I've seen deals fall apart over inventory more times than I can count. A buyer and seller agree on a $1.2 million purchase price, shake hands, and then a physical inventory count reveals $340,000 in obsolete merchandise that nobody wants. Suddenly everyone's angry, the deal gets repriced, and half the time it collapses entirely.

Inventory is one of the most misunderstood parts of a business sale. Sellers tend to overvalue it because they paid full price for it. Buyers discount it heavily because they're taking on the risk of selling it. The gap between those two positions creates real friction, and if you don't have a clear process in place before you go to market, you're setting yourself up for a painful closing.

Here's what you need to know, whether you're the one selling or the one buying.

Why Inventory Matters More Than Most Sellers Expect

When you're selling a business, inventory is working capital that transfers hands. Unlike equipment, which depreciates predictably, or goodwill, which is somewhat abstract, inventory is a concrete asset sitting on shelves or in a warehouse. Its value can swing dramatically based on condition, age, demand, and how it's counted.

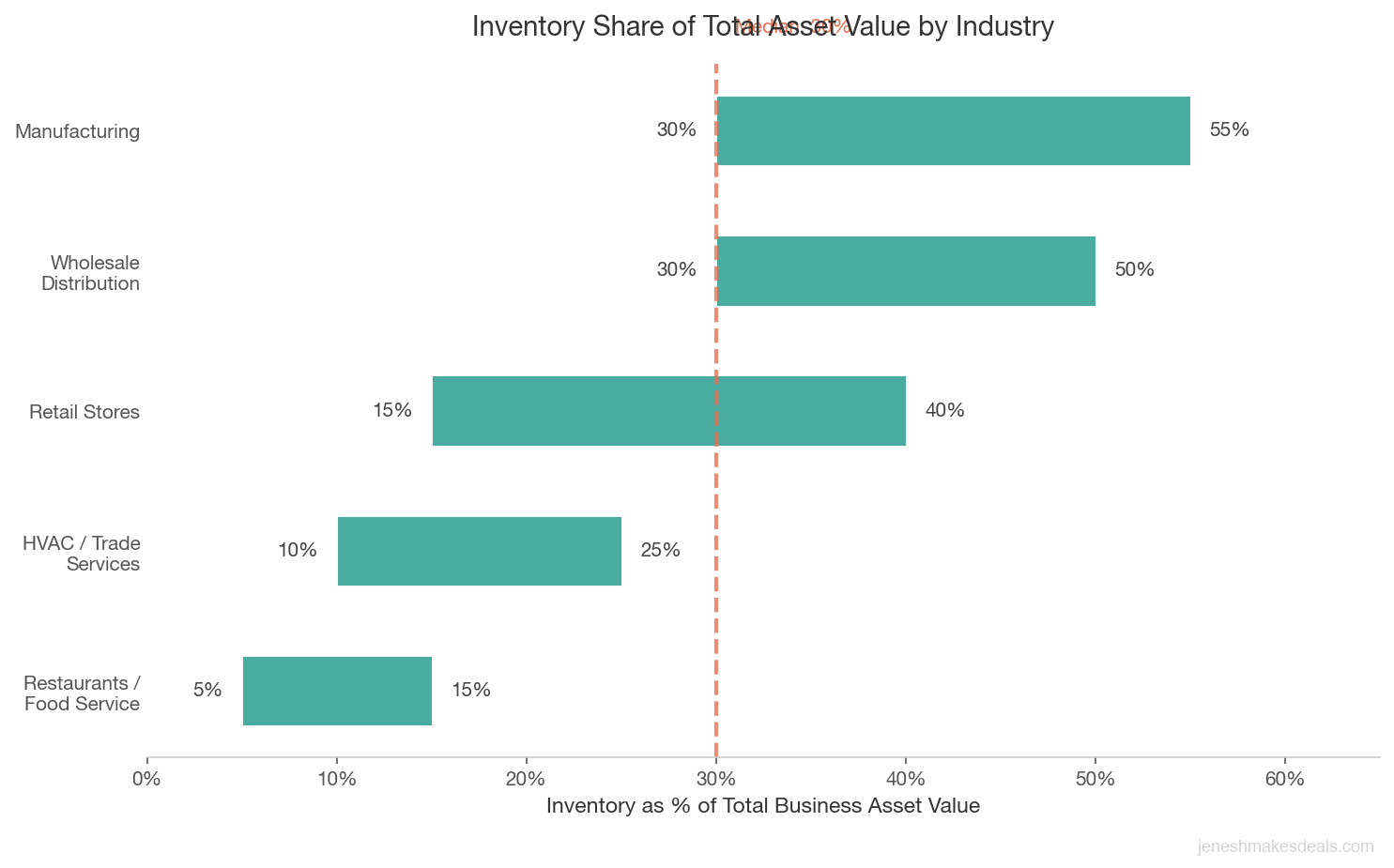

For most retail businesses, inventory represents 15 to 40 percent of total asset value. For manufacturing companies, that number can climb above 50 percent. That means the way inventory is handled in the purchase agreement can shift the final purchase price by hundreds of thousands of dollars.

Buyers care about inventory for a different reason than sellers. They're asking: "Can I actually sell this stuff, and at what margin?" A buyer inheriting $200,000 in slow moving inventory that takes two years to turn isn't the same as inheriting $200,000 in fast moving product that clears in 60 days. The dollar amount looks the same on paper, but the cash flow implications are completely different.

