You've accepted an offer on your business. The letter of intent is signed. You're feeling a mix of relief and excitement. But then your broker or attorney says, "Now we open escrow," and you realize you have no idea what that actually means.

You're not alone. Most business sellers have never been through escrow before. It's the part of the deal where everything either comes together or falls apart, and yet nobody really explains what's happening behind the scenes. I've walked dozens of sellers through this process, and I can tell you that understanding escrow before you're in it makes everything less stressful.

Here's exactly what happens, step by step, from the moment escrow opens to the day you hand over the keys.

What Escrow Actually Is (And Why It Exists)

Escrow is a neutral holding period where a third party manages the transfer of money, documents, and assets between buyer and seller. Think of the escrow agent as a referee. They don't work for you, they don't work for the buyer. They work for the deal.

The escrow agent holds the buyer's deposit, collects all required documents, makes sure every condition in the purchase agreement gets met, and then coordinates the final closing. They release funds to the seller only when every requirement has been satisfied.

Why does this exist? Because neither party should have to trust the other blindly. The buyer doesn't want to hand over $300,000 before confirming the business is what you said it is. And you don't want to hand over your customer list and trade secrets before confirming the buyer actually has the money. Escrow protects both sides.

In most business sales, escrow lasts 30 to 60 days. SBA financed deals can stretch to 75 or even 90 days because the lender adds its own requirements. Cash deals sometimes close in as little as 21 days, but that's rare.

The biggest mistake I see sellers make is treating escrow as someone else's problem. The escrow agent manages the process, but you are the one who controls the pace. Every document you delay, every phone call you dodge, every question you leave unanswered adds days to your timeline and gives the buyer more time to reconsider.

Who's Involved in the Escrow Process

A surprising number of people need to coordinate during escrow. Here's who's at the table and what they do.

The escrow agent or escrow company. This is the neutral third party managing the process. In business sales, this is often a specialized business escrow company, not the same kind of escrow you'd use for a house. They hold deposits, prepare closing documents, handle funds disbursement, and file required notices.

Your attorney. Reviews every document before you sign it and negotiates any changes to the purchase agreement that come up during due diligence. Makes sure you're not agreeing to something that could bite you later, like an overly broad non compete.

The buyer's attorney. Same role, opposite side. Good attorneys on both sides actually make deals close faster because they resolve issues instead of creating them.

The buyer. They're doing the bulk of the work during escrow, reviewing your financials, talking to your landlord, inspecting equipment, and securing financing.

The lender (if applicable). About 70% of small business acquisitions involve SBA financing. The lender has its own checklist of requirements, and they won't fund until every box is checked. This is the single biggest source of escrow delays.

The landlord. If your business operates from a leased location, the landlord needs to approve the lease assignment or negotiate a new lease with the buyer. I've seen more deals delayed by landlords than by any other single factor.

The franchisor (if applicable). Franchise transfers require franchisor approval, which can add 30 to 60 days on top of the normal escrow timeline.

Your business broker. That's where I come in. I coordinate between all these parties, chase down missing documents, and keep everyone moving toward the closing date. A good broker is basically a project manager for the entire escrow period.

