You've agreed on a price, signed a letter of intent, and you're moving through due diligence. Then your buyer's attorney sends over a redline of the purchase agreement, and you notice something. The buyer wants to exclude accounts receivable from the deal. Or they want to buy them at a discount. Or they're saying the AR needs to be cleaned up before closing.

What exactly is going on?

Accounts receivable is one of the most commonly misunderstood and most frequently disputed line items in a business sale. I've worked through dozens of AR negotiations, and I can tell you that how you handle this before and during the sale process has a direct impact on how much money you walk away with.

Here's what you need to know.

What Accounts Receivable Actually Means in a Sale

Accounts receivable is the money your customers owe you for work you've already done or products you've already delivered. On your balance sheet, it shows up as a current asset because it's expected to be collected within 12 months.

In the context of a business sale, AR is significant for a specific reason: it represents cash that exists in the business that someone is going to collect. The question is who. And the answer depends entirely on how the deal is structured.

If your business carries $150,000 in outstanding receivables at the time you sell, that's real money. The buyer knows it. You know it. And both of you have a stake in what happens to it. The negotiation around AR is essentially a negotiation over which party is entitled to that cash and who bears the risk of non collection.

The Three Ways AR Gets Handled in a Business Sale

There's no single standard for how AR is treated. The approach varies by deal size, industry, buyer sophistication, and what both parties can agree to. But virtually every deal falls into one of three structures.

Option 1: The Seller Keeps the AR

This is the most common approach in small business asset sales. The buyer purchases the operating business, equipment, goodwill, inventory, and everything else, but accounts receivable are explicitly excluded from the purchase. The seller retains the receivables and collects them after closing using the old business entity.

This structure is clean for the buyer. They don't have to worry about collecting money from someone else's customers, and they're not taking on the risk of uncollectible receivables. They simply start fresh with new revenue coming in the door.

For the seller, this means the deal price doesn't include AR. But you still collect it post closing. On a $150,000 AR balance with a 90% collection rate, you'd expect to collect roughly $135,000 over the 30 to 90 days after closing. That's money that comes to you separately from the purchase price.

The downside is that you're now a former owner trying to collect money from customers you no longer serve. Some customers will pay quickly. Others will use the ownership transition as an excuse to delay payment or dispute invoices. Getting all the cooperation you need from the new owner, who controls the customer relationships, can be a challenge.

Option 2: The Buyer Purchases the AR

In this structure, the buyer pays for the receivables as part of the deal. The AR is included on the balance sheet that transfers and the buyer takes over collection responsibilities.

This sounds simple but it introduces a valuation problem immediately. Not all receivables are worth face value. An invoice that's 10 days old and owed by a reliable Fortune 500 company is worth close to 100 cents on the dollar. An invoice that's 110 days old from a customer you've been chasing for three months is worth considerably less.

Buyers who purchase AR typically apply a discount schedule based on the age of each receivable. We'll talk about how that discount schedule works in a moment.

Option 3: AR Is Included in the Working Capital Target

In larger deals, especially acquisitions of businesses with $1 million or more in SDE, AR is often treated as part of the working capital calculation rather than as a separate line item negotiation. The purchase agreement establishes a working capital peg, and AR is one of the current assets that goes into that calculation.

If you want the full picture on how working capital pegs are calculated and how they affect your net proceeds, I covered it in detail in my post on working capital adjustments. For purposes of this discussion, know that when AR is inside the working capital structure, the negotiation shifts from "who keeps the AR" to "what's the right amount of AR to include in the peg."

Need help thinking through your deal structure? Reach out for a free consultation and we can walk through the specifics of your situation.

The AR Aging Schedule Explained

Whether you're selling the AR or keeping it, the first thing any buyer is going to ask for is an AR aging schedule. This is a report that shows every outstanding invoice, sorted by how old it is.

