If you're thinking about selling your business, the first question you need to answer is simple: what is it actually worth?

Not what you hope it's worth. Not what your neighbor's cousin sold his business for. Not what some online calculator spits out after you enter three numbers. You need a realistic, defensible number that a real buyer will agree with.

That's where a broker opinion of value comes in. It's one of the most useful tools in the business selling process, and most owners don't even know it exists. I prepare these for business owners every week, and I can tell you that the owners who get a BOV before listing their business consistently make better decisions about timing, pricing, and deal structure.

Let me walk you through exactly what a BOV is, how it works, and why it matters for your exit.

What Is a Broker Opinion of Value?

A broker opinion of value (BOV) is a professional estimate of what your business would likely sell for on the open market. It's prepared by an experienced business broker who analyzes your financials, your industry, comparable sales data, and the current market to arrive at a realistic price range.

Think of it like a real estate CMA (comparative market analysis), but for businesses. A real estate agent looks at recent home sales in your neighborhood to estimate your home's value. A business broker does the same thing, but with business sales data, financial performance, and industry specific multiples.

A BOV typically includes:

- A valuation range (not a single number) based on your business's adjusted earnings

- The methodology used to calculate the value (SDE multiples, EBITDA multiples, or both)

- Comparable sales data from similar businesses that have recently sold

- Key value drivers that make your business more or less attractive to buyers

- Recommendations for improving value before listing

The important thing to understand is that a BOV is an opinion, not a certified appraisal. It's based on the broker's experience, market knowledge, and analysis of your specific business. That said, a good BOV from an experienced broker is remarkably accurate. In my experience, the final sale price lands within the BOV range about 80% of the time.

How a BOV Is Different from a Formal Business Appraisal

People often confuse a BOV with a formal business appraisal, but they serve different purposes and carry different weight.

| Feature | Broker Opinion of Value (BOV) | Formal Business Appraisal |

|---|---|---|

| Prepared by | Licensed business broker | Accredited business appraiser (ASA, CVA, ABV) |