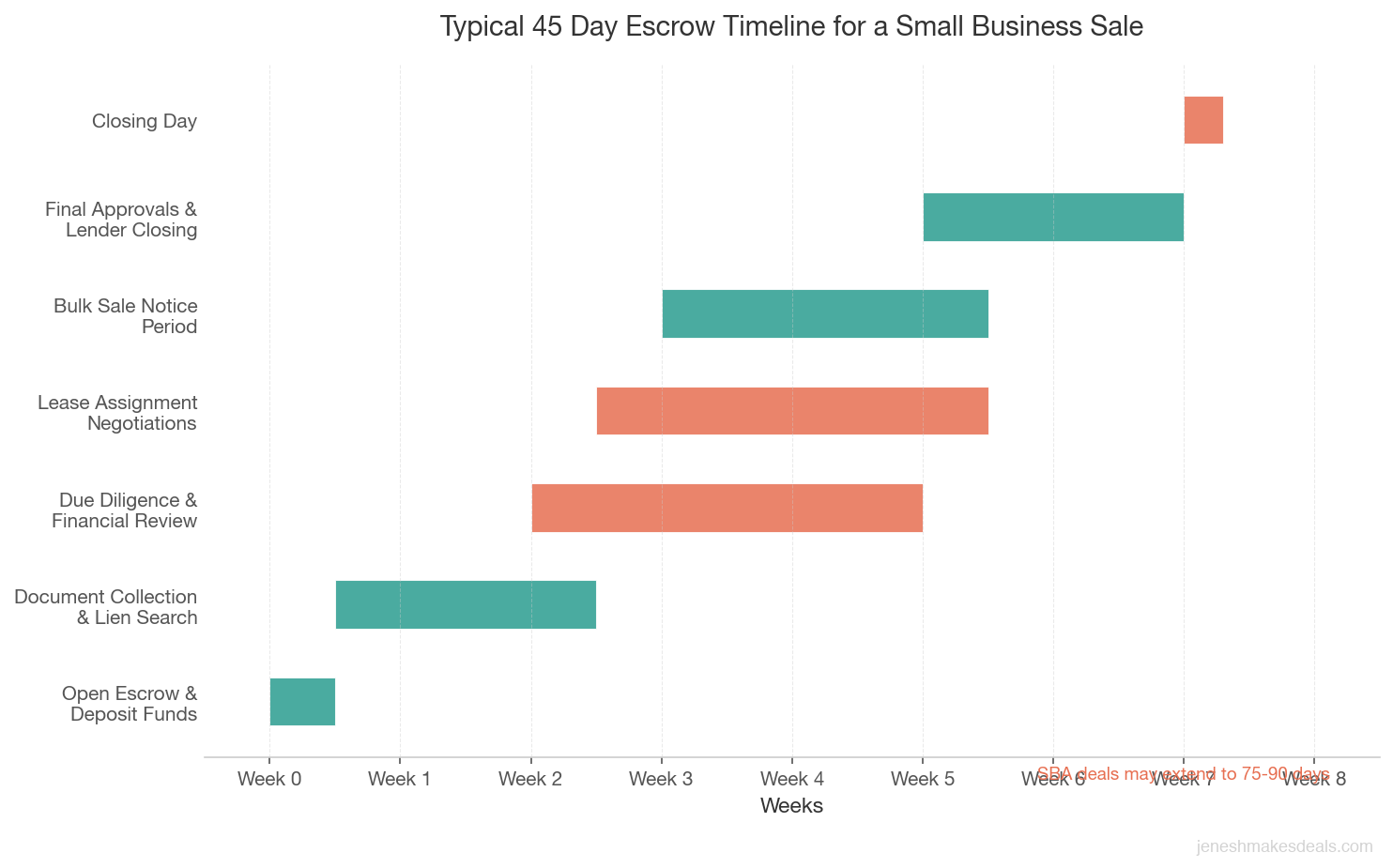

The Escrow Timeline: What Happens Week by Week

Let me break down a typical 45 day escrow for a small business sale in the $200,000 to $2,000,000 range.

Weeks 1 and 2: Opening and Document Collection

Day 1 starts when the escrow agent receives the fully executed purchase agreement and the buyer's earnest money deposit. The escrow agent opens a file, assigns a number, and sends both parties an escrow instruction letter outlining every condition that must be met before closing.

During these first two weeks, here's what's happening:

- The buyer deposits earnest money (typically $5,000 to $50,000 depending on deal size, usually 5% to 10% of the purchase price)

- The escrow agent orders a lien search through the Secretary of State's office (UCC search)

- You start gathering documents the buyer needs for due diligence: three years of tax returns, profit and loss statements, balance sheets, equipment lists, customer contracts, vendor agreements, employee records, and lease documents

- If SBA financing is involved, the lender issues a commitment letter and sends their own list of required documents

- The buyer's due diligence period formally begins

I always tell sellers to have their document package ready before escrow opens. If a buyer asks for your tax returns on day one and you need two weeks to get them from your accountant, you've already burned through half the due diligence period.

