You accepted an offer. The letter of intent is signed. You're mentally spending the proceeds. Then due diligence starts, and everything falls apart.

I've watched it happen dozens of times. A seller gets a strong offer, celebrates too early, and then fumbles the due diligence phase so badly that the buyer walks away or renegotiates the price down by 20%. It's painful to watch because most of these mistakes are completely avoidable.

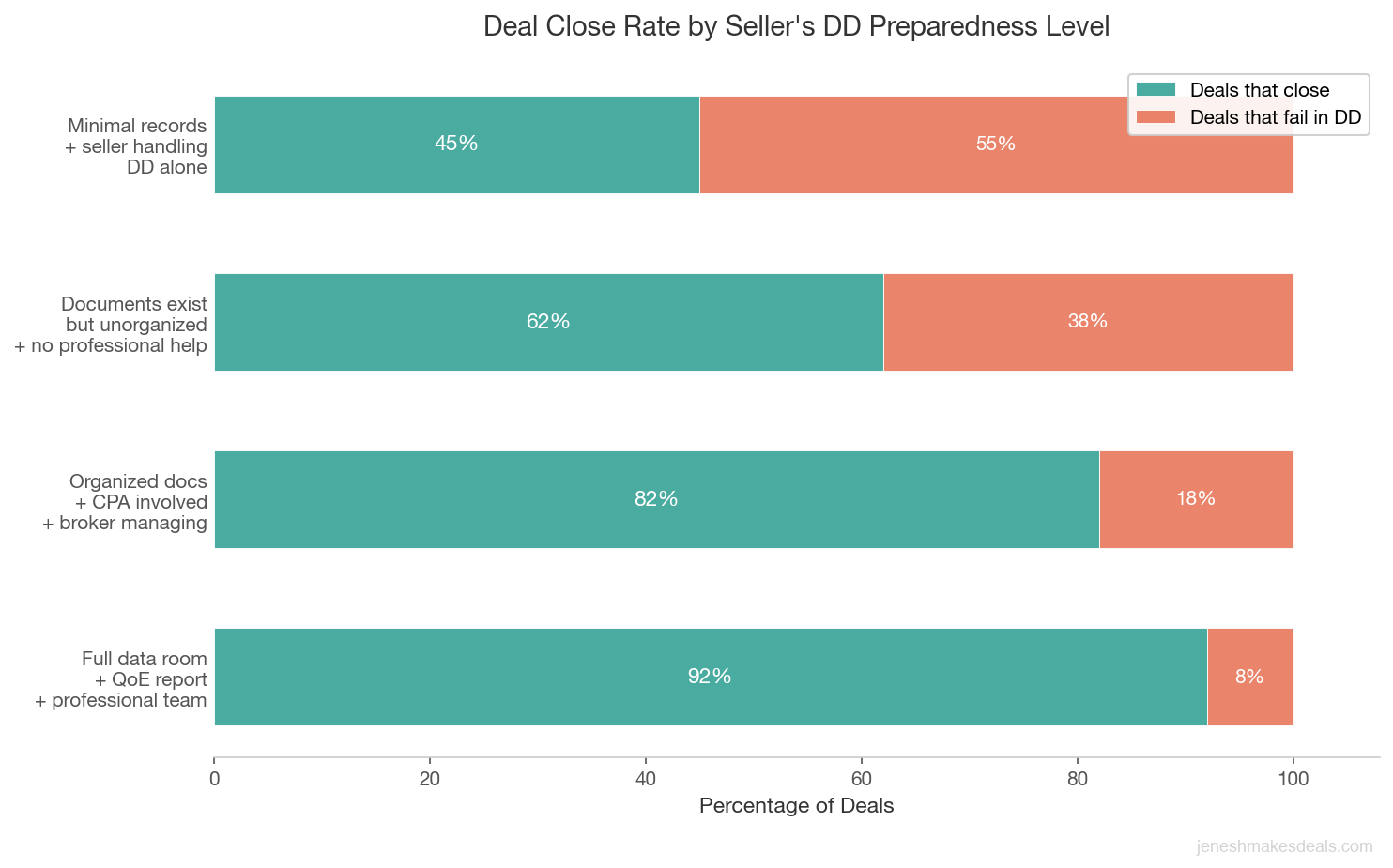

Here's the reality: somewhere between 30% and 50% of small business deals that reach the LOI stage never make it to closing. The number one reason isn't price disagreements. It's what happens during due diligence. Sellers either can't produce what buyers need, they try to hide problems, or they sabotage their own deal through carelessness and ego.

