You signed the papers. The wire transfer hit your account. The business is sold.

Now what?

Here's what most sellers don't realize until it's too late: the deal isn't really done at closing. The 30 to 90 days after you hand over the keys are some of the most important days of the entire transaction. I've seen deals that looked perfect on paper fall apart during the transition because the seller checked out too early, or the buyer got overwhelmed, or nobody planned for how the handoff would actually work.

The transition period is where your reputation, your earn out payments, and sometimes even the deal itself live or die. Let me walk you through how to handle it the right way.

The Transition Period Is Part of the Deal

If you're selling a business, you need to understand something upfront: the transition period isn't a favor you're doing for the buyer. It's a contractual obligation baked into virtually every purchase agreement.

Most deals include a transition period of 30 to 90 days. For businesses with complex operations, seasonal cycles, or key customer relationships, it can stretch to 6 months or even a year. During this time, you're expected to help the buyer learn how the business operates, introduce them to important relationships, and transfer institutional knowledge that only lives in your head.

I tell every seller I work with to think of the transition as the final chapter of the deal, not an afterthought. If you mess this up, you could face legal disputes, clawback provisions, or damage to your professional reputation. And if you have an earnout tied to the sale, a rocky transition can directly cost you money.

The transition is where you prove the business is everything you said it was. Take it seriously.

The sellers who treat the transition as a box to check are the ones who end up in disputes six months later. The sellers who treat it as the final, most important deliverable of the deal are the ones who walk away clean and keep their reputation intact.

What a Typical Transition Agreement Includes

Before closing, your purchase agreement should spell out exactly what the transition looks like. If it doesn't, that's a red flag. Here's what a solid transition agreement covers.

Duration and hours. Most agreements specify a set number of hours per week over a defined period. A common structure is 20 hours per week for the first 30 days, then 10 hours per week for the next 60 days. Some deals taper down gradually. Others set a flat commitment.