A standard aging schedule breaks receivables into four buckets:

| Aging Bucket | Description | Typical Collectibility |

|---|---|---|

| Current (0-30 days) | Within normal payment terms | 95-100% |

| 31-60 days | Slightly past due | 85-95% |

| 61-90 days | Clearly past due | 70-85% |

| 91+ days | Seriously delinquent | 40-60% (or less) |

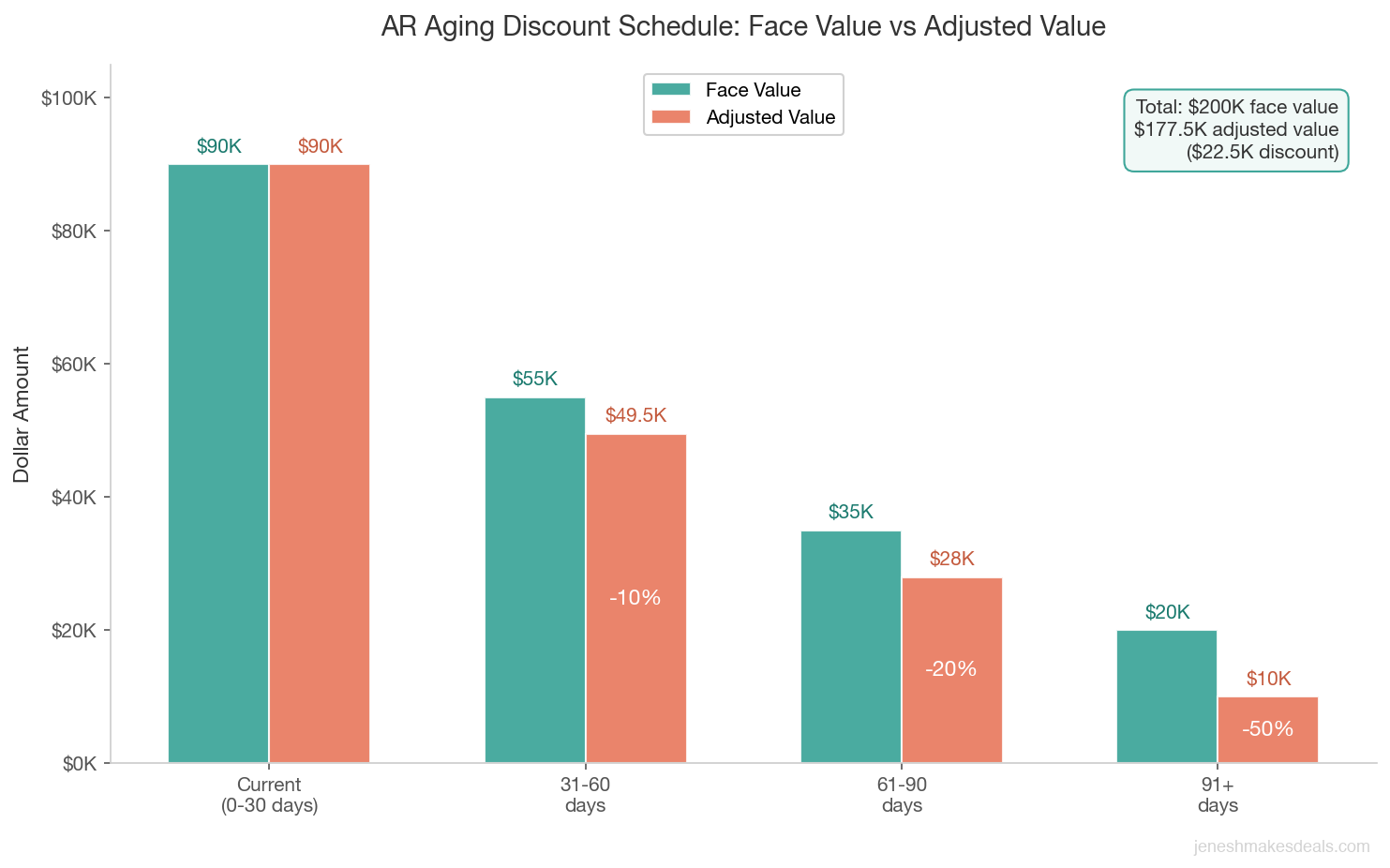

Let me put real numbers to this. Say your business has $200,000 in total AR:

- $90,000 current (0-30 days)

- $55,000 at 31-60 days

- $35,000 at 61-90 days

- $20,000 at 91+ days

That's $200,000 on paper. But what's it actually worth?

