I've sat across the closing table on a lot of deals, and one of the questions I get most often from both buyers and sellers is about what happens after the sale closes. What if the financials turn out to be slightly off? What if a lawsuit surfaces that the seller didn't disclose? What if a key customer contract has an assignment restriction nobody caught?

That's where representations and warranties insurance comes in. It's one of those tools that used to be reserved for massive private equity deals, but it's moved steadily into the middle market and even smaller transactions over the last decade. If you're buying or selling a business in the $10 million to $100 million range, you've probably heard it mentioned. If you haven't yet, you will.

This post breaks down exactly what R&W insurance is, how it works, who pays for it, what it costs, and whether it makes sense for your deal.

What Are Representations and Warranties in a Purchase Agreement?

Before you can understand R&W insurance, you need to understand what reps and warranties actually are in the context of a business sale.

When a seller signs a purchase agreement, they're making a series of factual statements about the business. These are called representations and warranties, or "reps and warranties" for short. They cover things like: the financial statements are accurate, there are no undisclosed lawsuits, all employees are properly classified, there are no environmental issues on the property, all material contracts are valid and in good standing.

The buyer relies on these statements when deciding whether to close the deal and at what price. If one of those statements turns out to be false or misleading, the buyer has suffered what's called a "breach of representations and warranties." That breach gives the buyer a claim against the seller for the resulting damages.

In a traditional deal structure, the seller sets aside a portion of the sale proceeds in escrow for 12 to 24 months to cover potential claims. Escrow amounts of 10% to 15% of the purchase price are common. This holdback is the buyer's security blanket if something goes wrong after closing.

The problem with escrow is that it's expensive for sellers. If you're selling a $15 million business and 10% goes into escrow, you're waiting on $1.5 million for up to two years. That's capital you can't reinvest, distribute to co-owners, or use to buy your next thing. And for buyers, even a $1.5 million escrow might not be enough if a major issue surfaces.

On a $15 million deal with a 10% escrow, the seller has $1.5 million locked up for up to two years. R&W insurance can eliminate or dramatically reduce that holdback, letting sellers walk away at closing with nearly the full purchase price.

R&W insurance was created to solve exactly this tension.

What Is R&W Insurance and How Does It Work?

Representations and warranties insurance is a policy that pays out when a covered breach of reps and warranties occurs in a business purchase agreement. Instead of the seller holding funds in escrow to cover claims, an insurance company steps in to pay valid claims up to the policy limit.

There are two types of policies: buy side (also called buyer side) and sell side. In the vast majority of deals today, about 90% of them, the buyer purchases the policy. The buyer side policy pays the buyer directly when a covered breach causes a loss. The seller side policy, which is much less common, protects the seller if the buyer brings a claim and wins.

Here's the basic mechanics of a buyer side policy. The buyer applies for coverage during due diligence. The insurer reviews the due diligence materials, the purchase agreement, and the rep and warranty schedules. The insurer then issues a policy that will pay covered losses caused by a breach of any representation in the agreement, up to the policy limit, subject to a retention amount (the equivalent of a deductible).

If a breach surfaces after closing, the buyer first absorbs losses up to the retention amount. Once losses exceed the retention, the insurer pays out up to the policy limit. The seller is largely off the hook, because the insurer's right to "subrogate" against the seller (sue the seller to recover what the insurer paid) is typically waived except in cases of fraud.

Who Pays for R&W Insurance?

In buyer side deals, which are the norm, the buyer pays the premium. This has become standard practice in private equity and strategic M&A transactions. The reasoning is straightforward: the buyer benefits from the coverage, so the buyer pays for it.

That said, deal economics are negotiated. In some situations, the seller effectively bears the cost by accepting a slightly lower headline price. In other deals, especially competitive processes where multiple buyers are bidding, the buyer absorbs the full cost to make their offer more attractive by promising a clean exit to the seller.

Seller side policies do exist and are occasionally used when a seller wants protection against a buyer bringing a spurious claim after closing. Sell side coverage is less common and generally more expensive relative to the risk it covers.

The party that pays the premium also matters for tax purposes. Premiums paid by the buyer for buyer side coverage are generally treated as part of the cost basis of the acquired business, not as a deductible expense. Sellers should confirm tax treatment with their CPA before closing.

What Does R&W Insurance Cost?

Pricing has come down significantly over the last several years as more insurers have entered the market. Here's what to expect.