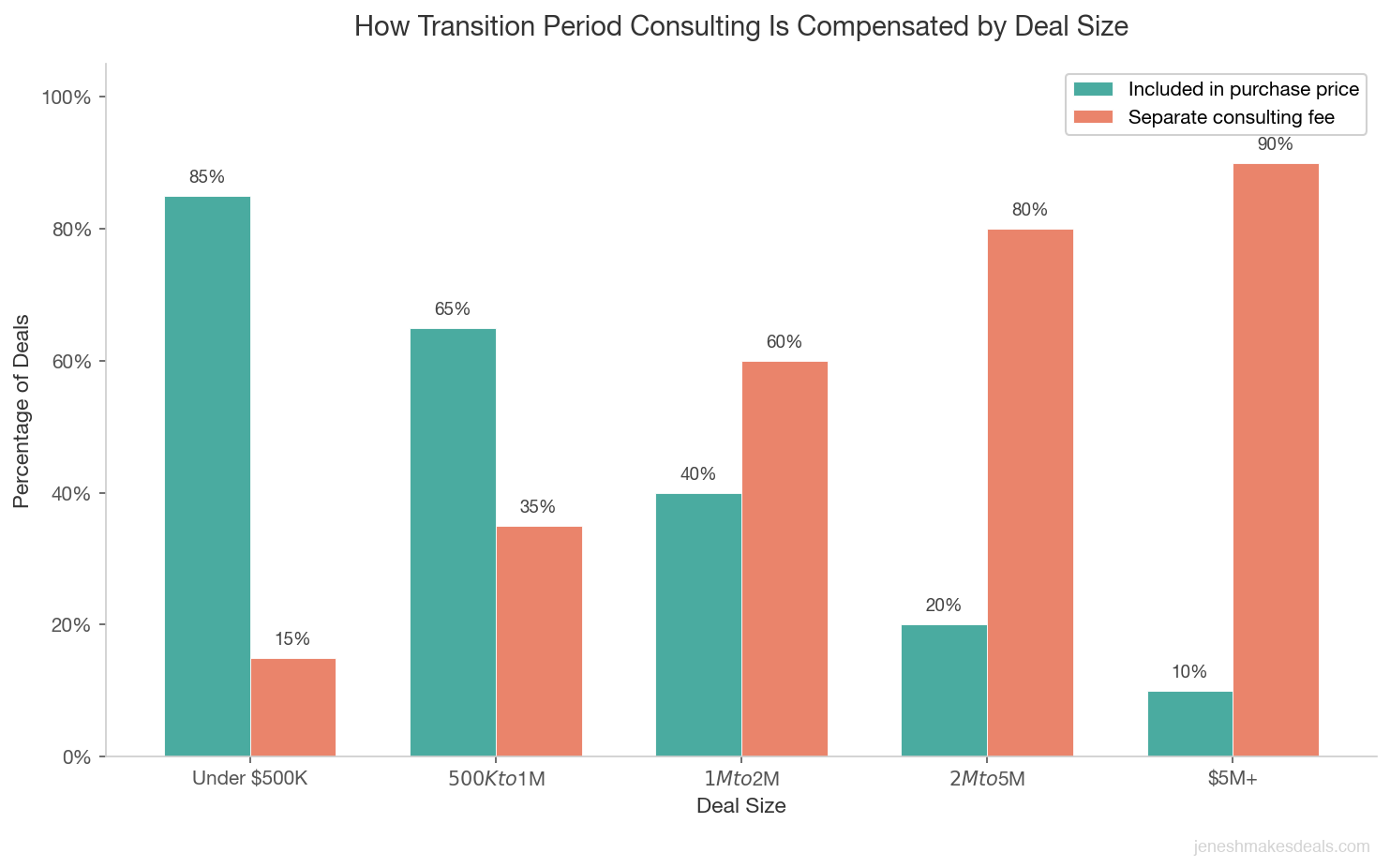

Compensation. In many small business sales under $2 million, the transition period is included in the purchase price. The seller doesn't get paid extra for their time. For larger deals, the seller might receive a separate consulting fee, typically $100 to $250 per hour or a monthly retainer of $5,000 to $15,000. This should be spelled out in the agreement.

Scope of work. The agreement should define what you're responsible for. Common items include training on day to day operations, introducing the buyer to customers and vendors, transferring systems access and passwords, explaining financial reporting, and walking through any seasonal patterns or cyclical workflows.

Availability and communication. How will you be available? On site? By phone? Email only after the first 30 days? Spell it out. I've seen disputes erupt because the buyer expected the seller to be on site five days a week and the seller thought phone calls would suffice.

Non compete provisions. Most transition agreements are paired with a non compete clause, usually 2 to 5 years within a defined geographic area. This is standard and protects the buyer's investment.

Get all of this in writing before you close. Verbal understandings have a way of becoming misunderstandings.