A buyer applying a standard discount schedule might value it like this:

| Bucket | Balance | Discount | Adjusted Value |

|---|---|---|---|

| Current | $90,000 | 0% | $90,000 |

| 31-60 days | $55,000 | 10% | $49,500 |

| 61-90 days | $35,000 | 20% | $28,000 |

| 91+ days | $20,000 | 50% | $10,000 |

| Total | $200,000 | $177,500 |

So a buyer might offer $177,500 for what looks like $200,000 in receivables. The discount reflects the reality that old receivables are harder to collect.

The older the invoice, the less it's worth in a buyer's eyes. Current AR trades at full value while anything past 90 days gets cut in half or more.

If the deal is structured so you keep the AR and collect it yourself post closing, this valuation exercise tells you what to expect. You probably won't collect all $200,000. Budgeting for 85-90% of face value on a typical AR book is realistic.

How Buyers Discount Old Receivables

The aging schedule is the starting point, but buyers often apply additional analysis to individual receivables based on customer specific factors.

A single invoice for $40,000 that's 75 days old matters a lot more than $40,000 spread across 20 customers at the same age. One big delinquent account is a concentration risk. Twenty small past due balances are a collection logistics problem.

Buyers also look at whether specific customers have a history of paying slowly. If you have a customer who always pays at 60 days even though terms are net 30, that's actually fine. Their receivables aren't really delinquent from a practical standpoint. A buyer who understands this won't apply the same discount to a habitual slow payer that they'd apply to a genuinely delinquent account.

On the other end, if a receivable is past due because the customer disputed the invoice, that's a red flag. Buyers will either exclude disputed invoices entirely or assign them a very high discount (60 to 80%). An invoice in dispute isn't really an asset. It's a potential liability.

The other thing buyers watch for is customer concentration in the AR. If 40% of your total receivables come from one customer, and that customer is 90 days past due, you have a problem. That's the kind of thing that can change deal structure or reduce the price.

Asset Sale vs. Stock Sale: How Deal Structure Changes the AR Picture

The difference between an asset sale and a stock sale has big implications for how AR is handled. If you want a full breakdown of those two deal structures, I've written about that here. But here's the AR specific version.

In an asset sale, the buyer specifies exactly which assets they're purchasing. The default in most small business asset sales is to exclude AR. The seller keeps the receivables and collects them through the old entity after closing. The buyer pays for the operating business without the receivable balance baked in.

In a stock sale, the buyer is purchasing the entire entity, which means they're getting everything on the balance sheet, including AR. There's no separate negotiation about whether to include receivables because they come with the purchase automatically.

| Factor | Asset Sale | Stock Sale |

|---|---|---|

| AR included by default? | No, explicitly excluded | Yes, comes with the entity |

| Who collects old AR? | Seller (via old entity) | Buyer (new owner of entity) |

| AR valuation negotiation | Separate from purchase price | Embedded in total deal price |

| Bad debt risk | Seller bears it | Buyer bears it (offset by discount) |

| Customer confusion | Higher (two entities involved) | Lower (same entity continues) |

| Typical business size | Small businesses under $1M SDE | Larger businesses, $1M+ SDE |

This distinction matters because it affects the price conversation. In an asset sale where AR is excluded, the buyer should not be paying for it. If a buyer's LOI is based on a trailing 12 month earnings multiple, and they're not taking the AR, the purchase price should reflect that. Sellers sometimes get confused and assume the AR is in the deal even when it isn't.

