One of the most emotionally charged parts of selling a business isn't the negotiation or the due diligence. It's the question of what happens to the people who helped you build it. I've had sellers tell me this is the thing they lose sleep over. They've worked alongside their employees for ten, fifteen, sometimes twenty years, and the idea of putting them in a precarious position doesn't sit right.

The good news is that most buyers want to keep good employees. They're not buying a building or a brand. They're buying a business that runs because of the people in it. But there are real legal, practical, and human dynamics at play, and sellers who don't understand them can make expensive mistakes, both financially and in terms of their reputation.

Here's what actually happens to employees when a business is sold, what you can and can't control, and how to handle it the right way.

The Number One Fear Employees Have When a Business Changes Hands

Ask any employee what they're afraid of when they hear their company is being sold and the answer is the same: "Am I going to lose my job?"

It's a reasonable fear. Business sales do sometimes result in layoffs, especially in situations where the buyer already has overlapping infrastructure, is buying for the assets rather than the operations, or plans to restructure the business significantly. But most small business acquisitions aren't like that. Most buyers are acquiring the business because it works, and the employees are a big part of why it works.

The problem is that employees don't know which type of buyer is coming. They assume the worst because that's what the news covers. Your job as a seller is to manage this fear thoughtfully, but the timing of how and when you do that matters enormously.

Most small business buyers are acquiring the business because it works, and the employees are a big part of why it works. Your team is an asset, not a liability.

Are Employees Required to Be Kept On After a Sale?

