You've negotiated the purchase price, agreed on the deal structure, and shaken hands with the buyer. But before you sign anything, there's a section of the purchase agreement that can come back to haunt you for years after closing. It's the indemnification clause, and most sellers don't fully understand what they're agreeing to.

An indemnification clause is essentially a promise between the buyer and seller about who will pay for certain problems that arise after the deal closes. If the business has a tax issue that nobody caught during due diligence, who pays? If a customer sues for something that happened before the sale, who's responsible? If the inventory was overstated and the buyer paid too much, who covers the difference?

The answers to all of these questions are determined by the indemnification clause. And if you don't negotiate it carefully, you could find yourself writing checks long after you thought you were done with the business.

The indemnification clause is the single most important section of a purchase agreement for sellers. It determines how much of the sale price you actually get to keep.

How Indemnification Works in a Business Sale

Think of indemnification as a financial safety net. The buyer wants protection against problems they didn't know about when they bought the business. The seller wants to limit their exposure so they're not liable for everything that happens after they walk away.

In a typical business purchase agreement, both the buyer and the seller make a series of representations and warranties. These are statements about the condition of the business at the time of the sale. The seller might represent that the financial statements are accurate, that there are no pending lawsuits, that all taxes have been paid, and that the business is in compliance with all applicable laws.

The indemnification clause is what happens when one of those representations turns out to be wrong. If the seller said there were no pending lawsuits but a lawsuit surfaces six months after closing, the indemnification clause determines whether the seller has to pay the buyer for the resulting damages.

Here's a simplified example. You sell your manufacturing business for $2 million. In the purchase agreement, you represent that all environmental permits are current and the facility is in compliance with all environmental regulations. Six months after closing, the buyer discovers that the facility has a groundwater contamination issue that predates the sale. The cost to remediate is $150,000.

Under the indemnification clause, the buyer would make a claim against you for the $150,000 because the environmental contamination contradicts your representation about compliance. Whether you actually have to pay depends on the specific terms of the indemnification clause, which is why those terms matter so much.

Key Components of an Indemnification Clause

Indemnification clauses can be long and complicated, but they generally cover a few key areas. Understanding each one is critical for sellers.

Scope of Indemnification

This defines what types of losses are covered. Most clauses cover losses arising from breaches of representations and warranties, breaches of covenants (promises about what you'll do or won't do before and after closing), and certain specific risks that were identified during the negotiation.

Some clauses are broad and cover "any and all losses, damages, liabilities, costs, and expenses." Others are narrower and only cover direct damages, excluding things like lost profits, consequential damages, and punitive damages. As a seller, you want the narrowest scope possible.

