You've spent fifteen or twenty years building a business. You're thinking about stepping away. And the person who knows your operation better than anyone, your general manager, your VP of operations, your right hand, is sitting ten feet away asking, "What if I bought it?"

That's a management buyout. It's one of the most natural exit strategies in small business, and when it works, it's one of the cleanest. The buyer already knows the customers, the employees, and the problems. The seller gets to hand the keys to someone they trust. And the transition is smoother than almost any outside sale.

But MBOs also fall apart all the time. The management team can't get financing. The price becomes a sore spot. The seller carries too much risk. The deal drags on for a year and everyone loses patience.

I've worked on MBOs that closed in 90 days and ones that blew up after six months of negotiation. The difference almost always comes down to three things: the management team's financial readiness, the deal structure, and whether both sides go in with realistic expectations.

What Exactly Is a Management Buyout?

A management buyout, or MBO, is when the existing management team purchases the business from the current owner. Instead of selling to an outside buyer found through a broker listing or a market search, you sell to the people who already run the day to day operations.

The concept is simple. The execution is not.

In a typical arm's length sale, you list the business, screen buyers, negotiate with strangers, and hope they can actually run the place after you leave. In an MBO, you skip the search process entirely. The buyer is already inside the building. They already know your seller's discretionary earnings, your peak months, your problem customers, and your best employees.

That insider knowledge is the MBO's biggest advantage and its biggest source of tension. The management team knows every weakness, every deferred maintenance item, every customer who's been threatening to leave. That makes them better operators after the sale, but it also gives them ammunition to push back hard on price.

The single biggest factor that separates MBOs that close from MBOs that collapse is whether both sides accept that having a relationship doesn't replace having a process. Get a third party valuation, put the deal terms in writing, and negotiate like adults. The friendship survives when the paperwork is clean.

An MBO is not the same as an ESOP (employee stock ownership plan), where a trust buys shares on behalf of all employees. It's a direct sale to specific members of the management team, structured like any other business acquisition but with the unique dynamic that buyer and seller already have a working relationship.

Why Sellers Choose MBOs Over Outside Sales

Not every seller should go the MBO route. But for certain situations, it's the best option available. Here's when I've seen MBOs work especially well.

Business Continuity

If your business depends heavily on relationships, institutional knowledge, or specialized processes, an outside buyer represents real risk. They might change the culture, lose key employees, or alienate long term customers during the transition. Your management team already knows how things work. The transition period is measured in weeks, not months.

I worked with a specialty manufacturing company where the owner had three plant managers who had been with him for over a decade. An outside buyer would have needed 6 to 12 months to learn the production processes, supplier relationships, and quality standards. The management team already had all of that. The transition took 30 days.

Employee Loyalty and Retention

When employees hear the business is being sold to an outsider, anxiety skyrockets. Will I lose my job? Will the new owner change everything? Will benefits get cut? Selling to the management team sends the opposite signal. The people running the show are the same people who have been running the show. Retention stays high. Morale stays stable.

Confidentiality

In a traditional sale, you have to market the business. That means creating a confidential information memorandum, listing on marketplaces, and showing financials to strangers who sign NDAs you can never fully enforce. With an MBO, the buyer pool is one person or a small team. Confidentiality risk drops to nearly zero.

Faster Close (Sometimes)

MBOs can close faster than outside sales because you skip the marketing, screening, and due diligence discovery phases. The management team already knows the business. They don't need 60 days to review operations. That said, the financing piece can add time, so "faster" is only true when the money comes together quickly.