Premium rates currently run between 2% and 4% of the policy limit. On a $10 million policy, that's $200,000 to $400,000 in premium, paid upfront at closing as a one-time cost. The rate varies based on deal size, industry, due diligence quality, and the specific reps being covered.

Retention amounts (the deductible) are typically set at 1% of the transaction value for the first period after closing, often dropping to 0.5% in the second year. On a $20 million deal, that means the buyer self-insures the first $200,000 to $400,000 of loss before the policy pays.

Policy limits are usually set at 10% to 20% of the enterprise value of the deal. Some transactions go higher, up to 30% or even full value in specific situations, but 10% to 15% is the sweet spot for most middle market deals.

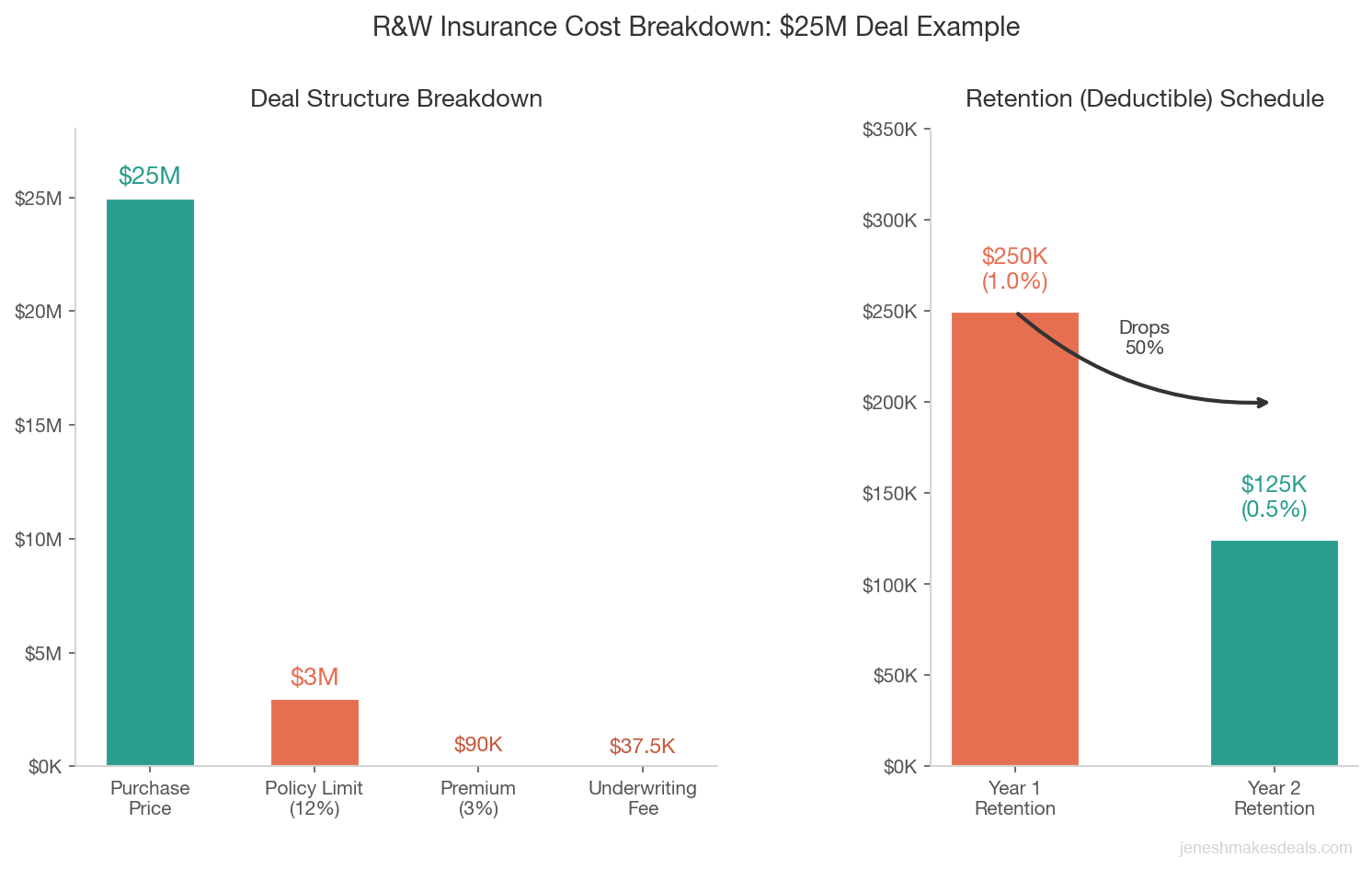

Here's a quick example to make the numbers concrete:

