How to Maintain Confidentiality When Selling Your Business

The moment word gets out that your business is for sale, the clock starts ticking against you. Employees start updating their resumes. Customers begin looking for alternatives. Competitors smell blood in the water. And suddenly the business you spent years building starts losing value before you even sit down at the negotiation table.

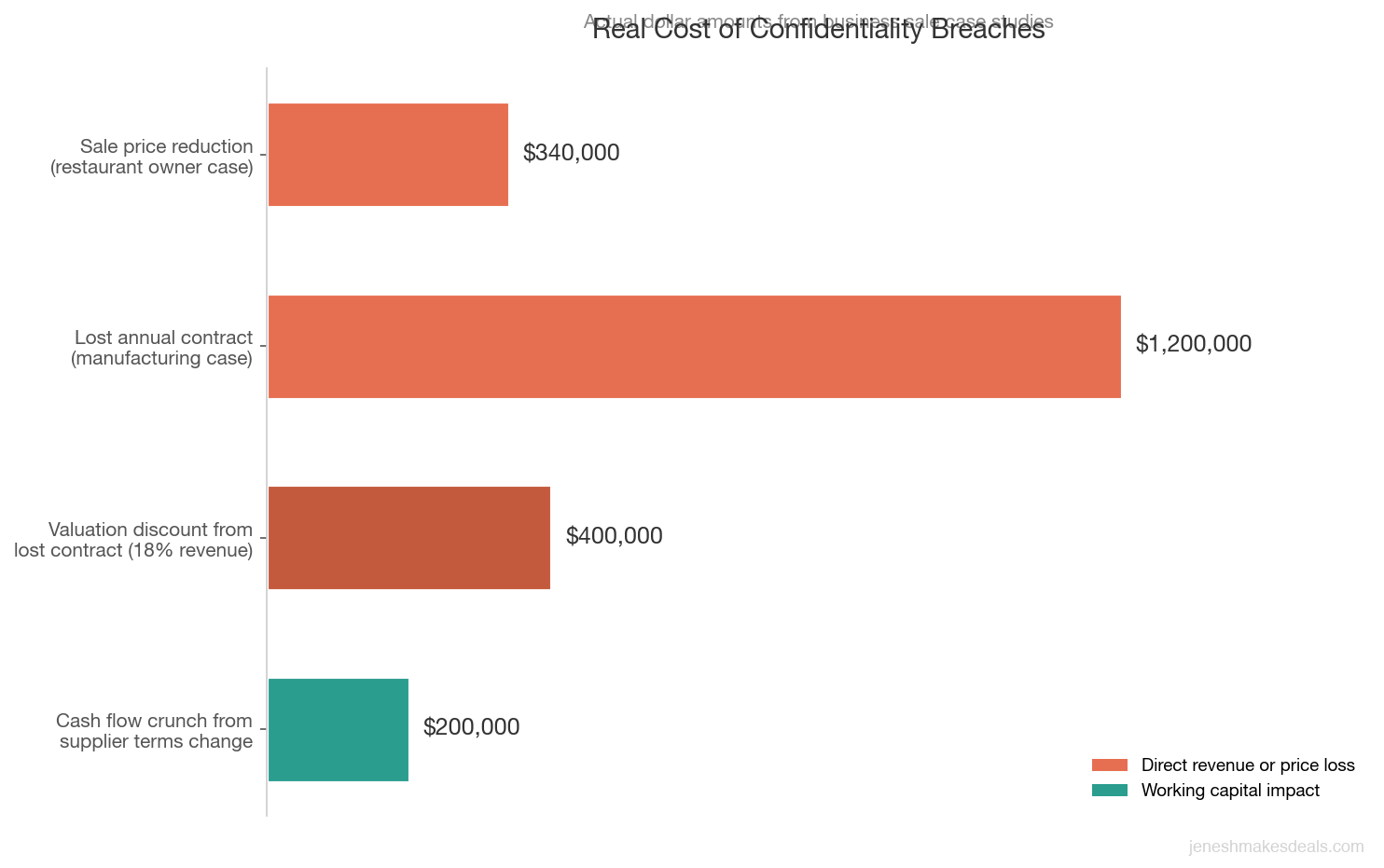

I've watched confidentiality breaches kill deals that were worth millions. One restaurant owner casually mentioned to a supplier that he was "thinking about getting out," and within two weeks his entire staff knew. Three key employees left within a month. The buyer who was circling walked away, citing "instability in the workforce." That owner ended up selling 14 months later for $340,000 less than the original offer.