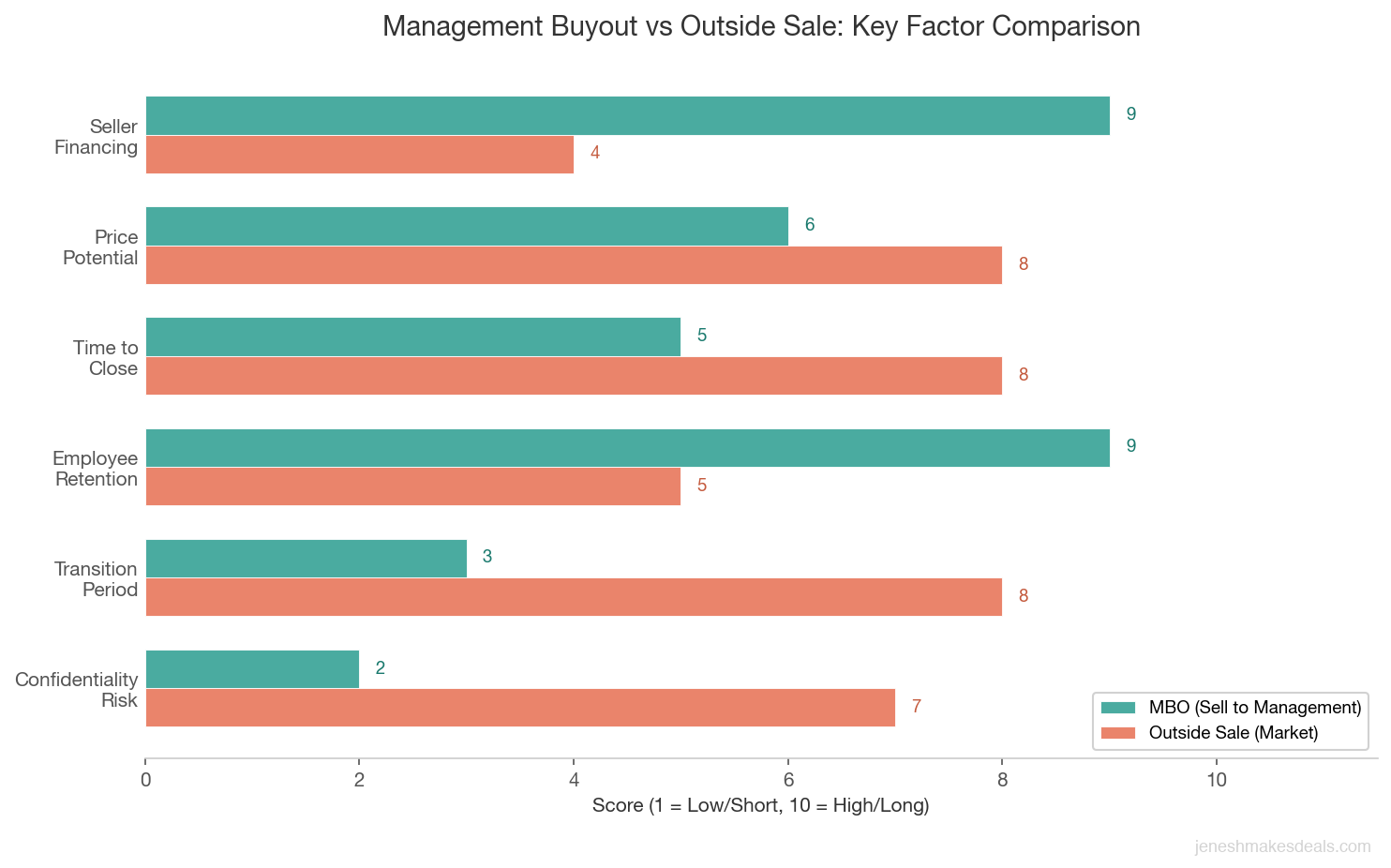

| Factor | MBO (Sell to Management) | Outside Sale (Market Listing) |

|---|---|---|

| Buyer Knowledge of Business | Deep, already operational | Starts from scratch during due diligence |

| Confidentiality Risk | Very low, no marketing needed | Higher, must share financials with strangers |

| Transition Period | 30 to 60 days typical | 3 to 12 months typical |

| Employee Retention | High, familiar leadership stays | Uncertain, anxiety often causes turnover |

| Competitive Bidding | No, single buyer | Yes, potential for multiple offers |

| Price Potential | Fair market value | Fair market value or higher with demand |

| Seller Financing Required | Almost always (10% to 30%) | Sometimes (0% to 20%) |

| Timeline to Close | 4 to 8 months | 6 to 12 months |

Thinking about selling to your management team? Let's talk about whether an MBO makes sense for your situation.

