If you're selling a business worth more than $1 million, there's a good chance a buyer is going to request a quality of earnings report. And if you've never heard that term before, you're not alone. Most small business owners go their entire career without encountering one until the day someone wants to buy their company.

A quality of earnings report, often called a QofE or QoE, is basically a deep financial audit performed by an independent accounting firm. It's not a standard audit in the traditional sense. It's specifically designed to answer one question: are the seller's reported earnings real, sustainable, and accurately presented?

I've been involved in deals where the quality of earnings report confirmed everything the seller claimed and the deal closed smoothly. I've also seen reports that uncovered problems the seller didn't even know about, leading to price reductions or deals falling apart entirely. Understanding what this report is and how to prepare for it can save you a lot of stress and money.

How a Quality of Earnings Report Differs From a Regular Audit

A standard financial audit checks whether your books follow generally accepted accounting principles (GAAP). It verifies that your numbers are accurately recorded and properly classified. An auditor might confirm that your revenue is recognized correctly, your expenses are categorized properly, and your balance sheet reflects reality.

A quality of earnings report goes much further. It doesn't just ask "are these numbers correct?" It asks "are these numbers meaningful for someone buying this business?"

Here's the difference in practice. Your tax returns might show $200,000 in net income. But a QofE analyst will dig into that number and ask questions like:

- Did any of that income come from a one time event that won't repeat, like selling a piece of equipment or receiving an insurance settlement?

- Are there personal expenses running through the business that inflate costs and deflate reported earnings, like your car payment, phone bill, or family members on payroll who don't actually work?

- Are there any revenue recognition issues, like booking revenue for work that hasn't been completed yet?

- Are vendor relationships and pricing stable, or is there a key supplier contract expiring that could significantly increase costs?

- Are customer relationships diversified, or does 40% of revenue come from one client who could leave?

The QofE takes your reported earnings and adjusts them to show what a buyer can actually expect to earn going forward. This adjusted number, often called normalized earnings or adjusted EBITDA, becomes the basis for the business valuation.