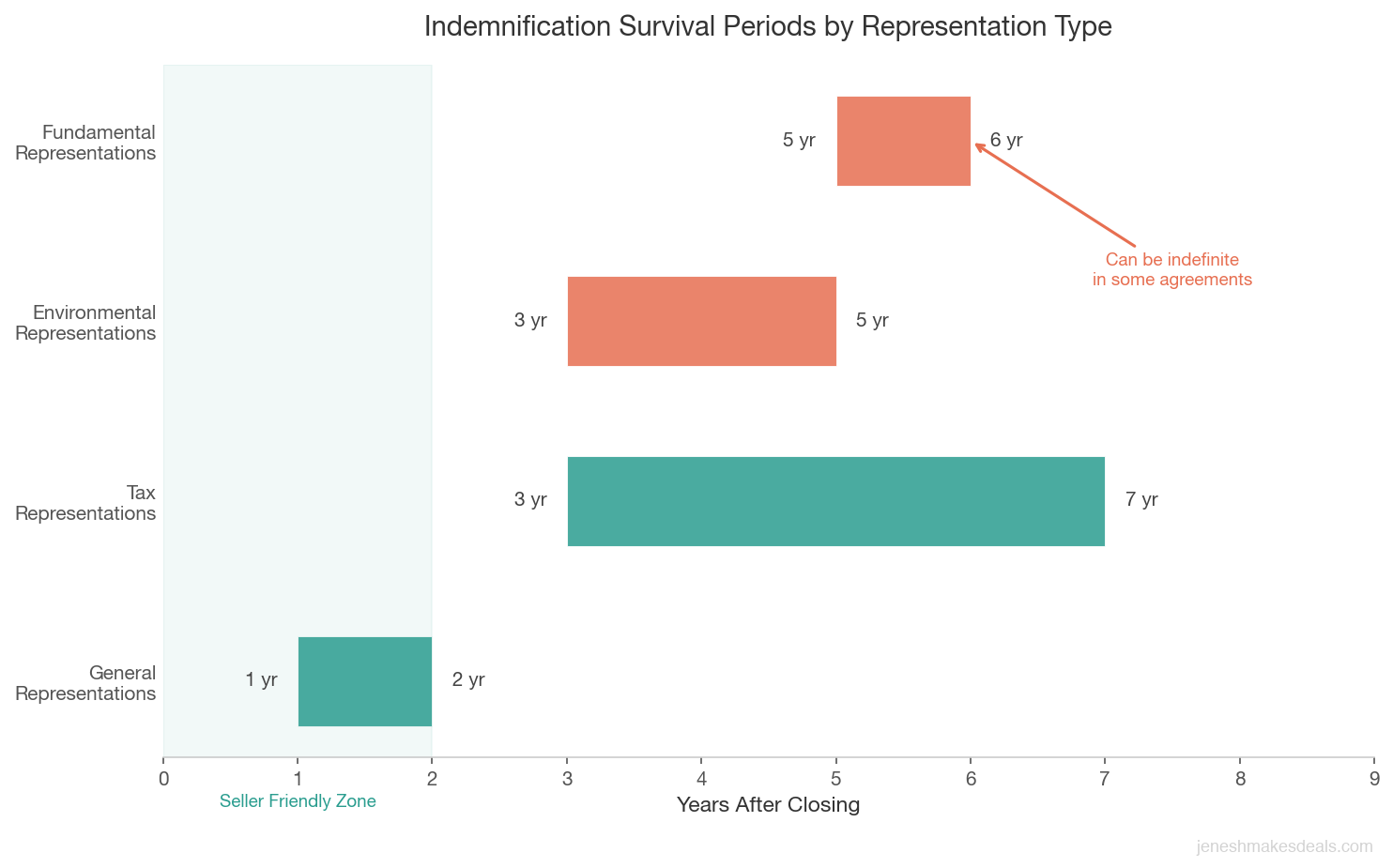

Survival Period

Representations and warranties don't last forever. The survival period sets how long after closing the buyer can make a claim. Typical survival periods are:

- General representations: 12 to 24 months after closing

- Tax representations: Until the statute of limitations expires (usually 3 to 7 years)

- Environmental representations: 3 to 5 years, sometimes longer

- Fundamental representations (ownership, authority, capitalization): 5 to 6 years or indefinite

The shorter the survival period, the better for the seller. Once the survival period expires, the buyer can no longer make claims against you for breaches of those representations.