How MBOs Are Financed: Where the Money Actually Comes From

This is where most MBOs either come together or fall apart. Your management team knows the business, but they probably don't have $1.5 million in cash sitting around. The financing structure is the whole game.

Here are the most common funding sources for small business MBOs, usually combined in layers.

SBA 7(a) Loans

The SBA 7(a) loan is the workhorse of small business acquisitions, including MBOs. These loans can cover up to 90% of the purchase price in some cases, with terms up to 10 years and interest rates tied to the prime rate plus a spread (typically prime + 2.25% to 2.75%).

For a $1.5 million MBO, an SBA loan might cover $1.05 million (70%). The buyer needs to bring a down payment (usually 10% to 20%), and the SBA will want to see that the business generates enough cash flow to cover the debt service, typically a minimum debt service coverage ratio of 1.25x.

The catch: the management team members need to personally guarantee the loan, have decent credit scores (680+), and demonstrate relevant management experience. If your team has been running the business for years, the experience piece is already covered. For a deeper look at SBA qualification and terms, see our SBA loans guide.

Seller Financing

In almost every MBO I've worked on, the seller carries some portion of the note. This is not just common. It's expected. Lenders actually like seeing seller financing because it shows the seller has confidence in the buyer and the business's future cash flow.

A typical seller note in an MBO covers 10% to 30% of the purchase price, sits subordinate to the SBA loan (meaning the bank gets paid first), and carries an interest rate of 5% to 8% with a 5 to 7 year term.

For our $1.5 million example: the seller might carry a $300,000 note (20%) at 6% over 7 years. That's roughly $4,400 per month going to the seller. If the business generates $40,000 per month in free cash flow after operating expenses, that payment is very manageable alongside the SBA loan payment.

If a seller refuses to carry any financing in an MBO, that's a signal to lenders and to the management team. It tells everyone that the seller doesn't believe in the business's ability to keep generating cash flow after the handoff. Carrying a note isn't charity. It's the strongest vote of confidence a seller can give, and it makes the whole deal easier to fund.

Want to understand seller financing in more detail? Read our full guide on how seller financing works in business acquisitions.

Management Team Equity (Down Payment)

The management team needs to have some skin in the game. Lenders and sellers both want to see that the buyers are putting their own money at risk. This is typically 10% to 15% of the purchase price.

For a $1.5 million deal, that means the management team needs to come up with $150,000 to $225,000 collectively. If there are three managers splitting the equity, that's $50,000 to $75,000 each. That's real money, but it's within reach for experienced managers who've been saving, especially if they can tap retirement funds through a ROBS 401(k) rollover.

Private Equity Backing

For larger MBOs ($3 million+), the management team sometimes partners with a private equity firm or a search fund investor who provides the equity capital. The PE firm puts up the down payment and sometimes more, and the management team contributes sweat equity plus a smaller cash investment.

This changes the dynamics significantly. The management team gets access to capital they wouldn't have on their own, but they give up equity and board control. The PE firm will want a seat at the table and an exit strategy of its own (usually a sale in 3 to 5 years).

I generally recommend PE involvement only when the management team can't fund the equity piece themselves and the business is large enough to justify the complexity.

| Funding Source | Typical Share of Price | Interest Rate | Term | Best For |

|---|---|---|---|---|

| SBA 7(a) Loan | 60% to 80% | Prime + 2.25% to 2.75% | Up to 10 years | Most MBOs under $5M |

| Seller Financing | 10% to 30% | 5% to 8% | 5 to 7 years | Bridging the gap, signaling seller confidence |

| Management Equity | 10% to 15% | N/A | N/A | Buyer skin in the game, lender requirement |

| Private Equity | 20% to 40% | N/A (equity stake) | 3 to 5 year hold | Larger deals ($3M+) where team lacks capital |

| ROBS 401(k) Rollover | Varies | N/A | N/A | Managers with retirement savings, no debt added |