In a stock sale, if you're sitting on $150,000 in receivables, the buyer is paying for those receivables whether they want to or not. This makes quality of AR much more important in stock sales. A buyer who discovers $40,000 in uncollectible receivables post closing has effectively overpaid for the business. That's exactly why buyers in stock sales ask detailed questions about AR quality during due diligence.

Working Capital Adjustments and AR

When AR is included in the working capital peg, it creates an ongoing measurement problem that I want to walk through carefully.

The working capital peg is set based on a trailing average, often 12 months. If your AR has historically averaged $100,000 and it's $60,000 on closing day, your working capital is below the peg by $40,000. The buyer can claim a working capital adjustment and reduce your proceeds accordingly.

This can be a trap for sellers. If you've been aggressively collecting receivables in the months before closing (which you naturally would, to maximize cash flow), you might inadvertently drop your AR below the historical average. That's going to trigger a working capital shortfall even if you didn't do anything wrong.

The flip side also happens. If you have a strong receivables month right before closing and AR is $140,000 instead of the $100,000 average, you might be entitled to an additional $40,000 from the buyer on the true up. That's a real gain.

The lesson here is to track your AR balance monthly for at least 12 months before going to market. Know what your average looks like. Run it in parallel with the overall working capital calculation so you're not surprised when the peg is established.

If you've been aggressively collecting receivables before closing, you can accidentally trigger a working capital shortfall that reduces your proceeds by tens of thousands of dollars.

Want to understand how your AR affects your business valuation? Use our free business valuation calculator to see how your current assets factor into a sale price estimate.

Who's Responsible for Collecting AR After Closing

This is the question sellers always ask and it depends entirely on deal structure.

If the seller keeps the AR, the seller is responsible for collection. The challenge is that you no longer own the business, you no longer have the customer relationships, and you're relying on the buyer to forward any payments that accidentally come to the business.

In a well structured deal, the purchase agreement will include a AR collection cooperation clause. This typically says something like: if a customer sends payment to the new business for an invoice that predates closing, the buyer is obligated to forward that payment to the seller promptly, typically within five business days. You want this in writing.

The reverse also matters. If a customer sends a post closing invoice payment to the old entity, make sure the seller knows to keep it. Confusion about which invoices belong to which period is a real source of conflict.

Some deals include a formal collection arrangement where the buyer agrees to assist with collection of the seller's old receivables for a period of 60 to 90 days after closing. This makes sense when the buyer has ongoing relationships with the customers and can more effectively facilitate payment. The seller might pay a small fee for this service, or it might be a condition of the deal.

What Happens to Bad Debt

Bad debt is uncollectible receivables, and every business has some. The question at closing is who bears the loss.

If the seller keeps the AR, the seller eats the bad debt. Whatever you can't collect stays on your problem list post closing. You can write it off on your taxes, but the economic loss is yours.

If the buyer purchases the AR, the bad debt risk has theoretically been addressed through the discount schedule. The buyer paid below face value precisely to account for expected losses. If actual collections come in worse than the discount implied, the buyer loses money. If collections are better than expected, the buyer profits from the spread.

When AR is inside a working capital structure, bad debt reserves need to be handled carefully. Sellers who haven't established an allowance for doubtful accounts are setting themselves up for a dispute. If your balance sheet shows $200,000 in AR with no bad debt reserve, but a reasonable reserve would be $20,000, the buyer will add that back as a reduction to working capital during the true up.

Keep your bad debt reserve accurate and current in the 12 months before going to market. It's a small thing that prevents a big dispute later.

Common AR Disputes at Closing

I want to be direct about the fights I've seen, because knowing where the flashpoints are is the best way to prevent them.

The seller collected aggressively before closing. In the 60 to 90 days before closing, the seller pushed hard to collect every outstanding invoice. AR dropped from $180,000 to $65,000. If AR was inside the working capital peg, the seller just triggered a significant shortfall. The buyer demands an adjustment. The seller says "I was just running the business." Both parties are annoyed.