Broker insight: I tell every seller the same thing: the value of your inventory is not what you paid for it. It's what someone else would pay to take it off your hands today. The sooner you accept that distinction, the smoother your closing will go.

The Three Types of Inventory and Why They're Valued Differently

Not all inventory is created equal. When you're preparing for a sale, you need to categorize what you have, because buyers and their accountants will absolutely be asking these questions.

Raw materials are inputs you've purchased but haven't yet used in production. A cabinet maker's unfinished lumber, a bakery's flour and sugar, a clothing manufacturer's uncut fabric. These are generally valued at cost and are the easiest to price objectively. Raw materials typically hold their value well unless they're highly perishable or commodity prices have shifted significantly since purchase.

Work in progress (WIP) is partially completed inventory. This is the trickiest category to value because you've incurred labor costs and overhead, but the product isn't finished or sellable yet. A custom furniture shop with three half built dining sets has WIP on its hands. The valuation usually involves cost of materials plus a portion of labor, minus a discount for the fact that a new owner has to complete the work. In practice, buyers often push hard to exclude WIP or value it at a heavy discount, sometimes 40 to 60 percent below full cost.

Finished goods are products that are ready to sell. This is the most straightforward category from a buyer's perspective, but valuation still depends on demand, age, and condition. Finished goods that are current, moving, and margin positive are valued close to cost or sometimes at replacement cost if demand is strong. Products that are sitting because nobody wants them are worth a fraction of that.