I'm going to walk you through the eight mistakes I see sellers make most often during DD, and exactly how to avoid each one.

Why Due Diligence Is Where Deals Die

Due diligence is the buyer's chance to verify that everything you told them about your business is actually true. They're going to dig through your financials, talk to your landlord, review your contracts, and look under every rock they can find. This isn't personal. It's business.

Most sellers don't realize how intense this process gets. A typical buyer or their advisor will request 50 to 150 individual documents. They'll ask questions that feel invasive. They'll challenge your numbers. They'll want explanations for every revenue dip and every unusual expense.

The deals that close smoothly are the ones where the seller was prepared, honest, and professional throughout. The deals that blow up are the ones where the seller got sloppy, secretive, or emotional. If you want a deeper look at what buyers are actually looking for, check out this due diligence checklist written from the buyer's perspective.

Broker insight: Due diligence is not the buyer attacking your business. It's the buyer building confidence to write you a very large check. Every document you produce quickly and every question you answer clearly moves them closer to closing. Every delay and every vague answer moves them closer to the exit.

Let me break down each mistake so you can avoid them.

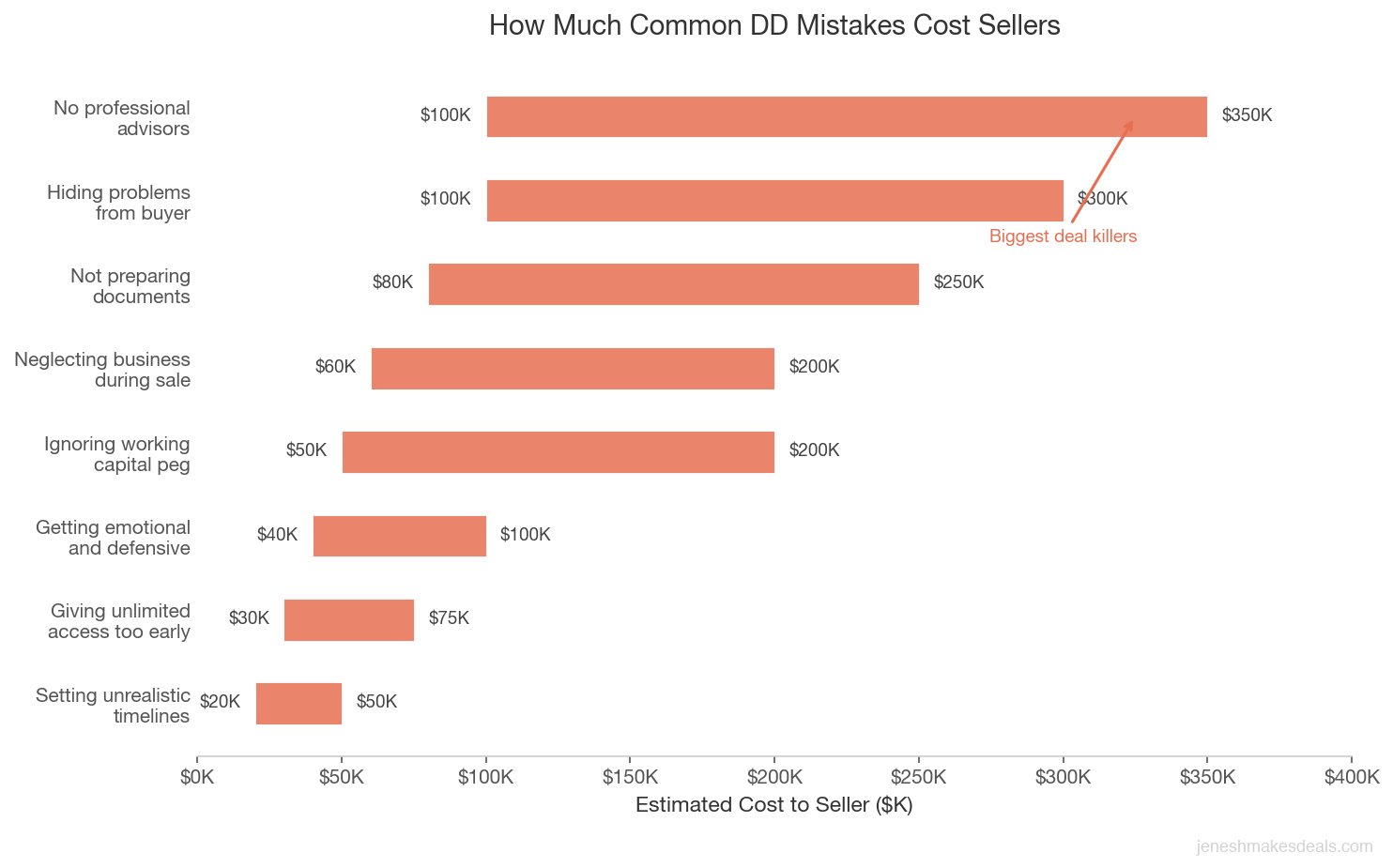

Mistake 1: Not Preparing Documents in Advance

This is the most common mistake I see, and it's the easiest to fix. A buyer submits their document request list on day one of due diligence. The seller looks at the list of 80 items and panics because half the documents are buried in filing cabinets, stored on an old laptop, or simply don't exist in any organized form.

Here's what a typical DD request includes:

- Three years of federal and state tax returns

- Monthly profit and loss statements for the trailing 24 months

- Balance sheets for the last three fiscal years

- Accounts receivable and accounts payable aging reports

- All lease agreements (real estate, equipment, vehicles)

- Employee roster with compensation, hire dates, and roles

- Customer contracts and revenue concentration data

- Vendor agreements and supplier contracts

- Insurance policies and claims history

- Permits, licenses, and regulatory compliance records

