Roughly half of all business deals that go under contract never make it to the closing table.

That number shocks most sellers when they hear it for the first time. They've found a buyer, signed a letter of intent, maybe even popped a bottle of champagne. Then the deal crumbles. Weeks or months of effort vanish, and they're back to square one with a stale listing and bruised confidence.

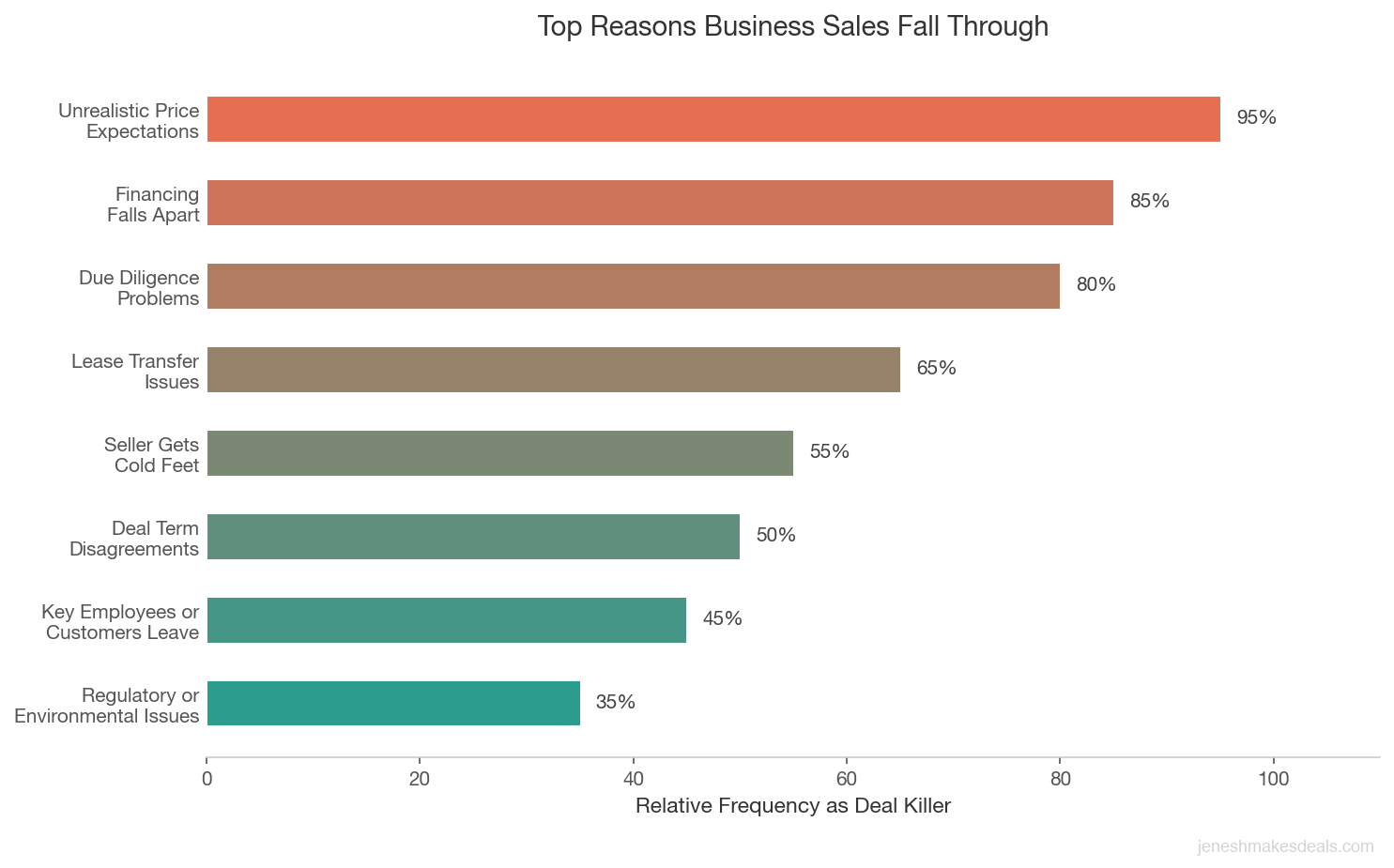

I've brokered enough deals to know that most of these failures are preventable. The same problems show up over and over again. Price disagreements. Financing gaps. Surprises in due diligence. Lease issues. Cold feet. If you know what kills deals, you can take steps to protect yours before it ever hits the market.