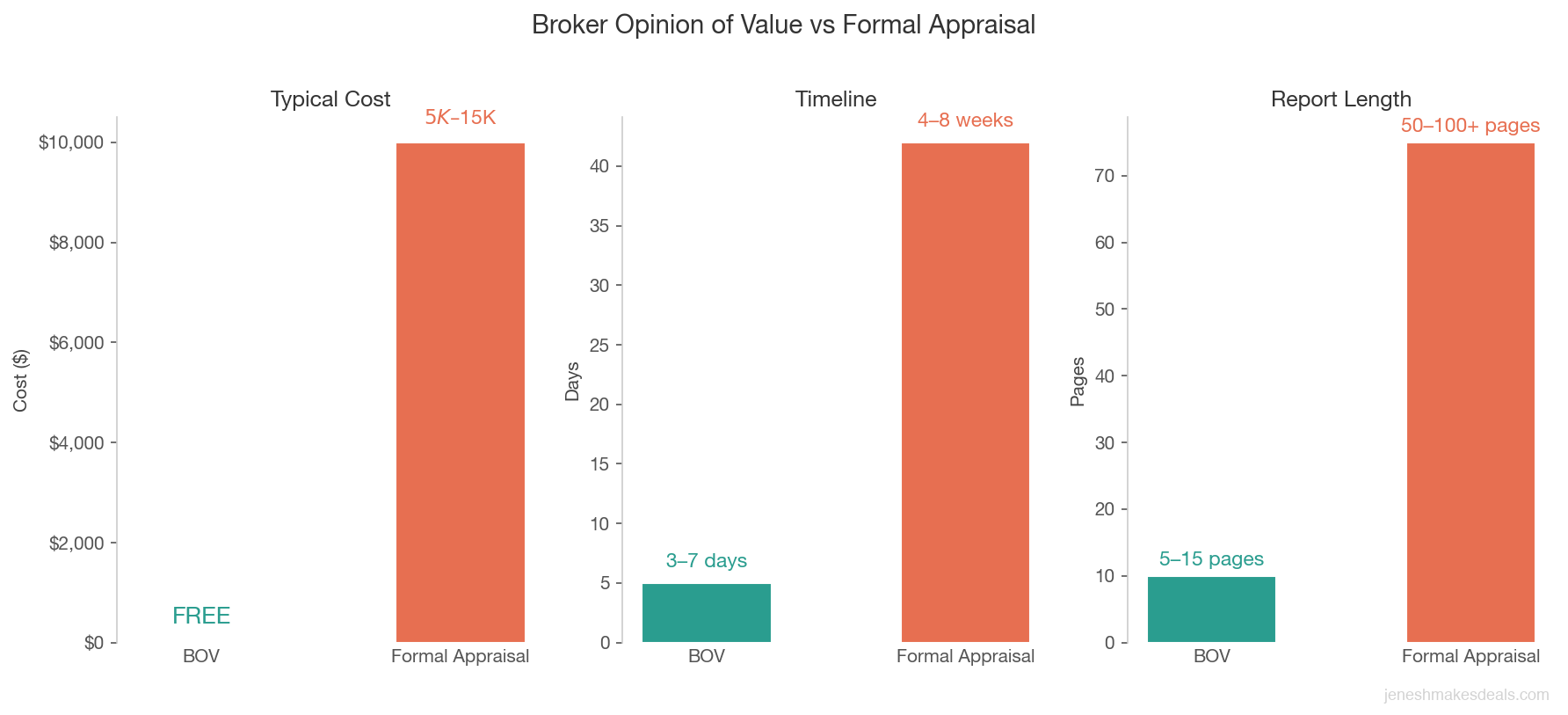

| Cost | Usually free (part of listing consultation) | $5,000 to $15,000+ |

| Timeline | 3 to 7 days | 4 to 8 weeks |

| Legal standing | Informal, advisory only | Legally defensible, court admissible |

| Methodology | Market based (comparable sales + multiples) | Three approaches: income, market, and asset based |

| Report length | 5 to 15 pages | 50 to 100+ pages |

| Best for | Listing preparation, exit planning, pricing strategy | SBA loans, divorce, estate tax, litigation |

A formal appraisal is a much more rigorous process. An accredited appraiser follows Uniform Standards of Professional Appraisal Practice (USPAP) and produces a detailed report that can hold up in court. They'll use three different valuation approaches and reconcile them into a final opinion of value.

A BOV, on the other hand, is practical and market focused. It tells you what a buyer will actually pay based on current market conditions. I've seen formal appraisals value a business at $1.2 million while the market reality was closer to $900,000, simply because the appraiser used assumptions that didn't reflect how buyers in that industry actually price deals.

Both have their place. But if your goal is to sell your business and you want to know what to expect, a BOV is the right starting point.

A BOV tells you what a buyer will actually pay. A formal appraisal tells you what the business is theoretically worth. When you're selling, market reality matters more than textbook value.

When You Should Get a Broker Opinion of Value

You don't need to be ready to sell tomorrow to benefit from a BOV. There are several situations where getting a professional value opinion makes sense.

Thinking about selling in the next 1 to 3 years. This is the most common reason owners reach out to me. They're not in a rush, but they want to understand what their business is worth today so they can make changes to increase value before going to market. A BOV gives you a baseline and a roadmap.

Partnership disputes or buyouts. When one partner wants to buy out another, you need an agreed upon value. A BOV provides a neutral, market based starting point for negotiations. I've helped dozens of partners work through buyouts using a BOV as the foundation.

Estate planning. If your business is a significant part of your estate, you need to know its value for planning purposes. A BOV gives you a current market estimate without the $10,000+ cost of a formal appraisal. Your estate attorney can use this to guide initial planning decisions.

Divorce proceedings. In many divorces, the business is the largest marital asset. While courts often require a formal appraisal for the final settlement, a BOV can help you understand the ballpark value early in the process so you can make informed decisions about negotiations.

Considering a growth investment. Sometimes owners want to know their current value so they can measure the ROI of a planned investment. If you're thinking about spending $200,000 on new equipment or a second location, knowing your current value helps you project how that investment will affect your exit price.

Annual check in. Some of my smartest clients get a BOV every year, even when they have no plans to sell. They track their business value the same way they track revenue and profit. When the value hits their target number, they know it's time.

Want to get a quick estimate right now? Try our free business valuation calculator to see where your business falls based on industry SDE multiples.

What Information a Broker Needs to Prepare a BOV

When a business owner asks me for a BOV, I don't just pull a number out of thin air. I need real data to give you a meaningful valuation. Here's what I'll ask for.

Financial statements for the last 3 years. This includes profit and loss statements and balance sheets. I need to see trends, not just a single snapshot. A business that grew from $500,000 to $800,000 in revenue over three years tells a very different story than one that dropped from $800,000 to $500,000.