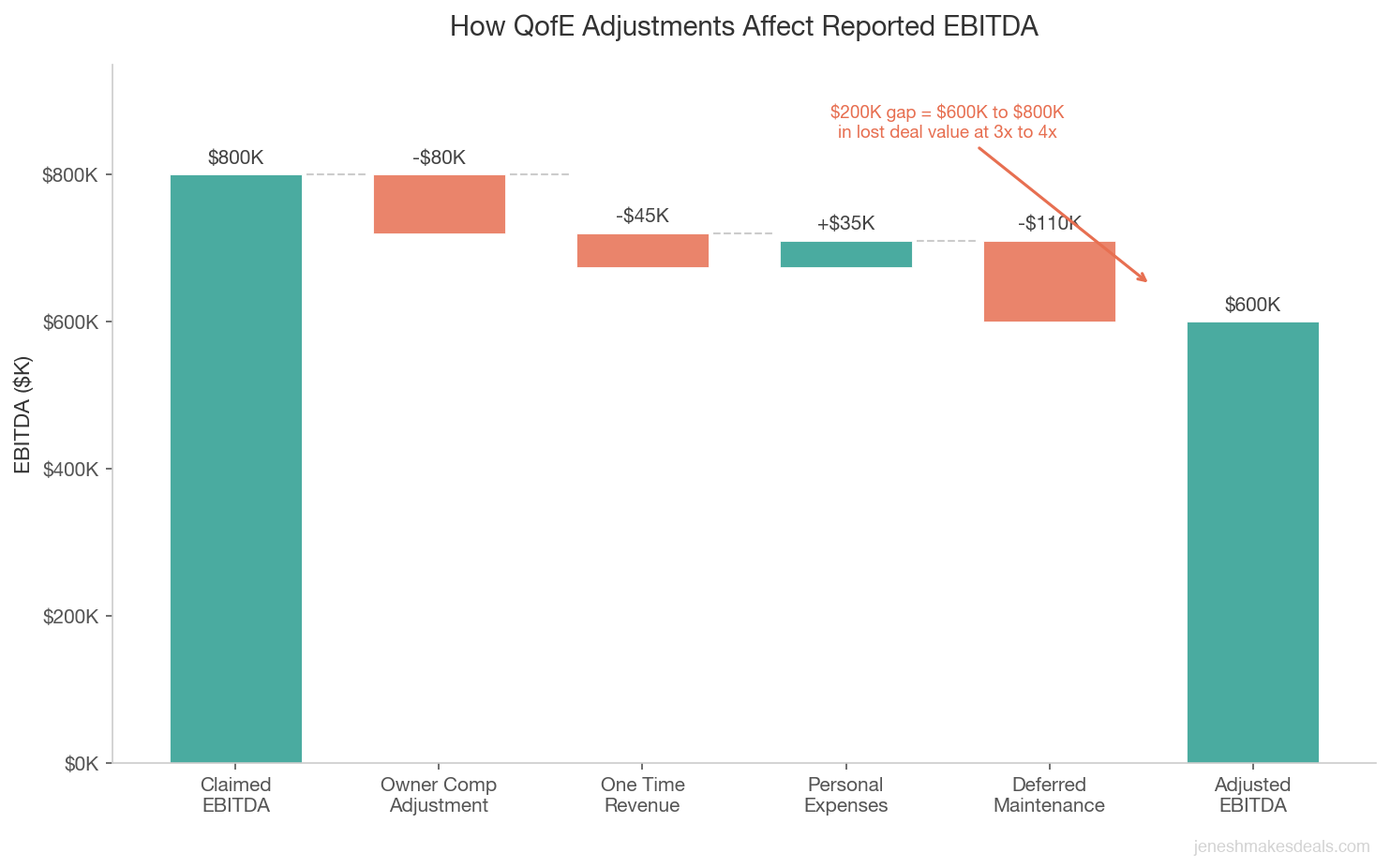

Think of a quality of earnings report as the difference between what your business earns on paper and what it actually earns in reality. I've seen QofE reports adjust a seller's claimed $800,000 EBITDA down to $550,000 after removing questionable add backs and one time revenue. That $250,000 gap, multiplied by a 3x to 4x multiple, can mean $750,000 to $1 million less at closing. The numbers have to be real.

What the Report Actually Covers

A typical quality of earnings report examines several areas of your business in detail. Here's what the analysts will look at.

