Every business sale reaches a point where both sides are nervous. The seller doesn't want to hand over financial records and trade secrets without knowing the buyer has real money. The buyer doesn't want to wire $400,000 without confirming the business is actually what the seller says it is. That's why escrow agents exist.

The escrow agent is the neutral party who sits between buyer and seller, holds the money, manages the documents, and makes sure nobody gets burned. I've worked on transactions where a good escrow agent saved a deal that was about to collapse, and I've worked on deals where a bad one nearly derailed a straightforward closing. The agent you choose matters more than most people realize.

Here's everything you need to know about the role of an escrow agent in a business transaction, from the moment escrow opens to the day funds are released.

What an Escrow Agent Actually Does

An escrow agent is a neutral third party who holds money, documents, and assets on behalf of the buyer and seller until all conditions of the purchase agreement are met. They don't represent either side. They work for the deal itself.

Here's what an escrow agent does during a typical business sale:

- Holds the buyer's earnest money deposit in a regulated trust account until closing conditions are met

- Collects and organizes all closing documents, including the purchase agreement, bill of sale, non compete agreements, and lease assignments

- Coordinates with lenders to make sure SBA or conventional funding requirements are satisfied

- Runs the UCC lien search to confirm no existing liens on the business assets

- Files bulk sale notices in states that require them, protecting the buyer from inheriting the seller's unpaid debts

- Manages expense prorations for rent, utilities, and prepaid costs based on the closing date

- Disburses funds at closing, paying the seller, clearing liens, distributing broker commissions, and sending remaining balances to the right parties

- Issues closing statements so both sides have a detailed accounting of every dollar

Think of the escrow agent as the air traffic controller of the deal. They don't fly the plane, but nothing lands safely without them.

When Escrow Opens and Where It Fits in the Deal

Escrow doesn't start when you first list the business. It opens after the buyer and seller sign a letter of intent and the buyer submits their earnest money deposit. That deposit going into the escrow account is what officially opens escrow.

Here's where escrow fits in the overall transaction timeline:

- Buyer finds the business and does preliminary research

- Buyer submits an LOI with proposed terms

- Seller accepts the LOI (or they negotiate and then sign)

- Buyer submits earnest money deposit to escrow. Escrow is now open.

- Due diligence period begins (buyer verifies everything)

- Buyer secures financing

- All contingencies are removed

- Closing documents are signed

- Funds are disbursed. Escrow is now closed.

The entire escrow period typically lasts 30 to 90 days. Cash deals close faster, usually in 30 to 45 days. SBA financed deals take longer because the lender has its own checklist, and escrow can't close until the lender gives final approval.

For a detailed walkthrough of what happens at each stage, I wrote a separate guide on the full escrow process in a business sale.

How Escrow Protects the Buyer

Buyers are taking on the bigger risk in most transactions. They're about to spend a large sum of money on a business they've only seen from the outside. Escrow provides several specific protections.

Your deposit is safe. Without escrow, you'd be handing your $30,000 or $50,000 deposit directly to the seller. If the deal falls apart because the seller misrepresented revenue, good luck getting that money back. With escrow, the agent holds your deposit in a regulated trust account. If the deal falls through for a valid reason covered by your contingencies, the agent returns your deposit.

You get time to verify everything. The escrow period is when due diligence happens. You're reviewing financial statements, tax returns, customer contracts, equipment condition, and lease terms. If you find something that doesn't match what the seller told you, you have the right to renegotiate or walk away. Escrow gives you this structured window.

Liens get cleared before you pay. The escrow agent runs a UCC search and identifies any existing liens on the business assets. If there's a $75,000 equipment loan outstanding, the escrow agent makes sure that loan gets paid off at closing from the seller's proceeds. You don't inherit someone else's debt.

Bulk sale protection. In many states, the escrow agent publishes a bulk sale notice that gives the seller's creditors a window (usually 12 business days in California) to file claims. This means any hidden debts surface before you close, not after.