Federal tax returns for the last 3 years. Tax returns verify what the financial statements show. They also reveal owner compensation, depreciation schedules, and other items that affect the adjusted earnings calculation.

A list of owner add backs and adjustments. Most small business owners run personal expenses through the business. That's normal. But I need to know about them to calculate your true seller's discretionary earnings (SDE). Common add backs include:

- Owner's salary and benefits

- Personal vehicle expenses

- Personal insurance premiums

- One time expenses (lawsuit settlement, major repair)

- Family members on payroll who don't work full time in the business

- Discretionary travel and entertainment

Lease details. The terms of your commercial lease matter more than most owners realize. A buyer needs to know the monthly rent, remaining term, renewal options, and whether the lease is transferable. A business with 8 years left on a below market lease is worth more than the same business with 6 months remaining.

Employee information. I need to know how many employees you have, their roles, tenure, and compensation. A business where three key employees have been there for 10+ years is more valuable than one with constant turnover.

Equipment and asset list. A summary of major equipment, vehicles, and other physical assets included in the sale, along with their approximate age and condition.

Customer concentration data. If one customer represents 40% of your revenue, that's a risk factor that affects value. I need to understand how diversified your customer base is.

The more complete and organized your information is, the more accurate your BOV will be. I tell every owner the same thing: the quality of the valuation depends on the quality of the data.

How Brokers Calculate Business Value: The Methodology

The most common method for valuing small to mid size businesses is the earnings multiple approach. Here's how it works in plain language.

Step 1: Calculate adjusted earnings. I take your reported net income and add back items that are specific to you as the owner. This gives us your SDE (seller's discretionary earnings) or EBITDA (earnings before interest, taxes, depreciation, and amortization).

For businesses under $1 million in value, SDE is the standard metric. For businesses over $1 million, EBITDA is more common because the buyer will likely hire a manager rather than run it themselves.

Step 2: Apply an industry multiple. Every industry has a range of multiples based on historical sales data. These multiples come from databases like BizComps, DealStats, and the IBBA Market Pulse, which track thousands of actual business transactions.