When a seller takes two weeks to produce basic tax returns, it sends a terrible signal. The buyer starts wondering what else is disorganized. They question whether the financials they've already seen are accurate. Every delay gives the buyer more time to get cold feet or find another deal.

I had a client last year who lost a $1.2 million deal because he couldn't produce clean P&L statements going back more than 18 months. His bookkeeper had quit, the QuickBooks file was a mess, and it took his CPA six weeks to reconstruct the financials. By then, the buyer had moved on to another acquisition.

The fix is simple: start preparing your financials at least six months before you list your business. Get your books cleaned up, your documents organized, and your data room ready before a single buyer walks through the door.

Mistake 2: Hiding Problems Instead of Addressing Them

Every business has problems. Every single one. Maybe revenue dipped 15% last quarter because you lost a key customer. Maybe there's an outstanding workers' comp claim. Maybe your biggest client represents 40% of revenue and their contract expires in eight months.

Sellers who try to hide these issues are making a catastrophic mistake. Buyers will find out. They always do. That's literally the point of due diligence.

Here's what happens when a buyer discovers something you tried to conceal: they lose trust. And once trust is gone in a business transaction, it almost never comes back. A buyer who finds a hidden liability doesn't just worry about that one issue. They start wondering what else you're hiding. Suddenly every number gets scrutinized three times. Every explanation gets questioned. The entire deal falls under a cloud of suspicion.

The better approach is proactive disclosure with context. If revenue dropped last Q3, explain why and show what you did to fix it. If there's pending litigation, present it with your attorney's assessment of the likely outcome. If customer concentration is high, show the pipeline of new customers you've been developing.

I've seen sellers disclose serious problems and still close at their asking price because they handled it right. One seller I worked with had an EPA compliance issue at his manufacturing facility. Instead of hiding it, he disclosed it in the first meeting, presented the remediation plan with cost estimates, and even got a contractor bid for the cleanup. The buyer respected the transparency and factored the cost into the deal structure rather than walking away.

