When you're selling your business, there's a section of the purchase agreement that your attorney will spend more time on than almost anything else. It's called representations and warranties, often shortened to "reps and warranties," and it's the part of the deal that defines what you're promising about your business and what happens if those promises turn out to be wrong.

Most sellers gloss over this section. It feels like legal boilerplate. Page after page of statements that seem obvious: "The seller has the legal authority to enter into this agreement." "The financial statements are accurate." "There are no pending lawsuits." Of course, you think. Why would I sign this if any of that weren't true?

But reps and warranties are far more than formalities. They're the foundation of the buyer's legal protection. If something goes wrong after closing, the buyer's first move will be to look at what you represented and warranted in the purchase agreement. If your representations were inaccurate, even unintentionally, you could be on the hook for damages.

I've seen sellers caught off guard by this. They assumed that once the deal closed, they were done. But a poorly negotiated reps and warranties section can come back to haunt you months or even years after you've cashed the check. Understanding what you're signing is essential.

Broker's note: Reps and warranties are not just legal formalities. They are the section of the deal that determines whether you walk away clean or spend the next two years defending claims from the buyer's attorney. Treat every line as if it has real financial consequences, because it does.

What Are Representations and Warranties?

Let me break these two terms apart because they're technically different, even though they're always discussed together.

Representations are statements of fact about your business as of a specific date. When you represent that your business has no outstanding tax liabilities, you're stating that as a fact. Representations are backward looking. They describe the current and historical state of your business.

Warranties are promises that certain conditions are true and will continue to be true through closing (and sometimes beyond). When you warrant that there are no material adverse changes to the business between signing and closing, you're making a forward looking promise.

In practice, the distinction rarely matters in negotiation. Lawyers draft these sections with overlapping language to cover both bases. What matters to you as a seller is that you understand what you're stating as fact, what you're promising, and what the consequences are if any of it is wrong.

The Most Common Reps and Warranties Sellers Make

Every purchase agreement is different, but there's a standard set of representations and warranties that appears in virtually every business sale. Here's what you'll be asked to affirm.

Authority and capacity. You have the legal right to sell the business. If it's an LLC, the operating agreement allows the sale. If it's a corporation, the board has approved it. If there are multiple owners, everyone has consented. This seems straightforward, but I've seen deals where a minority partner hadn't actually agreed and the whole thing fell apart.

Financial statements accuracy. Your financial statements fairly present the financial condition of the business. This is one of the most important reps because the buyer is basing their purchase price on your reported earnings. If the financials turn out to be materially inaccurate, this is the representation the buyer will point to.