Disputed invoices nobody mentioned. One customer has been holding $30,000 in invoices because they have an unresolved dispute about a project deliverable. The seller didn't mention this during due diligence. The buyer discovers it at closing when the aging schedule shows the invoices as current but the customer hasn't paid in 90 days. Now there's a credibility problem and a collection problem at the same time.

The old entity went dark. After closing, the seller wound down the old entity quickly and stopped monitoring their email. Customers who were supposed to pay the old entity direct don't hear anything back. Some of them just stop paying. The seller loses tens of thousands in collections because they checked out too early.

No cooperation from the buyer. A customer calls the new owner asking about an old invoice. The buyer says he doesn't know anything about it and refers them to the seller. The customer gets confused, gets irritated, and eventually stops responding. The buyer could have facilitated a clean payment with one five minute conversation. The cooperation clause would have required it.

Post closing credits. A customer received defective product under the previous owner's watch and claims a credit against their open invoice. Under the old ownership that would have been resolved. Now the customer is deducting $8,000 from their payment and the seller argues the buyer should handle it because the buyer controls the relationship. This kind of thing needs to be addressed in the purchase agreement.

Industry Specific Considerations for AR

AR dynamics vary significantly by industry, and if you're in one of these three sectors, you need to understand the specific issues.

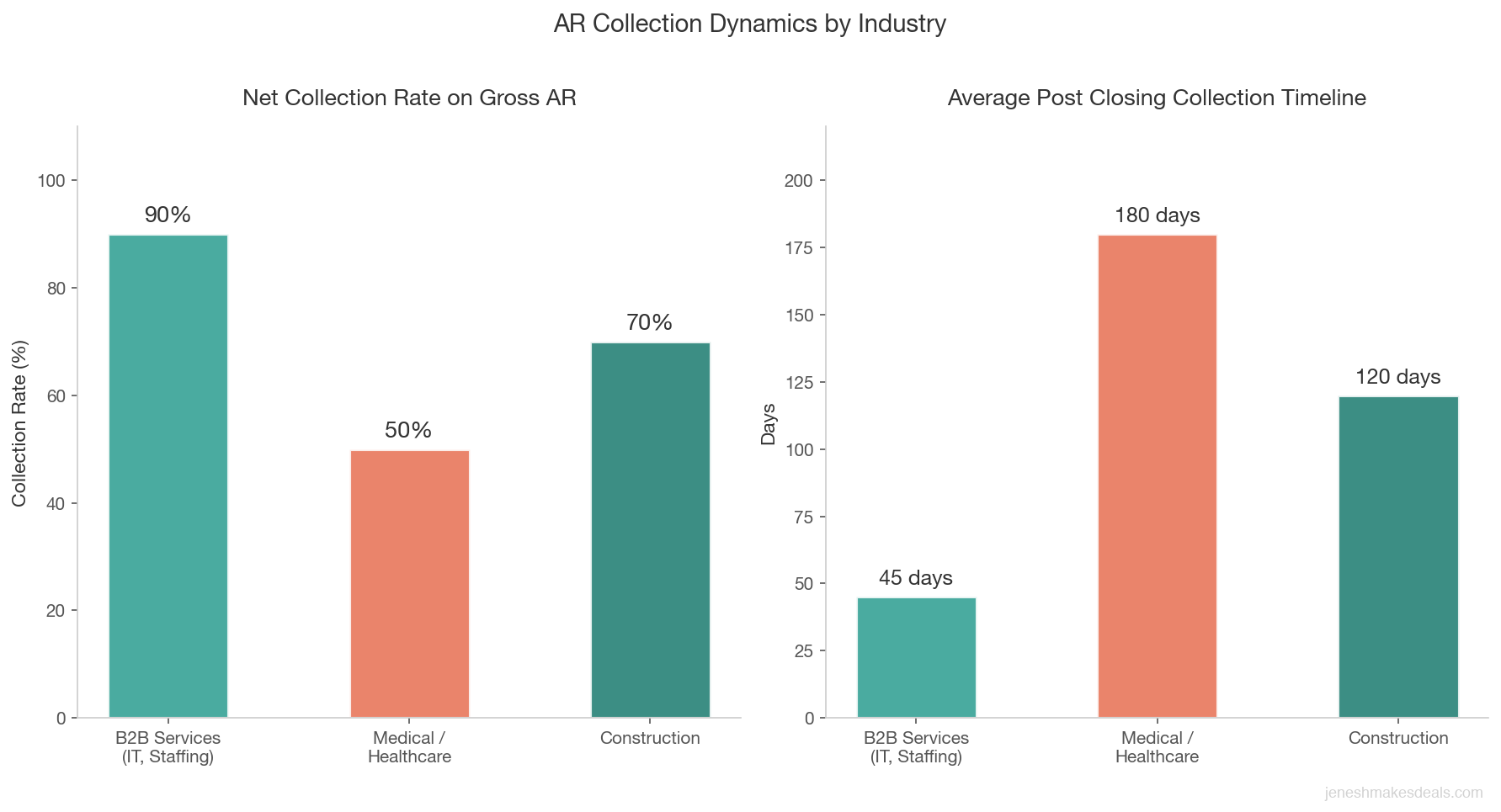

B2B Services (IT, Marketing, Consulting, Staffing)

B2B service businesses often have substantial AR because corporate clients pay on net 30 or net 60 terms. A staffing agency doing $2 million in annual revenue might carry $150,000 to $300,000 in AR at any given time.

The good news is that AR from established corporate clients is highly collectible. A Fortune 500 company's payables department may be slow, but they will pay. Buyers discount this less aggressively.

The risk is customer concentration. If 40% of your AR comes from one client, and that client decides to reassign the account after the ownership change, your receivables quality drops dramatically. Buyers scrutinize customer concentration hard in B2B service businesses.

Medical and Healthcare