Need help figuring out what your business is worth? Use our free business valuation calculator to get a quick estimate, even with issues factored in.

Mistake 3: Getting Emotional and Defensive

You built this business from nothing. You worked 70 hour weeks for years. You sacrificed vacations, missed your kid's soccer games, and poured everything you had into making it work. I get it. This business is your identity.

But when a buyer asks, "Why did margins decline from 22% to 18% over the last two years?" the wrong answer is, "Are you calling me a liar? My numbers are solid." The right answer is, "Good question. We invested in two new hires ahead of revenue growth, and raw material costs increased 8%. Here's the data showing margins recovering over the last two quarters."

Buyers aren't attacking you when they ask tough questions. They're protecting a six or seven figure investment. If someone was about to hand you $800,000, wouldn't you ask hard questions too?

I coach my sellers to treat DD questions like a job interview. Stay professional. Answer with data, not emotion. If you don't know the answer, say so and commit to getting it within 48 hours. Never guess. Never bluff.

The sellers who stay calm and factual during due diligence close faster and at higher prices. The sellers who get defensive create friction that slows everything down and often leads to price reductions.

Key takeaway: The moment you get defensive during due diligence, you start costing yourself money. Buyers read emotion as a signal that something is wrong. Data shuts down doubt. Defensiveness amplifies it. Put your ego aside and let the numbers do the talking.

One practical tip: designate someone other than yourself to handle DD communications. Your broker, your attorney, or your CFO. Having a buffer between you and the buyer's pointed questions prevents emotional reactions from derailing the deal.

Mistake 4: Neglecting the Business During the Sale

This one is a deal killer that sneaks up on sellers. The sale process is consuming. Between document requests, buyer meetings, attorney calls, and the general stress of it all, it's easy to take your eye off the ball. Revenue starts slipping. Customer service quality drops. Key employees sense something is off and start updating their resumes.

Here's the problem: buyers are watching your numbers in real time. Most purchase agreements include a requirement that you deliver monthly financials through closing. If your trailing three month revenue drops 10% during DD, the buyer has every right to renegotiate the price. And they will.

I had a deal where the seller's revenue dropped $40,000 per month during the 60 day DD period because he was spending all his time on the sale instead of running the business. The buyer used that decline to negotiate a $200,000 price reduction. The seller essentially paid $200,000 for the privilege of being distracted.

The solution is to build a team around the sale. Delegate more day to day operations to your managers. Hire a temporary operations person if you need to. Whatever it costs to maintain business performance during DD is a fraction of what you'll lose if revenue slips.

Your business needs to be running at peak performance right up until the day you hand over the keys. That's true whether the deal is structured as an asset sale vs stock sale. Either way, the buyer is paying for a going concern that's performing at the level you represented.

Mistake 5: Giving Buyers Unlimited Access Too Early

Information is power in any negotiation, and too many sellers hand over everything at once to buyers who haven't even secured financing. I've seen sellers email their entire customer list, vendor contracts, and proprietary processes to someone who signed an NDA three days ago and hasn't shown a single proof of funds.

This is dangerous for several reasons. First, not every buyer is a real buyer. Some are competitors fishing for intelligence. Some are tire kickers who will never close. Sharing sensitive business information with unqualified buyers exposes you to competitive risk with zero upside.

Second, even legitimate buyers don't need everything at once. Due diligence should be staged. There's a natural progression that protects the seller while still giving the buyer what they need to make informed decisions.

Here's how I structure information release:

Stage 1 (Before LOI): High level financials, summary P&L, general business description, reason for sale. Enough for the buyer to make an initial offer.

Stage 2 (After LOI, before DD): Detailed tax returns, full P&L and balance sheets, lease summary, employee count and general roles. Buyer must show proof of funds or financing pre approval.

Stage 3 (During DD): Customer lists (with revenue by customer), vendor contracts, employee details with compensation, proprietary processes, IT systems. Buyer must have financing commitment and escrow deposit.