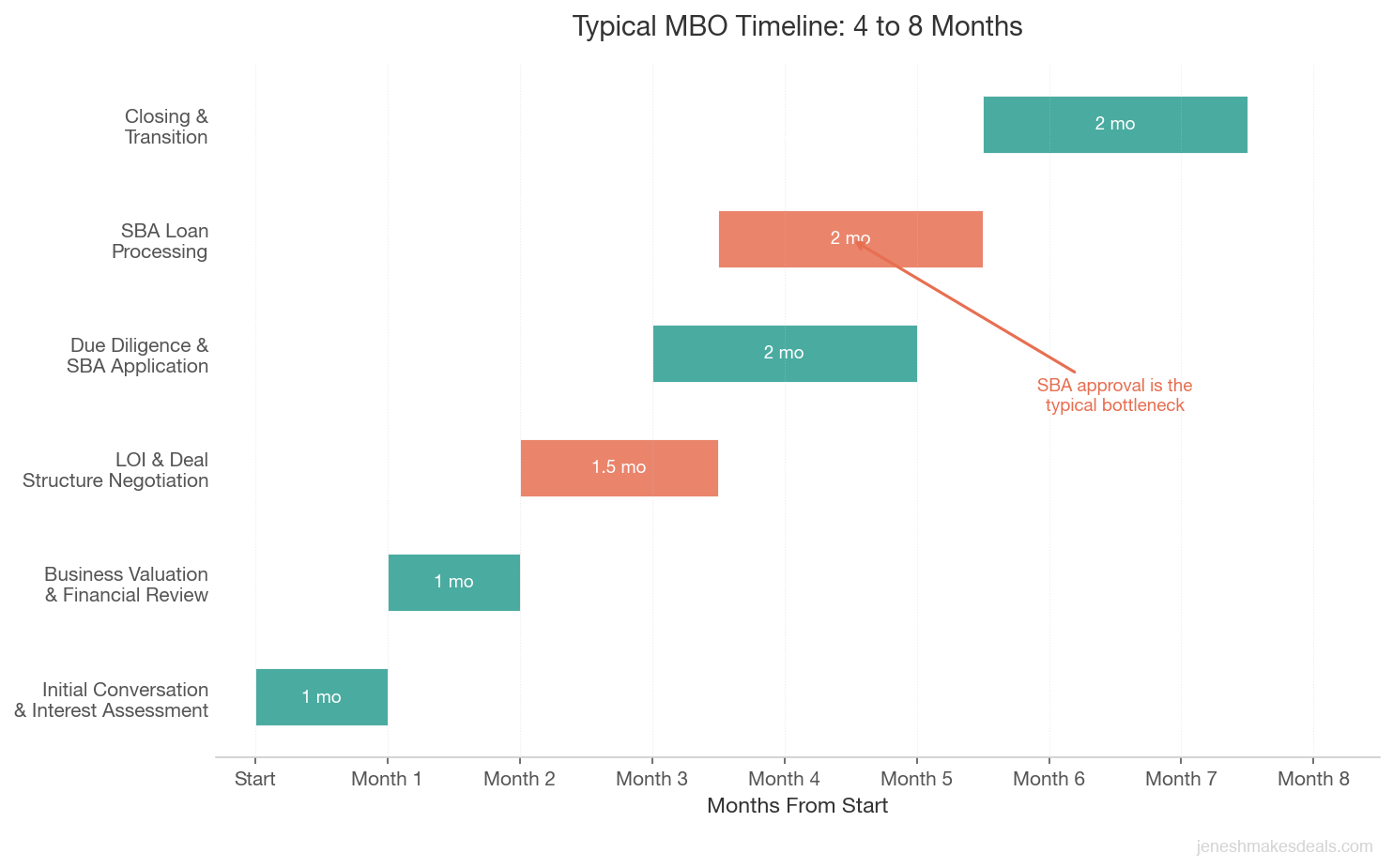

The MBO Process: From First Conversation to Closing

Here's what a typical small business MBO timeline looks like. Most of mine take 4 to 8 months from initial conversation to closing day.

Month 1: The Conversation

It starts with the owner and the management team having a real conversation about interest, expectations, and financial reality. This is not a handshake deal. It's the beginning of a structured process.

I recommend bringing in a broker or advisor at this stage, even though there's no marketing to do. You need someone who can guide the process, keep emotions in check, and make sure both sides are thinking clearly about price, structure, and timeline.