| Deal Component | Example |

|---|---|

| Purchase price | $25,000,000 |

| Policy limit (12%) | $3,000,000 |

| Premium rate | 3% |

| Total premium cost | $90,000 |

| Initial retention (1%) | $250,000 |

| Year 2 retention (0.5%) | $125,000 |

In this example, the buyer spends $90,000 at closing to get $3 million of coverage. If a breach surfaces and causes $500,000 in damage, the buyer absorbs the first $250,000 (the retention) and the insurer pays the remaining $250,000. If the loss hits $1.5 million, the buyer pays $250,000 and the insurer covers $1,250,000.

Here's how those claim scenarios play out side by side:

| Scenario | Loss Amount | Buyer Pays (Retention) | Insurer Pays | Buyer Recovery Rate |

|---|---|---|---|---|

| Small breach | $500,000 | $250,000 | $250,000 | 50% |

| Medium breach | $1,500,000 | $250,000 | $1,250,000 | 83% |

| Policy limit breach | $3,000,000 | $250,000 | $2,750,000 | 92% |

| Exceeds policy | $4,000,000 | $1,250,000 | $2,750,000 | 69% |

There are also underwriting fees. Most insurers charge a non-refundable diligence fee of $25,000 to $50,000 just to review the deal, which is separate from the premium. Some brokers bundle this into the closing costs; others quote it as a standalone line item. To see how the R&W premium fits into your total closing costs alongside broker fees, legal, and taxes, run the numbers through the business sale cost calculator.

When Does R&W Insurance Make Sense?

This is the question I get most often. Not every deal needs R&W insurance, and it's not available for every deal. Here's how I think about the thresholds.

Deal size. Most R&W insurers have a minimum transaction size, generally $10 million to $15 million in enterprise value. Below that threshold, the economics don't work because the minimum premium makes coverage prohibitively expensive as a percentage of deal value. There are some newer insurers trying to push into the $5 million to $10 million range with simplified products, but the market is still thin at that level.

Deal structure. R&W insurance works best in asset deals and stock deals where the purchase agreement is well-drafted with detailed rep schedules. Deals that close quickly with minimal due diligence are harder to insure because the insurer won't have enough information to underwrite the risk.

Competitive auctions. If a seller is running a formal sale process with multiple bidders, offering a clean exit without a large escrow holdback is a real competitive advantage. R&W insurance makes that possible, and savvy sellers in competitive processes often encourage buyers to get coverage as a deal sweetener.

Private equity buyers. PE firms use R&W insurance on nearly every deal above $15 million because it's a clean, institutionally accepted way to handle post-closing liability. If you're selling to a PE firm, expect them to bring it up early in the process.

Owner-operator sellers. If you built the business over 20 years and you want a clean break, R&W insurance can eliminate or dramatically reduce the escrow holdback. Instead of waiting 18 months for 10% of your proceeds, you walk away at closing with nearly the full amount.

Benefits for Sellers: The Clean Exit

For sellers, R&W insurance is mostly about getting your money and moving on. The traditional escrow structure is a real drag. You've closed the deal, but 10% of the purchase price is sitting in an escrow account you can't touch for a year or two. Meanwhile, the buyer can file claims against that escrow for almost any reason, valid or not, and you have to spend time and money defending yourself.

With R&W insurance in place, the seller's liability is typically capped at a much smaller amount, sometimes just the retention, and the escrow is either eliminated or reduced substantially. A $20 million deal might drop from a $2 million escrow to a $500,000 "fraud carve out" fund, or no escrow at all.

The other major benefit is relationship preservation. In owner-operated businesses, sellers often stay on for a transition period. Having the insurance company, not the buyer's attorney, as the party investigating a post-closing claim makes that transition much less adversarial. Claims become an insurance matter rather than a personal dispute between buyer and seller.

If you want to understand what a clean exit really looks like financially, run your numbers through the business valuation calculator to see what your net proceeds might be after accounting for taxes, advisor fees, and deal structure.