Confidentiality isn't just a nice to have when selling a business. It's the foundation that holds the entire deal together.

Why Confidentiality Matters More Than You Think

When I talk to first time sellers, most of them understand that they shouldn't broadcast the sale on social media. But they underestimate just how quickly information travels and how much damage even a rumor can cause.

Here's what actually happens when word gets out.

Employees leave. This is the most immediate and damaging consequence. Your best employees, the ones with the most options, are the first to go. They don't wait around to find out if the new owner will keep them. According to IBBA data, businesses that experience a confidentiality breach during the sale process lose an average of 15% to 25% of their workforce before closing. If you want to understand the full picture, read about what happens to employees during a sale.

Customers start hedging. If your customers find out you're selling, they start diversifying away from you. A manufacturing company I worked with lost a $1.2 million annual contract because the customer's procurement team heard the business was for sale and decided to "reduce single source risk." That contract represented 18% of the company's revenue, and its loss reduced the sale price by over $400,000.

Competitors get aggressive. Your competitors will use the information against you. They'll tell your customers that your business is "in transition" and offer special deals to poach them. They'll recruit your employees. I've seen competitors approach a seller's key accounts within days of learning about a sale.

Suppliers change terms. Suppliers who hear you're selling may tighten credit terms, require prepayment, or start looking for backup customers. One distributor I worked with had a key supplier switch them from net 60 to net 15 after hearing about the sale, creating a $200,000 cash flow crunch at the worst possible time.

Landlords get nervous. If you lease your space, your landlord may refuse to extend or renew the lease, or they may try to renegotiate terms. A buyer who can't secure a long term lease walks away from the deal.

A single confidentiality breach can cost hundreds of thousands of dollars in lost deal value, and the damage is almost always irreversible once information is out.

The bottom line: a confidentiality breach doesn't just create awkward conversations. It destroys tangible value and can kill the deal entirely.

The NDA Is Just the Beginning

Every business sale starts with a non disclosure agreement. But too many sellers treat the NDA as a magic shield that makes everything safe. It's not. An NDA is a necessary first step, but it has real limitations.

A good NDA should cover the fact that the business is for sale, all financial information shared during due diligence, customer and vendor lists, proprietary processes and trade secrets, employee compensation details, and the terms of any offers or negotiations. It should also specify damages and remedies for breach, including injunctive relief.

But here's the reality. If a buyer signs your NDA and then tells someone that your business is for sale, you can sue them. But by the time you get to court, the damage is already done. Your employees already quit. Your customers already left. You can't un ring that bell.

That's why smart sellers don't rely on NDAs alone. They control the flow of information so that even if someone talks, they don't have enough details to identify the business or cause real damage.

Think of the NDA as your legal safety net. But your real protection comes from how you structure the entire information sharing process.

How to Market Your Business Without Revealing It

This is the part that surprises most sellers. You can actively market your business to thousands of potential buyers without anyone knowing it's yours. The key is using blind listings and a structured approach to buyer engagement.

Blind listings describe your business without identifying it. A typical blind listing for a plumbing company might read: "Established residential and commercial plumbing service company in the greater Phoenix metro area. 22 years in business, $3.8M revenue, $620K SDE, 28 employees, strong recurring maintenance contracts." That description could match dozens of plumbing companies in Phoenix. No one reading it would know which one it is.

Teaser profiles go a step further. They include enough financial and operational detail to attract serious buyers while keeping the identity hidden. A good teaser includes general industry and geography, high level financial metrics (revenue range, earnings range, growth trend), business highlights (years in business, employee count, customer count), and the general reason for selling.

What you never include in a teaser: the company name, the exact address, specific customer names, the owner's name, or any detail unique enough to identify the business.

Using a broker as intermediary. When I work with sellers, all buyer communication goes through me first. Buyers contact me, not the seller. I qualify them before they learn anything specific. The seller's phone never rings with random buyer calls, and their email never gets a message from someone they don't know asking about the sale. This buffer is one of the biggest advantages of working with a broker. If you're weighing your options, it's worth thinking about whether you need a broker for exactly this reason.