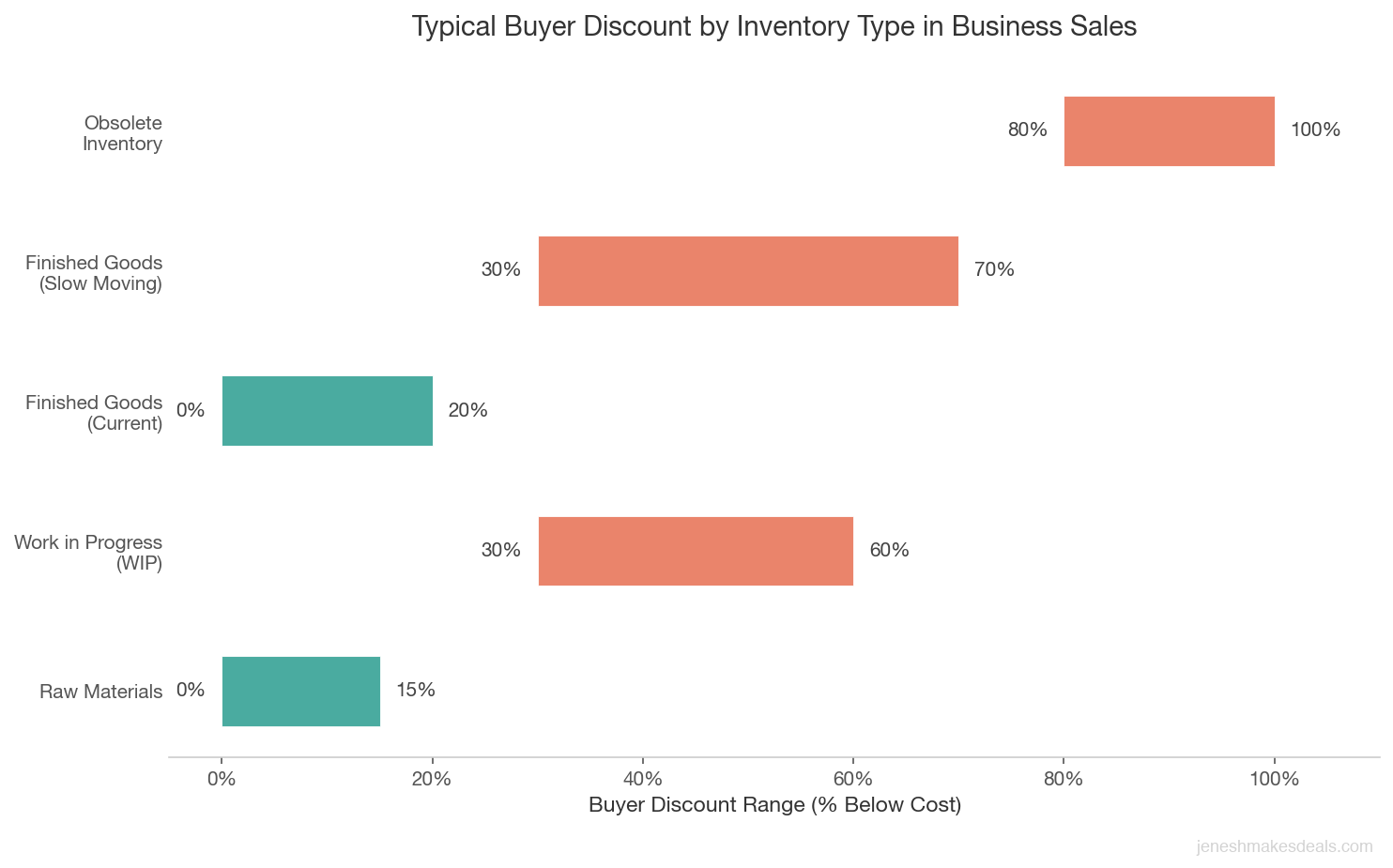

Here's a simple breakdown of how these categories typically get treated in a deal:

| Inventory Type | Typical Valuation Approach | Buyer Discount Range |

|---|---|---|

| Raw materials | Cost (purchase price) | 0-15% |

| Work in progress | Cost + partial labor | 30-60% discount |

| Finished goods (current) | Cost or lower of cost/market | 0-20% |

| Finished goods (slow moving) | Market value or liquidation | 30-70% discount |

| Obsolete inventory | Scrap value or zero | 80-100% discount |

How Inventory Gets Valued: Three Methods You Need to Know

The valuation method used for inventory affects the final number significantly. There are three methods that come up most often in business sales.

Cost method is the most common. You value inventory at what you paid for it, using either FIFO (first in, first out) or LIFO (last in, first out) accounting. Most small businesses use FIFO, which means older inventory is considered sold first. This matters because if your supplier raised prices, your current inventory may be "worth" more on paper using FIFO than what you actually paid for the most recent units.

Lower of cost or market (LCM) is what most accountants recommend for business sales. You compare what you paid for the inventory versus what you could realistically sell it for today, and you use whichever number is lower. This is a conservative approach that tends to favor buyers, but it's hard to argue with as a standard. If you bought widgets at $8 each but they're now selling on Amazon for $6, LCM says your inventory is worth $6 per unit, not $8.

Retail method is used primarily by retail businesses that carry hundreds or thousands of SKUs. Instead of tracking cost per item, you apply your historical cost to retail ratio (say, 55 percent) to the retail value of your total inventory to estimate cost. It's faster than a line item count but less precise. Buyers with serious diligence teams will usually want to validate a retail method estimate with spot checks on actual cost data.

If you're a seller, your choice of accounting method matters. Make sure your bookkeeper can clearly explain which method your financial statements use, because buyers will ask.