Benefits for Buyers: Protection Without the Chase

For buyers, R&W insurance solves a different problem. Even with an escrow in place, collecting on a breach of reps can be a nightmare. You have to prove the breach, quantify the damages, and then fight the seller (or their lawyer) over whether the claim is covered. Sellers drag their feet, claim the problems existed when you bought the business, and generally make collection difficult. By the time you actually recover anything, you've spent 20% of the recovery on legal fees.

With R&W insurance, the buyer files a claim with an insurance company instead of chasing down a former business owner. Insurers have claim adjustment processes, coverage counsel, and financial resources. You're not waiting on a seller to wire money from a personal account. You're working with a counterparty whose entire business is paying valid claims.

Buyers also get broader protection. Seller escrows typically cover only indemnified losses. A well-structured R&W policy covers all covered reps, including some that might not be subject to traditional indemnification in the purchase agreement.

This matters particularly in deals where the seller is an institution, like a PE-backed company, because institutional sellers negotiate hard to minimize post-closing exposure. R&W insurance lets buyers get coverage even when the seller's indemnification obligations are minimal.

If you're evaluating a business acquisition, use the deal calculator to model out how insurance costs affect your overall acquisition economics.

The Underwriting Process

Getting R&W insurance isn't instant. Here's what the underwriting process actually looks like on a timeline.

Step 1: Broker engagement. You engage an insurance broker who specializes in M&A insurance (not your general business insurance broker). They submit a deal summary to multiple insurers to get indication terms.

Step 2: Indication terms. Insurers respond with non-binding indication letters within two to three business days. These show the expected premium range, retention, and any major exclusions they anticipate.

Step 3: Underwriting call. If the deal moves forward, the insurer conducts a one to two hour underwriting call with the deal team. They ask about due diligence scope, known issues, financial performance, and specific reps. This is where you discuss any "known issues" that won't be covered.

Step 4: Due diligence review. The insurer (and sometimes outside coverage counsel) reviews your due diligence materials. They're looking for gaps, inconsistencies, and issues that signal elevated claim risk. Expect to share financial models, legal diligence, environmental reports, and the purchase agreement itself.

Step 5: Policy issuance. If everything checks out, the insurer issues a binder a day or two before closing. The final policy follows within 30 days.

The whole process takes two to three weeks from engagement to binder if everything goes smoothly. I recommend starting the process at least four weeks before the expected close date, because underwriting delays can push back the timeline.

Common Exclusions and Limitations

R&W insurance does not cover everything. This is important to understand before you rely on it as your sole form of post-closing protection.

Known issues. Anything identified in due diligence, disclosed in the rep schedules, or known to the buyer before closing is excluded. The insurer's whole model is based on unknown, unforeseen breaches. If you know about a problem and still close, you can't insure it.

Forward-looking statements. Reps about future performance, projections, or forecasts are generally not covered. If the seller says revenue will hit $5 million next year and it doesn't, that's not an R&W claim.

Environmental contamination. Some policies exclude environmental reps entirely or severely limit coverage. If there are any environmental concerns, you typically need a separate environmental liability policy.

Pension and benefits liabilities. ERISA and employee benefit obligations often have limited coverage due to the complexity and open-ended nature of the liability.

Purchase price adjustments. Working capital true-ups and post-closing price adjustments are almost universally excluded. Those get handled separately through the purchase agreement mechanics.

Fraud by the insured. If the buyer commits fraud in the application process, the insurer can deny coverage.

Tax matters. Tax reps are sometimes excluded or subject to a separate tax liability policy, particularly for complex tax structures.

The exclusion list is one reason you still need good legal and financial due diligence even when R&W insurance is in place. The policy is a backstop for unexpected breaches, not a substitute for thorough diligence.