Controlling Information Flow With Staged Disclosure

The biggest mistake sellers make with confidentiality is sharing too much too soon. You don't hand someone the keys to your house before they've even made an offer. The same logic applies here.

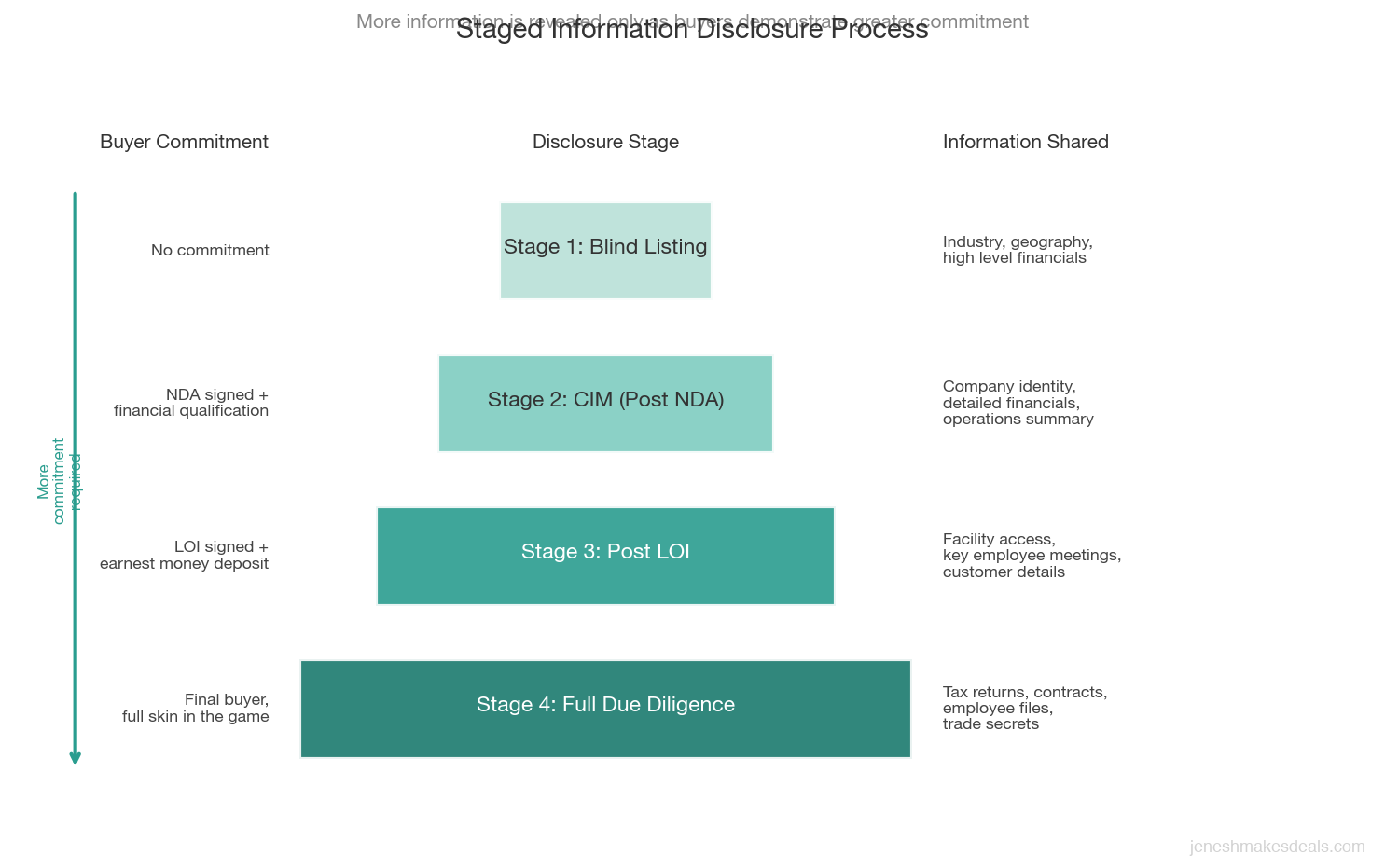

I use a staged disclosure process that reveals information in layers, with each layer requiring more commitment from the buyer.