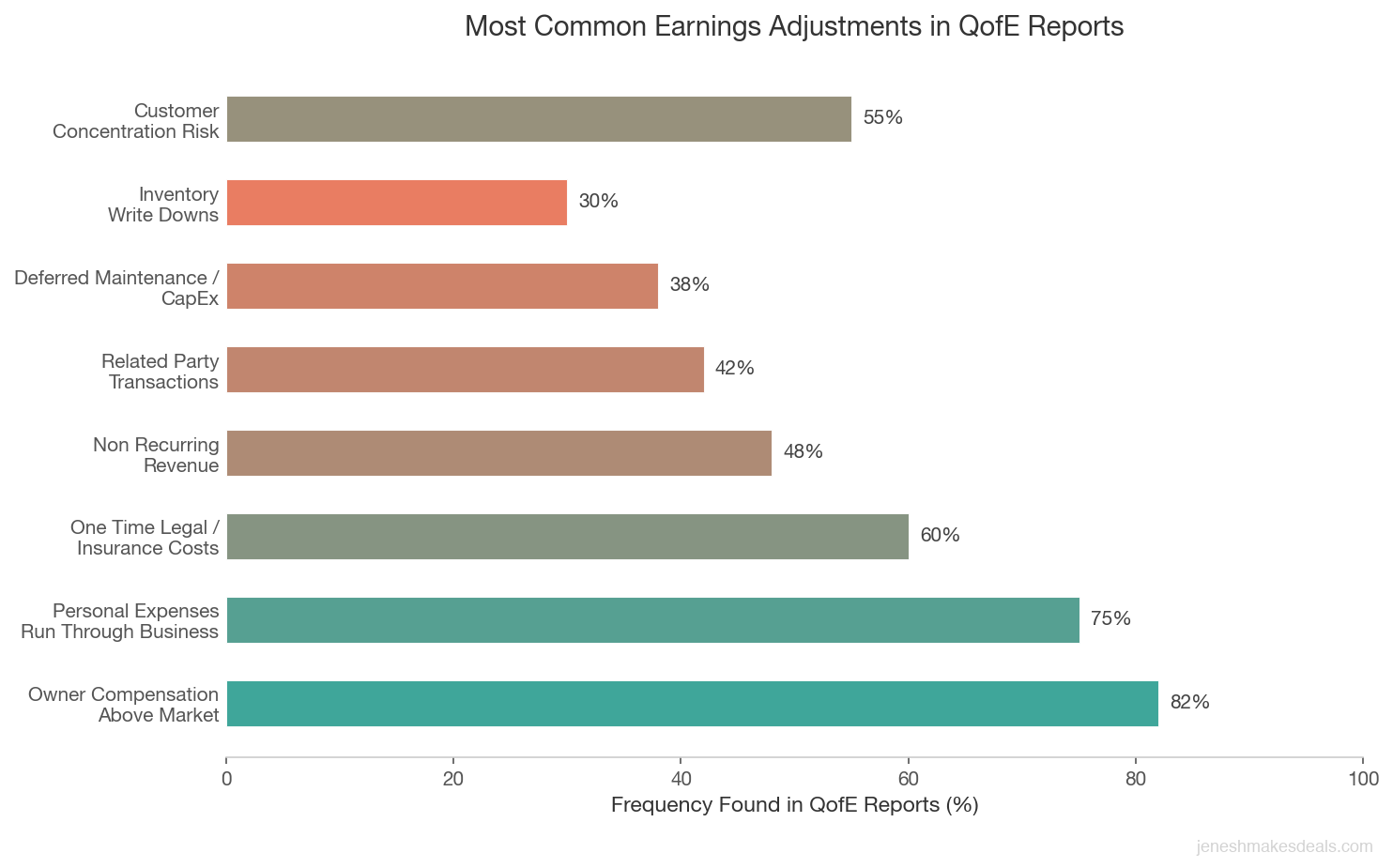

Revenue analysis. They'll break down your revenue by customer, product or service line, and time period. They're looking for trends, concentration risk, seasonality patterns, and anything unusual. If your revenue spiked 30% last year, they want to know why and whether it's sustainable.

Expense normalization. This is where they identify add backs. Personal expenses, one time costs, above market compensation, and non recurring items all get adjusted. The goal is to show what the business would earn under a new owner running it at market rates.

Working capital assessment. Buyers need to know how much cash is required to keep the business running day to day. The QofE will analyze your accounts receivable, inventory, accounts payable, and other current assets and liabilities to determine the normal working capital needs of the business.

Customer and revenue quality. Are your customers on contracts or do they buy on a transactional basis? What's your customer retention rate? How long has your average customer been with you? Revenue from long term contracts with creditworthy customers is worth more than revenue from one time buyers.

Earnings sustainability. This is the big picture analysis. Can a buyer expect these earnings to continue? Are there any factors that could cause a significant change, like a lease expiring, a key employee planning to retire, pending regulation changes, or technology disruption?

Balance sheet review. The analysts will verify asset values, check for hidden liabilities, review debt terms, and assess the condition of equipment and inventory. An accounts receivable aging analysis will reveal whether your outstanding invoices are collectible or if you've been carrying bad debt.

Need help understanding what your business is worth? Use our free business valuation calculator to get a baseline estimate based on your industry's typical multiples.

When Sellers Should Get a QofE Report

Traditionally, the buyer orders and pays for the quality of earnings report. It's part of their due diligence. But there are situations where getting your own report, called a sell side QofE, makes a lot of strategic sense.

When your business is worth $2 million or more. At this price point, buyers and their lenders will almost certainly require a QofE. Getting your own done first means you can identify and address any issues before they become deal killers. You control the narrative instead of reacting to someone else's findings.

When you have complicated financials. If your business has multiple entities, intercompany transactions, a mix of cash and accrual accounting, or significant owner add backs, a sell side QofE helps you present clean, credible financials from the start.