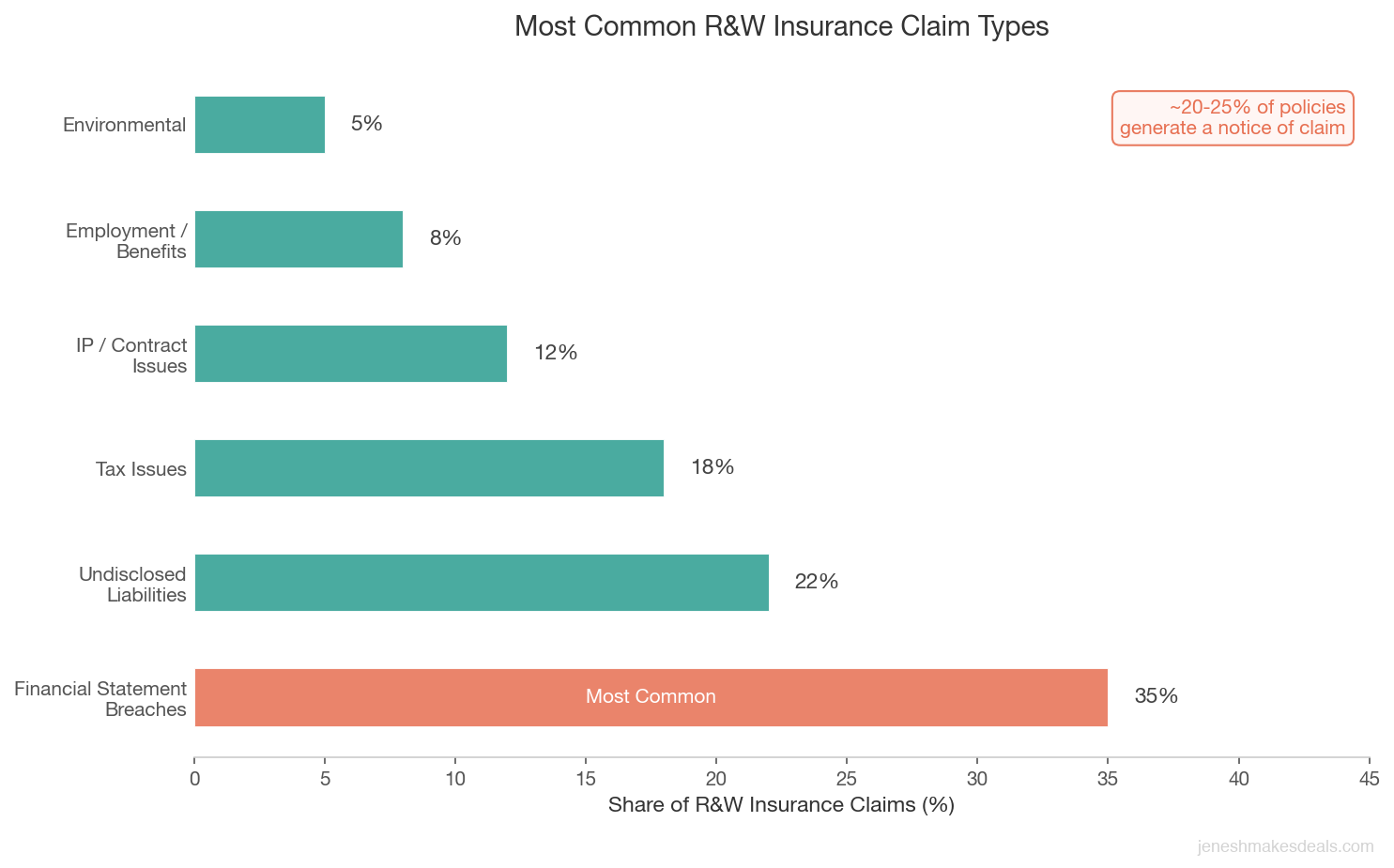

Real World R&W Insurance Claims: What Actually Goes Wrong

To make this concrete, here are the types of breaches that actually generate R&W insurance claims, drawn from published insurer data and industry case studies.

Financial statement breaches are the most common category. A manufacturing company sold for $30 million. After closing, the buyer discovered that $800,000 in inventory had been overvalued in the financial statements. The seller hadn't disclosed a slow-moving stock issue that required a write-down. The R&W insurer paid out after the retention.

Undisclosed liabilities. A professional services firm was sold for $18 million. Six months after closing, a former employee filed a wrongful termination lawsuit alleging events that predated the sale. The seller hadn't disclosed the situation. The R&W policy covered the defense costs and eventual settlement.

Tax issues. A $45 million distribution company had misclassified workers as independent contractors for several years before the sale. The IRS audit surfaced 14 months after closing. The resulting payroll tax liability and penalties exceeded $1.2 million. The R&W policy paid above the retention amount.