Here are the eight most common reasons business sales fall through and exactly what you can do about each one.

The Brutal Reality: Why So Many Deals Die

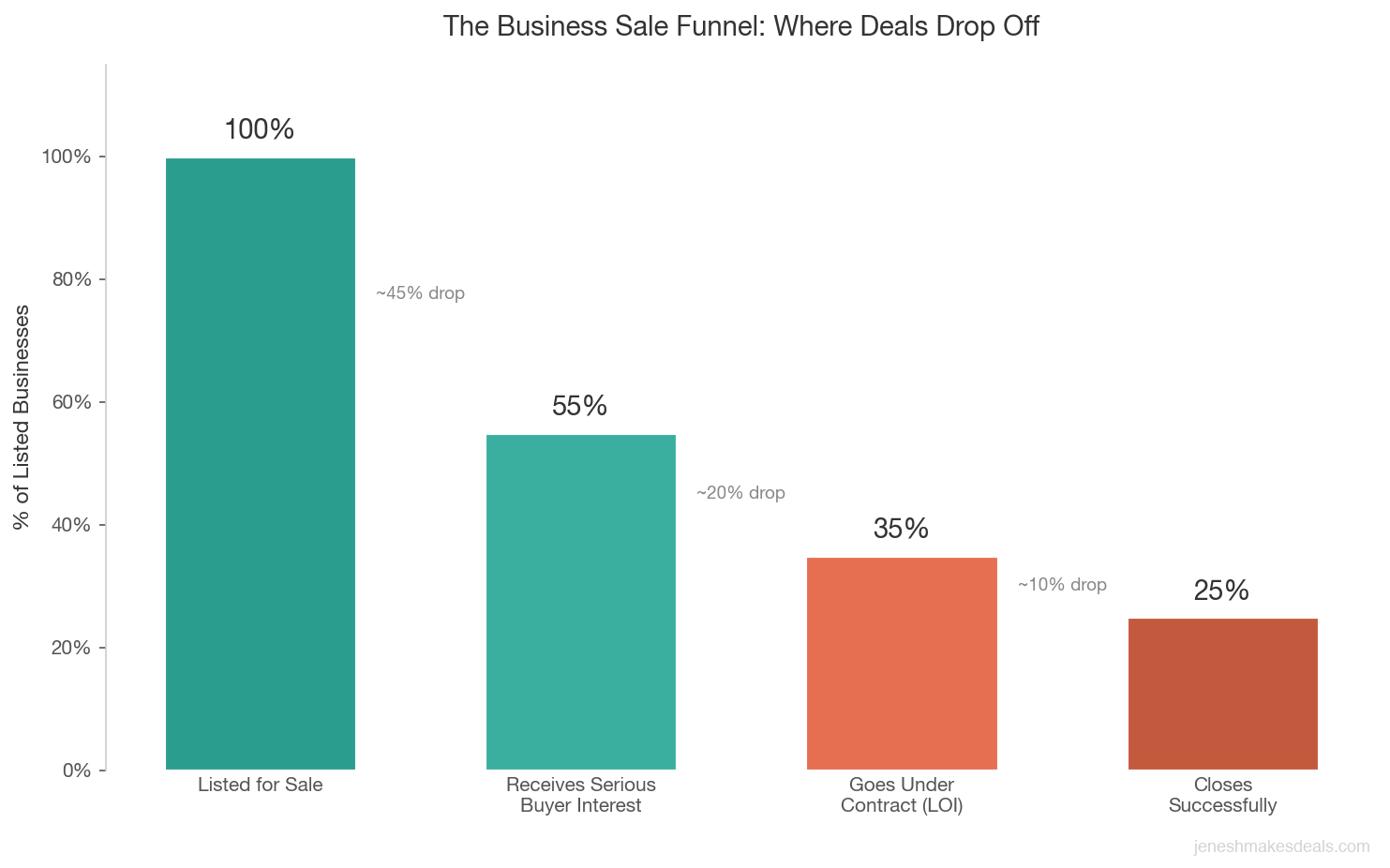

Before we get into specifics, let's talk about the numbers. Industry data from BizBuySell and the International Business Brokers Association consistently shows that only about 20 to 30% of listed businesses actually sell. Of those that attract a buyer and go under contract, roughly 40 to 50% still fail to close.