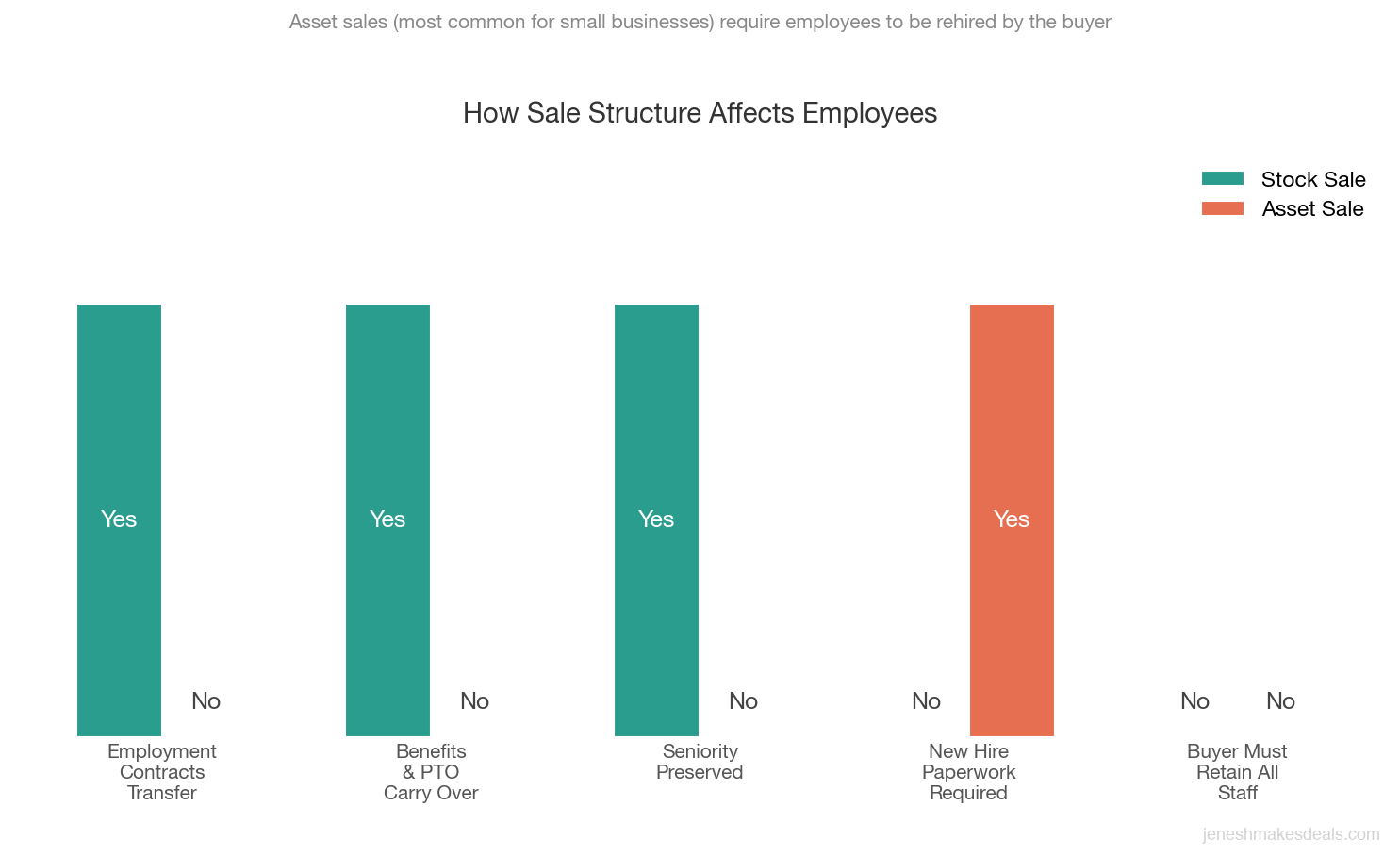

The short answer is no. In most small business asset sales, the buyer is not legally required to retain any employees. They're buying the assets and agreeing to hire staff as they see fit.

This is different from a stock sale, where the buyer takes over the legal entity itself and the existing employment contracts carry over. In an asset sale, which is the most common structure for small business transactions, employment relationships technically end with the sale and begin fresh with the new owner.

That said, most purchase agreements include provisions around employee matters. The buyer and seller typically agree that the buyer will offer employment to most or all current employees at the same or comparable compensation, at least for a transition period. These aren't always legally binding on the buyer past that transition window, but they're standard deal terms.

If retaining staff is important to you as a seller, you can negotiate for it. You can make it a condition of the sale that the buyer offers employment to key employees for a minimum period, say six to twelve months, before any reductions. Buyers who are serious and have a legitimate plan for the business will typically agree to this.

Employment at Will: What Sellers Can and Cannot Promise

Most employees in the U.S. work under "at will" employment, meaning either party can end the relationship at any time for any lawful reason. This creates a difficult reality for sellers: you may genuinely want to reassure your employees that their jobs are safe, but you can't legally make that promise on behalf of the buyer.

Even if the purchase agreement includes provisions for employee retention, those provisions only bind the buyer for a defined period. After that window, the buyer is free to make staffing decisions as any employer would.

This is an area where sellers sometimes create problems by overpromising. If you tell employees "the new owner promised you'll all keep your jobs," and the buyer restructures the team six months later, you've damaged both your credibility and your relationship with those employees. Worse, if it's in writing, it could expose you to legal liability.

What you can say is that the buyer has indicated their intention to retain the team and that employment will be offered as part of the transition. That's honest and accurate without making a promise you can't keep.

Never say "your job is safe" on behalf of the buyer. Instead, say the buyer has indicated their intention to retain the team. It's honest, accurate, and protects you from liability.

Key Employee Retention: Identifying Who You Can't Afford to Lose

In most small businesses, there are one or two or maybe three people without whom the business really struggles. It might be the operations manager who knows every client relationship. The lead technician who's the only one who can run the equipment. The bookkeeper who has 15 years of institutional knowledge in their head.

These are your key employees, and they need special attention in a sale process.

For sellers, key employees are both an asset and a risk. A buyer who learns that one person's departure would tank the business will either discount the offer significantly or walk away. So your job before and during the sale is to document what key employees do, cross train where possible, and give buyers confidence that the business can survive a transition. Employee stability is consistently one of what buyers look for in a small business in 2026.

Want to understand how owner dependence and key employee reliance affects your valuation? Read our post on how to value a business and see what buyers are actually paying for.

Documenting Key Employee Roles

Before you go to market, write down what each key employee is responsible for. What do they do daily? What would break without them? What processes are only in their head? This documentation serves two purposes: it reassures buyers that the business isn't held together by one person's memory, and it starts the knowledge transfer process before any buyer comes in.

Retention Bonuses: How Sellers Use Them to Protect the Deal

Retention bonuses are one of the most practical tools sellers have for protecting both their employees and the deal. Here's how they work.