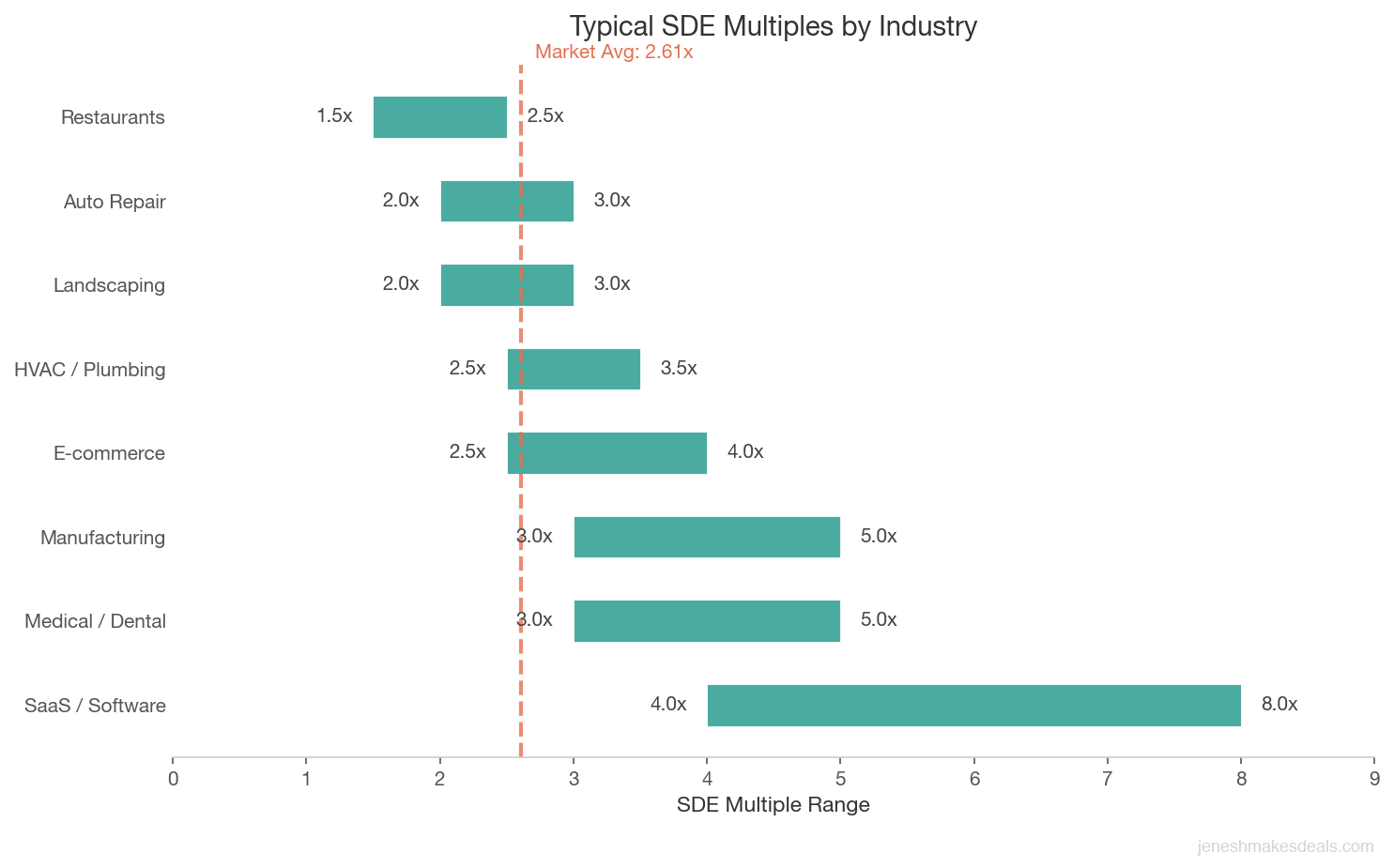

Here are some common SDE multiple ranges for small businesses:

| Industry | Typical SDE Multiple |

|---|---|

| Restaurants | 1.5x to 2.5x |

| Landscaping/Lawn Care | 2.0x to 3.0x |

| HVAC/Plumbing | 2.5x to 3.5x |

| E-commerce | 2.5x to 4.0x |

| Medical/Dental Practices | 3.0x to 5.0x |

| SaaS/Software | 4.0x to 8.0x |

| Manufacturing | 3.0x to 5.0x |

| Auto Repair | 2.0x to 3.0x |

Your industry determines the starting range. Where you land within that range depends entirely on how you've built and documented your business.

Step 3: Analyze comparable sales. Multiples give you a range. Comparable sales data helps you narrow it down. I look at actual transactions in your industry, region, and size bracket to see what real buyers paid for similar businesses.

Step 4: Adjust for your specific business. No two businesses are identical. I adjust the multiple up or down based on factors like growth trends, customer concentration, recurring revenue, owner involvement, and location.

The result is a value range that reflects what a qualified, motivated buyer would realistically pay for your business in the current market.