Weeks 3 and 4: Due Diligence and Negotiations

This is the most intense part of escrow. The buyer is deep in your financials, and questions are coming fast.

- The buyer reviews your books and records, often with their accountant

- Lease assignment negotiations begin with the landlord

- The buyer may request adjustments to the purchase price based on what they find (this happens in about 30% of deals I handle)

- If the business requires licenses or permits, the buyer starts the application process

- The bulk sale notification goes out (more on this below)

- The lender orders an independent business appraisal (SBA deals)

- Equipment inspections happen

- The buyer may spend time in the business, observing operations

This is where deals get tense. The buyer might find that your revenue dropped 15% last quarter, or that a key employee is planning to leave, or that the roof needs $40,000 in repairs. Each discovery triggers a conversation, and sometimes a renegotiation.

My advice: be honest about everything upfront. I've seen sellers try to hide a bad month or a pending lawsuit, and it always comes out during due diligence. When it does, the buyer loses trust, and trust is the currency of every deal.

If a buyer finds something during due diligence that you didn't disclose, the price reduction they demand will always be larger than the hit you would have taken by being upfront. Surprises kill deals. Honesty renegotiates them.

Weeks 5 Through 8: Final Approvals and Closing

If due diligence goes well, the final weeks are about checking boxes and preparing for the handoff.

- The lender issues final loan approval and prepares closing documents

- The landlord signs the lease assignment or new lease

- License and permit transfers are finalized (or at least in process)

- The escrow agent prepares the closing statement showing exactly how funds will be distributed

- Both parties review and sign closing documents

- The buyer secures business insurance (required before closing)

- Final walk through of the business premises

- The seller prepares a transition plan and training schedule

- Funds are wired to the escrow agent

- Closing day: everyone signs, funds are released, keys change hands

The closing statement is one of the most important documents you'll see. It breaks down every dollar: purchase price, prorations for rent and utilities, escrow fees, broker commissions, lien payoffs, and the net amount you'll receive. Review it carefully with your attorney at least 48 hours before closing.

Wondering what your business might actually sell for? Get a data backed estimate with our free business valuation calculator.

What Goes Into Escrow: Deposits and Documents

The Earnest Money Deposit

The buyer's earnest money deposit is the first thing that goes into escrow. This is their way of saying, "I'm serious about this deal." Here's what you should know about it:

- Typical range: $5,000 to $50,000 for businesses selling under $2 million

- Percentage: Usually 5% to 10% of the purchase price

- Timing: Deposited within 3 to 5 business days of opening escrow

- Who holds it: The escrow agent, not you and not the buyer's broker

- Refundability: Usually refundable during the due diligence period, non refundable after contingencies are removed

For a $500,000 business sale, I typically see earnest money deposits of $25,000 to $50,000. For a $200,000 deal, $10,000 to $20,000 is standard. If a buyer offers less than 5%, it can be a sign they're not fully committed. I always push for at least 10% because it keeps the buyer engaged and less likely to walk away over minor issues.

The Document Package

Here's what you'll need to provide during escrow. Start pulling this together the moment you decide to sell:

- Federal and state tax returns (3 years)

- Monthly profit and loss statements (3 years)

- Balance sheets (3 years)

- Bank statements (12 months minimum)

- Equipment list with approximate values

- Current lease and any amendments

- Customer contracts and recurring revenue documentation

- Vendor and supplier agreements

- Employee list with compensation details

- Insurance policies

- Business licenses and permits

- Franchise agreement (if applicable)

- Any pending or past litigation

- Accounts receivable and accounts payable aging reports

- Inventory list with values (if applicable)

Missing even one of these can delay closing by a week or more. I had a deal last year where the seller couldn't locate their original franchise agreement. It took three weeks to get a copy from the franchisor, which pushed the closing date back and nearly cost us the deal because the buyer's rate lock was about to expire.