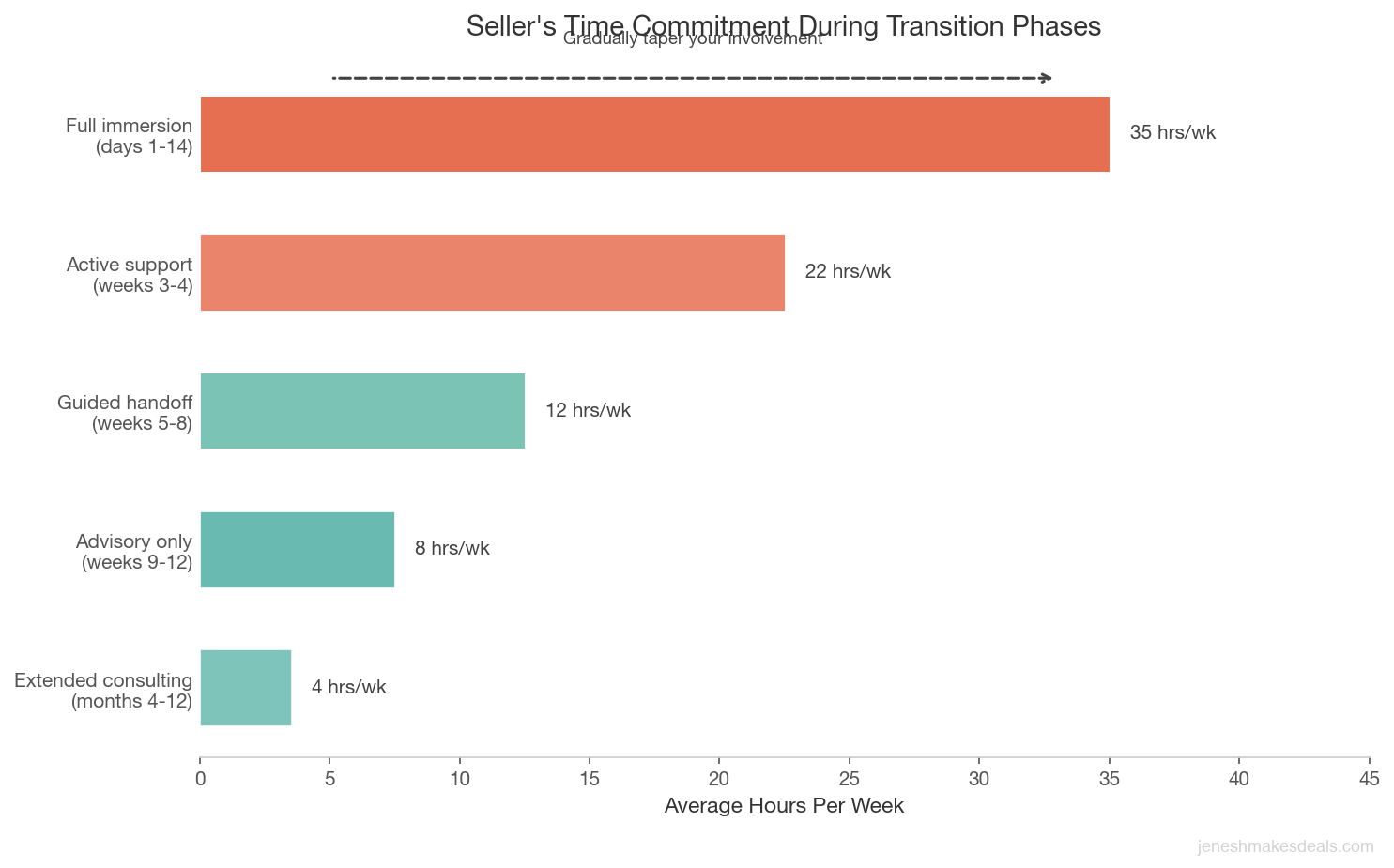

| Transition Phase | Timeframe | Seller's Role | Hours Per Week |

|---|---|---|---|

| Full immersion | Days 1 to 14 | On site daily, shadow training, lead all introductions | 30 to 40 |

| Active support | Weeks 3 to 4 | On site 3 days per week, buyer leads with seller backup | 20 to 25 |

| Guided handoff | Weeks 5 to 8 | On site 1 to 2 days, available by phone for questions | 10 to 15 |

| Advisory only | Weeks 9 to 12 | Phone and email support, scheduled weekly check ins | 5 to 10 |

| Extended consulting (if applicable) | Months 4 to 12 | Monthly calls, available for specific issues as needed | 2 to 5 |

Introducing the New Owner to Customers

This is the part that makes most sellers nervous, and for good reason. Your customer relationships are probably the most valuable asset you're transferring. Handle the introductions poorly and customers bolt. Handle them well and the buyer inherits a loyal customer base.

Timing matters. Don't tell customers about the sale before closing. Deals fall apart all the time, and if your customers hear you're selling and then the deal dies, you've created unnecessary anxiety. Wait until the ink is dry.

Frame it as a positive. Customers don't want to hear that you're cashing out. They want to know that the business will continue to serve them well. Here's a script that works:

"I'm excited to let you know that [Business Name] is entering a new chapter. [New Owner] is taking over, and I've been really impressed with their background in [relevant experience]. I'll be working closely with them over the next few months to make sure everything continues running smoothly. You're in great hands."

Do it in person when possible. For your top 10 to 20 customers (the ones who generate 80% of revenue), schedule face to face meetings or at minimum phone calls. Don't send a mass email to your best customers. That feels impersonal and signals that you don't care enough to have a conversation.

Let the buyer lead. After the initial introduction, step back. The goal is for the buyer to build their own relationship with the customer, not to keep the customer attached to you. I usually recommend that by week 3 or 4, the buyer should be the primary point of contact.

For one deal I worked on, the seller had a landscaping company with 150 residential accounts. We created a tiered introduction plan: personal phone calls to the top 30 accounts, a personalized letter to the next 50, and a general announcement to the rest. The buyer retained 92% of accounts through the first year. That's what good planning looks like.