Stage 1: Blind listing and teaser. This is what every potential buyer sees first. It contains no identifying information. Buyers who are interested sign an NDA to move forward.

Stage 2: The CIM. After the NDA is signed and the buyer is pre qualified (meaning they've demonstrated they have the financial ability and genuine interest to buy), they receive the confidential information memorandum. The CIM reveals the business identity and includes detailed financials, operations, and growth opportunities. But it still doesn't include the most sensitive items like customer lists with contact information, exact employee compensation, or proprietary formulas.

Stage 3: Management meetings and site visits. Only after the buyer has submitted a letter of intent and the seller has accepted it do we arrange facility tours and meetings with key personnel. These happen after hours or off site when possible.

Stage 4: Full due diligence. The buyer gets access to everything: tax returns, customer contracts, employee files, vendor agreements, and all other sensitive documents. This only happens after a signed letter of intent with an earnest money deposit. At this point, the buyer has real skin in the game.

| Stage | What's Shared | Who Sees It |

|---|---|---|

| Blind listing | Industry, geography, high level financials | Anyone browsing |

| Post NDA teaser | Company name, detailed financials, operations summary | Qualified, NDA signed buyers |

| Post LOI | Facility access, key employee meetings, customer details | Serious buyer with earnest money |

| Full due diligence | Tax returns, contracts, employee files, trade secrets | Final buyer only |

This staged approach means that by the time someone has enough information to cause damage, they've invested significant time, signed legal documents, and put up real money. That creates strong incentives to keep quiet.

Ready to talk about selling? Contact us for a free consultation and we'll walk you through your options.

Managing Employee Confidentiality

This is the question I get asked more than almost any other: "When do I tell my employees?"

My answer is almost always the same: as late as possible.

Tell employees after the deal is signed and all contingencies are removed. Even your most loyal employees act in their own self interest when they learn the business is being sold.

For most businesses, that means telling employees after the deal is signed and all contingencies are removed. Sometimes that means employees find out on the day of closing or the day after. That might feel uncomfortable, but it's the right call in most situations.

Here's why. Employees, even your most loyal ones, act in their own self interest. If they know the business is being sold, they start worrying about their jobs. That worry leads to distraction, lower productivity, resume updating, and conversations with competitors. Even if they don't leave, the uncertainty affects morale and performance. And that uncertainty can last months if the deal takes a while to close.

What to do if your behavior changes. Selling a business requires meetings, phone calls, and time away from the office. Your employees will notice. Here's how to handle it.

If you're meeting with buyers during business hours, tell employees you're working on a "new strategic partnership" or "exploring growth opportunities." These explanations are vague enough to be true without revealing anything.

If you need to provide financial documents or operational reports that you don't normally prepare, tell your accountant or bookkeeper you're refinancing debt or applying for a line of credit. Both require similar documentation.

If outside people (like buyers doing a site visit) show up, introduce them as "consultants" or "advisors" helping with operational improvements.

| Suspicious Activity | Cover Story | Why It Works |

|---|---|---|

| Frequent off site meetings | Exploring a new strategic partnership | Vague enough to be true without revealing anything |

| Preparing unusual financial reports | Refinancing debt or applying for a line of credit | Both require similar documentation |

| Unknown visitors at the business | Consultants or advisors for operational improvements | Common enough that employees won't question it |

| Owner leaving early or taking long lunches | Client meetings or networking events | Consistent with normal business development |

| Attorney or accountant meetings | Tax planning or compliance review | Routine and unremarkable to employees |

What if an employee finds out early? It happens. If a key employee discovers the sale, you have two options.

First, you can bring them into confidence. Tell them the truth, explain why confidentiality matters, and give them an incentive to stay and keep quiet. A stay bonus (typically 5% to 15% of their annual salary, paid at closing) works well. This also signals to the buyer that key talent is retained, which can increase the sale price.

Second, if the employee isn't key to operations, you can downplay it. Tell them you "explored the idea but decided not to move forward." This only works if they haven't seen hard evidence like listing documents or buyer communications.

Protecting Customer and Vendor Relationships

Customers and vendors are the lifeblood of your business value. Losing a major customer or having a key supplier change terms during the sale process can reduce your sale price by 10% to 30%.