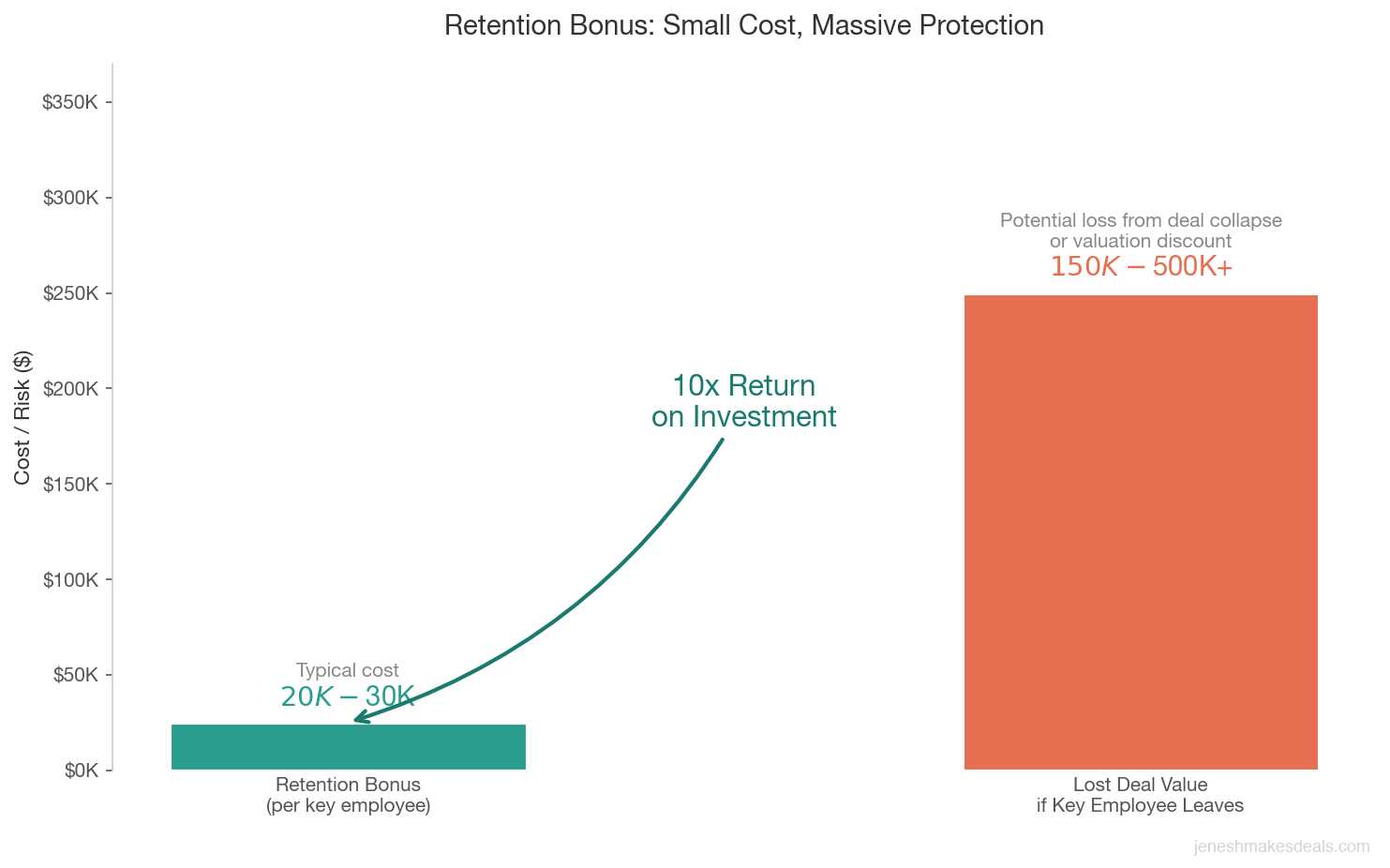

The seller agrees to pay a bonus to key employees who remain employed through a certain date, typically six to twelve months after closing. The bonus is funded either by the seller or by the buyer, or split between them. It's negotiated as part of the deal.

For example, a seller might say: "I'll pay my operations manager a $25,000 retention bonus if she stays for nine months after closing." That gives the buyer nine months to learn from her, build their own relationship with her, and either retain her long term or successfully transition her knowledge to someone else.

Retention bonuses do a few things at once. They incentivize key employees to stay, which protects the deal value. They signal to employees that they're valued and that the seller is looking out for them. And they give the buyer a runway to stabilize the business before any staffing changes.

The cost is worth it. I've seen deals fall apart because a key employee left during due diligence and the buyer lost confidence in the business. A $20,000 or $30,000 retention bonus is cheap insurance against a deal collapse.

Thinking about how to structure your exit and protect your team? Explore funding options that can cover retention bonuses and transition costs as part of your sale preparation.