That means the odds are stacked against you from the start. But here's the thing: the sellers who close successfully aren't lucky. They're prepared.

| Deal Stage | Approximate Success Rate |

|---|---|

| Business listed for sale | 100% |

| Receives serious buyer interest | 50 to 60% |

| Goes under contract (LOI signed) | 30 to 40% |

| Closes successfully | 20 to 30% |

Every stage is a filter. And at every stage, specific problems knock deals out. Let me walk you through each one.

Reason 1: Unrealistic Price Expectations

This is the number one deal killer. It's not even close.

I worked with a restaurant owner named Marco who turned down a $400,000 offer because he believed his business was worth $600,000. His reasoning? He'd invested over $500,000 in buildout costs and equipment over the years, plus "sweat equity." But the market doesn't care about sunk costs. The business was generating $150,000 in seller's discretionary earnings, and restaurants in his area were trading at 2.5 to 2.8x SDE. That put fair market value right around $375,000 to $420,000.

Marco rejected the offer. Nine months later, revenue had dropped because he'd mentally checked out and stopped investing in the business. He ended up selling for $320,000.

The gap between what sellers think their business is worth and what buyers will actually pay is the single biggest reason deals never happen. The market sets the price, not your retirement goals.

Sellers anchor on what they need for retirement, what they've invested over the years, or what they heard a competitor sold for. Buyers anchor on cash flow, risk, and market comparables.

How to prevent it:

- Get a professional valuation before listing, not after you've already rejected two offers

- Use SDE multiples specific to your industry, not generic rules of thumb

- Accept that the market sets the price, not your retirement goals

- Look at actual closed transactions in your industry, not asking prices

Not sure what your business is actually worth? Use our free valuation calculators to get a data driven estimate based on real industry multiples.

Reason 2: Financing Falls Apart

Even when buyer and seller agree on price, the money has to come from somewhere. And financing is where a huge number of deals go to die.

About 75% of small business acquisitions under $5 million involve SBA lending. SBA loans are great for buyers because they offer long repayment terms and relatively low down payments (typically 10 to 20%). But SBA approval is not guaranteed, and the process is full of landmines.

Common financing failures I've seen:

- Buyer doesn't qualify. The buyer's credit score is too low, they lack sufficient liquid assets for the down payment, or they don't have relevant industry experience. SBA lenders care about all three.

- The business doesn't qualify. The business has declining revenue, messy books, or cash heavy transactions that can't be verified. Lenders need to see that the business can service the debt, and they use strict debt service coverage ratios (typically 1.25x or higher).

- Appraisal comes in low. The lender orders a third party business appraisal and it comes back below the purchase price. Now there's a gap that somebody has to fill.

- The process takes too long. SBA loans can take 60 to 90 days to close. During that time, the business might hit a slow month, the buyer might get nervous, or the seller might lose patience.

I had a deal for a printing company last year where the buyer was prequalified, the LOI was signed, and everything looked solid. Then the SBA lender's appraiser valued the business at $380,000 against a $450,000 purchase price. The buyer couldn't bridge the $70,000 gap. We spent three weeks negotiating a revised price and restructured the deal with a $40,000 seller note. It closed, but it almost didn't.

How to prevent it:

- Only accept offers from buyers who provide proof of funds or a lender prequalification letter

- Keep your books clean and up to date so the underwriting process goes smoothly

- Be prepared to offer a seller note for 10 to 20% of the purchase price, which actually makes your deal more attractive to lenders

- Set realistic timelines that account for the SBA lending process

Want to understand how SBA financing works for your deal? Try our SBA loan calculator to see what a buyer's monthly payments would look like.

Reason 3: Due Diligence Uncovers Problems

Due diligence is the buyer's opportunity to verify everything you've told them about your business. It's supposed to confirm the deal. But too often, it's where the deal goes off the rails.

The problems I see most frequently during due diligence fall into three categories.