Handling customer due diligence. Buyers will want to verify your customer relationships. They'll want to see contracts, retention rates, and revenue concentration. Share this information through documents, not direct customer contact. No buyer should be calling your customers before the deal is closed.

In rare cases, a buyer may insist on speaking with one or two key customers before closing. If this happens, keep the pool small (one or two customers maximum), only allow it after the LOI is signed with earnest money, have the conversation framed as a "potential partnership" rather than a sale, and be present for the conversation.

Protecting vendor relationships. Vendors are tricky because many contracts have assignment clauses that require notification or consent when ownership changes. Review your vendor contracts early in the process with your attorney. Identify which ones require consent for assignment and plan the notification timing. Ideally, you handle vendor notifications after closing, not before.

If a vendor contract requires consent before closing, approach it late in the process and frame it positively. "We're bringing in a partner with additional capital and expertise" works better than "I'm selling and leaving."

Contract assignment clauses. Some contracts, especially long term service agreements and leases, have change of control provisions that can be triggered by a sale. Your attorney should review all material contracts during the preparation phase and flag any that could be problematic. The last thing you want is a key contract getting terminated because you didn't handle the notification properly.

The Biggest Confidentiality Mistakes Sellers Make

After working on hundreds of business sales, I see the same mistakes over and over. Here are the most common ones.

Telling friends and family too early. This is the number one source of leaks. You tell your brother in law that you're selling, and he mentions it at a barbecue to someone who knows your biggest customer. I've seen this exact scenario play out multiple times. Don't tell anyone who doesn't need to know. If you need emotional support through the process, talk to your broker, your attorney, or your accountant. They're all bound by professional obligations to keep it quiet.

Casual conversations with industry peers. Business owners talk to each other. You're at a trade association meeting and someone asks how business is going. You say something like, "Good, but I'm ready for a change." That's enough for people to start speculating. In small industries, word travels fast.

Social media behavior changes. If you suddenly start posting nostalgic content about your business journey or sharing "lessons learned" content, people notice. One owner started posting LinkedIn articles about "what I wish I knew when I started my business" while actively selling. His employees connected the dots within two weeks.

Changing your behavior at work. If you've always been the first one in and the last one out, and you suddenly start taking long lunches and leaving early for "meetings," people notice. Try to maintain your normal routine as much as possible. Schedule buyer meetings early in the morning, after hours, or off site.

Meeting buyers at the business. Never have potential buyers visit your business during operating hours without a solid cover story. Site visits should happen after hours, on weekends, or when employees are away. If a daytime visit is unavoidable, the buyer should be introduced as a consultant, investor, or advisor.

Searching for your own business online. If you Google "sell [your business name]" from your work computer, and your IT person sees the search history, that's a problem. Use a personal device on a separate network for all sale related research.

| Common Mistake | Risk Level | Potential Damage | How to Avoid It |

|---|---|---|---|

| Telling friends and family | High | Word spreads to customers and employees through social circles | Only tell spouse, attorney, accountant, and broker |

| Casual industry conversations | High | Competitors and peers speculate and spread rumors | Avoid discussing "changes" or "getting out" at events |

| Social media behavior changes | Medium | Employees and contacts connect the dots quickly | Maintain your normal posting patterns |

| Changing your work routine | Medium | Staff notices unusual absences and meetings | Schedule buyer meetings before or after hours |

| Meeting buyers at the business | High | Employees see unfamiliar visitors and ask questions | Use off site locations or after hours visits |

| Searching on work devices | Low | IT staff or shared devices expose search history | Use personal devices on separate networks |

Need help figuring out what your business is worth? Use our free business valuation calculator to get a quick estimate.

What to Do If Confidentiality Is Breached

Despite your best efforts, breaches happen. Maybe an employee overheard a phone call. Maybe a buyer mentioned it to someone. Maybe your accountant slipped up. Whatever the cause, here's how to handle it.

Step 1: Assess the damage. Before you react, figure out exactly what was disclosed and to whom. A rumor among a few employees is very different from your biggest customer knowing the full details of the sale.

Step 2: Address it directly. If employees have heard rumors, don't ignore it. Silence confirms suspicion. Instead, hold a brief meeting and address it head on. You can say something like: "I've heard some rumors going around. I want you to know that I'm always looking at ways to grow this business and create opportunities for all of us. Nothing is changing in how we operate, and your jobs are secure." This is honest without confirming a sale.