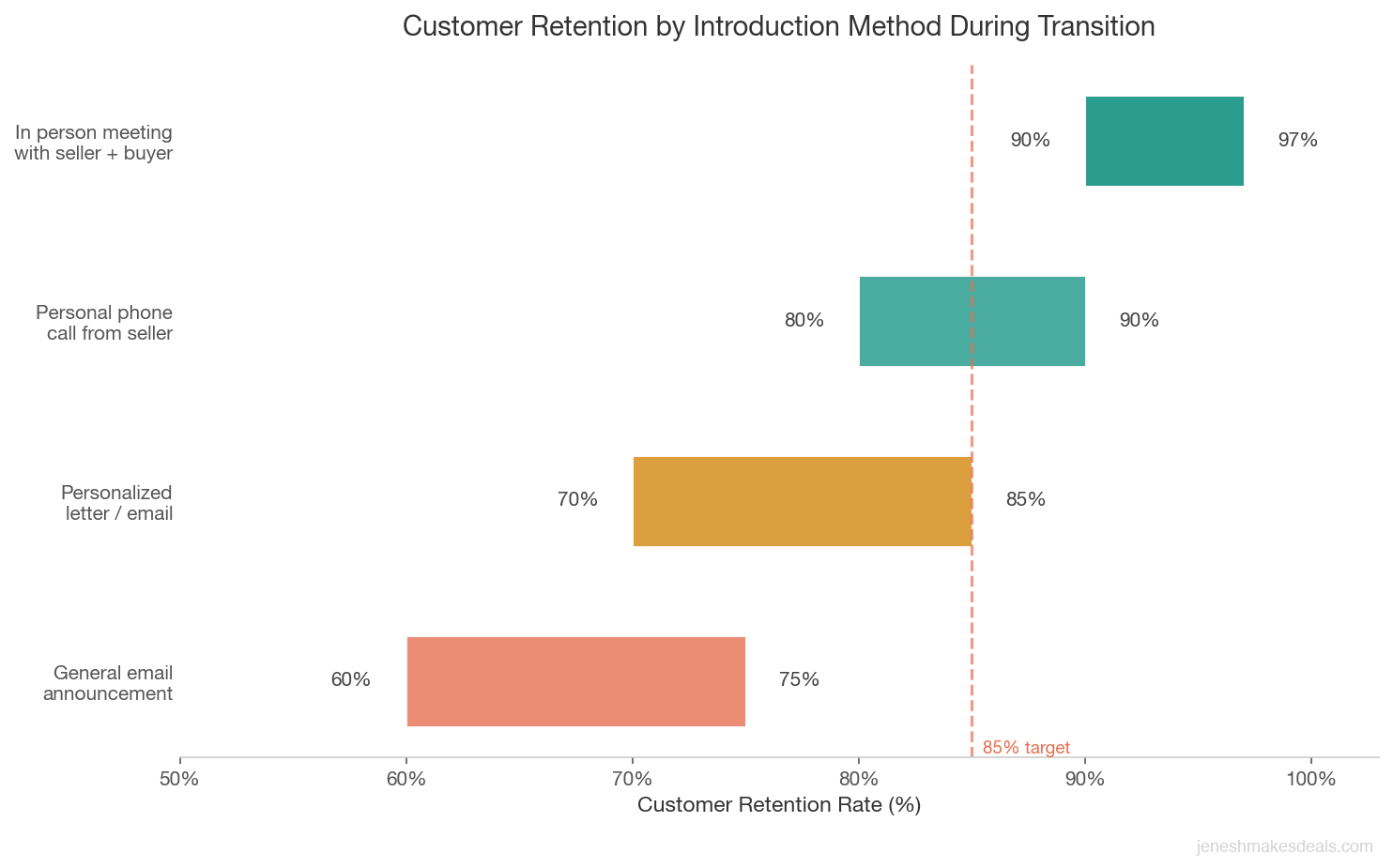

| Customer Tier | Introduction Method | Timing | Expected Retention |

|---|---|---|---|

| Top 10% by revenue | In person meeting with seller and buyer together | Week 1 | 90% or higher |

| Next 20% by revenue | Personal phone call from seller, followed by buyer outreach | Weeks 1 to 2 | 80% to 90% |

| Next 30% by revenue | Personalized letter or email from seller introducing buyer | Weeks 2 to 3 | 70% to 85% |

| Remaining 40% | General announcement email or newsletter | Weeks 3 to 4 | 60% to 75% |

Customer retention during the transition is the single best predictor of whether a deal succeeds long term. If the buyer loses 20% or more of accounts in the first 90 days, the business valuation you agreed on starts looking wrong very quickly. Invest the time in introductions. It protects your earn out and your reputation.