When you want to maximize your sale price. A sell side QofE done by a reputable firm adds credibility to your asking price. When buyers see that an independent third party has verified your earnings, they're more likely to accept your valuation and less likely to negotiate aggressively on price.

When you're approaching private equity or strategic buyers. These buyers are sophisticated and they will do their own QofE regardless. Having yours done first shows professionalism and speeds up their process. PE buyers in particular appreciate sellers who come to the table prepared.

When there's been a recent change in the business. If you lost a major customer, hired a bunch of new people, invested heavily in equipment, or made any other big change in the past year, a QofE helps explain those changes and their impact on future earnings.

What It Costs and Who Pays

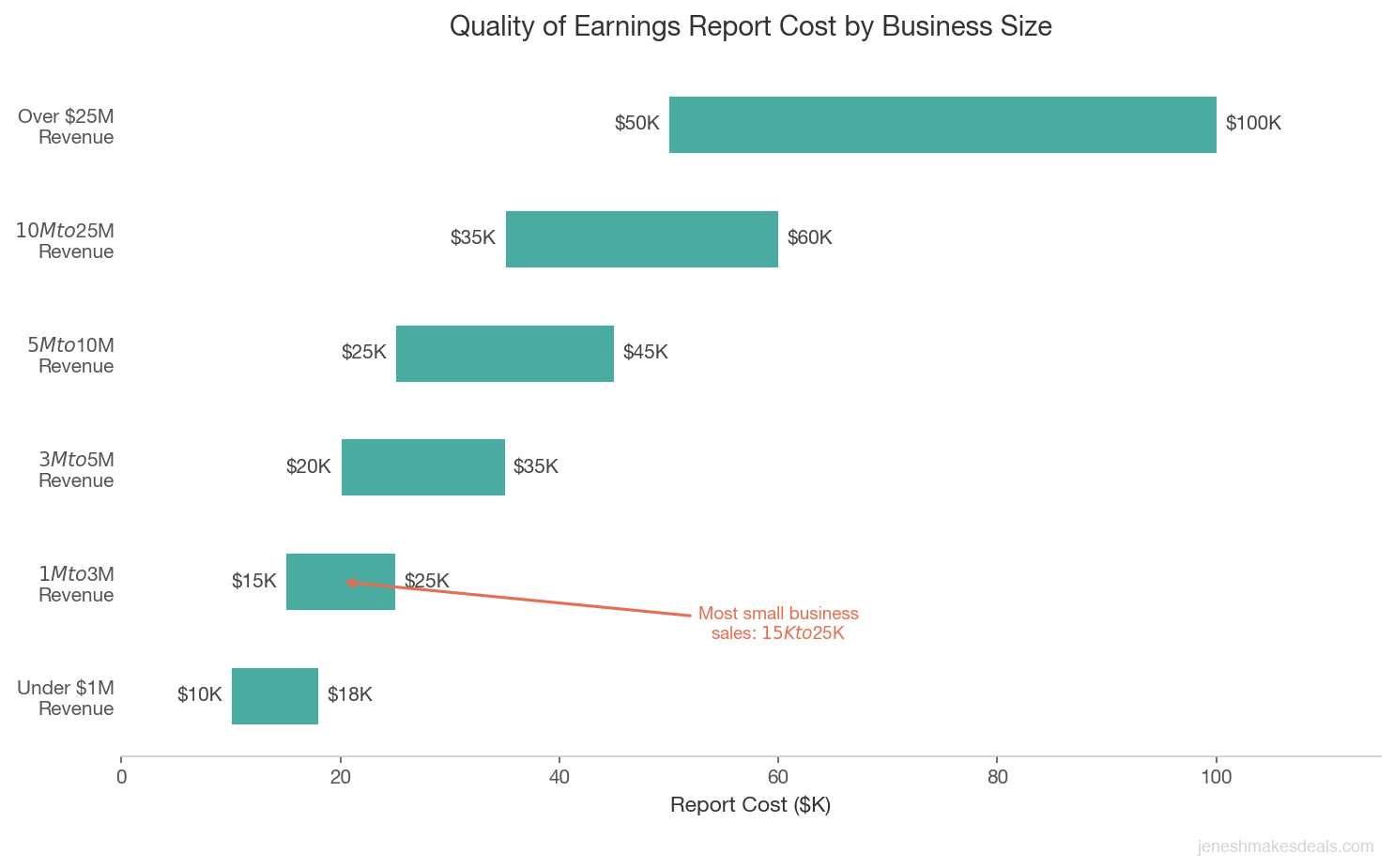

A quality of earnings report typically costs between $15,000 and $50,000 depending on the size and complexity of the business. For businesses under $5 million in revenue, expect to pay $15,000 to $25,000. For larger, more complex businesses, the cost can climb to $50,000 or more.

In a buyer initiated QofE, the buyer pays. This is the norm and you shouldn't be asked to cover it. However, you will need to cooperate extensively with the analysts, providing documents, answering questions, and making your bookkeeper or accountant available.

In a sell side QofE, you pay. But think of it as an investment. If a $20,000 report helps you justify a sale price that's $200,000 higher because buyers trust the numbers, the return on investment is obvious.

Some sellers worry that a QofE might reveal something negative. That's actually a reason to do it early. If there's a problem, you want to know about it before you're in the middle of negotiations. Finding a customer concentration issue or an accounting error during your own preparation gives you time to address it. Finding it during the buyer's due diligence gives you a price reduction.

Every problem found in a sell side QofE is a problem you can fix on your own terms. Every problem found in the buyer's QofE is a bargaining chip they will use against you. I always tell sellers: it is better to spend $20,000 learning about an issue six months before listing than to lose $200,000 in price negotiations because a buyer discovered it first.

How to Prepare for a Quality of Earnings Report

Whether you're commissioning your own or preparing for a buyer's, the process requires significant preparation. Here's how to set yourself up for the best possible outcome.