Non-Compete Agreements for Employees Versus Owners

Non-competes come up in two different contexts in a business sale, and buyers and sellers often confuse them.

Owner Non-Competes

The seller is almost always required to sign a non-compete as part of the sale. This prevents you from taking the purchase price and immediately opening a competing business across the street. Typical owner non-competes run two to five years and cover a defined geographic area.

Employee Non-Competes

Buyers often ask whether existing employees have non-compete agreements. This matters because if key employees don't have non-competes and they leave after the sale, they could take clients or start a competing business. If you've never had employees sign non-competes, expect the buyer to ask about this and to potentially require them as part of the transition.

Enforceability of non-competes varies by state. California barely enforces them. Florida is more aggressive. Whatever agreements exist, have your attorney review them and be prepared to explain the situation to the buyer honestly.

Thinking about selling and want to understand what buyers will ask about? Contact us for a free consultation and we can walk through how to prepare your business for a sale.

How to Communicate the Sale to Employees: Timing Matters

This is where most sellers make their biggest mistake. They want to tell their employees as soon as possible because they feel guilty about keeping a secret. But announcing the sale too early can blow up a deal and leave everyone worse off.

Before the Deal Is Signed

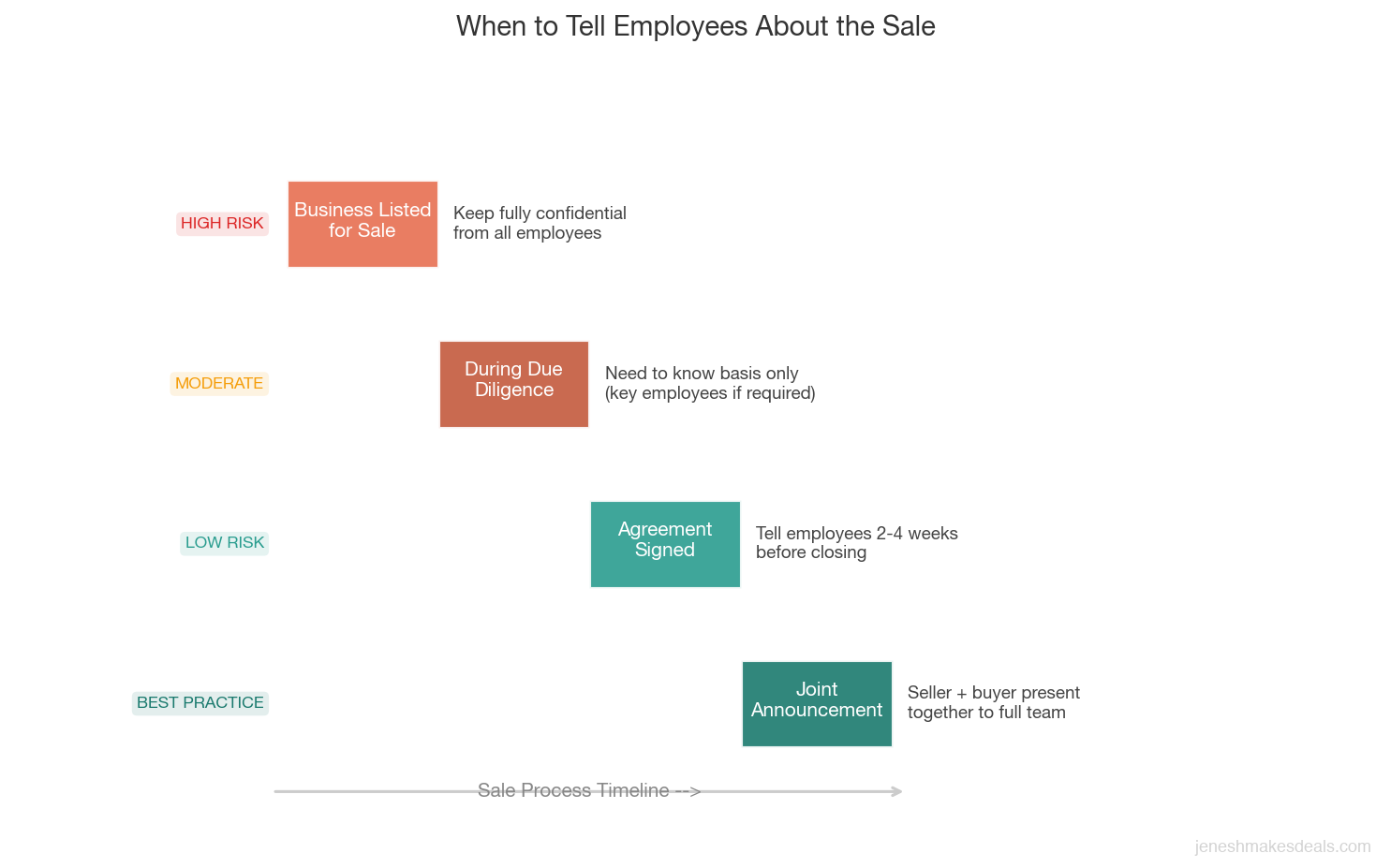

Telling employees before you have a signed purchase agreement is almost always a mistake. Deals fall apart. Buyers walk away. If you've already told your team the business is being sold and then the deal collapses, you've created anxiety and uncertainty for months, potentially lost good employees who started job searching, and damaged morale.

During Due Diligence

During due diligence, most buyers will need access to the business. This is where it gets tricky. Buyers want to talk to employees and verify operations. But you don't want every employee to know you're selling. The compromise is usually to give the buyer access to key employees on a need to know basis, ideally framing it as consulting with a business advisor or operations review.

Most buyers understand this and will keep confidences during due diligence. But it requires active communication between seller and buyer to manage well.

After Signing, Before Closing

The best time to tell employees is after you have a signed agreement, ideally a few weeks before closing. This gives them time to process the news, ask questions, and get reassurance from both you and the buyer before the transition happens. It also gives the buyer a chance to introduce themselves and begin building relationships before day one.

Benefits, PTO, and Existing Contracts: What Transfers and What Doesn't

In an asset sale, employment contracts and benefit obligations don't automatically transfer to the buyer. The buyer is hiring employees as new employees under their own employment structure.

This means a few things for employees:

| Employee Benefit | What Happens in an Asset Sale | What the Seller Should Do |

|---|---|---|

| Accrued PTO | May not be honored by buyer; depends on negotiation | Pay out accrued PTO at closing to clear the liability |