I tell every buyer the same thing: escrow is not a cost, it's insurance. I've seen buyers try to skip formal escrow on smaller deals to save a few thousand dollars. In almost every case, they ended up spending more in legal fees sorting out problems that a proper escrow process would have caught upfront.

Want help structuring a deal that protects your interests? Talk to a broker who's been through this.

How Escrow Protects the Seller

Sellers sometimes feel like escrow is all about protecting the buyer. That's not true. Escrow protects you in several important ways.

The buyer's deposit is real. When a buyer says they're serious, escrow proves it. That $25,000 or $50,000 sitting in escrow tells you the buyer has skin in the game. If they walk away without a valid reason after contingencies are removed, you may be entitled to keep that deposit as liquidated damages.

You don't transfer anything until the money is confirmed. Without escrow, you'd have to trust that the buyer's wire transfer actually went through before handing over your customer list, equipment, and business name. The escrow agent verifies that funds are in the account before closing documents are executed and assets are transferred.

Confidentiality stays intact during due diligence. Because the deal is structured through escrow with clear contingencies and timelines, you're not just handing over sensitive financial information to someone who may or may not be serious. The formal escrow process creates accountability.

You have a clear record of the transaction. The escrow agent's closing statement documents everything. Every dollar in, every dollar out. This is invaluable for your tax filing and for resolving any disputes that come up after closing.

Escrow Agents vs. Title Companies vs. Closing Attorneys

People use these terms interchangeably, but they're not the same thing. Which one you use depends on the type of transaction and which state you're in.

Escrow agents and escrow companies specialize in holding funds and managing the closing process. In business sales, you want an escrow company that handles business transactions specifically. They understand bulk sale laws, UCC searches, and the unique requirements of transferring a going concern.

Title companies are standard in real estate transactions. If your business sale includes commercial real estate, you'll likely use a title company for the property portion and a separate escrow agent for the business portion. Make sure any title company you use has business sale experience.

Closing attorneys handle escrow functions in certain states. In the Northeast (New York, Massachusetts, Connecticut), it's common for an attorney to manage the escrow account and conduct the closing. The advantage is that your legal counsel also manages logistics. The disadvantage is that attorneys charge more per hour than escrow companies.

In practice, here's how it usually works:

- West Coast (especially California): Specialized business escrow company

- East Coast and Southeast: Attorney managed closing with escrow held in attorney trust account

- Midwest and Mountain states: Varies. Could be an escrow company, a title company, or an attorney depending on local custom

- SBA deals anywhere: The lender often dictates who handles escrow

Your broker or attorney can recommend the right option for your state and deal structure.