Medical AR is its own ecosystem. Insurance reimbursements, Medicare and Medicaid claims, and patient balances all move on very different timelines. A medical practice might have $400,000 in gross AR but only $200,000 in net collectible AR after accounting for contractual adjustments, insurance denials, and patient portion write offs.

Healthcare buyers know this. They will not pay face value for medical AR under almost any circumstances. They'll want a detailed breakdown of payer mix, historical collection rates by payer, and any outstanding claim denials. Buyers in healthcare deals typically apply 40 to 60% discounts to gross AR as a starting point.

If you're selling a medical practice, expect to retain the AR and collect it yourself over the 12 to 24 months post closing. The collections process for insurance claims is long and complex. A new owner trying to collect your pre closing insurance claims while also running the practice is not a recipe for success.

Construction

Construction AR is notoriously difficult to value. Progress billings, retainage, disputed change orders, and lien rights all complicate the picture. A general contractor might show $500,000 in AR but $200,000 of that could be retainage that won't be released for six months after project completion.

Buyers in construction deals almost always exclude AR from the purchase, with the seller retaining and collecting it. The seller is in a better position to resolve contract disputes, chase retainage release, and process change order claims that require knowledge of each job's history.

If you're selling a construction business, get your AR as current and documented as possible before going to market. Close out completed jobs. Resolve disputed change orders. Get retainage released where you can. Clean AR is one of the clearest signals to a buyer that your business is well managed.

How to Clean Up AR Before You Sell

This is the most actionable section of this post. If you're 6 to 18 months away from selling, AR cleanup is something you can do right now that directly improves your deal.

Collect aggressively on anything over 60 days. Any invoice past 60 days that isn't in dispute needs a formal collection push. Call the customer. Send a formal past due notice. Set a payment plan if needed. A collected invoice is worth 100 cents on the dollar. An invoice that's 90 days old when you go to market is worth 50 to 60 cents in a buyer's eyes.

Write off what's truly uncollectible. Some AR is dead. The customer is out of business. The invoice is disputed beyond resolution. The amount is too small to pursue. Write it off now, update your bad debt reserve, and clean the balance sheet. Buyers who see $15,000 in three year old invoices still sitting on the books immediately question your financial hygiene.