Month 2: Valuation and Financial Review

You need an independent business valuation before anyone starts negotiating price. This is non negotiable. The management team will have opinions about what the business is worth. The seller will have different opinions. A third party valuation gives everyone the same starting point.

The management team should also start organizing their personal financial statements, credit reports, and preliminary conversations with SBA lenders. If anyone on the team has credit issues or insufficient personal net worth, it's better to find out now than three months into the process.

Months 3 to 4: LOI and Deal Structure

Once both sides have a general agreement on price range, you put together a letter of intent. The LOI outlines the purchase price, financing structure, transition terms, and key contingencies.

This is where the real negotiation happens. How much seller financing? What's the interest rate? How long is the transition period? Does the seller stay on as a consultant? What happens if the management team defaults on the note?

Months 4 to 6: Due Diligence and Financing

Even though the management team knows the business, formal due diligence still happens. The SBA lender will require it. The management team's attorney will require it. And the management team itself should want a formal review to make sure there aren't liabilities they didn't know about.

Simultaneously, the SBA loan application is being processed. This is typically the longest part of the timeline. SBA approvals take 45 to 60 days on average, sometimes longer if the lender needs additional documentation.

Months 6 to 8: Closing and Transition

Once financing is approved and due diligence is complete, you close. The purchase agreement is signed, funds are distributed, and ownership transfers. The seller typically stays on for 30 to 90 days in a consulting or advisory role to ensure a smooth handoff.

Ready to explore the MBO process for your business? Schedule a call to discuss your timeline.

How to Value the Business in an MBO

Valuation in an MBO is both easier and harder than in a typical sale. Easier because both sides have access to the same operational information. Harder because the relationship between buyer and seller creates emotional pressure on the price.

The Standard Approach: SDE or EBITDA Multiple

For most small businesses (under $5 million in revenue), the valuation starts with seller's discretionary earnings (SDE). SDE is the total financial benefit the owner receives from the business, including salary, benefits, personal expenses run through the business, and add backs for non recurring items.

You then apply an industry multiple to the SDE. For most small businesses, that multiple falls between 2x and 4x SDE, depending on the industry, growth trajectory, customer concentration, and how dependent the business is on the owner.

For a business generating $400,000 in SDE with a 3.5x multiple, the valuation comes out to $1.4 million. If the business is growing and has low owner dependence (which is often the case if the management team has been running things), the multiple might be higher. If the business has risks, it might be lower.

For larger businesses, you'll use EBITDA instead of SDE. The principles are the same, but the multiples tend to be higher (3x to 6x for most industries at this level). See our guide on EBITDA in business valuation for more detail.

The Discount Question

Should the seller offer a price discount in an MBO? This comes up in every deal I work on. The management team argues they've been loyal, they've helped build the value, and they deserve a break. The seller feels they've already paid the team well through salaries and bonuses.

My advice: don't discount the price. Discount the terms.

Sell at fair market value but offer favorable seller financing terms. A lower interest rate, a longer repayment period, or a smaller down payment requirement. This preserves the seller's total proceeds while making the deal more accessible for the management team. It also looks better to SBA lenders, who want to see the business being purchased at a defensible price.

If you do choose to offer a direct price discount, do it consciously and put a number on it. "I'm selling at a 10% discount to fair market value as a loyalty bonus." Don't let the relationship just erode the price without making a deliberate choice.

I tell every seller considering an MBO the same thing: generous terms beat a discounted price, every time. A lower interest rate on the seller note or a longer repayment window costs you relatively little over the life of the deal, but it can make the difference between a management team that qualifies for financing and one that doesn't.

Want to run the numbers on your business? Use our free valuation calculators to get an estimate of what your business might be worth.