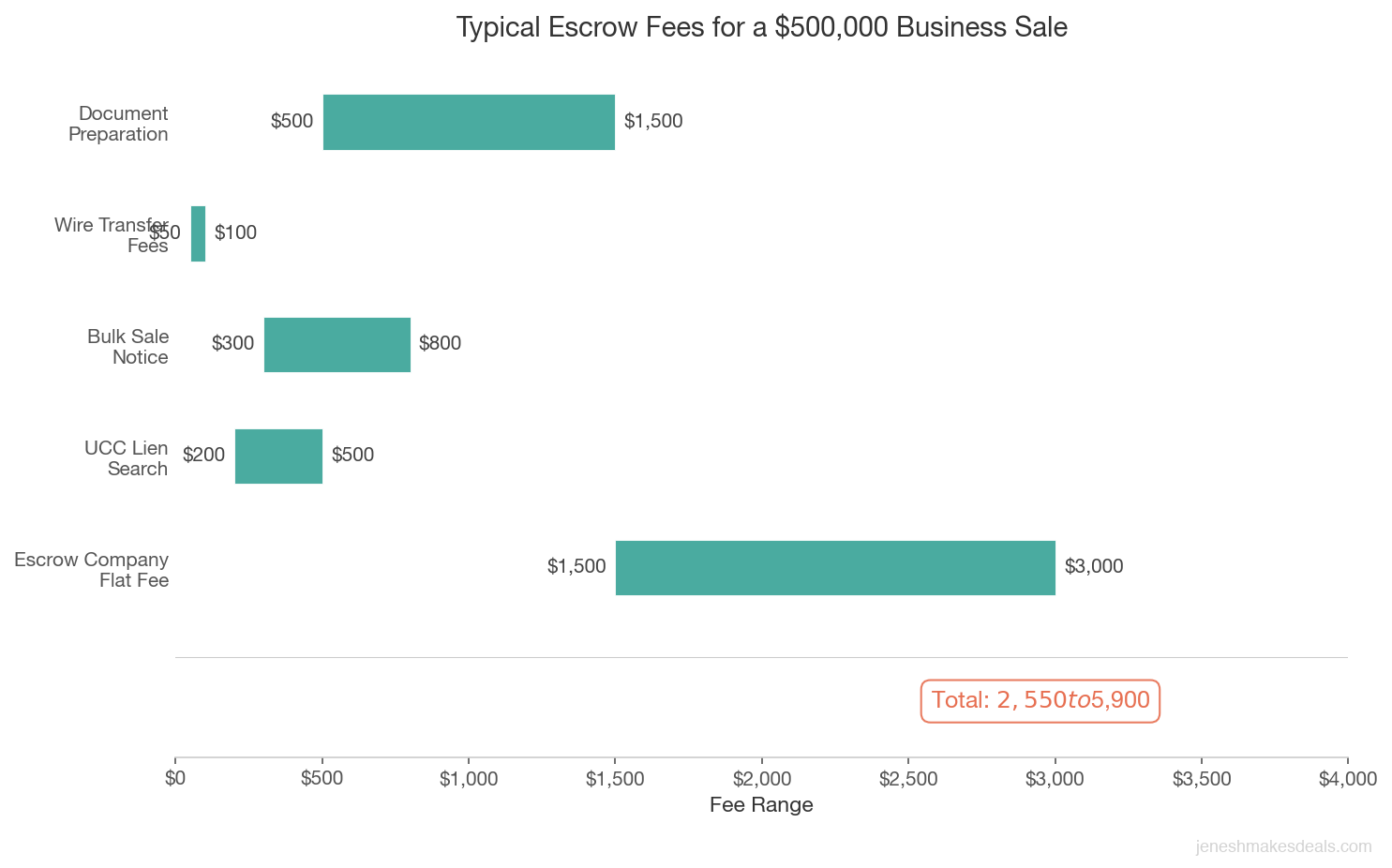

Typical Escrow Fees and Who Pays Them

Escrow isn't free. Someone has to pay the escrow agent for their time, their trust account management, and all the document handling they do. Here's what it typically costs.

Flat fee escrow. For transactions under $500,000, many escrow companies charge $1,000 to $3,000 flat. This covers opening the account, managing documents, handling the closing, and issuing closing statements.

Percentage based escrow. For larger transactions, fees are often 1% to 2% of the sale price. On a $1.2 million deal, you might pay $12,000 to $15,000 in escrow fees.

Attorney escrow. When an attorney manages escrow, you're paying their hourly rate ($250 to $500 per hour) plus a flat fee for account management. Total costs usually run $3,000 to $7,000.

Who pays? It varies by region. In California, buyer and seller typically split 50/50. In other states, the buyer often pays. There's no universal rule. It depends on what you negotiate in the purchase agreement.

Here's a rough breakdown for a $500,000 business sale:

| Fee Type | Typical Range |

|---|---|

| Escrow company flat fee | $1,500 to $3,000 |

| UCC lien search | $200 to $500 |

| Bulk sale notice (if required) | $300 to $800 |

| Wire transfer fees | $25 to $50 per wire |

| Document preparation | $500 to $1,500 |

| Total escrow costs | $2,500 to $5,850 |

These fees are small relative to the total deal value. Skipping escrow to save $3,000 on a $500,000 transaction is not a smart decision.

Wondering what the total closing costs look like for your deal? Use our calculators to estimate your numbers.