Due Diligence During Escrow

Due diligence is the buyer's investigation period, and it happens inside escrow. This is where the buyer verifies that everything you represented about the business is accurate.

Financial Review

The buyer (or their accountant) will go through your financials with a fine tooth comb. They're looking for:

- Revenue trends (growing, flat, or declining)

- Profit margins and whether they're consistent

- Owner add backs and discretionary expenses

- One time expenses that inflate or deflate true earnings

- Customer concentration (if one customer is 40% of revenue, that's a red flag)

- Seasonality patterns

- Tax return consistency with your P&L statements

A common sticking point: the numbers on your tax returns don't match your internal financial statements. This happens more often than you'd think, and it always raises questions. Make sure your accountant can explain any discrepancies before the buyer asks.

Lease Assignment

If your business has a physical location, the lease is often the most critical piece of the deal. Here's what happens:

- The buyer or their attorney contacts the landlord to request a lease assignment

- The landlord reviews the buyer's financial qualifications

- Negotiations happen around any lease modifications (rent increase, term extension, personal guarantee requirements)

- The landlord signs a consent to assignment or issues a new lease

Some landlords see a business sale as an opportunity to raise rent by 10% to 20%. Others require a larger security deposit from the new tenant. I always recommend sellers give their landlord a heads up early in the process. A cooperative landlord can shave two weeks off your escrow timeline.

License and Permit Transfers

Depending on your industry, this can be simple or extremely complicated:

- Liquor licenses: Can take 30 to 90 days to transfer. In some states, you need to apply for a new license entirely. This is often the longest lead item in a restaurant or bar sale.

- Health permits: Usually transferred at closing or shortly after with a new inspection

- Contractor licenses: Often tied to a specific individual, so the buyer may need their own

- Professional licenses: Cannot be transferred. The buyer must have their own.

- Business operating permits: Usually transferred with a simple application and fee ($50 to $500)

Thinking about selling your business? Let's talk about your specific situation and what the escrow process would look like for your industry. Schedule a free consultation.

The Bulk Sale Notification Process

This one catches a lot of sellers off guard. In many states, when you sell a business, you're required to publish a notice of the sale under the Uniform Commercial Code (UCC) bulk sale provisions. The purpose is to protect your creditors by giving them notice that the business assets are being transferred.

Here's how it works:

- The escrow agent publishes a Notice to Creditors of Bulk Transfer in a local newspaper (yes, an actual print newspaper)

- The notice runs for a specified period, usually 12 business days in California

- Creditors have a window to file claims against the business assets

- The escrow agent holds funds to cover any valid claims

- After the notice period expires with no claims (or after claims are resolved), escrow can close

This process adds about 2 to 3 weeks to the escrow timeline. Some states have repealed their bulk sale laws. California still has them, and they apply to most business sales. Your attorney can tell you whether bulk sale requirements apply in your state.

The cost of the newspaper publication is typically $150 to $400, and it's usually charged to the escrow. Some purchase agreements specify that the buyer pays for it, others say the seller. It's a small number, but make sure it's addressed in your agreement.