Step 3: Reassure key customers. If a key customer has heard something, call them personally. Don't wait for them to come to you. Tell them that you're committed to the relationship, that any changes would only happen in a way that strengthens the service they receive, and that you're not going anywhere tomorrow. Most customers care about continuity of service, not who owns the company.

Step 4: Lock down the leak. Figure out where the breach came from and close it. If it was a buyer, remind them of their NDA obligations and consider limiting their access going forward. If it was an internal source, bring that person into confidence with a stay bonus and a clear understanding of the consequences of further disclosure.

Step 5: Inform your buyer. If you have an active buyer, tell them about the breach. They need to know because it could affect the business's value, employee retention, and customer stability. A good buyer will work with you to manage the situation. A buyer who tries to use the breach as a bargaining chip for a lower price is not someone you want to sell to.

Step 6: Document everything. If the breach came from someone who signed an NDA, document the breach and the damages. Even if you don't pursue legal action immediately, having a record protects you if the deal falls through and you need to seek damages.

Working With a Broker to Protect Confidentiality

One of the primary reasons sellers hire brokers is confidentiality protection. A good broker acts as a buffer between you and the market, and that buffer is worth its weight in gold.

Here's specifically how a broker protects your confidentiality.

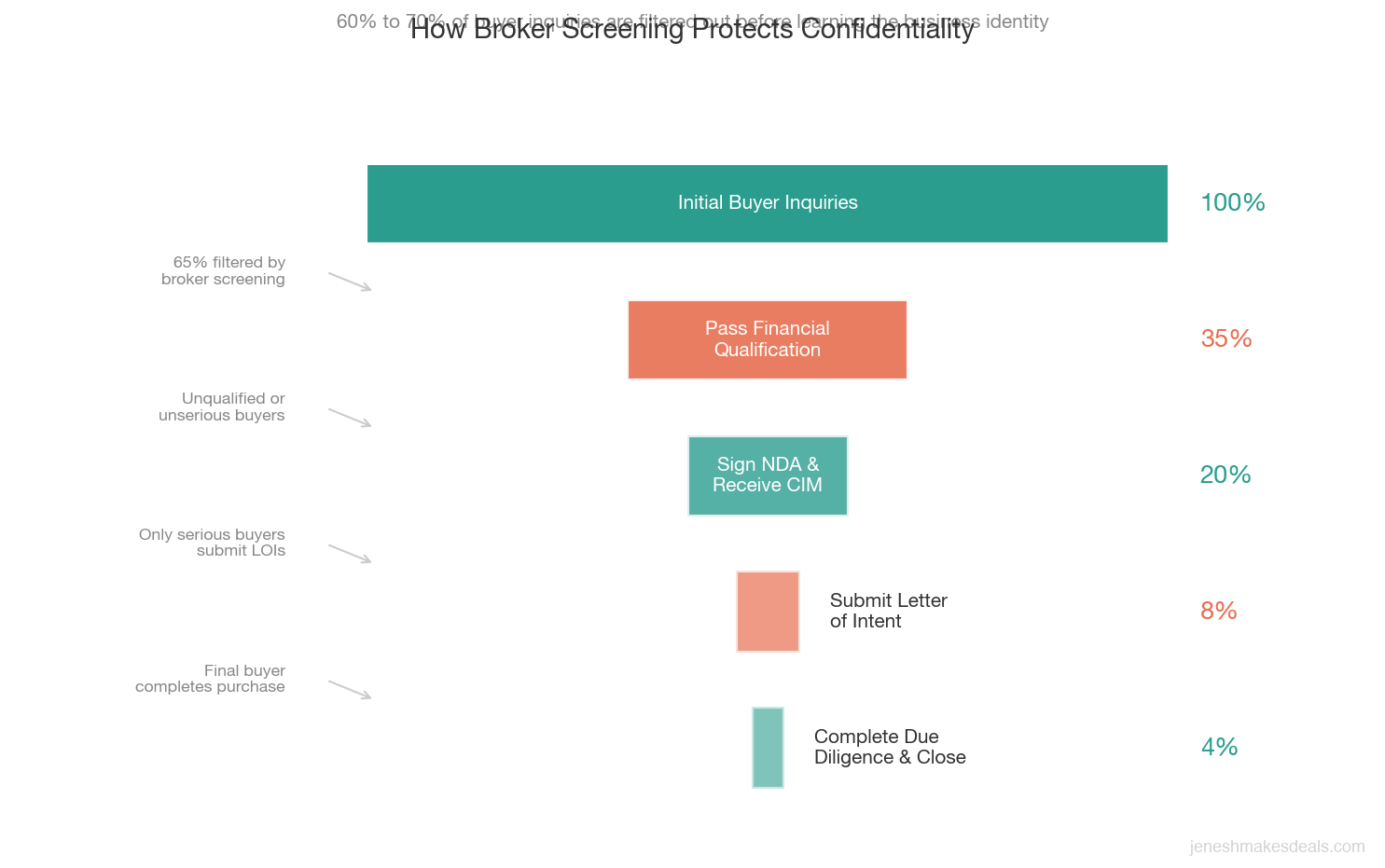

Buyer screening. Before any buyer learns your business name, they go through a qualification process. I verify their financial capacity, their experience, their motivation for buying, and whether they're a competitor or someone connected to your industry. This is the process of screening buyers properly, and it eliminates tire kickers and people who might use your information against you. Roughly 60% to 70% of initial buyer inquiries get filtered out during this stage.

Information control. All sensitive documents go through the broker. The buyer never gets raw files with your company name or metadata. Financial summaries are reformatted. Customer lists are anonymized until appropriate. This controlled distribution means you always know exactly who has seen what.

Communication management. The broker handles all buyer communication, which means you don't get random calls or emails that your assistant or employees might see. Everything flows through a separate, secure channel.

Cover stories and scheduling. An experienced broker knows how to schedule site visits, management meetings, and due diligence sessions without raising red flags. They've done it hundreds of times and know what works.