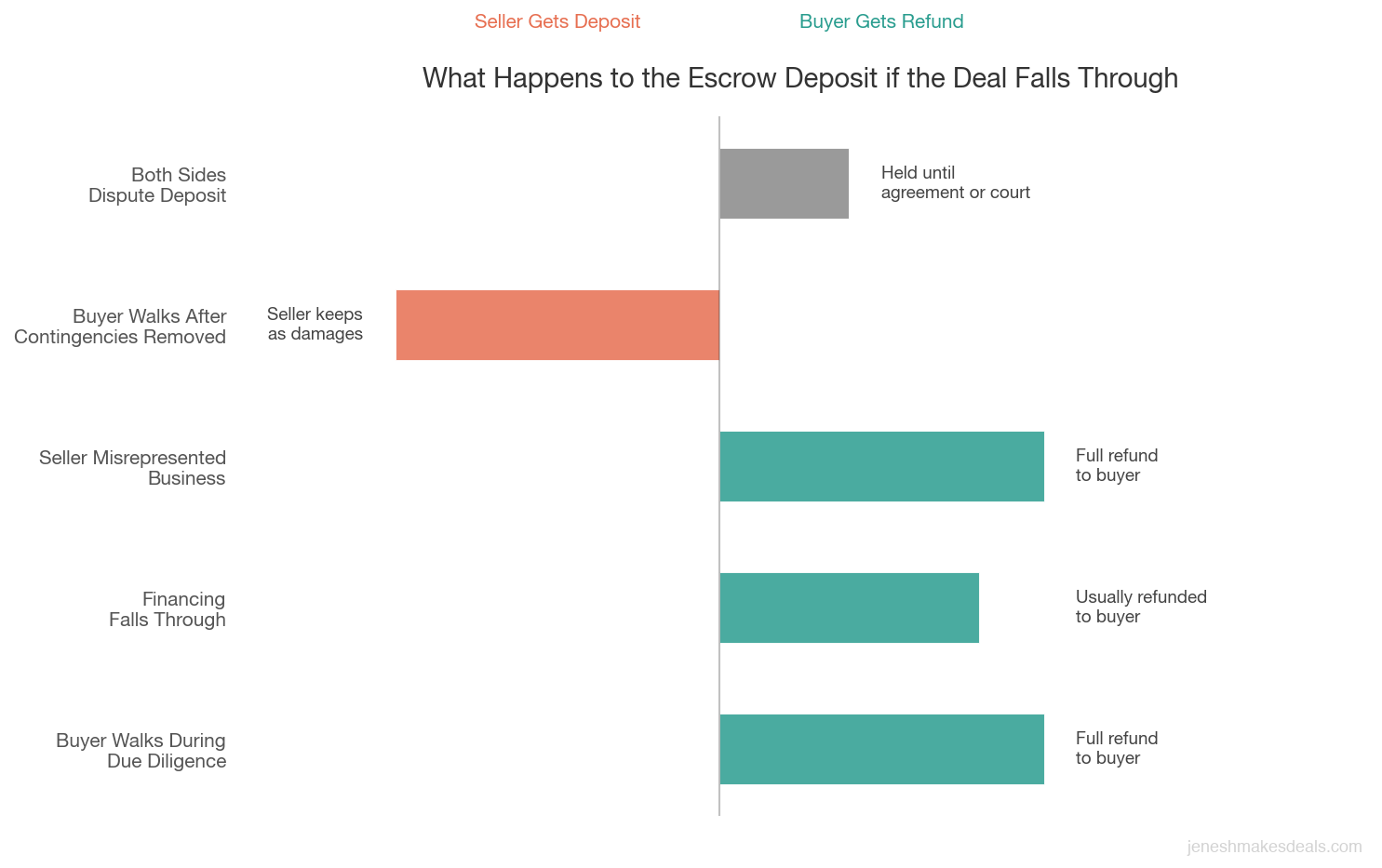

What Happens to the Escrow Deposit if the Deal Falls Through

This is one of the most common questions I get from both buyers and sellers. The short answer: it depends on why the deal fell through and what your purchase agreement says.