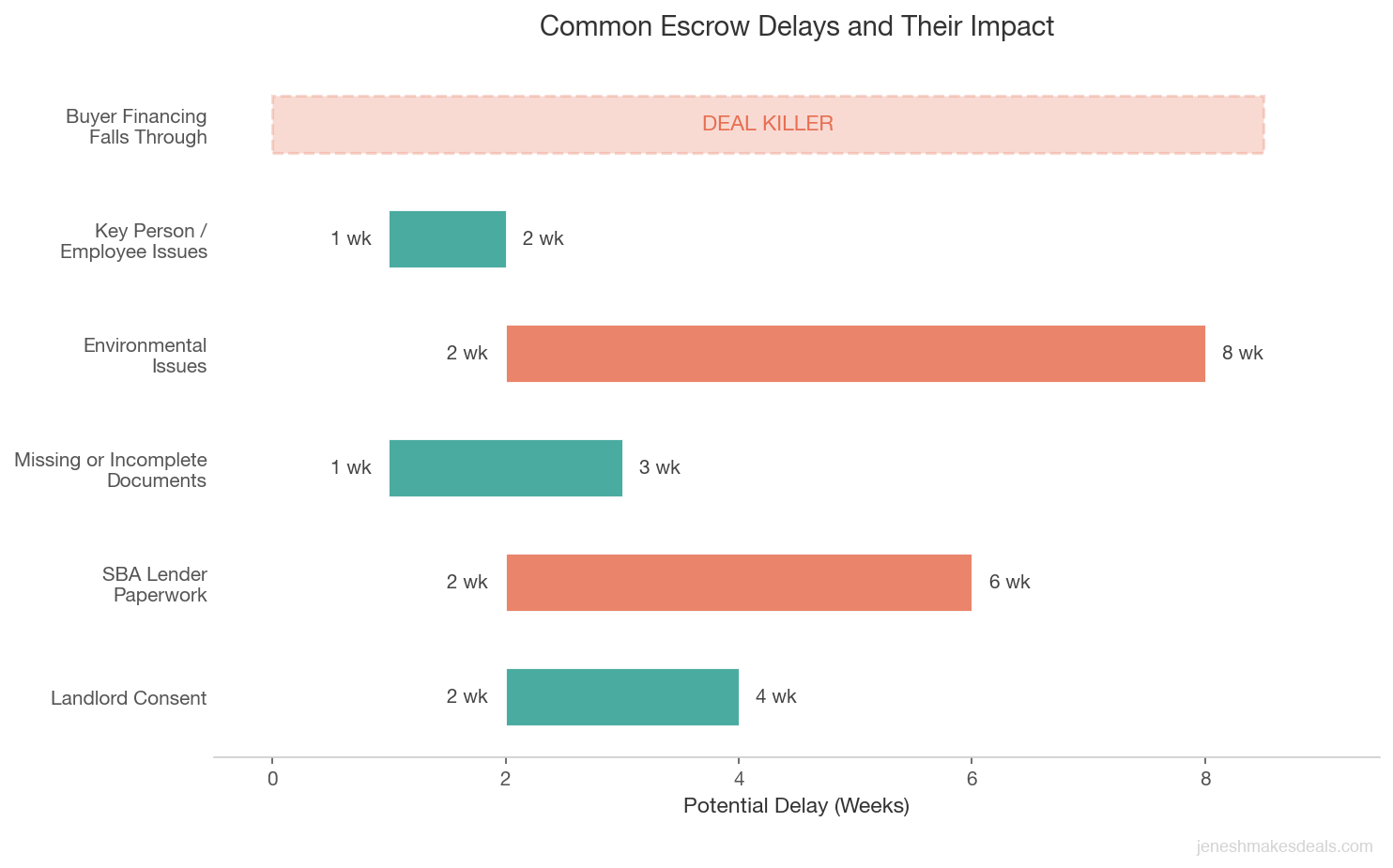

Common Escrow Delays and How to Prevent Them

I've seen dozens of escrows delayed, and the causes are almost always predictable. Here are the most common culprits and how to avoid them.

Landlord Consent (2 to 4 Week Delay)

The problem: The landlord is slow to respond, demands unreasonable lease modifications, or flat out refuses to approve the assignment.

The prevention: Talk to your landlord before you list your business. Let them know a sale is possible. Ask what their requirements would be for a new tenant. Get any verbal assurances in writing if you can. I've seen landlords demand $50,000 lease buyouts that killed deals entirely.

SBA Lender Paperwork (2 to 6 Week Delay)

The problem: The SBA lender has a mountain of requirements: environmental reviews, business appraisals, insurance requirements, personal financial statements, and more. Each document request triggers another round of back and forth.