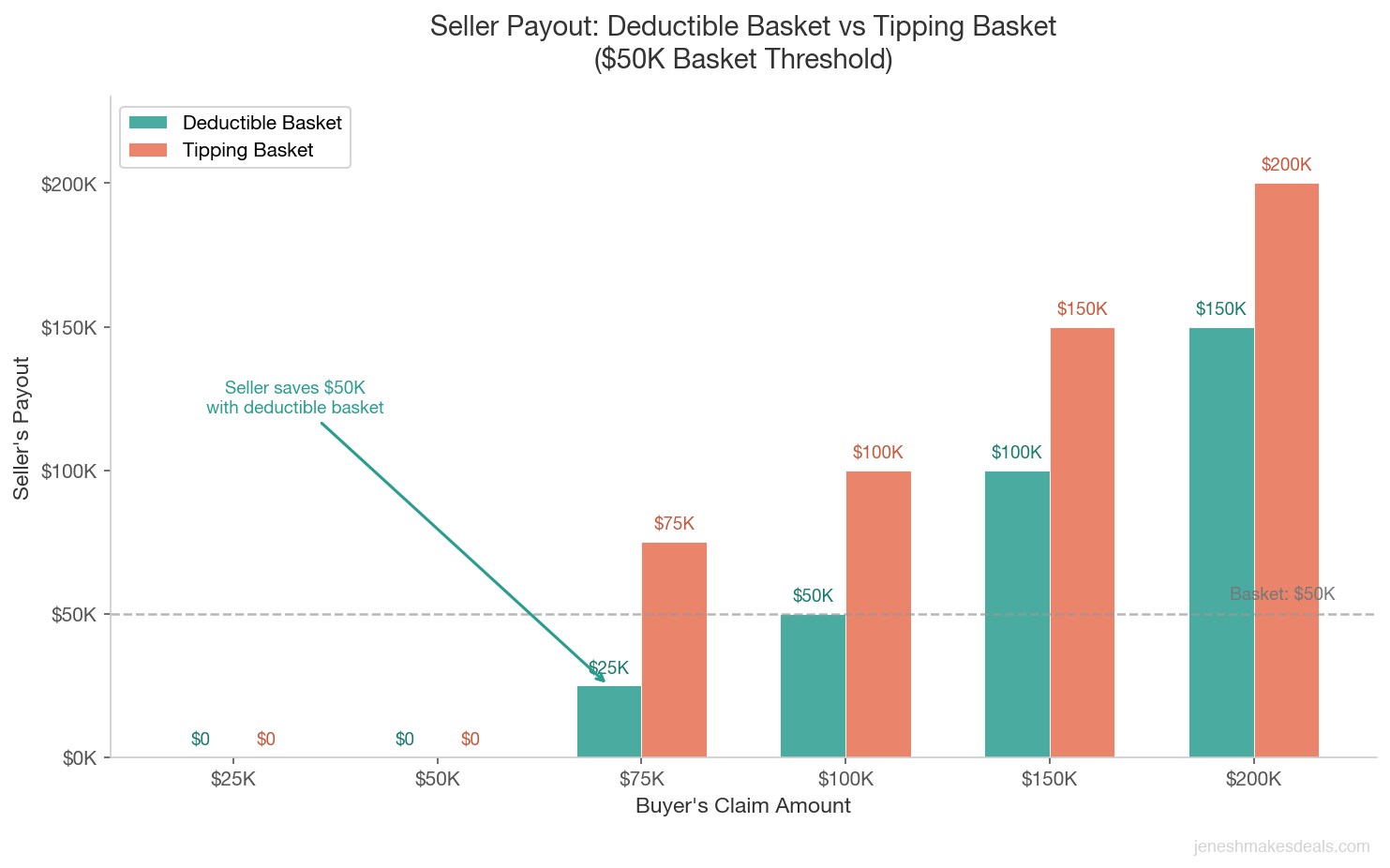

Baskets and Deductibles

A basket is like a deductible on an insurance policy. It sets a minimum threshold that the buyer's losses must exceed before they can make an indemnification claim.

There are two types:

- Deductible basket (true deductible). The buyer must absorb the first portion of losses. If the basket is $50,000 and the buyer's claim is $75,000, the seller only pays $25,000.

- Tipping basket (first dollar). Once the buyer's losses exceed the threshold, the seller is responsible for the entire amount from the first dollar. If the basket is $50,000 and the claim is $75,000, the seller pays the full $75,000.

As a seller, you always want a deductible basket. It significantly reduces your exposure because you're only on the hook for amounts above the threshold.

Typical basket amounts range from 0.5% to 1.5% of the purchase price. For a $2 million deal, that would be $10,000 to $30,000.

| Claim Amount | Deductible Basket (Seller Pays) | Tipping Basket (Seller Pays) | Seller Savings with Deductible |

|---|---|---|---|

| $25,000 | $0 | $0 | $0 |

| $50,000 | $0 | $0 | $0 |

| $75,000 | $25,000 | $75,000 | $50,000 |

| $100,000 | $50,000 | $100,000 | $50,000 |

| $150,000 | $100,000 | $150,000 | $50,000 |

| $200,000 | $150,000 | $200,000 | $50,000 |

Always push for a deductible basket over a tipping basket. On a $75,000 claim with a $50,000 threshold, the difference is $50,000 out of your pocket.