Stage 4 (Pre closing): Trade secrets, passwords, key customer introductions. Only after all contingencies are removed.

| Stage | Timing | Documents Shared | Buyer Must Provide |

|---|---|---|---|

| Stage 1 | Before LOI | Summary P&L, high level financials, business overview | Signed NDA |

| Stage 2 | After LOI, before DD | Tax returns, full P&L and balance sheets, lease summary, employee count | Proof of funds or financing pre approval |

| Stage 3 | During DD | Customer lists with revenue, vendor contracts, employee compensation, IT systems | Financing commitment and escrow deposit |

| Stage 4 | Pre closing | Trade secrets, passwords, key customer introductions | All contingencies removed |

This staged approach protects you while keeping the deal moving forward. Any buyer who insists on seeing your full customer list before they've proven they can actually close the deal is a red flag.

Ready to talk about selling? Contact us for a free consultation and we'll walk you through how to protect your information during the sale process.

Mistake 6: Not Having Professional Help

Selling a business is not a DIY project. I don't care how smart you are or how well you know your business. The legal, financial, and strategic complexities of a business sale require professional help. Period.

Here's the team you need during due diligence:

A business broker or M&A advisor who manages the process, coordinates between parties, and keeps the deal on track. That's where I come in. A good broker has seen hundreds of DD processes and knows exactly what's normal and what's a red flag.

A transaction attorney who reviews the purchase agreement, handles legal due diligence responses, and protects your interests in the contract language. Your cousin who does real estate closings doesn't count. You need someone who specializes in business transactions.

A CPA or financial advisor who can prepare clean financial statements, explain adjustments like owner add backs, and respond to the buyer's financial questions with authority. Your bookkeeper who does your monthly reconciliation might not be enough here.

I've seen sellers try to save $15,000 to $30,000 in professional fees by handling DD themselves, and then lose $100,000 or more because they missed a liability in the purchase agreement, agreed to an earnout structure they didn't understand, or failed to negotiate proper indemnification caps.

The purchase agreement alone can be 40 to 60 pages of dense legal language. Representations and warranties, indemnification provisions, non compete terms, transition requirements. Missing a single clause can cost you more than your entire professional fee budget.

Mistake 7: Ignoring the Working Capital Negotiation

This is the mistake that catches even experienced sellers off guard. Most buyers expect the business to come with a certain level of working capital, and the negotiation around this number can shift the effective purchase price by $50,000 to $500,000 depending on the size of the deal.

Working capital is basically your current assets minus your current liabilities. It's the cash, inventory, accounts receivable, and prepaid expenses that keep the business running day to day, minus the accounts payable, accrued expenses, and other short term obligations.

Here's how it typically works: during DD, the buyer and seller agree on a "peg" amount for working capital. This is the target level that should be in the business at closing. If actual working capital at closing is above the peg, the buyer pays the seller the difference. If it's below, the seller pays the buyer. This is called a "true up" and it usually happens 60 to 90 days after closing, once the final numbers are calculated.

The mistake sellers make is either not understanding how the peg is calculated or not paying attention to it until it's too late. I've seen sellers agree to a peg based on a 12 month average when the last three months had unusually high working capital, costing them $80,000 at true up. I've also seen sellers drain working capital before closing by pulling out cash and delaying payables, which triggers a true up that wipes out a chunk of their proceeds.

Work with your CPA to understand your trailing 12 month working capital levels. Know what's normal for your business. Negotiate the peg based on an appropriate time period, and don't artificially manipulate your working capital in the months before closing. Buyers and their accountants will catch it.

Warning: Working capital is the most overlooked number in deal negotiations. I have seen sellers lose $50,000 to $100,000 at the true up because they didn't understand how the peg was calculated or they drained cash in the weeks before closing. Know your working capital numbers cold before you negotiate this provision.