Intellectual property issues. A software company sold for $22 million had been using open source code in a way that violated the license terms. The buyer discovered this post-close and received a demand from the open source licensor. The IP rep in the purchase agreement covered this situation, and the R&W insurer paid the claim.

According to AIG and other major R&W insurers, claim rates have increased significantly over the last decade. Roughly 20% to 25% of policies now generate at least a notice of claim, and about 15% of policies result in actual payouts. That's much higher than most people expect.

About 20% to 25% of R&W insurance policies generate at least a notice of claim, and roughly 15% result in actual payouts. Financial statement breaches are the single most common claim category, making thorough financial due diligence critical even when insurance is in place.

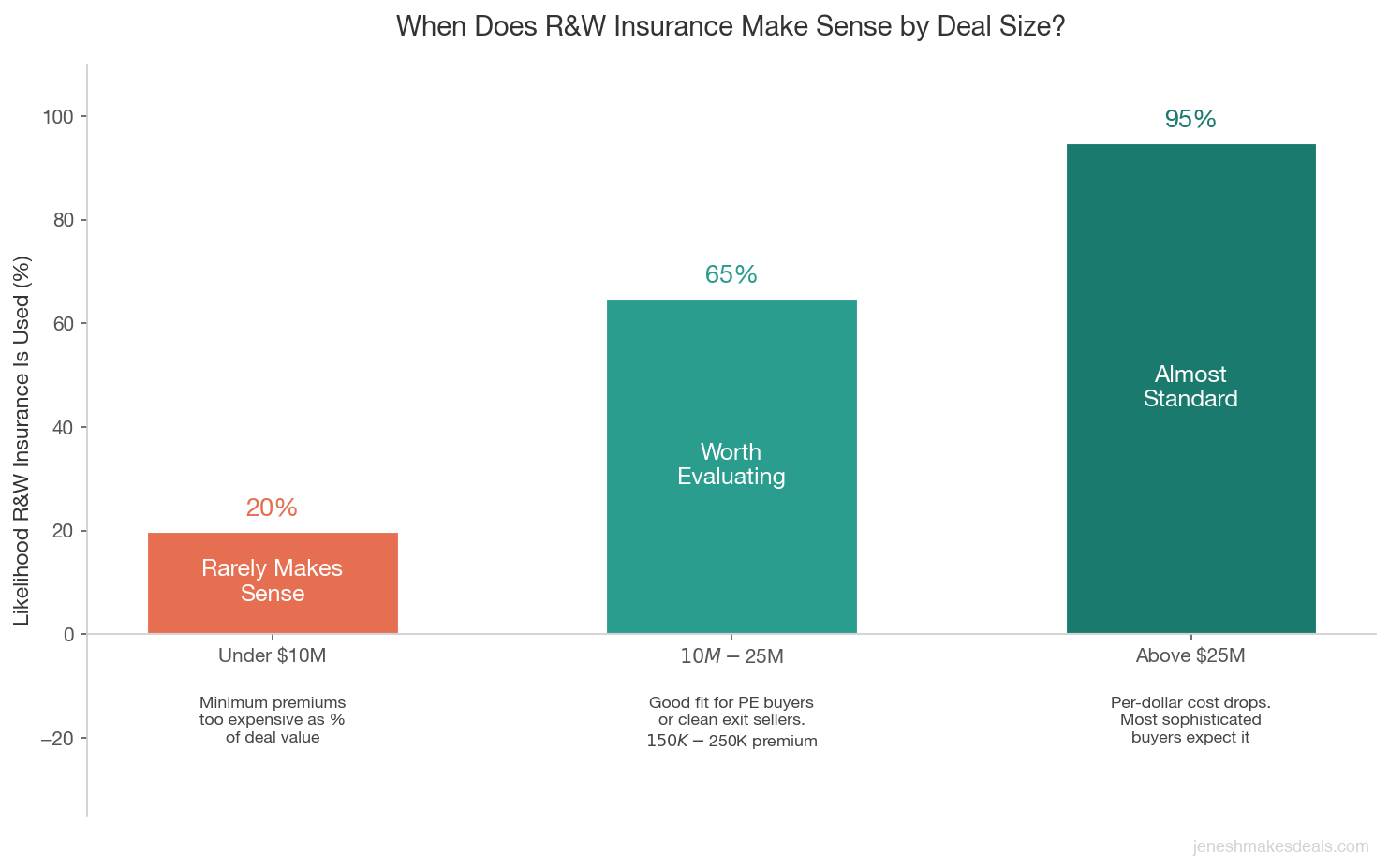

Should Small Business Sellers Consider R&W Insurance?