Clean up your books at least 12 months in advance. Make sure your financial statements are current, accurate, and reconciled. Fix any categorization errors. If you've been running personal expenses through the business, document them clearly. The cleaner your books, the smoother the process.

Organize three to five years of financial documents. The QofE team will want tax returns, profit and loss statements, balance sheets, bank statements, accounts receivable aging, accounts payable aging, and general ledger detail for the most recent three to five years. Have these ready in a well organized digital folder.

Prepare an add back schedule. Document every personal expense, one time cost, and non recurring item. For each add back, provide supporting documentation. "Owner's car payment" needs a lease agreement and evidence it's on the company books. "One time legal settlement" needs the settlement agreement showing it won't recur.

Brief your bookkeeper or accountant. The QofE analysts will have questions that only someone familiar with your day to day accounting can answer. Make sure your bookkeeper knows this is coming and has time available to respond promptly. Delays in providing information slow down the entire process.

Be honest and complete. Trying to hide problems is the worst thing you can do. QofE analysts are professionals who look at businesses like yours every day. They will find inconsistencies. When they do, it damages your credibility far more than the underlying issue would have on its own.

Ready to start preparing your business for sale? Contact us for a free consultation and we'll help you identify what to prioritize.

What Happens When the Report Reveals Problems

Let me be real about this. Not every QofE comes back clean. And when problems surface, here's how they typically play out.

Earnings are lower than represented. This is the most common issue. After normalization, the adjusted earnings come in lower than what the seller claimed. Maybe the add backs weren't as strong as presented, or there were expenses the seller overlooked. This usually leads to a price reduction proportional to the earnings gap. If the business was valued at 3x adjusted EBITDA and the QofE shows EBITDA is $100,000 less than claimed, expect the price to drop by about $300,000.

When a QofE reveals an earnings gap, the price reduction is almost always larger than the gap itself. Buyers don't just adjust for the dollar amount. They also factor in the credibility hit and wonder what else might be off. A $100,000 earnings shortfall can easily turn into a $400,000 or $500,000 reduction once the buyer recalculates risk. Accuracy from the start is your best defense.