Scenario 1: Buyer walks away during due diligence. If the purchase agreement includes a due diligence contingency (and it should), the buyer can cancel for any reason and get their full deposit back. This is the most common cancellation scenario.

Scenario 2: Buyer walks away after contingencies are removed. Once contingencies are removed, walking away gets expensive. The seller is typically entitled to keep the earnest money as liquidated damages. If the buyer put down $40,000 and backs out without a valid reason, that $40,000 goes to the seller.

Scenario 3: Financing falls through. If the purchase agreement includes a financing contingency and the buyer's loan gets denied, the buyer usually gets their deposit back. This is why sellers should verify the buyer's financial qualifications before accepting an offer.

Scenario 4: Seller can't deliver what was promised. If due diligence reveals misrepresented revenue, hidden liabilities, or lease assignment problems, the buyer can cancel and get their deposit returned.

Scenario 5: Both sides dispute the deposit. If the buyer and seller disagree about who's entitled to the deposit, the escrow agent can't pick a side. They'll hold the funds until both parties agree or a court decides. This mediation process can take 60 to 120 days.

The key takeaway: your deposit protection is only as good as the contingencies in your purchase agreement. Work with your attorney to make sure every contingency has clear trigger conditions and timelines.

The number one mistake I see in deposit disputes is vague contingency language. "Subject to satisfactory due diligence" means nothing in court. Spell out exactly what conditions allow the buyer to walk away and get their deposit back, including specific deadlines for each one.

Holdback Escrow for Post Closing Adjustments

Here's something most first time buyers and sellers don't know about: the escrow relationship doesn't always end at closing.

A holdback escrow (also called a post closing escrow or indemnification escrow) is an arrangement where a portion of the purchase price is held back in escrow for a set period after the deal closes. The purpose is to protect the buyer against problems that surface after closing.

How much gets held back? Typically 5% to 15% of the purchase price. On a $600,000 deal, that means $30,000 to $90,000 sits in escrow after closing.

How long does the holdback last? Most holdback escrows last 6 to 18 months. The specific duration is negotiated in the purchase agreement.

What triggers a holdback claim? Common reasons include inaccurate financial statements, customer contracts that don't transfer, undisclosed tax liabilities, equipment in worse condition than represented, and working capital below the agreed target.

How does the release work? If no claims are filed during the holdback period, the full amount is released to the seller. If the buyer files a claim, the escrow agent holds the disputed portion until the parties resolve the issue.

Holdback escrows are standard in deals over $1 million. For smaller deals, they're less common but still worth considering if there's any uncertainty about the business post closing.

Thinking about selling your business and want to understand your potential deal structure? Get a free valuation estimate.