The Inventory Count Process Before Closing

Here's where deals either get smoother or get messy. A physical inventory count is almost always required as a condition of closing, typically within 5 to 10 days before the actual closing date. This count determines the final purchase price adjustment.

The standard process works like this. Both the buyer and seller do a joint physical count of all inventory on hand. Each party brings their own people if the inventory is significant. You count everything, record it on a standardized sheet, and then apply the agreed upon valuation method to get a dollar amount. If the count comes in at the number used in the purchase agreement, no adjustment is made. If it's higher, the buyer pays more. If it's lower, the buyer pays less.

That sounds simple, but in practice it gets complicated fast. I worked on a deal for a janitorial supply distributor where the inventory count took two full days and uncovered $87,000 in products that hadn't been entered into the inventory management system. The seller was certain those products were in their books. The buyer's team found them sitting in a back warehouse. Nobody was lying, the record keeping was just sloppy. That led to a three week delay and almost killed the deal.

To prevent that kind of mess, here's what I tell sellers to do before listing:

- Conduct your own internal count at least 90 days before you expect to close

- Reconcile your physical count to your accounting system

- Identify and tag obsolete or damaged items separately

- Make sure all inventory is recorded in your system, including consignment, samples, and display items

- Get your vendor statements current so there's no confusion about what's been paid for

Buyers should insist on language in the purchase agreement that specifies the counting methodology, who pays for the count if a third party counter is hired, and what happens if there's a discrepancy between the two parties' counts (usually a third party arbitration clause).

Dealing With Obsolete and Slow Moving Inventory

This is where most of the negotiation heat comes from. The seller says the inventory is worth $180,000. The buyer says half of it is dead stock and won't offer more than $90,000. Both parties dig in, and a deal that should close in 60 days drags to 120 days.

The honest reality is that every business has some obsolete or slow moving inventory. The question is how much, and who bears the cost of that.

I define slow moving inventory as anything that hasn't turned in the last 12 months. Obsolete inventory is anything that can no longer be sold at a meaningful margin, whether because it's been discontinued, superseded by a newer product, or simply unsaleable in the current market. For a deal to close cleanly, both of these categories need to be addressed explicitly in the purchase agreement.