| Health Insurance | Resets under buyer's plan; possible coverage gap | Negotiate overlap period or COBRA bridge in the purchase agreement |

| 401(k) / Retirement | Does not transfer; tied to seller's entity | Notify employees early so they can arrange rollovers |

| Seniority / Tenure | May not carry over for benefits like extra vacation | Negotiate that buyer recognizes prior service for benefits accrual |

These details matter to your employees, and they matter to the buyer's ability to retain them. If your team finds out on day one that they've lost three weeks of accrued vacation they were counting on, they'll be frustrated and less likely to give the new owner their best work.

As a seller, address this in the purchase agreement. Negotiate who pays out accrued PTO, how long employees stay on your benefits, and what the buyer's first day onboarding will look like. The buyers who handle this well keep more of the team. The ones who ignore it often see a wave of departures in the first 60 days.

When a Buyer Plans to Make Changes: How to Handle It Honestly

Some buyers will acquire your business and change very little. Others have a clear plan to restructure. If you know a buyer intends to cut staff, change roles, or shift the business model significantly, you need to handle that knowledge carefully.

As a seller, you're not required to tell employees exactly what the buyer plans to do. But you shouldn't actively mislead them either. If a buyer has told you they plan to eliminate two of your five positions, you can't ethically tell your employees "everything will stay the same."

The right approach is to tell employees what you know: that the business is being sold, that the buyer is planning to continue operations, and that more information will come directly from the buyer. You don't have to predict or explain the buyer's future decisions. But you shouldn't promise things you know aren't true.

If a buyer is planning substantial changes, encourage them to be honest with employees about it during the transition period. Employees who understand what's happening and why are far more likely to cooperate with the transition, even if they're being laid off. For buyers, how they handle the first 90 days after acquisition sets the tone for everything that follows.

What Sellers Should Disclose Versus What Stays Confidential Until Closing

The confidentiality question cuts both ways. Sellers have obligations to keep deal information confidential during the process. Employees have interests in knowing what's happening to their jobs.

| Information | Keep Confidential Until | Disclose To Employees When |

|---|---|---|

| Business is for sale | Signed purchase agreement | After agreement is signed |

| Buyer's identity | Buyer consents to disclosure | After buyer gives consent |

| Purchase price and deal terms | Closing (or never) | Generally not disclosed to employees |

| Employment plans | Buyer finalizes their plan | After buyer provides their staffing plan |

| Benefits and HR changes | Details are confirmed | During the transition period before closing |

What Buyers Expect From Sellers on Disclosure

Good buyers want employees informed and prepared. They don't want to inherit a team that's blindsided on day one. Work with your buyer to coordinate a joint announcement that you present together, ideally with you expressing confidence in the new owner and the buyer expressing commitment to the team.