This is where I give you the honest answer: probably not, but it depends.

For deals under $10 million, the economics rarely work. The minimum premiums ($100,000 or more when you factor in underwriting fees) represent too large a percentage of the deal value. You're better off negotiating a smaller escrow and investing in thorough due diligence and well-drafted rep schedules.

For deals in the $10 million to $25 million range, R&W insurance is worth evaluating, especially if the seller wants a clean exit or if the buyer is a PE firm that expects it. The premium might run $150,000 to $250,000, which is a real number but manageable in the context of the overall deal.

For deals above $25 million, R&W insurance is almost standard. The per-dollar cost of coverage drops, the protection is meaningful, and most sophisticated buyers expect it as part of a professionally run sale process.

The other factor is the nature of the business. A service business with simple financials, minimal IP, no environmental issues, and a clean employment record is a much easier underwriting proposition than a manufacturing company with complex inventory, multiple locations, and dozens of employees. The easier the underwriting, the lower the premium and the fewer exclusions.

| Factor | Easier to Insure | Harder to Insure |

|---|---|---|

| Industry | Professional services, SaaS | Manufacturing, construction |

| Financials | Clean audited statements | Complex, multi-entity |

| Employees | Small team, W-2 only | Many employees, 1099 mix |

| Environmental | Office based, no exposure | Industrial sites, hazmat |

| IP | Minimal or clearly owned | Licensed, open source dependent |

| Deal timeline | 4+ weeks to close | Rushed closing under 2 weeks |

For deals above $25 million, R&W insurance is almost standard practice. The per dollar cost of coverage drops, the protection is meaningful, and most sophisticated buyers expect it as part of a professionally run sale process.

If you're thinking about selling your business in the next 12 to 24 months and want to understand how deal structure, including R&W insurance, affects your net proceeds, reach out and let's talk through your specific situation. I work with sellers across a wide range of industries and deal sizes, and I can help you figure out whether R&W insurance makes sense for your exit.

How to Get R&W Insurance for Your Deal

If you've decided R&W insurance makes sense, here's the practical path forward.

Hire a specialist broker. This is not something to run through your regular commercial insurance agent. You need a broker who specializes in M&A insurance and has relationships with multiple R&W insurers. Names like Lockton, Marsh, Willis Towers Watson, and Alliant have dedicated M&A practices. There are also boutique brokers that specialize in middle market deals.

Start early. Engage the insurance broker when you're about 60% through due diligence. That gives enough time for underwriting without rushing. If you wait until a week before closing, you'll either pay a rush premium or push the close date.

Be transparent in the application. The worst outcome is getting coverage denied at close because you withheld information during underwriting. Full disclosure is in your interest.

Read the exclusions carefully. Before binding coverage, have your attorney review the policy's exclusion schedule. Make sure you understand exactly what's not covered before you rely on the policy.

Pair it with good diligence. R&W insurance is not a reason to do less due diligence. It's a reason to do thorough diligence and still have a backstop. The diligence protects both parties; the insurance covers what diligence misses.

For a full picture of how your deal financing and structure affects your returns, use the deal financing tools here to model different scenarios before you get to the closing table.

The Bottom Line

Representations and warranties insurance has moved from a niche product used only on billion dollar deals to a mainstream tool in middle market M&A. If you're buying or selling a business worth $10 million or more, it's worth understanding how it works and whether it fits your deal.

For sellers, it means walking away from closing with more cash in hand and less exposure to post-closing claims. For buyers, it means getting paid by an insurance company instead of chasing a former owner. For deals with multiple bidders, it can be the factor that makes one offer stand out from another.

It's not cheap, it doesn't cover everything, and it's not right for every transaction. But for the right deal, it's one of the most useful tools in a well-structured M&A transaction.

If you're thinking about selling your business and want a broker who understands deal structure, not just deal price, let's connect. I'll help you understand what a well-structured exit actually looks like for a business like yours.

Ready to start the conversation? Tell us about your business and we'll take it from there.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

April 25, 2026

The Role of an Escrow Agent in a Business Transaction

Escrow agents protect both buyer and seller during closing. Learn what they do, what they cost, and how to choose one.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.