NDA enforcement. If a buyer breaches confidentiality, the broker follows up immediately. Having a professional intermediary handle this is much more effective than doing it yourself, especially if emotions are running high.

A broker's buyer screening alone filters out 60% to 70% of inquiries before anyone learns your business name. That single step prevents the majority of potential confidentiality breaches.

The cost of a broker (typically 8% to 12% of the sale price for small businesses) is easily justified by the confidentiality protection alone. I've seen deals where a broker's confidentiality management preserved hundreds of thousands of dollars in value that would have been lost to employee departures, customer attrition, or supplier changes.

Ready to sell your business confidentially? Contact us for a free consultation and I'll show you exactly how we keep your sale under wraps from start to finish.

Putting It All Together

Maintaining confidentiality when selling your business isn't about one big thing. It's about dozens of small decisions made correctly over a period of months.

Start by accepting that the default should be silence. Nobody knows unless they need to know. Your spouse or partner should know. Your attorney and accountant should know. Your broker should know. That's it. Everyone else finds out on a need to know basis, and most people don't need to know until the deal is closed.

Use a staged disclosure process so that sensitive information is only shared with qualified, committed buyers. Use blind listings and teaser profiles to market without revealing your identity. Maintain your normal routine at work. Don't talk about the sale at industry events, family gatherings, or on social media.

And if something goes wrong and confidentiality is breached, don't panic. Move quickly, address rumors directly, reassure the people who matter most, and lock down the source.

Selling a business is one of the most significant financial events of your life. The way you handle confidentiality can mean the difference between getting full value and watching your business lose value in real time as word spreads.

Ready to explore what your business could sell for? Contact us for a confidential conversation. Everything we discuss stays between us. You can also download our free Complete Guide to Selling Your Business in 2026 to see how confidentiality fits into the broader selling process.

Related Articles

April 16, 2026

Preparing Your Business for Sale: The 12 Month Checklist

The best time to start preparing your business for sale is 12 months out. Here's exactly what to do each quarter.

April 12, 2026

How to Handle Multiple Offers on Your Business

Multiple offers are a great problem to have. But picking the wrong one can cost you months and thousands. Here's how to evaluate them.

April 9, 2026

Best Time of Year to List Your Business for Sale

Timing your listing right can mean more buyers, better offers, and a faster close. Here's what the data says about when to go to market.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.