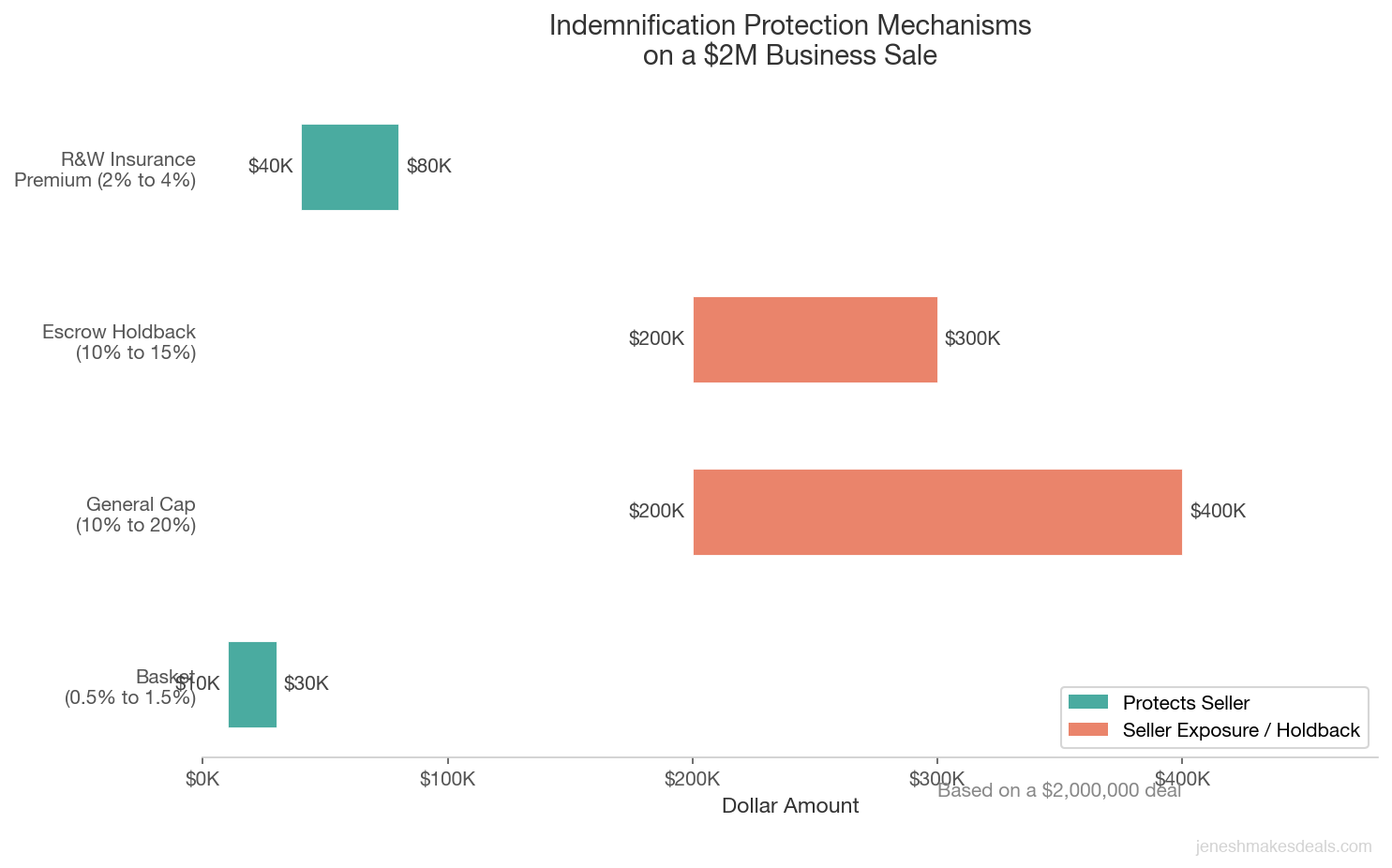

Caps

A cap sets the maximum amount the seller can be required to pay under the indemnification clause. This is one of the most important protections for sellers.

Common cap amounts:

- General representations: 10% to 20% of the purchase price

- Fundamental representations: 100% of the purchase price (no cap)

- Specific indemnities (tax, environmental): Often uncapped or capped at the full purchase price

For a $2 million deal, a general cap of 15% would mean your maximum exposure for general representation breaches is $300,000. That's still a lot of money, but it's much better than being on the hook for the full purchase price.

| Protection Mechanism | Typical Range (% of Price) | Dollar Amount ($2M Deal) | Who It Protects |

|---|---|---|---|

| Basket (Deductible) | 0.5% to 1.5% | $10,000 to $30,000 | Seller |

| General Cap | 10% to 20% | $200,000 to $400,000 | Seller |

| Escrow Holdback | 10% to 15% | $200,000 to $300,000 | Buyer |

| R&W Insurance Premium | 2% to 4% of policy limit | $40,000 to $80,000 | Both |

Need help understanding what your business is worth? Use our free business valuation calculator to get a baseline estimate based on your industry's typical multiples.