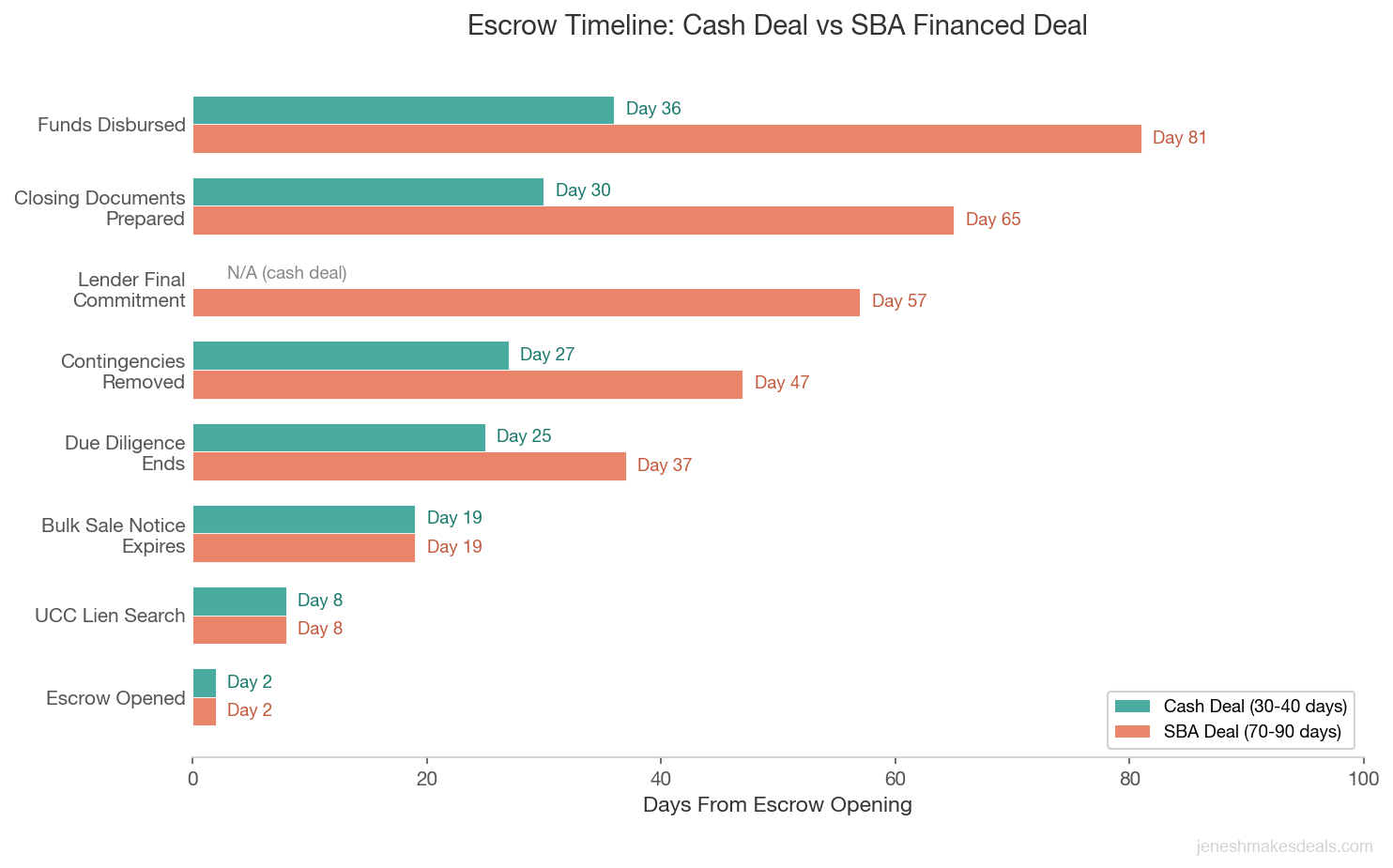

The Escrow Timeline Step by Step

Here's a realistic timeline for a typical escrow period on a small business transaction. I've included both cash deal and SBA financed timelines since the difference is significant.

| Milestone | Cash Deal | SBA Financed Deal |

|---|---|---|

| LOI signed, deposit submitted | Day 1 | Day 1 |

| Escrow opened, deposit received | Day 1 to 3 | Day 1 to 3 |

| Due diligence begins | Day 3 | Day 3 |

| UCC lien search completed | Day 7 to 10 | Day 7 to 10 |

| Bulk sale notice published (if required) | Day 5 to 10 | Day 5 to 10 |

| Bulk sale notice period expires | Day 17 to 22 | Day 17 to 22 |

| Due diligence period ends | Day 21 to 30 | Day 30 to 45 |

| Buyer removes contingencies | Day 25 to 30 | Day 45 to 50 |

| Lender issues final commitment | N/A | Day 50 to 65 |

| Lease assignment approved by landlord | Day 20 to 30 | Day 30 to 60 |

| Final closing documents prepared | Day 28 to 33 | Day 60 to 70 |

| Closing day: documents signed, funds wired | Day 30 to 40 | Day 70 to 90 |

| Funds disbursed to seller | Day 31 to 41 | Day 71 to 91 |

| Holdback escrow begins (if applicable) | Day 31 | Day 71 |

A few things to notice. SBA deals take roughly twice as long as cash deals because the lender is the bottleneck in almost every SBA transaction. And the landlord can delay things no matter how the deal is financed. I always tell my clients to start the landlord conversation as early as possible because a slow landlord can push your closing date back by weeks.