Undisclosed liabilities. A buyer finds out the business has pending litigation, unpaid taxes, outstanding vendor disputes, or warranty claims that the seller didn't mention. I had a buyer walk away from a service company deal after discovering $80,000 in unpaid payroll taxes that the seller had "forgotten" to mention. That's not something you forget. It destroyed the trust, and the deal was dead.

Declining revenue trends. The financials looked great at first glance, but the trailing six months showed a clear downward trend. Maybe a major customer left, a competitor opened nearby, or the seller stopped marketing. Buyers are buying the future, not the past. If the trend line is going the wrong direction, they'll either renegotiate hard or walk.

Customer concentration. If one customer accounts for more than 20 to 25% of revenue, that's a massive risk flag. I've seen deals collapse when the buyer's lender refused to finance a business where a single customer represented 40% of sales. What happens if that customer leaves after the sale? The buyer is stuck with a loan they can't service.

How to prevent it:

- Disclose everything upfront, even the ugly stuff. Buyers will find out eventually, and finding out during due diligence is way worse than hearing it in the first meeting

- Address customer concentration before going to market by diversifying your client base

- Fix any tax, legal, or compliance issues before listing

- Prepare a due diligence package with organized financials, contracts, leases, and employee records so the process moves fast and clean

Reason 4: The Landlord Won't Transfer the Lease

This one blindsides sellers constantly. You can have a fully financed buyer, a signed purchase agreement, and a clean due diligence process. But if your business operates from a leased location and the landlord refuses to assign the lease or negotiate acceptable terms with the buyer, the deal is dead.

I worked with a buyer named Sarah who was purchasing a yoga studio in Brooklyn. Everything was perfect. The business was profitable, the asking price was fair, the financing was approved. Then the landlord decided he wanted to raise the rent by 40% as a condition of the lease assignment. The math didn't work at the new rent, and the buyer walked.

Common lease problems that kill deals:

- Landlord refuses to assign the lease to the new owner

- Landlord demands a significant rent increase as a condition of assignment

- The remaining lease term is too short (less than 3 to 5 years), and the landlord won't extend

- The lease has a demolition clause or personal guarantee requirements that scare off the buyer

- SBA lenders typically require a remaining lease term that matches the loan term (usually 10 years)

How to prevent it:

- Review your lease's assignment clause before listing your business

- Talk to your landlord early. Not after you have a buyer, but before you go to market

- Negotiate a lease extension or renewal option before listing

- If your landlord is difficult, factor that into your asking price and be transparent with buyers

- Consider whether your business could relocate if the lease situation is truly toxic

Dealing with a tricky lease situation? Let's talk about your options before it becomes a deal breaker.

Reason 5: The Seller Gets Cold Feet

Selling a business is an emotional experience. Sellers build these businesses from nothing. They've poured years of their life, their savings, and their identity into them. When the moment comes to actually sign the papers, some sellers just can't do it.

Backing out of a signed deal doesn't just kill the transaction. It can expose you to legal liability and will almost certainly burn the bridge with that buyer forever.

I've seen this happen more times than I'd like to admit. The seller starts second guessing the decision. They wonder if they're selling too cheap. They worry about what they'll do with their time after the sale. They feel guilty about "abandoning" their employees. They convince themselves the business will be worth more in two years if they just hold on.

One seller, a woman who ran a successful bookkeeping firm for 15 years, backed out of a deal three days before closing. The buyer had already given notice at his corporate job. The earnest money was at risk. She called me in tears and said she just wasn't ready. We managed to negotiate a 90 day extension, and she eventually closed. But it almost cost her the deal and a lawsuit.

How to prevent it:

- Be honest with yourself about your readiness to sell before you list

- Talk to a financial advisor about your post sale plan. Knowing you have a clear path forward makes it easier to let go

- Set a "no turning back" mental deadline before the process starts

- Remember that backing out at the last minute can expose you to legal liability and will almost certainly burn the bridge with that buyer

Reason 6: Buyer and Seller Can't Agree on Deal Terms

Price is just one number in a business deal. The terms of the sale are often where negotiations break down, even when both sides agree on the purchase price.

The most common term disputes I see:

- Seller financing. The buyer wants the seller to carry a note for 20 to 30% of the purchase price. The seller wants all cash at closing. Neither side budges.