Resolve disputes before you list. If you have customers with disputed invoices, do whatever it takes to resolve them before you start the sale process. Even if you need to accept a partial payment or issue a credit, a resolved dispute is better than an open one that will scare off buyers during due diligence.

Document your aging schedule clearly. Every outstanding invoice should have a clear record of when it was issued, what it was for, when you last communicated with the customer, and what the customer's response was. When a buyer asks about specific large invoices, you should be able to tell the story of each one without digging through emails.

Separate recurring customer slow payers from truly delinquent ones. If you have customers who habitually pay at 45 days even though terms are net 30, flag them as slow payers with a long track record of eventually paying. A buyer who sees that pattern in the data won't apply the same discount they'd apply to a genuinely delinquent account.

Stop carrying AR that shouldn't exist. Some businesses have unbilled work: completed projects where the invoice hasn't been sent. Get those invoices out immediately. Unbilled AR that shows up during due diligence as "work in progress" creates confusion about whether it's actually collectible.

Planning to sell in the next year or two? Reach out to talk through your preparation timeline and we can help you figure out where to focus.

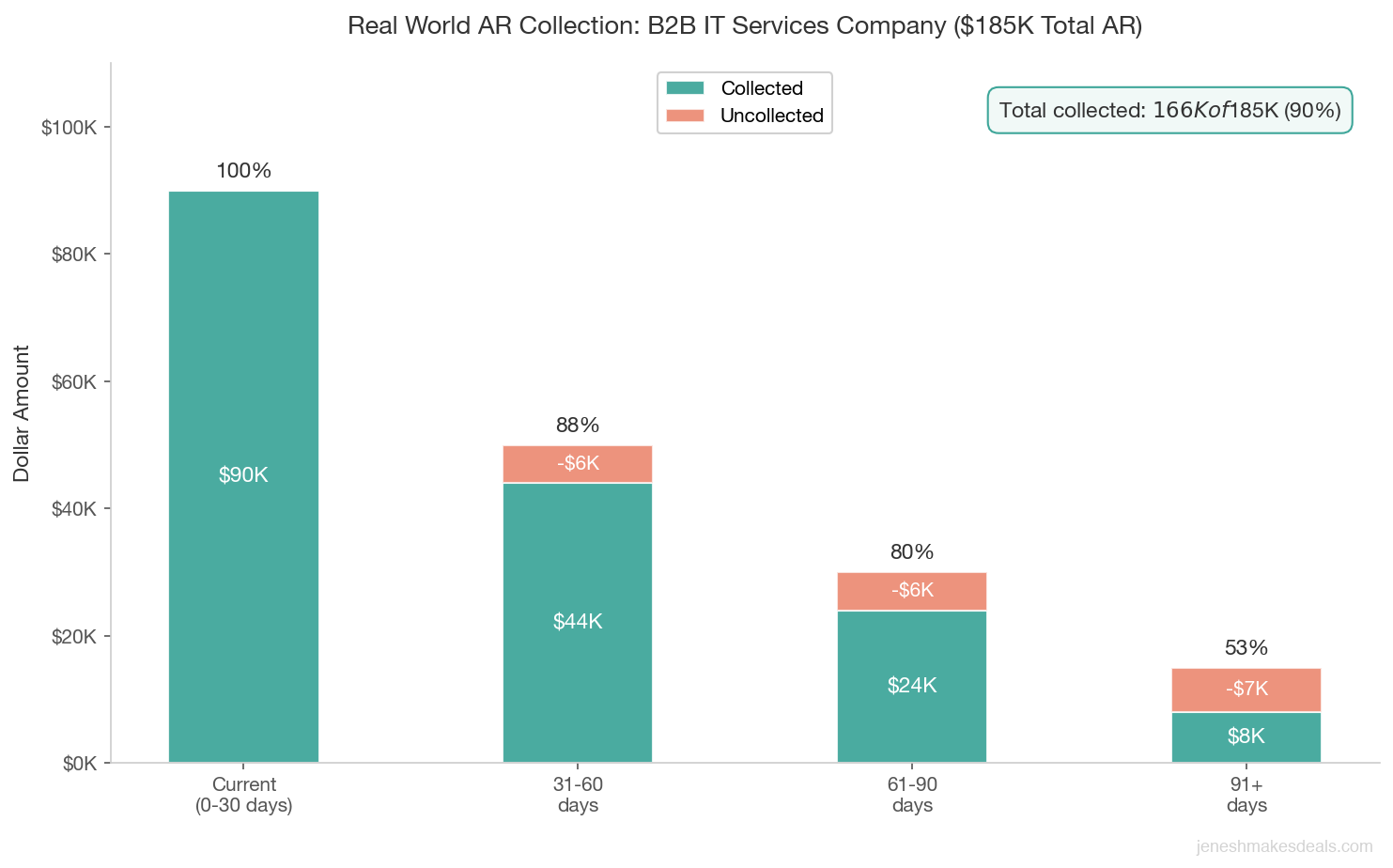

A Real World Example of How AR Affects the Deal

Let me walk you through a scenario I've seen play out more than once.

A B2B IT services company. $800,000 in annual revenue. $210,000 in SDE. Asking price: $630,000 at a 3x multiple. On the balance sheet at the time of going to market: $185,000 in AR.

The aging schedule breaks down like this:

- $90,000 current (under 30 days)

- $50,000 at 31-60 days

- $30,000 at 61-90 days

- $15,000 at 91+ days (two old invoices from a customer who went through management changes and had been slow to resolve)

The buyer comes in with an asset purchase offer. They exclude the AR. The seller retains the receivables. The buyer pays $630,000 for the operating business.

Now what does the seller actually get?

He collected $90,000 of the current AR within 30 days of closing. The 31-60 day bucket came in at $44,000 (lost $6,000). The 61-90 bucket took 90 days post closing and came in at $24,000 (lost $6,000). The 91+ bucket? One customer paid $8,000, the other never paid. He wrote off $7,000.