Introducing the New Owner to Vendors and Suppliers

Vendor introductions are less emotionally charged than customer introductions, but they come with their own complications.

Contract assignments. Some vendor contracts have assignment clauses that require the vendor's consent before the contract can be transferred to a new owner. Review every vendor contract before closing and identify which ones need formal approval. Start the approval process early because some vendors take 2 to 4 weeks to process assignment requests.

Credit terms. If you had net 30 or net 60 terms with suppliers, those terms were based on your credit history. The new owner may need to reapply or provide a personal guarantee. Warn the buyer about this early so they're not blindsided when a vendor demands payment upfront.

Personal relationships. If you have a great relationship with a key supplier who gives you preferential pricing or priority fulfillment, introduce the buyer directly. A warm handoff goes a long way. Tell the vendor something like: "This is [New Owner]. They're taking over the business and I want to make sure the relationship continues. They're great to work with."

Transition accounts and logins. Make a complete list of every vendor, their contact information, account numbers, login credentials, payment terms, and any special arrangements. Put it in a shared document and walk through it with the buyer.

I had a client who sold a printing business and forgot to transfer their paper supplier account. The buyer ran out of specialty paper stock two weeks in and had to scramble to set up a new account at higher prices. Don't let small details like this derail the transition.

Training the New Owner on Operations

This is the meat of the transition. You need to transfer everything you know about running the business, and you probably know a lot more than you think.

Create an operations manual. If you don't already have one (most small business owners don't), start building one before closing. Document your daily, weekly, monthly, and quarterly routines. Include step by step instructions for common tasks, troubleshooting guides, and contact information for everyone the business depends on.

A good operations manual covers:

- Opening and closing procedures

- Employee scheduling and payroll processes

- Inventory management and reorder points

- Customer service protocols and escalation procedures

- Equipment maintenance schedules

- Software systems and login credentials

- Financial reporting and bookkeeping workflows

- Seasonal patterns (when to ramp up hiring, when to stock inventory, etc.)

Shadow period. The most effective training I've seen involves a shadow period where the buyer works alongside you for the first 1 to 2 weeks. They see how you handle a difficult customer call. They watch you do the weekly inventory count. They sit in on a staff meeting. There's no substitute for seeing how the business actually runs in real time.

Systems and technology transfer. Make a list of every system the business uses: POS, accounting software, CRM, email marketing, social media accounts, website hosting, domain registrars. Transfer ownership or create new admin accounts for the buyer. Do this methodically because missing one login can cause problems weeks later.

The things you do without thinking. Every business owner has habits and routines they don't even realize are important. Maybe you always check the equipment before the first shift. Maybe you call your biggest customer every Friday. Maybe you know that the HVAC system acts up when the temperature drops below 40 degrees. Write these things down. They seem obvious to you, but the buyer has no idea.

Need help figuring out what your business is worth? Use our free business valuation calculator to get a quick estimate.

Managing Employee Concerns During Transition

Employees find out the business has been sold and their first thought is: "Am I going to lose my job?" That's natural. And how you handle their concerns during the transition will determine whether the buyer inherits a motivated team or a group of people already updating their resumes.

I've written about what happens to employees after a sale in detail, but here are the key points for the transition period specifically.

Tell employees as soon as possible after closing. Don't let them hear it through the grapevine. Call a team meeting within the first day or two and explain what's happening. Be honest about what you know and what you don't.

Reassure them, but don't make promises you can't keep. You can say, "The new owner plans to keep the team intact and is excited to work with everyone." You should not say, "Nobody is going to lose their job, I promise." That's not your promise to make anymore.

Introduce the new owner quickly. Employees want to see who's in charge now. Have the buyer attend that first team meeting. Let them say a few words about their background and their plans. First impressions matter enormously.