- Transition period. The buyer wants the seller to stay on for 6 to 12 months to ensure a smooth handoff. The seller wants to be done in 30 days.

- Non compete agreement. The buyer wants a 5 year, 100 mile non compete. The seller thinks 2 years and 25 miles is enough.

- Working capital. How much cash, inventory, and accounts receivable are included in the sale price? This is a constant source of friction.

- Earnout provisions. The buyer wants to tie part of the purchase price to future performance. The seller doesn't want their payout to depend on how the buyer runs the business.

| Deal Term | What Buyers Typically Want | What Sellers Typically Want |

|---|---|---|

| Seller financing | 20 to 30% carried as a note | All cash at closing |

| Transition period | 6 to 12 months of hands on support | Done in 30 days |

| Non compete | 5 years, 100 mile radius | 2 years, 25 miles |

| Working capital | Generous cash and inventory included | Minimal assets included |

| Earnout | Tie 10 to 20% of price to future results | Full payment upfront |

I brokered a deal for an IT services company where the buyer and seller agreed on a $1.2 million purchase price within the first week. Then they spent the next four months arguing about whether the seller would carry a $200,000 note and whether the non compete should be 3 years or 5 years. The deal nearly died twice over terms that represented maybe 5% of the total deal value.

How to prevent it:

- Decide your position on seller financing, transition period, and non compete before you go to market

- Include your key terms in the listing or confidential information memorandum so buyers know what to expect

- Be willing to negotiate. Rigidity on every term is a deal killer

- Use a broker or attorney to mediate term disputes so they don't become personal

Reason 7: Key Employees or Customers Leave During the Process

Business sales take time. The typical small business transaction takes 6 to 12 months from listing to close. During that window, things can change. And the two most damaging changes are losing key employees or key customers.

The employee problem. Employees find out the business is for sale (they always find out) and start looking for new jobs. Your best manager gets an offer from a competitor. Your top salesperson decides the uncertainty isn't worth it. By the time the buyer takes over, the team that made the business valuable has scattered.

I had a deal for a pest control company where the owner's top two technicians, who handled 60% of the service calls, both quit during the due diligence period. They'd heard rumors about the sale and decided to start their own operation. The buyer rightfully asked for a $150,000 price reduction to account for the lost revenue capacity. The seller refused, and the deal died.

The customer problem. A major customer finds out about the sale and decides to rebid their contract or move to a competitor. Or a key customer's contract expires during the sale process and they choose not to renew because of the uncertainty.

How to prevent it:

- Keep the sale confidential for as long as possible. Only tell employees who absolutely need to know

- Identify key employees early and consider offering retention bonuses tied to a successful sale

- Lock in customer contracts before going to market, especially with your largest accounts

- Have a communication plan ready for when employees do find out, focused on stability and opportunity under new ownership

Reason 8: Environmental or Regulatory Issues Surface

This one tends to hit deals involving manufacturing, auto repair, gas stations, dry cleaners, or any business that handles chemicals or operates on land with a long industrial history.

A buyer makes an offer on an auto body shop. During due diligence, an environmental assessment reveals soil contamination from decades of paint and solvent use. The cleanup estimate is $200,000 to $400,000. The buyer walks immediately.

Common regulatory deal killers:

- Environmental contamination (soil, groundwater, underground storage tanks)

- Missing or expired business licenses and permits

- Zoning violations that the seller has operated under for years without being challenged

- Health department violations in food service businesses

- OSHA compliance issues in manufacturing or construction businesses

- Pending regulatory changes that could affect the business model

How to prevent it:

- Get a Phase I environmental assessment done before listing if your business involves any chemicals, fuel, or industrial processes

- Verify that all licenses, permits, and certifications are current and transferable