The prevention: If your buyer is using SBA financing, build at least 60 days into your escrow timeline. Provide every document the lender requests within 48 hours. Delays compound quickly. One missing document can push closing back by 10 days.

Missing or Incomplete Documents (1 to 3 Week Delay)

The problem: You can't find your original lease, your tax returns have discrepancies, or you don't have documentation for equipment you claim to own.

The prevention: Build your document package months before going to market. Work with your accountant to reconcile any differences between tax returns and financial statements. Create a clean equipment inventory with photos, serial numbers, and approximate values.

Environmental Issues (2 to 8 Week Delay)

The problem: The SBA requires a Phase I environmental assessment for many deals. If it uncovers potential contamination, a Phase II assessment (actual soil and water testing) is needed.

The prevention: If your business involves auto repair, dry cleaning, gas stations, or manufacturing, get a Phase I done before listing. It costs $2,000 to $4,000 but can prevent a much longer delay during escrow.

Buyer's Financing Falls Through (Deal Killer)

The problem: The buyer's loan gets denied, often because of credit issues, insufficient collateral, or a business appraisal that comes in lower than the purchase price.

The prevention: Require a lender pre qualification letter before accepting an offer. Better yet, require a commitment letter within the first 10 days of escrow. If the buyer can't get one, you haven't wasted 60 days.

Employee or Key Person Issues (1 to 2 Week Delay)

The problem: A key employee learns about the sale and threatens to leave, or the buyer discovers that the business is overly dependent on you personally.

The prevention: Have a transition plan ready. Show the buyer that the business can run without you. If you have key employees, consider retention bonuses tied to the sale. And for the love of all that is holy, don't tell your employees about the sale until it's absolutely necessary.