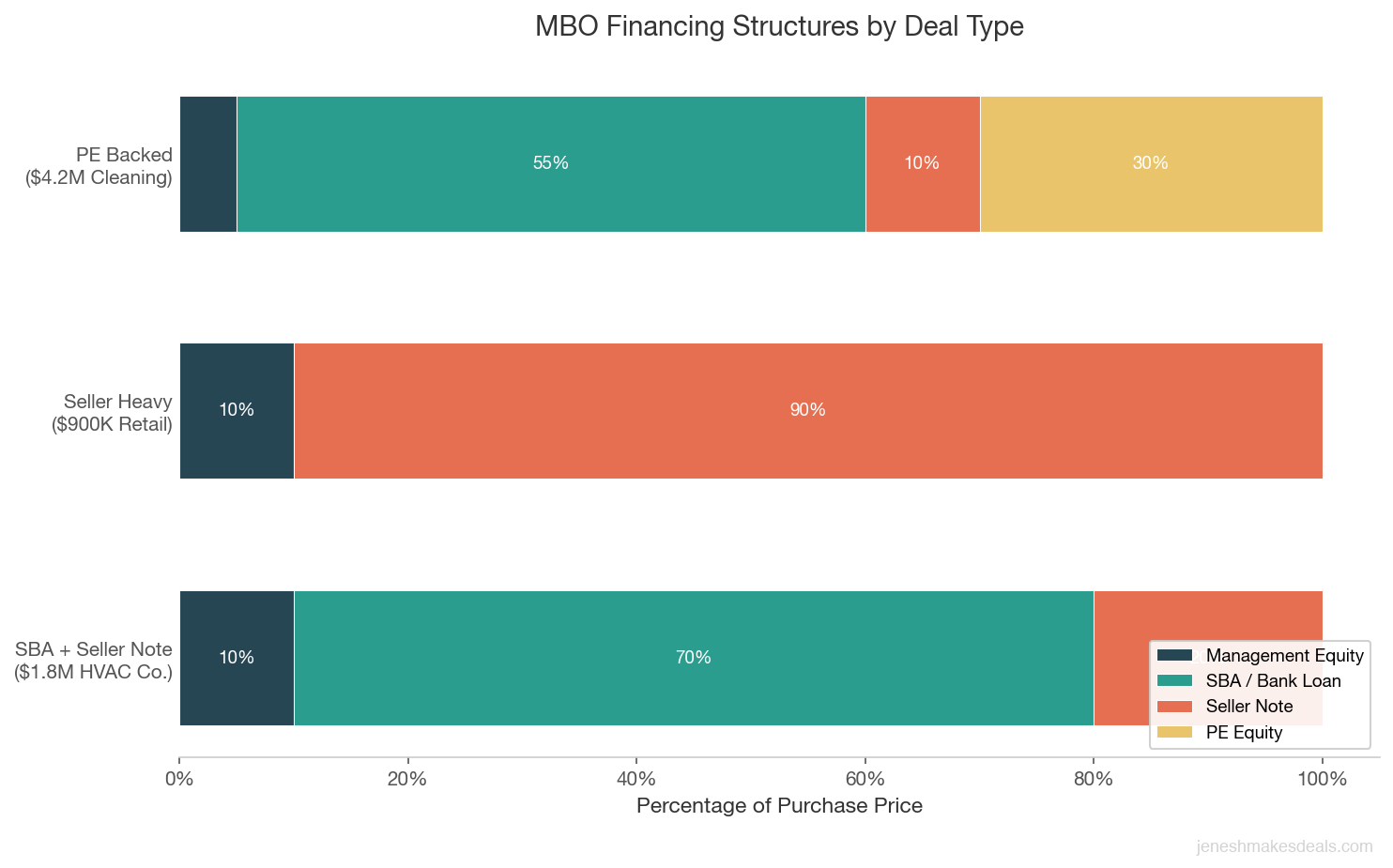

Common MBO Deal Structures With Dollar Examples

Let me walk through three common MBO structures I've seen work in practice. These are based on real deals (with numbers adjusted for privacy).

Structure 1: SBA Loan + Seller Note (Most Common)

Business: HVAC company, $1.8 million sale price, $500,000 SDE

- Management equity (down payment): $180,000 (10%)

- SBA 7(a) loan: $1,260,000 (70%), 10 year term, 8.5% interest

- Seller note: $360,000 (20%), 7 year term, 6% interest, 2 year standby (no payments for first 2 years)

- Monthly SBA payment: approximately $15,600

- Monthly seller note payment (after standby): approximately $6,200

- Total monthly debt service: $21,800

- Business monthly cash flow after expenses: $35,000

- Debt service coverage ratio: 1.6x (healthy)

The 2 year standby on the seller note is a common feature in MBO deals. It gives the new owners breathing room during the transition period and ensures the SBA loan gets priority in the early months.