Step back and let the new owner lead. This is hard, especially if you're close with your employees. But the moment you sold the business, the reporting relationship changed. If employees keep coming to you with problems instead of the new owner, gently redirect them. Say, "That's a great question for [New Owner]. Let me walk you over to them."

Watch for flight risk. Key employees who feel uncertain might start job hunting. If the buyer wants to retain them, this is the time to discuss retention bonuses or new employment agreements. I've seen buyers lose a critical manager during the transition because nobody thought to have a conversation about their future with the company.

One seller I worked with had a restaurant with 25 employees. She held a team dinner the night before the official transition, introduced the new owner, and gave everyone a small gift card as a thank you for their years of service. That simple gesture set a positive tone for the entire transition. The new owner retained 22 of 25 employees through the first six months.

When Transition Goes Wrong

Not every transition is smooth. Here are the most common problems I see and how to handle them.

The buyer calls you 50 times a day. Some buyers get anxious and lean on the seller for every decision, no matter how small. If this happens, set boundaries early. Establish designated check in times (say, a 30 minute morning call and a 15 minute afternoon call) and redirect non urgent questions to those times. If the buyer genuinely needs more support, that's a conversation about extending the consulting agreement, not about you being available 24/7.

The buyer makes drastic changes immediately. New owners sometimes want to put their stamp on the business right away. They change the menu, fire a manager, renegotiate vendor contracts, or rebrand the website in week two. This can be jarring for employees and customers. As the seller, you can offer your perspective ("I'd suggest waiting 90 days before making major changes so you understand the baseline"), but you can't force them to listen. It's their business now.

The buyer blames you for problems. "You didn't tell me the roof leaks" or "You said this customer was loyal and they just canceled." Some of this is legitimate, some of it is a new owner looking for someone to blame when reality sets in. Document everything you disclose during the transition. Follow up verbal conversations with emails: "Per our conversation today, I showed you the maintenance log for the HVAC system and explained the service schedule." This protects you if disputes arise later.

The seller can't let go. Sometimes the problem is you. You keep showing up unannounced. You second guess the buyer's decisions. You tell employees, "That's not how we used to do it." If you catch yourself doing this, stop. You sold the business. Your job during the transition is to transfer knowledge, not to keep running things.

Ready to talk about selling? Contact us for a free consultation and we'll walk you through your options.

Extended Transition and Consulting Agreements

Some deals include an extended consulting agreement beyond the initial transition period. This is especially common when the seller has deep industry expertise, key customer relationships, or technical knowledge that takes months to transfer. If you're considering selling to an employee or family member, extended transitions are almost always part of the arrangement.

How long. Extended consulting agreements typically run 6 to 12 months, though I've seen some go up to 2 years for highly specialized businesses.

How to structure compensation. There are two common models. The first is an hourly rate, usually $100 to $300 per hour depending on the seller's expertise and the size of the business. The second is a monthly retainer, typically $3,000 to $15,000 per month for a set number of hours. I generally recommend monthly retainers because they create predictability for both parties.

Set declining hours. A good consulting agreement tapers off. Month 1 might be 40 hours. Month 3 might be 20 hours. Month 6 might be 5 hours. This forces the buyer to become self sufficient and prevents the seller from becoming a permanent crutch.

Define the scope clearly. "Available for consulting" is too vague. Specify what the consulting covers: strategic advice, customer relationship support, vendor negotiations, staff training. Exclude things like day to day management decisions, which should be the buyer's responsibility.

Know when to end it. Some sellers enjoy staying involved because they miss the work. Some buyers keep the seller around because they're afraid to fly solo. Neither of these is healthy long term. Set a firm end date and stick to it. A successful business transition means the buyer can run the business without you.

The Emotional Transition

This is the part nobody prepares for, and it hits harder than most sellers expect.

I've written about the emotional side of selling before, but the transition period brings its own specific emotional challenges. You're physically present in the business, watching someone else make decisions about something you built. It's like watching someone redecorate your childhood home.

The identity shift. For years, you've been "the owner of [Business Name]." People in the community know you by your business. Your daily routine revolved around it. Now you're... what, exactly? This identity vacuum is real and it catches a lot of sellers off guard. Some sellers describe the weeks after selling as feeling like retirement, even if they're only 45.