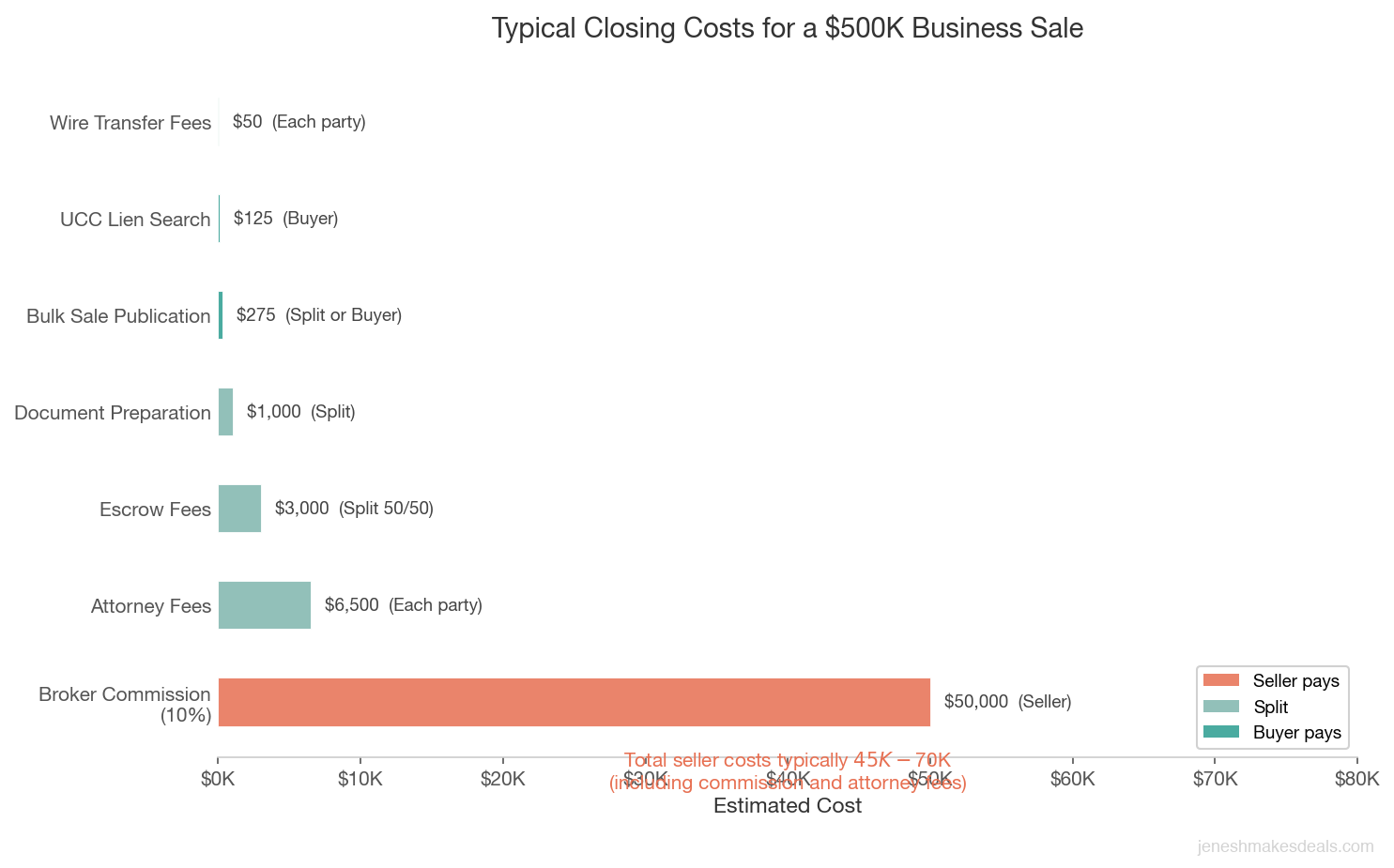

Escrow Costs: Who Pays What

Escrow isn't free. Here's what you can expect:

Escrow fees: $2,000 to $5,000 depending on the deal size and complexity. For a $500,000 business sale, expect around $2,500 to $3,500.

How fees are typically split:

- 50/50 between buyer and seller (most common)

- Buyer pays 100% (sometimes negotiated)

- Seller pays 100% (less common)

The fee structure is usually outlined in the purchase agreement. Don't wait until closing to find out who's paying.

Additional costs that come through escrow:

| Cost | Typical Range | Who Usually Pays |

|---|---|---|

| Escrow fees | $2,000 to $5,000 | Split 50/50 |

| Bulk sale publication | $150 to $400 | Split or buyer |

| UCC lien search | $50 to $200 | Buyer |

| Document preparation | $500 to $1,500 | Split |

| Wire transfer fees | $25 to $50 per wire | Each party |

| Broker commission | 8% to 12% of sale price | Seller |

| Attorney fees | $3,000 to $10,000 each | Each party |

For a $500,000 business sale, the total closing costs for the seller typically run $45,000 to $70,000 when you include the broker commission and attorney fees. The escrow specific costs are a relatively small portion of that total.

Not sure what your business is worth after closing costs? Run the numbers with our seller's discretionary earnings calculator to see your true bottom line.

What Happens If the Deal Falls Through During Escrow

Not every deal closes. About 20% to 30% of business sales that enter escrow end up falling apart. Here's what happens when they do.

During the Due Diligence Period

If the buyer backs out during the contingency period (typically the first 15 to 30 days), they usually get their full earnest money deposit back. This is the most common time for deals to die. Reasons include:

- Financials don't match what was represented

- The lease can't be assigned on acceptable terms

- The buyer's financing falls through

- The buyer discovers undisclosed liabilities

- The buyer simply gets cold feet (it happens)

After Contingencies Are Removed

If the buyer backs out after removing contingencies, you may be entitled to keep the earnest money deposit as liquidated damages. The purchase agreement should spell out exactly what happens in this scenario. In most deals I structure, the deposit becomes non refundable once the due diligence period ends.