Structure 2: Seller Heavy Financing (When SBA Isn't an Option)

Business: Specialty retail, $900,000 sale price, $280,000 SDE

- Management equity: $90,000 (10%)

- Seller note: $810,000 (90%), 8 year term, 7% interest

- Monthly seller note payment: approximately $12,500

- Business monthly cash flow after expenses: $20,000

- Debt service coverage ratio: 1.6x

This structure happens when the management team can't qualify for an SBA loan, often due to credit issues or the business not meeting SBA requirements. The seller takes on more risk but gets a higher interest rate and often negotiates additional protections like a personal guarantee, a non compete, and the right to retake the business if payments fall behind by more than 90 days.

Structure 3: PE Backed MBO (Larger Deals)

Business: Commercial cleaning company, $4.2 million sale price, $1.1 million EBITDA

- PE firm equity: $1,260,000 (30%)

- Management team equity: $210,000 (5%)

- Senior debt (bank loan): $2,310,000 (55%)

- Seller note: $420,000 (10%), 5 year term, 6.5% interest

- Monthly bank payment: approximately $28,400

- Monthly seller note payment: approximately $8,200

- Total monthly debt service: $36,600

- Business monthly cash flow: $65,000

- Debt service coverage ratio: 1.78x

In this structure, the PE firm owns the majority equity stake and the management team owns a minority stake (usually 15% to 25% of the total equity). The management team runs the business day to day, and the PE firm provides strategic support, capital for growth, and an eventual exit path.

Risks and Downsides of an MBO

MBOs aren't all upside. Here are the real risks both sellers and management teams need to consider.

For Sellers

You're the bank. If you carry a seller note (and you almost certainly will), you're exposed to the business's future performance. If the new owners make bad decisions and cash flow drops, your note payments are at risk.

Lower total price potential. In an open market process, you might get multiple offers and bid the price up. In an MBO, you have one buyer. There's no competitive tension. You may get fair market value, but you're unlikely to get above market value.

Emotional complexity. Negotiating price and terms with people you've worked with for years is uncomfortable. Conversations about personal guarantees, default remedies, and collateral feel different when they're with your long time operations manager versus a stranger.

Longer exposure. Between the seller note and the transition period, you're tied to this business for years after the sale. If something goes wrong at year 3 of a 7 year note, you're back in the picture.

For the Management Team

Personal financial risk. You're signing personal guarantees on SBA loans. You're investing your savings. If the business fails, you lose your investment and potentially face personal liability.

The skill gap. Managing a business and owning a business are different things. You might be great at operations, but have you managed cash flow, debt service, capital allocation, and strategic planning at the ownership level? The responsibilities shift significantly.

Partnership dynamics. If multiple managers are buying together, you now have business partners. Partnerships need clear operating agreements, defined roles, and dispute resolution mechanisms. I've seen MBOs succeed on the acquisition side and then fall apart because the partners couldn't agree on how to run the business.

When an MBO Is the Wrong Choice

Not every business should be sold through an MBO. Here are the situations where I'd steer a seller toward an outside sale instead.

Your Management Team Doesn't Have the Capital or Credit

If the management team collectively can't come up with a 10% down payment and at least one member can't qualify for an SBA loan, the financing will be extremely difficult. You'll end up carrying 80% to 90% of the deal as seller financing, which puts too much risk on you.

Before going down the MBO path, sit down with a lender and have the management team get pre qualified. Better to find out early that the money isn't there than to spend six months negotiating a deal that can't close.

The Market Would Pay Significantly More

If your business is in a hot industry with strong buyer demand, an MBO might leave money on the table. Private equity firms, strategic acquirers, and well funded individual buyers might pay a premium that your management team simply can't match.

I worked with a home services company that the management team wanted to buy for $2.5 million. We took it to market and got offers at $3.2 million from two PE backed buyers. That $700,000 difference was real money. The seller chose the higher offer.

Your Management Team Is Really Just One Person

A true MBO involves a team. If you have one key manager who wants to buy the business and everyone else is a line level employee, that's not really an MBO. That's selling to an individual, and it should be evaluated as an employee buyout with different considerations.