- Address any known compliance issues before going to market

- Be transparent about the property's history so there are no surprises

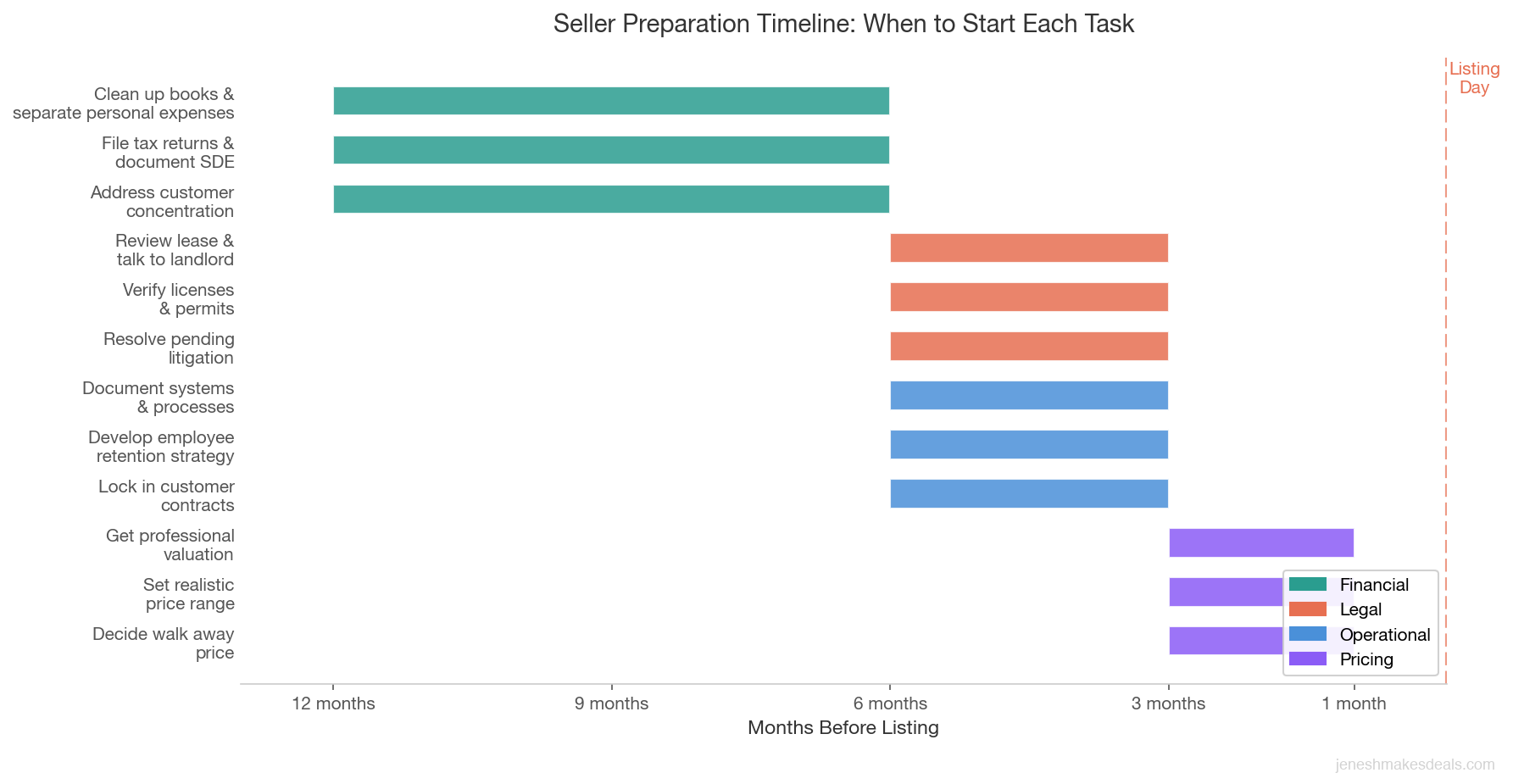

How to Prevent Deal Failures: A Seller's Preparation Checklist

If you've read this far, you can see a pattern. Almost every deal failure traces back to a lack of preparation. The sellers who close successfully are the ones who do the hard work before they list.

Here's your preparation checklist.

Financial preparation (6 to 12 months before listing):

- Clean up your books. Hire a bookkeeper if needed

- Separate personal expenses from business expenses

- File all tax returns on time (no extensions if you're planning to sell)

- Document your add backs and seller's discretionary earnings clearly

- Address any customer concentration issues

Legal and compliance preparation (3 to 6 months before listing):

- Review your lease and talk to your landlord about assignment

- Verify all licenses, permits, and certifications are current

- Resolve any pending legal disputes or litigation

- Get a Phase I environmental assessment if applicable

- Review all customer and vendor contracts for change of ownership clauses

Operational preparation (3 to 6 months before listing):

- Document your systems and processes so the business can run without you

- Identify key employees and develop a retention strategy

- Lock in major customer contracts with longer terms

- Invest in the business. This is not the time to cut costs to inflate short term profits

Pricing preparation (1 to 3 months before listing):

- Get a professional valuation based on market comparables and industry multiples

- Understand your industry's typical deal structure (how much seller financing, typical transition periods)

- Set a realistic price range, not a single number

- Decide your walk away price before negotiations start

Thinking about selling in the next year or two? Start your preparation now so you're not scrambling when a buyer shows up.