A Walkthrough Example: Valuing a Landscaping Company

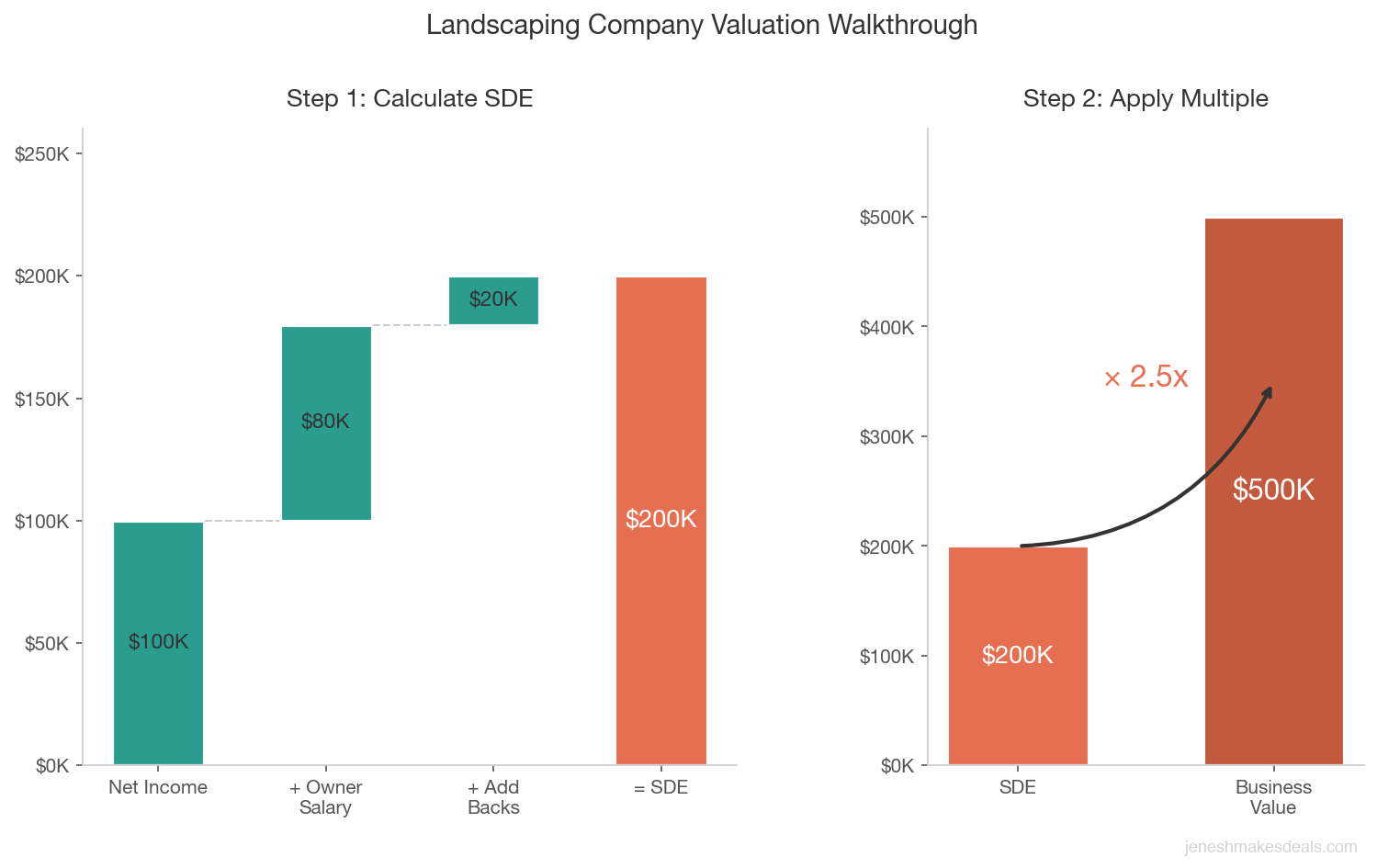

Let me show you how this works with a real world example. Say a landscaping company owner calls me and wants to know what his business is worth.

The business profile:

- Annual revenue: $800,000

- Owner's reported salary: $80,000

- Net income on tax returns: $100,000

- Owner add backs: $20,000 (personal vehicle, cell phone, one time equipment repair)

- Calculated SDE: $200,000 ($100,000 net income + $80,000 owner salary + $20,000 add backs)

Applying the multiple:

Landscaping businesses typically sell for 2.0x to 3.0x SDE. But where does this specific business fall within that range? I look at the details.

Factors pushing the multiple higher (toward 3.0x):

- 60% of revenue comes from recurring maintenance contracts

- The owner works about 30 hours per week, mostly managing, not mowing

- Revenue has grown 10% per year for the last three years

- Two crew leaders have been with the company for 5+ years

- All equipment is in good condition and included in the sale

Factors pushing the multiple lower (toward 2.0x):

- The business operates in a seasonal market (revenue drops 40% in winter)

- One commercial client represents 25% of revenue

- The owner handles all sales and estimates personally

Given these factors, I'd place this business at a 2.5x to 3.0x multiple.

The BOV range: $500,000 to $600,000

That's the realistic range a qualified buyer would pay. The owner now has a clear picture of what to expect and can make decisions about timing, improvements, and deal structure.

If that owner spent the next 12 months reducing his involvement in sales (by hiring a part time estimator) and diversifying away from that one large commercial client, the multiple could move closer to 3.0x or even above it. That's the power of getting a BOV early. It shows you exactly where to focus.

How a BOV Differs from Online Valuation Calculators

Online valuation calculators are a great starting point. I built one myself at /calculators because I believe every owner should have a ballpark sense of their business value.

But here's where calculators fall short.

They can't account for nuance. A calculator takes your SDE and multiplies it by an industry average. It doesn't know that your lease is below market, that your top employee just gave notice, or that you have a pending lawsuit. These things dramatically affect what a buyer will pay.

They use broad industry averages. A calculator might say landscaping businesses sell for 2.5x SDE. But a landscaping company in Phoenix with 12 month revenue is very different from one in Minnesota with a 7 month season. The multiple should reflect that.