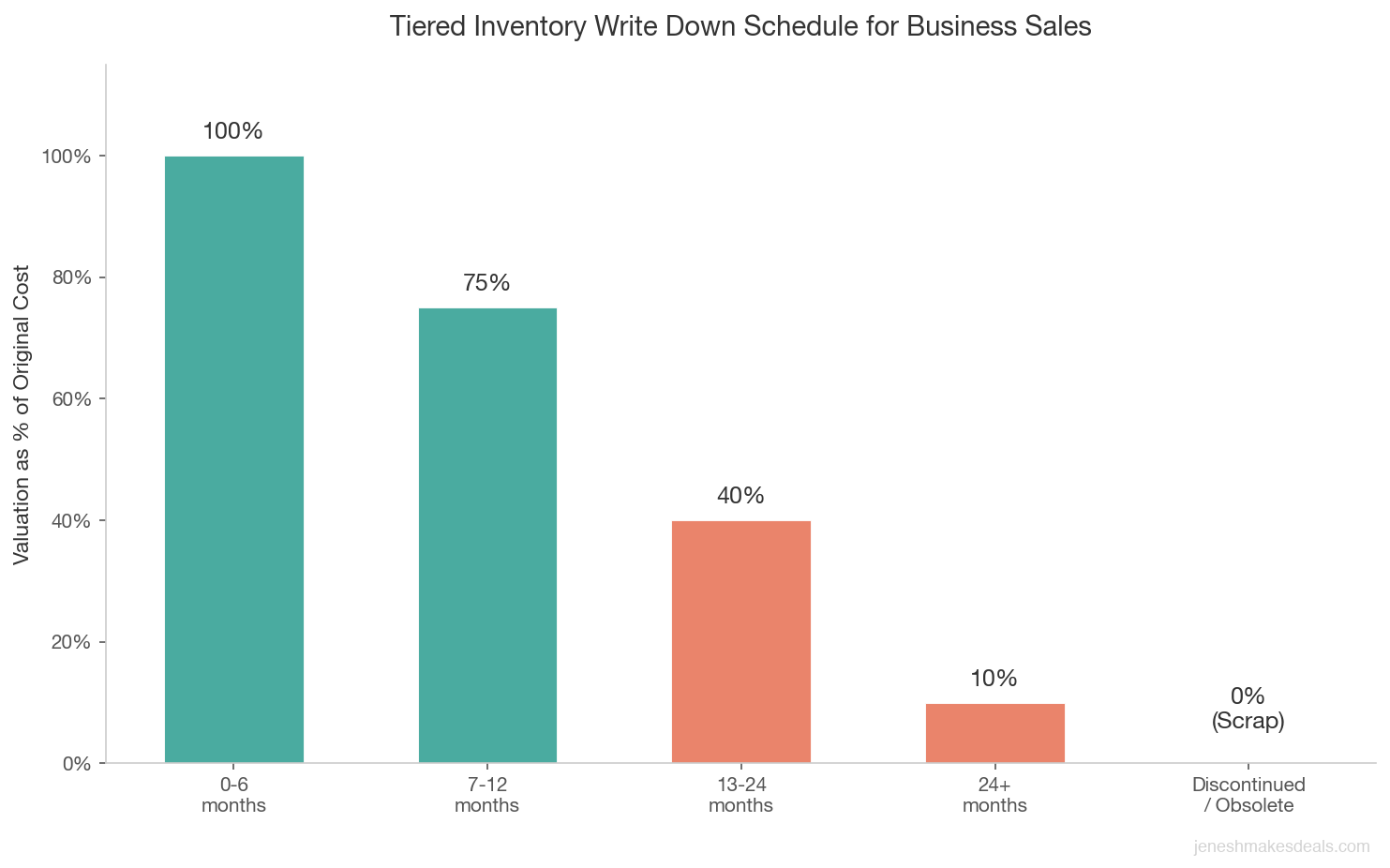

The most common approach is a tiered write down schedule. Here's an example of what I've seen work in practice:

| Inventory Age (No Movement) | Valuation as % of Cost |

|---|---|

| 0-6 months | 100% |

| 7-12 months | 75% |

| 13-24 months | 40% |

| 24+ months | 10% |

| Discontinued / obsolete | 0% |

Some sellers push back on this because they believe their slow moving inventory will eventually sell. That may be true, but the buyer is taking on the carrying cost, the storage cost, and the risk of further price erosion while that inventory sits. The discount is appropriate.

One solution I've negotiated is a "take back" clause for obsolete inventory. The seller removes the obsolete stock before closing and takes it themselves. They can liquidate it, donate it, or scrap it. The buyer gets a cleaner inventory base at a fair value, and the seller gets to extract whatever remaining value they can on their own. This approach has saved more than a few deals in my experience.

Key takeaway: Never let a $30,000 inventory dispute kill a $1 million deal. A take back clause or tiered write down schedule solves 90% of the arguments I see between buyers and sellers over obsolete stock. Get creative with the structure before you get stubborn on the number.

How Inventory Affects the Purchase Price Structure

There are two main ways inventory gets handled in a purchase agreement: included in the purchase price, or priced separately as an add on.

Included in the purchase price is the simpler approach, usually used for smaller deals under $500,000 where inventory is relatively modest. You say the business sells for $650,000 and that includes inventory up to $80,000. If the count comes in above $80,000, the buyer pays extra for the overage. If it comes in below, the price adjusts down. This is sometimes called an "inventory collar" with a floor and a ceiling.

Priced separately (inventory at cost) is more common for larger businesses. The purchase price covers the goodwill, equipment, and intangibles. Inventory is then priced at cost, counted at closing, and added on top. So a buyer might agree to pay $900,000 for the business plus inventory at cost. If the final count values inventory at $210,000, the total closing payment is $1,110,000. This approach is cleaner for accounting purposes and reduces disputes about what's included.

If you're a seller, I strongly recommend knowing your average monthly inventory value over the trailing 12 months before you list. If your inventory naturally fluctuates (seasonal business, for example), you want the purchase agreement to reflect a normalized level, not whatever happens to be on the shelves the week you close.

If you're a buyer, pay attention to what "at cost" actually means. Ask the seller to provide invoices or cost records for a sample of high value SKUs to validate that the cost figures in their system are accurate.