What a Good Broker Does to Keep Deals Together

I'm biased, obviously. But I've seen the difference between brokered deals and deals where the seller tries to go it alone. The closing rate for brokered transactions is significantly higher, and it's not because brokers are magicians. It's because they've seen every way a deal can fail and they know how to prevent it.

Here's what a good broker actually does to protect your deal:

Pre listing preparation. Before your business ever hits the market, a good broker will identify potential deal killers and help you fix them. Messy books? Let's get them cleaned up. Lease expiring in 18 months? Let's get an extension. Customer concentration above 25%? Let's talk about a diversification strategy.

Buyer qualification. Not every person who expresses interest in your business is a real buyer. A broker screens buyers for financial capability, relevant experience, and serious intent before they ever get access to your confidential information. This saves you from wasting months on buyers who were never going to close.

Managing expectations. A broker has the data to show both buyer and seller what similar businesses are actually trading for. When a seller wants 5x and the market says 2.5x, the broker has the comps to prove it. When a buyer lowballs at 1.5x, the broker can show them why that's unrealistic too.

Deal structure expertise. Most deal disputes aren't about the total price. They're about the terms. A good broker knows how to structure deals that work for both sides. Maybe the seller gets a higher price but carries a 15% seller note. Maybe the transition period is 90 days instead of 12 months, but the seller is available for consulting calls after that. Creative structuring saves deals.

Keeping emotions in check. Sellers get offended by low offers. Buyers get frustrated by slow responses. Due diligence findings create tension and finger pointing. A broker acts as a buffer between the two sides, keeping the conversation productive and professional even when emotions run high. I've had deals where the buyer and seller weren't speaking to each other directly for the last three weeks. But they were both speaking to me, and we got it closed.

Pushing through obstacles. When the SBA appraisal comes in low, a good broker doesn't just throw their hands up. They negotiate a revised price, restructure the deal with a seller note, or find a different lender. When the landlord wants a rent increase, the broker negotiates directly. When due diligence reveals an issue, the broker helps both sides find a solution instead of letting it become a deal breaker.

Need someone in your corner to keep your deal on track? Schedule a free consultation and let's talk about your situation.

The Bottom Line: Preparation Beats Luck Every Time

Half of all business deals fall through. That's the reality. But the deals that fall through almost always share common traits: unprepared sellers, unqualified buyers, unrealistic expectations, or unresolved problems that blow up during due diligence.

The deals that close share different traits: realistic pricing, clean financials, qualified buyers, addressed lease issues, resolved compliance problems, and clear communication from start to finish.

You can't control everything. Sometimes a buyer's financing falls through for reasons nobody could have predicted. Sometimes a key employee quits at the worst possible time. But you can control your preparation, your pricing, your financial records, and your choice of advisors.

The sellers who take 6 to 12 months to prepare before listing close at a dramatically higher rate than those who wake up one morning and decide to sell. Preparation beats luck every single time.

The prepared sellers I've worked with also get higher prices, better terms, and fewer headaches along the way.

Don't let your deal become a statistic.

Ready to sell your business the right way? Get started with a free consultation and we'll build a plan that maximizes your chances of getting to the closing table.

Related Articles

April 29, 2026

Selling a Franchise Business vs an Independent Business

Selling a franchise is a fundamentally different process than selling an independent business. Here is what every franchise owner needs to know.

April 21, 2026

What Is a Management Buyout and Is It Right for Your Business?

A management buyout lets your team buy the business. Learn how MBOs work, what they cost, and when they make sense for sellers.

April 13, 2026

How to Find the Right Business Broker for Your Industry

Not all brokers know your industry. Here's how to find one who actually understands your business and can get you top dollar.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.