Watching someone do things differently. The new owner is going to do things you disagree with. They'll change the hours. They'll stop offering that product you loved. They'll reorganize the stockroom in a way that makes no sense to you. Unless they're violating the terms of the purchase agreement or doing something that affects your earn out, let it go. Different doesn't mean wrong.

The impulse to micromanage. You'll feel it. You'll want to say, "Actually, we always did it this way." Resist that impulse. Share your reasoning once. If the buyer chooses a different path, respect their decision. You hired them (in a sense) by agreeing to sell to them. Trust the process.

Give yourself something to look forward to. The sellers who handle the emotional transition best are the ones who already have a plan for what comes next. Maybe it's another business. Maybe it's travel. Maybe it's finally coaching your kid's baseball team. Having a next chapter makes it easier to close the current one.

One seller I worked with, a guy who owned an auto repair shop for 22 years, told me the hardest moment was the first Monday morning after the transition ended. He woke up at 5:30 AM out of habit, got dressed, and was halfway to the shop before he realized he had nowhere to go. He sat in a parking lot for 20 minutes. That story stuck with me because it's so common. Plan for those moments.

Protecting Yourself During Transition

The transition period can create legal exposure if you're not careful. Here's how to protect yourself.

Document everything. Every piece of information you share, every system you hand over, every customer introduction you make. Keep a running log. If the buyer later claims you withheld information or failed to properly train them, your documentation is your defense.

I tell every seller to send a brief daily email to the buyer summarizing what was covered that day during the transition. It takes five minutes and creates a paper trail that's saved more than one seller from a post closing dispute. If it's not in writing, it didn't happen.

Don't make verbal promises. If the buyer asks you to stay an extra two weeks beyond the agreement, don't just say, "Sure, no problem." Get it in writing. An amendment to the consulting agreement, even a simple email confirming the terms, protects both parties.

Stick to the agreement. If your transition agreement says 20 hours per week, don't work 40 because you feel guilty. If it says you'll train on operations but not on marketing strategy, don't volunteer extra services. Scope creep during the transition is one of the most common sources of post sale disputes.

Handle disputes through your attorney. If the buyer accuses you of misrepresentation, if they try to renegotiate terms after closing, or if they threaten to withhold an earn out payment, don't try to resolve it yourself. Call your attorney. That's why you have one.

Keep copies of everything. Before you hand over systems and accounts, make personal copies of any documentation that relates to the sale: the purchase agreement, transition agreement, financial disclosures, and your transition log. Store these securely. You may need them years later.

Tax implications. How the transition and consulting payments are structured affects your taxes. Consulting fees are taxed as ordinary income, which is different from how capital gains on the sale might be taxed. Make sure your CPA is involved in structuring these payments.

A Smooth Transition Protects Everyone

The transition period isn't glamorous. It's not the exciting part of selling a business. But it's the part that determines whether the deal actually works long term. A seller who handles the transition well walks away with a clean break, a solid reputation, and the satisfaction of knowing they set the buyer up for success. A seller who phones it in risks legal disputes, damaged relationships, and a deal that unravels.

Here's my checklist for a successful transition:

- Get the transition agreement in writing with clear hours, duration, scope, and compensation

- Create or update an operations manual before closing

- Plan customer and vendor introductions in advance with a tiered approach

- Communicate with employees honestly and quickly after closing

- Set boundaries on your availability and stick to them

- Document everything you do during the transition

- Let the new owner lead, even when it's hard to watch

- Plan your own next chapter so you have something to move toward

If you're thinking about selling your business and want to understand what the process looks like from start to finish, I'm happy to walk you through it.

Ready to explore your options? Contact us for a free consultation and we'll help you plan a transition that works for everyone involved.

Related Articles

April 16, 2026

Preparing Your Business for Sale: The 12 Month Checklist

The best time to start preparing your business for sale is 12 months out. Here's exactly what to do each quarter.

April 12, 2026

How to Handle Multiple Offers on Your Business

Multiple offers are a great problem to have. But picking the wrong one can cost you months and thousands. Here's how to evaluate them.

April 9, 2026

Best Time of Year to List Your Business for Sale

Timing your listing right can mean more buyers, better offers, and a faster close. Here's what the data says about when to go to market.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.