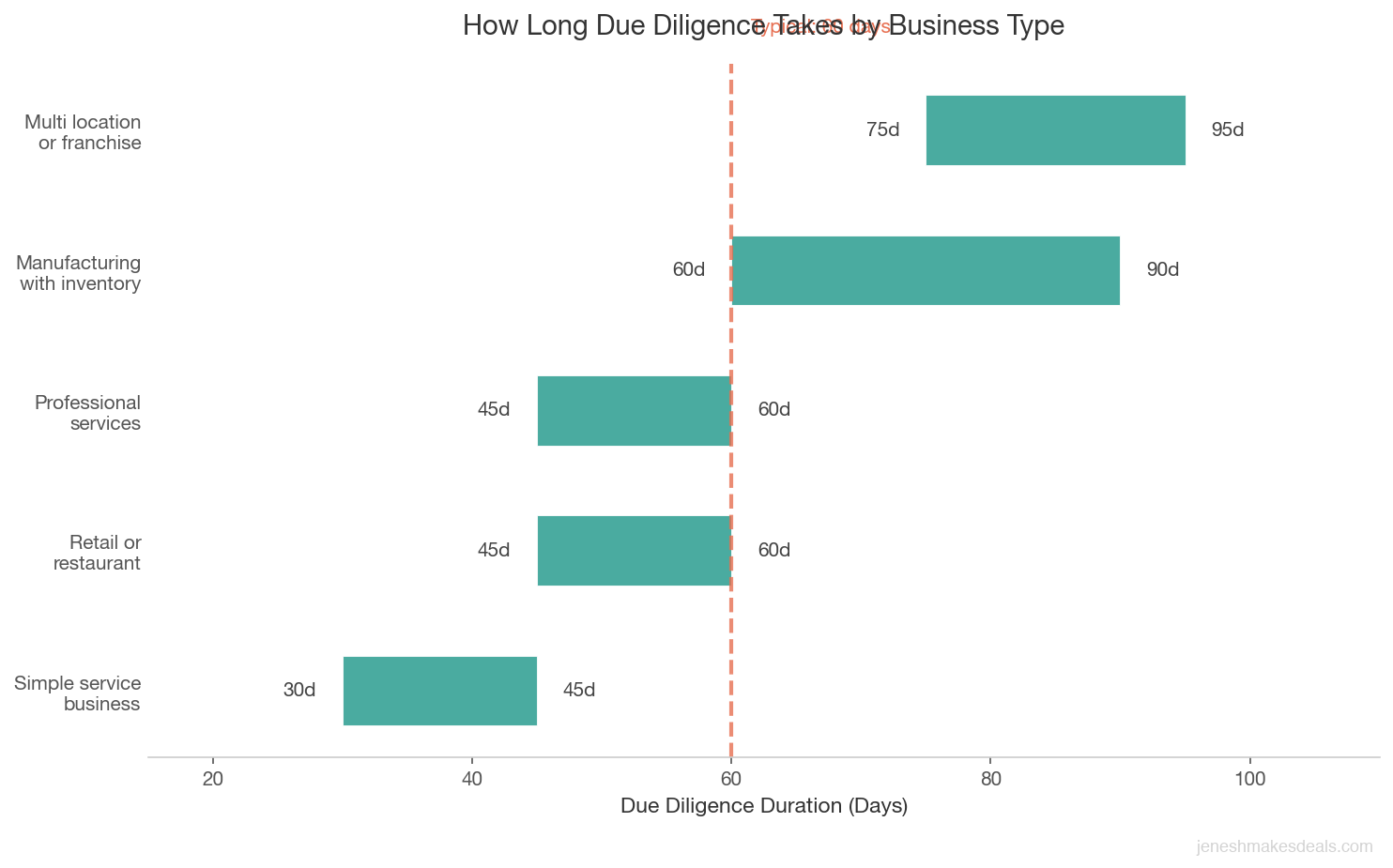

Mistake 8: Setting Unrealistic Timelines

Due diligence typically takes 30 to 90 days, depending on the complexity of the business. A simple service business with clean books might close DD in 30 days. A manufacturing company with environmental considerations, multiple real estate locations, and complex inventory might need 90 days or more.