Common Representations That Trigger Indemnification Claims

In my experience, the most common areas where indemnification claims arise are:

Financial statement accuracy. The buyer discovers that revenue was overstated, expenses were understated, or the financial statements contained material errors. This is the number one source of post closing disputes.

Tax liabilities. Unpaid taxes, incorrect tax filings, or tax positions that the IRS later challenges. Tax claims can be particularly expensive because they often include interest and penalties on top of the underlying tax liability.

Employee related issues. Undisclosed employment lawsuits, misclassified workers (treating employees as independent contractors), unpaid overtime, or benefits issues that predate the sale.

Environmental contamination. Hidden environmental problems at the business's physical location. These can be extremely expensive to remediate and often have long survival periods in the purchase agreement.

Customer contracts. Representations about customer agreements that turn out to be inaccurate. For example, saying a key customer is under contract through 2027 when the contract actually expires in 2026.

Intellectual property. Claims that the business's products or services infringe on someone else's patents, trademarks, or copyrights.

Litigation. Undisclosed lawsuits, threatened claims, or regulatory investigations that predate the sale.

The lesson here is simple. Be thorough and honest in your representations. The more accurate your disclosures are, the less likely you are to face an indemnification claim after closing.

How to Negotiate Indemnification as a Seller

Indemnification is one of the most negotiated sections of any purchase agreement. Here's what I recommend sellers push for:

Short survival periods. The shorter, the better. Push for 12 months on general representations and try to limit longer survival periods to only the areas where they're truly necessary, like taxes.

Deductible basket, not tipping. This alone can save you tens of thousands of dollars if a claim arises.

Reasonable cap. Try to keep your general cap at 10% to 15% of the purchase price. Push back hard against any attempt to set the cap at 50% or higher.

Exclude consequential damages. Make sure the indemnification clause only covers direct damages, not lost profits, consequential damages, or punitive damages. These types of damages can be enormous and unpredictable.

Mini basket (de minimis threshold). In addition to the main basket, push for a mini basket that excludes individual claims below a certain amount. For example, you might agree that individual claims under $5,000 don't count toward the basket at all. This prevents the buyer from nickel and diming you with tiny claims.

Sole and exclusive remedy. Include language stating that indemnification is the buyer's sole and exclusive remedy for post closing claims (other than fraud). This prevents the buyer from suing you under other legal theories on top of the indemnification claim.

Mitigation obligation. Require the buyer to take reasonable steps to mitigate their losses before making an indemnification claim. If the buyer could have fixed a $10,000 problem but instead let it grow into a $50,000 problem, they shouldn't be able to pass the full $50,000 to you.

The Relationship Between Escrow and Indemnification

Many business sales use an escrow arrangement to secure the seller's indemnification obligations. Here's how it works.

At closing, a portion of the purchase price, typically 10% to 15%, is deposited into an escrow account managed by a neutral third party. If the buyer makes a valid indemnification claim during the survival period, the funds to pay the claim come out of the escrow.

If no claims are made, the escrow funds are released to the seller at the end of the escrow period, which usually aligns with the survival period for general representations.

For sellers, escrow is a double edged sword. On one hand, it limits your exposure to the amount in escrow (assuming the cap equals the escrow amount). On the other hand, it means you don't receive a chunk of your sale proceeds right away, and you're effectively lending the buyer money interest free while the escrow is in place.

Here's what to negotiate with escrow:

- Keep the escrow amount as low as possible. 10% is standard, but some buyers push for 15% to 20%.

- Negotiate periodic releases. Instead of holding the full amount for the entire survival period, negotiate releases at 6 month or 12 month intervals. For example, 50% of the escrow might be released after 12 months if no claims have been made.

- Earn interest. Make sure the escrow agreement specifies that any interest earned on the escrowed funds goes to the seller (or is split).

- Set clear claim procedures. The escrow agreement should have a defined process for how claims are made, disputed, and resolved. Without this, disputes about escrow releases can drag on for months.