What Documents Go Through Escrow

The escrow agent handles a lot of paper. Here are the main categories of documents that flow through escrow.

Core transaction documents: Purchase agreement, bill of sale, assignment and assumption of lease, non compete agreements, and promissory notes or security agreements if seller financing is involved.

Financial and legal documents: UCC lien search results, bulk sale notice and proof of publication, the escrow agent's closing statement, and the allocation of purchase price for tax purposes.

Lender documents (SBA or conventional): Loan agreement, SBA authorization letter, personal guarantees, life insurance assignment, and standby agreements for any seller financing.

State and local filings: Tax clearance certificates, sales tax clearance, liquor license transfers (if applicable), and business license paperwork.

Operational transfer documents: Inventory list with values, customer and vendor contract assignments, employee information, training agreements, and domain name or social media account transfer authorizations.

The escrow agent tracks every document on a checklist and won't proceed to closing until every item is accounted for. Missing a single document can delay closing by days or weeks.

How to Choose an Escrow Company

Not all escrow companies are created equal. Here's what to look for and what to avoid.

Choose a company that specializes in business sales. A residential real estate escrow company may not understand bulk sale requirements, UCC searches, or SBA closings. Ask: "How many business sales have you closed in the past 12 months?" You want someone who's done at least 20 to 30 per year.

Ask about their closing timeline. A good escrow company can open within 24 to 48 hours of receiving the deposit. If they tell you it takes a week, find someone else.

Check their communication style. Some escrow agents send weekly status updates. Others go silent for days. Ask for references from recent clients and specifically ask about responsiveness.

Verify their licensing and bonding. In California, escrow companies must be licensed by the DFPI. In other states, requirements vary. Always confirm proper licensing and bonding.

Understand their fee structure upfront. Get a written estimate of all fees before you commit. Some companies quote a low base fee and add charges for every additional service.

Red flags to watch for:

- They can't provide a clear timeline or checklist

- They charge significantly less than competitors

- They don't have errors and omissions insurance

- They've never handled a deal with SBA financing

I keep a short list of escrow agents I trust and introduce my clients to them early so there's no scramble when it's time to open escrow.

Common Escrow Problems and How to Avoid Them

I've seen deals go sideways during escrow for all kinds of reasons. Here are the most common problems and what you can do to prevent them.

Problem: The landlord takes forever to approve the lease assignment. This is the number one source of escrow delays in my experience. The fix: start the landlord conversation the day escrow opens, not after due diligence is complete. Build in extra time because landlord delays will happen.

If your deal depends on a lease assignment, treat the landlord as a third party to the transaction. I've seen closings delayed by 30 or more days because nobody contacted the landlord until week six of escrow. Reach out on day one, get their requirements in writing, and follow up weekly.

Problem: UCC search reveals unexpected liens. The buyer finds a $60,000 equipment loan lien the seller forgot to mention. The fix: sellers should run their own lien search before listing. If there are liens, disclose them upfront and include a plan for paying them off at closing.

Problem: SBA lender keeps requesting additional documents. The loan was supposed to be approved in 30 days, but the lender keeps asking for more documentation. The fix: use an experienced SBA lender who has processed acquisition loans before. Inexperienced lenders cause the most delays.

Problem: Buyer and seller disagree on inventory valuation. The purchase agreement says inventory transfers at "fair market value" but doesn't define what that means. The fix: specify the valuation method, who counts inventory, and when. An independent third party count the day before closing eliminates most disputes.

Problem: The buyer's wire transfer doesn't arrive on closing day. The fix: initiate wire transfers at least 2 business days before the scheduled closing. Same day wires can be delayed by the receiving bank's processing.