Negotiation Strategies Around Inventory

Inventory negotiation isn't just about the dollar value. There are structure and process elements that can make both parties feel better about the outcome.

Set the methodology in advance. Before you're under contract, agree on how inventory will be valued. If you're a seller and you've been using cost method for 10 years, you don't want a buyer to suddenly propose lower of cost or market three days before closing. Put the valuation methodology in the letter of intent, not just the purchase agreement.

Use a third party counter for large inventories. If you're dealing with more than $200,000 in inventory, it's worth spending $3,000 to $8,000 on a professional inventory counting firm. They reduce disputes because neither party controls the count. The cost is usually split 50/50.

Build in a trailing average adjustment. For businesses with seasonal inventory swings, I recommend using a 12 month average inventory value as the baseline, then adjusting up or down from the closing count. This prevents a seller from loading up on inventory in the 30 days before closing to inflate the payout.

Negotiate a holdback for disputed items. If there's a disagreement about $30,000 worth of items, don't let that kill the deal. Put those items in escrow at a negotiated value, with a 90 day period for the buyer to attempt to sell them. If they sell, the seller gets the proceeds up to cost. If they don't, the buyer keeps the escrow. This splits the risk fairly.

Warning: The biggest mistake I see sellers make is waiting until they're under LOI to think about inventory methodology. By then, the buyer has already formed their own assumptions. Lock in the valuation method and counting process in the letter of intent, not the purchase agreement. If you leave it for later, you're handing the buyer negotiating power they didn't earn.

You can use the business valuation calculator to model how different inventory values affect total deal price and ROI for buyers.

Common Inventory Disputes and How to Prevent Them

After hundreds of transactions, I've seen the same disputes come up over and over. Here are the five most common and what you can do to prevent each one.

"The books say $250K but the count shows $190K." This gap between book inventory and physical count is usually a record keeping problem, not fraud. Shrinkage, unreturned customer merchandise, damaged items that weren't written off, samples given away. The fix is for sellers to reconcile book to physical at least once a quarter, not just at tax time.

"Half this inventory is junk." The buyer discovers items that are years old, discontinued, or damaged. The seller insists it's all sellable. The solution is to agree on an aging schedule in the purchase agreement before this conversation happens.

"You loaded up inventory before closing." A seller, knowing inventory will be priced at cost and included in the sale, buys an extra $80,000 of product in the 60 days before closing. The buyer ends up paying for inventory they wouldn't have ordered themselves. The fix is a covenant in the purchase agreement that inventory purchases during the closing period must stay within 110 percent of the prior year monthly average.

"This inventory is consigned, not ours." Sometimes a business holds product on consignment that technically belongs to a vendor. If that gets counted as owned inventory, the buyer is overpaying. Sellers need to clearly separate and label any consignment stock before the count.

"The price tags say retail, not cost." In a retail business, if inventory records are kept at retail price and the buyer's team is counting at retail, you'll get a very different number than if you're counting at cost. Both parties need to agree before the count starts: what number are we using?

If you want help structuring the inventory terms in your deal, reach out to me directly. This is exactly the kind of thing where getting the language right in the LOI saves weeks of pain later.

Industry Specific Inventory Considerations

Inventory issues look different depending on what kind of business you're selling or buying. Here's what I watch for in the industries I work in most.

Retail businesses have the most complex inventory situations because they carry large numbers of SKUs. A gift shop or boutique clothing store might have 2,000 to 10,000 distinct items. Physical counting takes time and accuracy matters. Retail buyers almost always want a current aging report sorted by last sale date before they'll agree on a value. Seasonal businesses (Christmas decorations, pool supplies) need to address the timing of the count relative to the season, because a pool supply store's inventory in November looks very different than it does in April.

Manufacturing businesses face the WIP challenge I described earlier. The added complexity is that WIP value depends on your cost accounting system, and many small manufacturers don't have clean job costing data. If you're selling a manufacturing company, get your cost accountant to prepare a clear WIP schedule showing material costs, labor costs, and overhead allocation per job. Buyers who can't understand how you got to your WIP number will discount it heavily.

Food service and restaurant businesses are a special case because most of their inventory is perishable. A restaurant sale typically includes only the shelf stable inventory (canned goods, dry goods, non food supplies). Perishable food inventory is often excluded from the sale entirely or priced at a very nominal amount ($1,000 to $5,000 as a standard line item). Nobody wants to pay $18,000 for produce that has a 5 day shelf life.