Total AR collected: $166,000 out of $185,000. That's 90% collection, which is normal.

Total proceeds: $630,000 purchase price + $166,000 AR = $796,000 before transaction costs. That's a better outcome than if the buyer had purchased the AR at a 15% discount and applied it to the purchase price. The seller came out ahead by retaining and collecting his own receivables.

If your AR is reasonably clean and current, retaining it and collecting it yourself will usually net you more than selling it to the buyer at a discount. Expect to collect around 90% of face value on a well managed AR book.

The risk is that collection takes time and requires ongoing effort after closing.

What to Do Right Now

If you're thinking about selling in the next 12 to 24 months, here's where to start.

Pull your AR aging schedule today. If you're not already running it monthly, start. Know exactly what's current, what's past due, and what's at risk. This isn't just a selling preparation task, it's good financial management.

Look at your largest past due balances individually. Are they disputes? Are they slow payers with a track record of paying eventually? Are they genuinely delinquent? Each one needs a different approach.

Talk to your accountant about your bad debt reserve. Is it accurate? Does it reflect actual collection history? A reserve that's too low will create problems in the due diligence process.

And if you're getting close to listing, discuss the AR strategy with your broker before you start talking to buyers. Do you want to retain the AR and collect it post closing? Include it in working capital? Offer to sell it to the buyer at an appropriate discount? Each approach has trade offs, and the right answer depends on your AR quality, your timeline, and your buyer's sophistication.

Ready to start thinking through your exit? Contact me for a confidential conversation about your business, your AR, and what a realistic deal looks like. No pressure, no obligation, just a straight conversation about your numbers.

You can also tell us about your business to get started on your exit planning today.

Related Articles

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

April 25, 2026

The Role of an Escrow Agent in a Business Transaction

Escrow agents protect both buyer and seller during closing. Learn what they do, what they cost, and how to choose one.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.