This is one of the things that separates clean transitions from messy ones. It doesn't cost anything extra and it dramatically affects the early days of the new ownership.

Thinking about selling and want to see what the full process looks like? Read our post on whether to use a business broker to sell your business to understand how to protect both yourself and your employees through the process.

Common Mistakes Sellers Make with Employees

I see the same patterns repeat. Here's what not to do.

Telling employees too early. I've seen deals fall apart after the seller told their team, leaving employees anxious for months until the seller found another buyer. Keep it confidential until you have a signed agreement.

Promising things you can't guarantee. "Your job is safe" is not yours to promise. "The buyer intends to keep the team" is accurate. Choose your words carefully.

Ignoring accrued PTO and benefits. Failing to address this in the purchase agreement creates real animosity with employees on day one. Pay out what you owe or negotiate a clear plan.

Skipping the joint announcement. Sellers who disappear and let the buyer handle communication leave employees feeling abandoned and confused. Stay involved in the announcement and transition, even if it's just for the first week.

Not identifying key employees early. Finding out during due diligence that the business can't run without someone who's not under contract and not committed to staying is a deal killer. Know your key people before you go to market and secure them before you start the sale process.

The sellers who handle employees well during a sale protect their deal value, their reputation, and their people. The ones who ignore it often see departures in the first 60 days and a deal that underperforms.

What To Do Next

If you're preparing to sell and you have employees, take these steps before you go to market.

First, identify your one to three key employees and think through what would happen if they left during the sale process. Second, review what accrued PTO and benefit obligations exist and decide how you'll handle them at closing. Third, talk to your attorney about non-compete agreements and whether any need to be updated. Fourth, plan your disclosure timeline so you're telling employees at the right moment, not too early and not too late. You can also use our business valuation calculators to understand what your business is worth before you start the process.

Most importantly, treat this process the way you'd want to be treated if you were the employee. Your reputation in your community and industry outlasts any single transaction.

If you're thinking about selling, start with our seller resources.

Ready to talk through the employee side of your business sale? Contact us for a free consultation and we'll help you think through the human side of the transaction before it becomes a problem.

For a full walkthrough of every stage of the selling process, including how to handle employees, download our free Complete Guide to Selling Your Business in 2026.

FAQ

Are employees automatically transferred when a business is sold? In a stock sale, yes. The legal entity continues and existing employment relationships carry over. In an asset sale, which is more common, employment relationships technically end and the buyer hires employees as new hires. In practice, most buyers offer employment to current staff as part of the deal.

Can I promise my employees their jobs are safe? You can tell them the buyer intends to retain the team, but you can't guarantee employment on behalf of the buyer. Making that promise exposes you to liability if the buyer later makes changes.

What happens to accrued vacation when a business is sold? This is negotiated in the purchase agreement. Sellers often pay out accrued PTO at or before closing to clear the liability. If you don't address it, the buyer may not honor accrued balances, which creates a real problem on day one.

When should I tell my employees the business is being sold? After you have a signed purchase agreement, ideally two to four weeks before closing. Telling them too early creates anxiety and can blow up the deal if it falls through.

What is a retention bonus and should I offer one? A retention bonus pays key employees a lump sum if they stay employed for a defined period, typically six to twelve months after closing. It protects the deal value by keeping critical people in place during the transition. Most buyers and sellers split the cost. It's almost always worth it.

Do employees have to sign new employment agreements after a sale? The buyer can require new employment agreements, and often does for key employees. These may include non-compete clauses, confidentiality agreements, or new compensation terms. This is standard in acquisition transactions.

Related Articles

April 16, 2026

Preparing Your Business for Sale: The 12 Month Checklist

The best time to start preparing your business for sale is 12 months out. Here's exactly what to do each quarter.

April 12, 2026

How to Handle Multiple Offers on Your Business

Multiple offers are a great problem to have. But picking the wrong one can cost you months and thousands. Here's how to evaluate them.

April 9, 2026

Best Time of Year to List Your Business for Sale

Timing your listing right can mean more buyers, better offers, and a faster close. Here's what the data says about when to go to market.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.