Sellers make timeline mistakes in both directions.

| Business Type | Typical DD Duration | Key Factors That Add Time |

|---|---|---|

| Simple service business with clean books | 30 to 45 days | Few if any physical assets, limited contracts |

| Retail or restaurant with lease | 45 to 60 days | Lease review, inventory verification, permits |

| Professional services (accounting, consulting) | 45 to 60 days | Client contract review, key person assessment |

| Manufacturing with equipment and inventory | 60 to 90 days | Equipment appraisal, inventory audit, environmental review |

| Multi location or franchise business | 75 to 90+ days | Multiple leases, franchise agreement review, state by state compliance |

Rushing DD creates suspicion. When a seller pushes for a 15 day DD period on a $2 million deal, the buyer immediately wonders why. What are they trying to prevent the buyer from finding? Aggressive timelines also increase the chance of mistakes on both sides. A buyer who feels rushed is more likely to walk away than to close faster.

Dragging out DD kills momentum. Every extra week adds risk. The buyer's financing commitment might expire. Interest rates could change. A competitor might approach the buyer with a different deal. The buyer's spouse might get cold feet. I've seen deals die simply because they took too long and life circumstances changed.

The right approach is to agree on a reasonable timeline upfront, build in specific milestones (financial review by day 15, legal review by day 30, etc.), and hold both sides accountable. Your broker should be managing this timeline actively, following up on outstanding items, and flagging delays before they become deal breakers.

If the buyer asks for a reasonable extension because they're waiting on a third party report or their lender needs additional documentation, grant it. Flexibility on minor timeline issues shows good faith. But open ended extensions with no specific end date are a warning sign that the buyer may be losing interest.

How to Prepare for Due Diligence Before You Even List

The best way to survive DD is to prepare for it before you ever go to market. Here's my recommended prep checklist:

Build a virtual data room. Set up a secure, organized folder structure with all the documents a buyer will request. Use a platform like Google Drive, Dropbox, or a dedicated data room service. Organize by category: financials, legal, operations, HR, real estate, customers, vendors. Our seller due diligence checklist tool can help you track every item you need to prepare.

Get a quality of earnings report. For deals over $1 million, consider getting a sell side quality of earnings report done before listing. This is a third party financial analysis that validates your adjusted EBITDA. It's expensive ($15,000 to $30,000) but it dramatically accelerates DD and gives buyers confidence in your numbers.

Fix known issues now. If your lease expires in six months, negotiate the renewal before listing. If you have an outstanding legal dispute, resolve it. If your books are messy, get them cleaned up. Every issue you fix before DD is one less thing that can derail or delay your deal.

Brief your key team members. Decide who on your team will know about the sale and what role they'll play during DD. Your controller or bookkeeper will need to produce financial data. Your operations manager may need to answer questions about processes. Prepare them without creating panic.

Document your processes. Buyers want to know the business can run without you. Create standard operating procedures for key functions. Document customer relationships, vendor arrangements, and operational workflows. This isn't just good for DD. It actually increases the value of your business.

Know your numbers cold. You should be able to explain every line item on your P&L and every significant balance sheet item without hesitation. If your insurance costs jumped 30% last year, know why. If a major customer's revenue dropped, know the story. Hesitation or vague answers during DD erode buyer confidence.

Ready to talk about selling? Contact us for a free consultation and we'll help you build a DD prep plan specific to your business.

The Bottom Line

Due diligence doesn't have to be the phase where your deal falls apart. It can actually be the phase where the buyer's confidence grows and the deal gains momentum toward closing. But that only happens when you're prepared, transparent, and professional throughout the process.

The sellers I've worked with who close successfully all share the same traits: they prepared their documents months in advance, they disclosed problems honestly, they kept running their business at full speed during the sale, they had good professional advisors, and they treated the buyer's questions as reasonable rather than offensive.

If you're thinking about selling your business in the next 12 to 24 months, start preparing for DD now. Not next month. Now. Get your books in order. Organize your contracts. Fix the issues you've been ignoring. The work you put in today will directly impact whether your deal closes and how much you actually walk away with.

Thinking about selling your business? Reach out for a confidential conversation about your situation. I'll give you an honest assessment of what you need to do before going to market and what your business might be worth. You can also grab our free Complete Guide to Selling Your Business in 2026 for a step by step walkthrough of the entire process.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.