Thinking about selling your business? Contact us for a free consultation and we'll help you understand the deal structure, including indemnification and escrow terms.

Representations and Warranties Insurance

For larger deals, typically $10 million and above, there's another option for managing indemnification risk: representations and warranties insurance, also called R&W insurance or RWI.

R&W insurance is a policy that covers losses arising from breaches of representations and warranties in the purchase agreement. Instead of the seller being personally liable for indemnification claims, the insurance policy pays the claims.

There are two types:

- Buyer side policy. The buyer purchases the policy and makes claims directly against the insurer instead of the seller. This is the most common type.

- Seller side policy. The seller purchases the policy, and the buyer makes claims against the seller, who then seeks reimbursement from the insurer. Less common and less preferred.

For sellers, buyer side R&W insurance is ideal because it essentially eliminates your indemnification exposure. The buyer has a deep pocketed insurance company to go after instead of you.

The cost of R&W insurance is typically 2% to 4% of the policy limit. For a $10 million deal with a $2 million policy limit, the premium would be $40,000 to $80,000. In many deals, the cost is shared between the buyer and seller, or the seller agrees to reduce the purchase price slightly to account for the premium.

While R&W insurance isn't practical for smaller deals due to the minimum premium requirements, it's becoming increasingly common in mid market transactions. If your deal is $5 million or above, it's worth asking your broker or attorney about it.

What Happens When an Indemnification Claim Is Made

If the buyer believes they've discovered a breach of your representations, they'll submit a written claim specifying the nature of the breach, the amount of damages, and the basis for their claim.

Here's the typical process:

- Notice. The buyer sends you a written notice of the claim, usually within a specified timeframe after discovering the issue.

- Review period. You have a set number of days (usually 30 to 60) to review the claim and respond. You can accept it, reject it, or dispute the amount.

- Negotiation. If you dispute the claim, the parties try to negotiate a resolution. Most indemnification claims are settled through negotiation rather than litigation.

- Escrow release or payment. If the claim is resolved, payment comes from the escrow account (if there is one) or directly from the seller.

- Dispute resolution. If the parties can't agree, the claim goes to the dispute resolution mechanism specified in the purchase agreement, usually mediation followed by arbitration or litigation.

My advice to sellers is to take every claim seriously, even if you think it's baseless. Respond promptly, document everything, and work with your attorney throughout the process. Ignoring a claim or missing a deadline can result in a default judgment against you.

How to Minimize Your Indemnification Risk Before Closing

The best defense against indemnification claims is preparation. Here's what I recommend:

Resolving known issues before listing your business is almost always cheaper than dealing with them through an indemnification claim after closing.

Get your financials audited or reviewed. If you can show that your financial statements were reviewed by an independent accountant, it's much harder for a buyer to claim they were misleading.

Be thorough in your disclosures. The purchase agreement will have disclosure schedules where you list any exceptions to your representations. Be comprehensive. It's much better to disclose something upfront than to have the buyer discover it later and claim you hid it.

Fix known issues before listing. If you know there's a tax issue, an employee dispute, or an environmental concern, address it before you put the business on the market. Resolving these issues proactively is almost always cheaper than dealing with them through an indemnification claim.

Keep detailed records. If a claim does arise, you'll need documentation to defend yourself. Maintain organized records of all financial transactions, customer contracts, employee files, permits, and compliance documentation.

Work with experienced advisors. An M&A attorney who regularly handles business sales will know how to negotiate indemnification terms that protect you. Don't try to handle this on your own.

The Bottom Line

Indemnification clauses are one of the most important and least understood parts of a business purchase agreement. They determine who bears the financial risk for problems that surface after closing, and they can affect how much money you actually walk away with from the sale.

As a seller, your goals should be to make honest and thorough representations, negotiate reasonable caps and baskets, push for short survival periods, and consider escrow and insurance options that limit your exposure.

Don't sign a purchase agreement without fully understanding the indemnification terms. And don't negotiate those terms without an experienced M&A attorney by your side.

Want to know what your business could sell for? Try our free business valuation calculator to get an estimate based on your industry's typical SDE multiples.

Ready to start the selling process? Contact us for a free consultation and we'll walk you through every step, including how to protect yourself in the purchase agreement.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.