Problem: Post closing surprise liabilities surface. The buyer discovers an unpaid vendor invoice for $15,000 that was never disclosed. The fix: this is exactly why holdback escrow exists. If you negotiated a holdback, the buyer can file a claim against the escrowed funds.

Have questions about your deal? Reach out and let's talk through your situation.

Real Scenarios Where Escrow Made the Difference

Let me share a few real situations from transactions I've been involved with. I've changed the details to protect privacy, but the lessons are accurate.

The Case of the Hidden Tax Lien

A buyer was purchasing a dry cleaning business for $350,000. Everything looked clean during due diligence. Financials matched, customers were loyal, the lease was in good shape. But when the escrow agent ran the UCC and tax lien search, they found a $42,000 state tax lien against the business.

The seller claimed he had "worked out a payment plan" with the state. He hadn't. The lien was active and would have attached to the business assets post closing.

Because we caught it through escrow, the solution was straightforward. The escrow agent held $42,000 from the seller's proceeds at closing and paid the state directly. The buyer got a clean business, and the seller still received the remaining balance. Without escrow and the lien search, the buyer would have inherited that tax debt.

The Financing That Almost Collapsed

A seller accepted an $800,000 offer for his landscaping company. The buyer was using SBA financing. On day 55, the lender discovered one of the buyer's partners had a bankruptcy from eight years ago and pulled back.

The seller wanted to cancel and move to the backup offer. But the buyer's $80,000 deposit was secure in the escrow account, and the escrow agent confirmed the financing contingency was still in effect. The buyer found a new SBA lender who approved the loan in 18 days, and the deal closed at day 95 instead of 75. Without escrow's structure and clear contingency language, this deal would have died.

The Inventory Dispute

Two partners were selling their restaurant for $275,000. The deal included inventory "at cost." Simple enough, right? Wrong.

At the inventory count two days before closing, the buyer and seller disagreed on the wine and liquor inventory. The seller said $28,000. The buyer's count came in at $19,000. The seller was counting at retail value, not cost.

The escrow agent paused the closing while both attorneys negotiated. They brought in a neutral third party to do a fresh count at wholesale cost, which came in at $21,500. The escrow agent adjusted the closing statement, and the deal closed two days late.

The lesson: define your terms precisely. "At cost" is not the same as "at retail" or "at replacement cost." The escrow agent can't resolve ambiguity in your contract.

Tips for a Smooth Escrow Experience

After dozens of deals, here's what I tell every buyer and seller before we open escrow.

For buyers:

- Get financing pre approval before submitting your LOI. Don't open escrow until your lender is likely to approve.

- Respond to document requests within 24 hours. Every day you delay extends the timeline.

- Don't make major financial changes during escrow. No new credit lines, no quitting your job, no large purchases. Your lender is watching.

For sellers:

- Have your documents organized before escrow opens. A due diligence checklist tells you exactly what the buyer will ask for.

- Disclose everything. Surprises during escrow kill deals.

- Keep running the business. Revenue drops during escrow spook buyers and lenders.

For both sides:

- Choose an experienced escrow agent. This is not the place to save $500.

- Build in buffer time. If you think escrow will take 60 days, plan for 75.

- Communicate through your broker. A single point of coordination prevents miscommunication.

- Don't panic when issues come up. Something unexpected happens in almost every escrow. The question isn't whether something will go wrong. It's how quickly you resolve it.

Ready to start the process of buying or selling a business? Let's connect and discuss your next steps.

Final Thoughts

The escrow agent is one of the most important people in your business transaction, and they're the one you'll probably think about the least. They work in the background, making sure every document is collected, every lien is cleared, every dollar ends up where it's supposed to go.

A good escrow agent won't make or break the business itself. But they can absolutely make or break the deal. Ask your broker for a recommendation, interview the escrow company before you commit, and don't treat this as an afterthought. The few thousand dollars you spend on a professional escrow agent is some of the best money you'll spend in the entire transaction.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.