One person carrying all the operational, financial, and strategic burden is riskier than a team splitting those responsibilities. Make sure your "management team" is actually a team and not just one ambitious person with a title.

The Business Is Too Owner Dependent

If you are the business, meaning customers come because of your reputation, your relationships, or your personal expertise, then it doesn't matter who buys it. The value walks out the door when you do.

MBOs work best when the business has been running without heavy owner involvement for at least a year or two. If you're still the primary salesperson, the main client relationship manager, and the final decision maker on everything, you need to build a business that runs without you before any sale, MBO or otherwise.

Not sure if your business is ready for an MBO? Reach out for a confidential assessment.

How to Tell if Your Management Team Is Ready

Before you commit to an MBO, you need to honestly evaluate whether your management team can handle ownership. Here's what I look at when advising sellers on this question.

Financial Readiness

Can the team collectively put together a 10% to 15% down payment? Does at least one team member have a credit score above 680? Do they have personal financial statements that won't scare an SBA lender? Have they saved money, or will they need to borrow the down payment too?

Financial readiness is the first filter. If the money isn't there, everything else is academic.

Operational Competence

Has the management team actually been running the business, or have they been executing your decisions? There's a big difference between a manager who handles daily operations because the owner told them what to do and a manager who independently makes strategic, financial, and operational decisions.

Test this by stepping back. Take a two week vacation. Then take a month. If the business runs smoothly without you, your team might be ready. If it barely functions when you're gone for a long weekend, they're not.

Business Acumen Beyond Operations

Running a business at the ownership level requires skills that operations managers don't always have. Financial management, tax strategy, capital allocation, vendor negotiation, legal decisions, insurance management, and long term strategic planning. Your operations manager might be brilliant at scheduling and quality control but have never looked at a balance sheet.

Identify the gaps early and create a plan to fill them. That might mean the management team takes some business courses, works with a mentor, or hires a CFO or fractional executive to cover the areas they're weak in.

Team Cohesion and Governance

If multiple managers are buying the business together, how do they work together? Do they have aligned visions for the future? Who makes final decisions when they disagree? What happens if one partner wants to sell their share in three years?

These governance questions need clear answers before the deal closes, not after. I've seen management teams that worked beautifully as employees but couldn't function as partners because they never defined decision making authority or profit distribution.

Before any MBO closes, the management team should have a formal operating agreement that covers ownership percentages, roles, compensation, decision making processes, dispute resolution, and buyout provisions for departing partners.

Making the MBO Work: Practical Steps to Get Started

If you've read this far and an MBO still sounds right, here's what I'd do next.

Step 1: Have a candid conversation with your management team about their interest and financial capacity. Don't make promises. Just gauge reality.

Step 2: Get a professional business valuation. Use our valuation calculators for a preliminary estimate, then hire a professional for a formal appraisal.

Step 3: Have the management team talk to an SBA preferred lender early. Pre qualification tells you immediately whether the financing is feasible.

Step 4: Engage a business broker or M&A advisor to structure the deal. The structure matters more than the price in many MBOs.

Step 5: Draft a letter of intent covering price, financing structure, transition terms, and timeline. Get it reviewed by attorneys on both sides.

Step 6: Allow 4 to 8 months from LOI to closing. A poorly structured MBO that closes fast is worse than a well structured one that takes an extra two months.

The best MBOs I've worked on share one thing: both sides went in with realistic expectations and structured the deal in a way that worked for everyone. The seller got fair value. The management team got a business they already loved. The employees got stability.

Want to discuss whether an MBO is right for your business? Get in touch for a free, confidential conversation.

Related Articles

April 29, 2026

Selling a Franchise Business vs an Independent Business

Selling a franchise is a fundamentally different process than selling an independent business. Here is what every franchise owner needs to know.

April 13, 2026

How to Find the Right Business Broker for Your Industry

Not all brokers know your industry. Here's how to find one who actually understands your business and can get you top dollar.

March 27, 2026

How to Find Businesses for Sale in 2026

Most buyers search the wrong places. Here's where to actually find businesses for sale and how to avoid wasting months on dead ends.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.