals.

Overpricing based on emotion. Your business might be your life's work. That emotional attachment doesn't translate to market value. Price it based on data, comparables, and realistic earnings, not on what you feel it's worth or what you need for retirement.

Thinking about selling? Contact us for a free consultation and we'll help you figure out where you are in this timeline and what to prioritize first.

The Bottom Line

The best exit is a prepared exit. Twelve months gives you enough time to clean up your financials, build transferable value, assemble the right team, and go to market with confidence.

You don't have to do everything on this list to sell your business. But every item you complete strengthens your position, increases your sale price, and reduces the chance of a deal falling apart. Start where you are, focus on the highest impact items first, and keep moving forward.

Your future self, and your bank account, will thank you.

Want to see what your business might be worth today? Try our free business valuation calculator to get a quick estimate and start planning your exit. For a full walkthrough of the selling process from start to finish, download our free Complete Guide to Selling Your Business in 2026.

When you're ready to start your 12 month countdown, tell us about your business and we'll help you build a plan.

Related Articles

April 12, 2026

How to Handle Multiple Offers on Your Business

Multiple offers are a great problem to have. But picking the wrong one can cost you months and thousands. Here's how to evaluate them.

April 9, 2026

Best Time of Year to List Your Business for Sale

Timing your listing right can mean more buyers, better offers, and a faster close. Here's what the data says about when to go to market.

April 3, 2026

How to Handle the Transition After Selling Your Business

The 30 to 90 days after closing can make or break the deal. Here's how to handle the transition smoothly.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.