They don't factor in comparable sales. I have access to databases with thousands of actual business transactions. I can see what a landscaping company with $200,000 SDE in the Southeast actually sold for last quarter. A calculator doesn't have that data.

They can't assess owner dependency. One of the biggest value drivers (or destroyers) is how dependent the business is on the owner. A calculator has no way to measure this. An experienced broker evaluates it in every BOV.

They don't consider deal structure. Many business sales include seller financing, earnouts, or training periods. These terms affect the effective value of the deal. A BOV considers realistic deal structures, while a calculator just gives you a raw number.

Use the calculator to get oriented. Use a BOV to get serious.

Factors That Increase or Decrease Your BOV

Your BOV isn't a fixed number. It's influenced by dozens of factors, some you can control and some you can't. Here are the ones that matter most.

Factors that increase value:

- Recurring revenue. Subscription models, maintenance contracts, and long term service agreements make your revenue predictable. Buyers pay a premium for predictability. A business with 70% recurring revenue can command a 20 to 30% higher multiple than one with all project based income.

- Low owner dependency. If the business runs without you, it's worth more. Buyers are buying a system, not a job. The less the business depends on any single person (including you), the higher the value.

- Revenue growth trends. Three consecutive years of 10%+ growth is one of the strongest value drivers. It tells buyers the business has momentum.

- Diversified customer base. No single customer should represent more than 10 to 15% of revenue. Customer concentration is one of the first things buyers and lenders look at.

- Strong team with tenure. Experienced employees who stay through the transition are worth their weight in gold. High turnover signals management problems and increases buyer risk.

- Clean financials. Organized, accurate financial records make due diligence easier and signal that the business is professionally managed. Messy books scare buyers away.

- Favorable lease terms. A long term lease at a good rate in a strong location is a hidden asset. It provides stability and protects the buyer from rent increases.

Here's a quick reference for the most common value drivers:

| Factor | Impact on Value | Why It Matters |

|---|---|---|

| Recurring revenue (70%+) | +20 to 30% multiple | Predictable cash flow reduces buyer risk |

| Owner works <20 hrs/week | +15 to 25% multiple | Business runs as a system, not a job |

| 3+ years of 10%+ growth | +10 to 20% multiple | Momentum signals future returns |

| No customer over 15% of revenue | Protects value | Diversification reduces single point failure |

| Declining revenue | -15 to 30% multiple | Raises questions about business viability |

| Owner is the business | -20 to 40% multiple | Buyer is purchasing a job, not an asset |

Factors that decrease value:

- Heavy owner involvement. If you're the top salesperson, the lead technician, and the only person who knows the passwords, your business is really just a well paying job. Buyers see that risk clearly.

- Declining revenue. Even one year of decline raises questions. Two or three years of decline will significantly reduce your multiple.

- Customer concentration. If you lose your biggest client, what happens? If the answer is "the business is in serious trouble," your BOV will reflect that risk.

- Deferred maintenance. Equipment that's falling apart, a building that needs repairs, or technology that's 15 years old all reduce value. Buyers factor in the cost of catching up.

- Pending legal issues. Lawsuits, regulatory problems, or unresolved tax issues create uncertainty. Uncertainty always lowers value.

- Industry headwinds. If your industry is facing disruption, regulation, or declining demand, your multiple will reflect the broader trend regardless of your individual performance.

How to Use the BOV in Your Exit Planning

A BOV isn't just a number. It's a planning tool. Here's how to use it strategically.

Set your target exit price. Most owners have a number in their head that represents financial freedom. Maybe it's $500,000 after taxes and fees. Your BOV tells you whether that number is realistic today or whether you need more time to build value.

Identify your value gaps. Your BOV should highlight the specific factors dragging your value down. If owner dependency is the issue, you know you need to hire a manager and delegate. If customer concentration is the problem, you know you need to diversify your revenue streams. This turns a vague goal ("increase business value") into a concrete action plan.

Choose the right time to sell. Timing matters in business sales just like it does in real estate. If your BOV shows you're at 2.5x SDE and your target requires 3.0x, your broker can help you build a 12 to 18 month roadmap to get there.

Price your listing correctly from day one. Overpriced businesses sit on the market for months, develop a reputation as stale listings, and eventually sell for less than they would have at the right price. A BOV prevents this by grounding your expectations in market reality.