But here's the reality. Even if you're legally entitled to the deposit, you might end up negotiating. If the buyer's SBA loan gets denied at the last minute due to something outside their control, keeping their $30,000 deposit might feel right on principle, but it won't get your business sold. Sometimes a partial refund and a quick return to market is the smarter play.

Cancellation Process

When a deal falls through, here's what happens:

- One party sends a cancellation notice to the escrow agent

- Both parties sign cancellation instructions

- The escrow agent returns the deposit according to the agreement terms

- If there's a dispute over the deposit, the escrow agent holds the funds until both parties agree or a court decides

If both parties can't agree on who gets the deposit, the escrow agent won't release it to either side. I've seen $25,000 deposits stuck in escrow limbo for over a year while attorneys sort it out.

Write your cancellation and deposit terms as if the deal will fall apart, because one in four does. The time to negotiate what happens with the earnest money is before escrow opens, not after both sides are angry and lawyered up.

Tips for Sellers to Keep Escrow on Track

After years of guiding sellers through escrow, here's my playbook for a smooth close.

Respond to document requests within 24 hours. Every day you delay sending a document is a day added to your escrow timeline. Set aside time every morning during escrow to check for requests and respond immediately.

Keep running your business at full speed. I cannot stress this enough. The worst thing you can do during escrow is mentally check out. If revenue drops during escrow, the buyer will notice, and they'll either renegotiate or walk away. I had a seller who stopped marketing his business during escrow. Revenue dropped 25% in two months, and the buyer reduced their offer by $150,000.

Don't make major changes. Now is not the time to fire an employee, sign a new vendor contract, or buy a $50,000 piece of equipment. Any material change to the business during escrow can trigger a renegotiation or give the buyer a reason to back out.

Stay in close contact with your broker. Your broker should be giving you weekly updates on escrow progress. If you're not hearing from them, call them. No news during escrow is rarely good news.

Be available for the buyer. The buyer will want to visit the business, meet key employees (at the right time), and ask you questions. Be responsive and open. The more comfortable the buyer feels, the less likely they are to look for reasons to back out.

Prepare your transition plan early. Buyers want to know you'll help them succeed after closing. A written transition plan that includes 2 to 4 weeks of training, customer introductions, and vendor relationship handoffs shows the buyer you're committed to a successful transfer.

Have your accountant on standby. Your CPA will need to answer questions, provide documents, and possibly write a letter confirming certain financial representations. Give them a heads up that you're in escrow and may need quick turnaround on requests.

Budget for surprises. Keep $5,000 to $10,000 set aside for unexpected costs that come up during escrow. Whether it's an equipment repair, a required permit renewal, or an attorney fee you didn't anticipate, having a buffer prevents panic.

Want expert guidance through every stage of your sale? I help business owners prepare for and manage the entire escrow process. Let's talk about your business.

Closing Day: What to Expect

Closing day itself is usually anticlimactic compared to the weeks of work that preceded it. The escrow agent confirms all funds have been received, both parties sign the bill of sale, assignment agreements, non compete, and any promissory notes. Keys, alarm codes, and passwords change hands. Funds are disbursed per the closing statement within 24 to 48 hours.

One important note: you probably won't receive all the money on closing day. If there's a seller's note (common in 60% to 70% of small business sales), you'll receive a portion at closing and the rest over 2 to 5 years. If there's a holdback for working capital adjustments, 5% to 10% of the purchase price may be held in escrow for 60 to 90 days after closing.

Make Escrow the Easiest Part of Your Sale

Escrow doesn't have to be a black box. When you understand the process, prepare your documents in advance, and stay engaged throughout, it becomes a manageable series of steps rather than a source of stress.

The sellers who have the smoothest escrow experiences are the ones who prepare before they go to market. They have clean financials, good relationships with their landlords, organized records, and realistic expectations about timelines and costs.

If you're thinking about selling your business and want to make sure you're ready for escrow and everything that comes before it, I'd love to help.

Ready to start planning your exit? Get in touch for a free, confidential consultation and we'll map out exactly what your escrow process will look like.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.