Wholesale and distribution businesses often have the highest absolute inventory values. A wholesale distributor might carry $500,000 to $2 million in inventory. At that scale, how inventory is priced and counted can be the single largest variable in the deal. These businesses often have complex inventory management systems, and buyers should plan 2 to 3 days for the count, not 2 to 3 hours.

HVAC, plumbing, and trade service businesses have a mix of shop inventory and truck stock. Truck stock is often the messiest to count because it's spread across 5 to 10 vehicles, constantly being used, and inconsistently tracked. I always recommend a separate truck stock count the night before closing, with both parties present.

How Sellers Should Prepare Inventory Before Listing

If you're thinking about selling in the next 12 to 24 months, here's a practical action plan to get your inventory in shape before you go to market. The cleaner your inventory, the stronger your negotiating position.

Do a full physical count now. Don't wait until you're under letter of intent to discover that your books and your shelves don't match. A clean, documented physical count from the last 6 months signals to buyers that you run a tight operation.

Write off obsolete inventory before listing. This is counterintuitive for some sellers. You think writing off $40,000 in dead stock makes your business look worse. In reality, it makes your balance sheet more credible. Sophisticated buyers will find that inventory and discount it anyway. By writing it off, you're removing a future dispute.

Organize your inventory by category and age. If you can hand a buyer a report showing inventory broken down by product line, age, and turnover rate, you've done their due diligence work for them. That's a signal of operational maturity, and it gives buyers confidence.

Avoid large inventory purchases in the 90 days before listing. Unless it's your normal seasonal buying pattern, don't stock up right before you sell. It looks suspicious and creates a higher inventory number that a buyer will want to discount.

Get supplier relationships documented. Buyers want to know they can maintain supply after the sale. A list of your top 10 suppliers with contact names, credit terms, and average monthly spend is a simple thing to prepare and a genuinely useful piece of due diligence that speeds up closing.

If you want a free valuation to understand what your business is worth, including a realistic inventory adjustment, use the valuation calculator or get in touch and I can walk you through it.

What Happens to Inventory After Closing

Once the deal closes, inventory becomes the buyer's responsibility. But there are a few situations where the transition creates post closing issues.

Returns from customers are the most common. A retail customer returns a $300 item two weeks after closing. Who owns that refund? The standard approach is to specify in the purchase agreement that customer returns submitted before closing are the seller's liability, returns after closing are the buyer's. For high volume retailers, some deals include a short holdback (usually 30 to 60 days) funded from the seller's proceeds to cover returns.

Vendor credits and RMAs (return merchandise authorizations) already in process at closing also need to be addressed. If the seller has $8,000 in credits sitting with a vendor that haven't been applied yet, those credits should either be transferred to the buyer or settled before closing.

Warranty obligations tied to specific inventory items are another issue for manufacturing and equipment businesses. If your company sold a product with a 2 year warranty and that warranty outlasts the closing date, the buyer needs to understand what potential liability they're assuming.

For more complex situations like these, contact me and we can talk through how to structure the deal terms to protect both sides.

The Bottom Line on Inventory

Inventory is one of those deal elements that feels like it should be simple but almost never is. The sellers who get the best outcomes are the ones who treat inventory preparation like they'd treat preparing their financial statements: clean, documented, and defensible.

The buyers who get the best outcomes are the ones who build inventory diligence into their process from day one, not as an afterthought three weeks before closing.

Whether you're a seller who wants to maximize what you get for your inventory, or a buyer who wants to make sure you're not inheriting a warehouse full of problems, the same principle applies: get specific, get documented, and don't leave inventory terms to a handshake.

If you're in the middle of a deal and inventory is becoming a sticking point, or if you're preparing to sell and want to know how to position your inventory before you list, reach out. I've worked through enough of these situations to help you find a structure that works.

Ready to get the process started? Tell us about your business and we'll help you figure out where inventory fits in your deal.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 25, 2026

The Role of an Escrow Agent in a Business Transaction

Escrow agents protect both buyer and seller during closing. Learn what they do, what they cost, and how to choose one.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.