Prepare for buyer questions. Buyers will ask how you arrived at your asking price. A well prepared BOV gives you a data backed answer. It shows buyers that the price is based on real comparable sales and industry multiples, not wishful thinking.

Evaluate offers objectively. When offers start coming in, your BOV gives you a benchmark. If the BOV range is $500,000 to $600,000 and you get an offer at $480,000, you know it's below range but close. If the offer is $350,000, you know it's unreasonable.

Ready to start planning your exit? Talk to me about getting a free BOV for your business. I'll walk you through where your business stands today and what it would take to reach your target.

When You Need a Formal Appraisal Instead of a BOV

A BOV covers most situations, but there are times when you need the legal weight of a formal appraisal.

SBA loan requirements. If the buyer is using an SBA loan to purchase your business and the deal is over $500,000, the lender will require a third party business appraisal from an accredited appraiser. This is a federal requirement, and there's no way around it. The appraisal protects the lender by providing an independent opinion of value.

Divorce settlements. Family courts typically require formal appraisals when a business is a marital asset. A BOV can help you understand the value early in the process, but your attorney will likely need a USPAP compliant appraisal for the final settlement.

Estate and gift tax filings. The IRS requires defensible valuations for estate and gift tax purposes. If you're transferring business ownership to family members or structuring your estate plan, a formal appraisal from an accredited valuator is essential.

Litigation. If the business value is being disputed in court (partnership disputes, shareholder lawsuits, breach of contract claims), you need an appraisal that can withstand cross examination. A BOV won't hold up in this context.

ESOP transactions. Employee stock ownership plans require annual valuations by independent appraisers. This is one of the most regulated areas of business valuation.

In these situations, expect to pay $5,000 to $15,000 for a formal appraisal, and the process will take 4 to 8 weeks. Your broker can often recommend qualified appraisers they've worked with before.

Red Flags: When a BOV Is Too High

Here's something most articles won't tell you. Not all BOVs are honest.

Some brokers inflate their valuations to win your listing. They tell you your business is worth $1.2 million when the market says $800,000. You sign an exclusive listing agreement based on that inflated number, the business sits on the market for 6 months with no offers, and then the broker suggests a price reduction to where it should have been all along.

This happens more often than you'd think. Here's how to spot it.

The multiple seems unusually high. If a broker tells you your restaurant is worth 4.0x SDE when the industry average is 1.5x to 2.5x, ask for the comparable sales data that supports that multiple. If they can't provide it, that's a problem.

They don't ask for detailed financials. A broker who gives you a value after looking at one year of tax returns and a five minute conversation hasn't done enough work. A real BOV requires a thorough analysis of at least three years of financial data.

They focus on revenue, not earnings. Buyers don't pay for revenue. They pay for cash flow. If a broker values your business based on a revenue multiple without calculating your SDE or EBITDA, they're skipping the most important step.

They don't discuss the risks. Every business has risk factors. If a broker's BOV doesn't mention customer concentration, owner dependency, lease expiration, or other potential issues, they're painting an incomplete picture.

They pressure you to sign quickly. A good broker gives you the BOV and lets you process it. A broker who inflated the number wants you to sign before you get a second opinion.

My advice: always get at least two opinions. A legitimate broker will welcome the comparison because they're confident in their analysis.

If a broker's valuation sounds too good to be true, it probably is. The best brokers tell you what you need to hear, not what you want to hear.

Thinking about selling your business and want an honest valuation? Schedule a free consultation and I'll prepare a BOV based on your actual financials and real comparable sales data.

The Bottom Line

A broker opinion of value is one of the smartest moves you can make as a business owner, whether you're selling next month or five years from now. It gives you clarity about where you stand, shows you where to improve, and prevents the kind of pricing mistakes that cost sellers tens of thousands of dollars.

The process is straightforward. You share your financials, your broker analyzes the data, and you get a realistic picture of what your business is worth in today's market. It costs nothing (most brokers offer it free as part of a listing consultation) and takes less than a week.

Don't guess what your business is worth. Don't rely solely on an online calculator. And definitely don't trust a broker who throws out a high number without doing the work.

Get a real BOV. Make informed decisions. Sell your business for what it's actually worth.

Want to start with a quick estimate? Use our free valuation calculator to see your business's estimated value based on industry SDE multiples.

Ready for a professional opinion? Get in touch for a free broker opinion of value. I'll give you an honest assessment based on your financials, comparable sales, and current market conditions.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.