Customer concentration is worse than disclosed. If the report reveals that one customer represents 35% of revenue and the seller said "no single customer is more than 20%," that's a credibility issue on top of a risk issue. The buyer will likely demand a lower price, an earnout tied to retaining that customer, or both.

Revenue trends are declining. If the most recent months show a clear downward trend that wasn't disclosed, buyers will either renegotiate significantly or walk away. This is why honesty from the beginning is so important. A declining business can still sell. A declining business that was presented as growing will not sell at any price.

Working capital needs are higher than expected. If the business requires more cash to operate than the buyer initially calculated, it changes the economics of the deal. The buyer might need more financing or might reduce the purchase price to compensate.

Hidden liabilities exist. Unpaid taxes, pending lawsuits, employee claims, or environmental issues discovered during the QofE can kill deals quickly. These are the kinds of things sellers sometimes "forget" to mention but that always come out during proper due diligence.

How the QofE Affects Deal Negotiations

Once the quality of earnings report is complete, it becomes one of the most important documents in the negotiation. Here's how it typically influences the deal.

It establishes the real earnings baseline. The purchase price is almost always calculated as a multiple of adjusted earnings. The QofE determines what that adjusted earnings number is. If the buyer's QofE shows adjusted EBITDA of $500,000 and both parties agree on a 3.5x multiple, the enterprise value is $1.75 million. That's the starting point.

It identifies areas for negotiation. The report might flag certain add backs as questionable. Maybe you claimed your spouse's $80,000 salary was an add back, but the QofE analyst says the role is necessary and a replacement would cost $60,000. Now there's a $20,000 difference per year to negotiate about.

It affects deal structure. If the QofE reveals risk factors like customer concentration or declining margins, the buyer might propose an earnout rather than paying full price upfront. An earnout ties a portion of the purchase price to the business hitting certain performance targets after closing.

It influences financing. SBA lenders rely heavily on QofE reports to determine how much they're willing to lend. If the QofE shows strong, sustainable earnings, the buyer gets better loan terms. If it raises concerns, the lender might require a larger down payment or higher interest rate.

Choosing the Right Firm for a Sell Side QofE

If you decide to commission your own quality of earnings report, choosing the right firm matters. Here's what to look for.

Independence matters. Don't use your own accountant. The whole point of a QofE is independent verification. Using the same firm that does your books undermines the credibility you're trying to build. Choose a firm that has no prior relationship with your business.

Industry experience matters. Just like finding the right broker, you want a QofE firm that has experience with businesses like yours. A firm that primarily audits tech companies might miss important nuances in a manufacturing or restaurant business.

Look for M&A transaction experience. Not all accounting firms do QofE reports. You want a firm that regularly works on M&A transactions and understands what buyers and lenders look for. Ask how many QofE reports they've completed in the past year.

Ask about timeline. A typical QofE takes four to eight weeks to complete. Some firms can expedite it if you're on a tight timeline. Make sure you understand the timeline before committing, especially if you're trying to have the report ready before going to market.

Get a fee estimate in writing. The cost should be based on the scope of work, not a surprise. Ask for a written engagement letter that spells out what's included, what could cause the fee to increase, and the expected timeline.

The Bottom Line on Quality of Earnings Reports

A quality of earnings report is one of those things that seems like an unnecessary hassle until you realize how much it can protect you as a seller. Whether a buyer orders one or you commission your own, understanding what it is and how to prepare makes a real difference in how smoothly your deal goes.

If you're selling a business worth more than $1 million, expect to encounter a QofE at some point in the process. If you're selling for more than $2 million, strongly consider getting your own done before going to market. The investment pays for itself many times over by building credibility, uncovering fixable problems early, and giving you confidence in your asking price.

The sellers who handle this process best are the ones who treat it as an opportunity to prove their business's value rather than as a threat to be feared. Start preparing early, keep honest books, and work with professionals who know what they're doing.

Thinking about selling? Contact us for a free consultation and we'll walk you through what to expect during due diligence, including the quality of earnings process.

Want a quick estimate before you start? Try our free business valuation calculator to see what businesses like yours typically sell for.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.