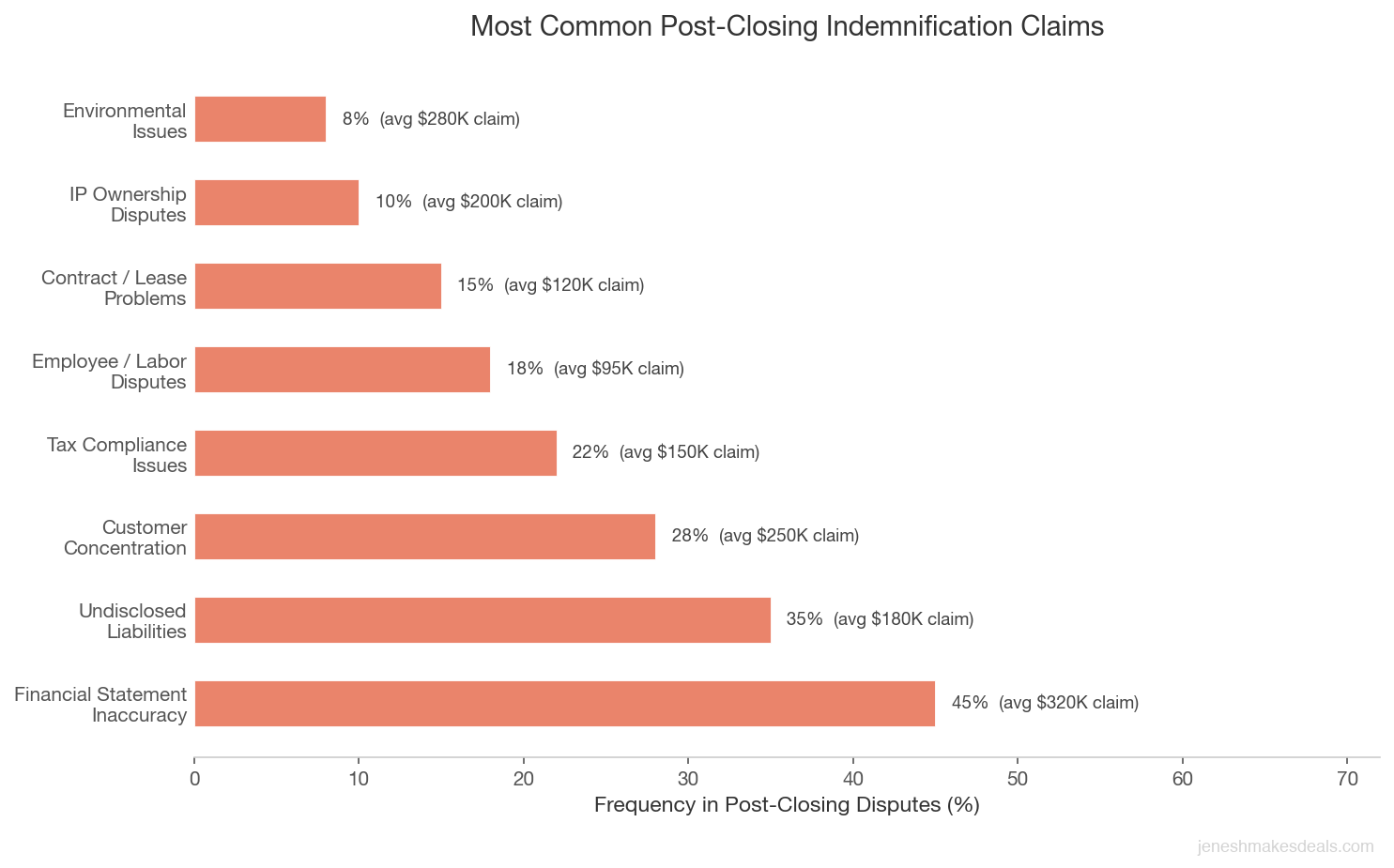

No undisclosed liabilities. There are no material debts, obligations, or liabilities that haven't been disclosed to the buyer. This includes pending lawsuits, tax disputes, employee claims, and any other obligations that could surprise the buyer after closing.

Tax compliance. The business has filed all required tax returns and paid all taxes owed. Any outstanding tax issues have been disclosed. Unfiled returns or unpaid taxes discovered after closing can trigger indemnification claims.

Legal compliance. The business complies with all applicable laws, regulations, and permits. This covers everything from employment law to environmental regulations to industry specific licensing requirements.

Material contracts. All significant contracts have been disclosed and are in good standing. This includes customer agreements, vendor contracts, equipment leases, loan agreements, and the lease for your business premises.

Employee matters. All employee related obligations have been met: wages paid, benefits provided, employment taxes remitted. There are no pending or threatened employee claims, discrimination complaints, or labor disputes.

Intellectual property. The business owns or has the right to use all intellectual property necessary for its operations, and that IP doesn't infringe on anyone else's rights. This covers trade names, trademarks, proprietary software, customer lists, and trade secrets.

No material adverse change. Between the date of the purchase agreement and closing, there has been no material adverse change in the business. Revenue hasn't dropped significantly, key employees haven't left, major customers haven't canceled, and no new liabilities have emerged.

Environmental compliance. The business operations comply with environmental laws, and there are no known contamination issues. This is especially important for manufacturing, auto repair, dry cleaning, and other businesses that handle hazardous materials.

| Representation | What You're Affirming | Why It Matters |

|---|---|---|

| Authority and Capacity | You have the legal right to sell | Prevents disputes with co owners or corporate governance issues |

| Financial Statements Accuracy | Your reported numbers are correct | Buyer's purchase price depends on these figures |

| No Undisclosed Liabilities | No hidden debts or obligations | Protects buyer from surprise costs after closing |

| Tax Compliance | All returns filed and taxes paid | Unfiled returns can trigger indemnification claims |

| Legal Compliance | Business follows all applicable laws | Violations can result in fines or forced shutdowns |

| Material Contracts | All key contracts disclosed and current | Buyer needs to know what obligations transfer with the sale |

| Employee Matters | All wages, benefits, and taxes are current | Unpaid obligations become the buyer's problem post closing |

| Intellectual Property | Business owns or licenses all required IP | IP disputes can shut down core operations |

Need help preparing your business for sale? Contact us for a free consultation and we'll help you identify potential issues before they become deal problems.

How Reps and Warranties Protect the Buyer

From the buyer's perspective, reps and warranties serve three important purposes.

Due diligence verification. Even after thorough due diligence, the buyer can't verify everything. Reps and warranties fill the gap. If the buyer asks "are there any pending lawsuits?" and you say no, you've now made that a legal representation. If a lawsuit surfaces after closing that existed before closing, the buyer has recourse.

Risk allocation. Reps and warranties determine who bears the risk of undisclosed or unknown problems. If something bad turns out to be true that contradicts your representations, you bear the financial consequences. This is fair because you know your business better than the buyer does, even after due diligence.

Indemnification trigger. The reps and warranties section is directly linked to the indemnification section of the purchase agreement. Indemnification is the mechanism by which the buyer can recover losses caused by inaccurate representations. Without reps and warranties, the buyer has no clear basis for a claim if something goes wrong after closing.

What Sellers Need to Negotiate

As a seller, your goal in negotiating reps and warranties is to be honest and fair while limiting your exposure to unreasonable claims. Here are the key points to negotiate.

Knowledge qualifiers. Add "to the seller's knowledge" or "to the best of the seller's knowledge" where appropriate. This limits your representations to things you actually know about. Without this qualifier, you could be liable for problems you didn't know existed. For example, "To the seller's knowledge, there are no pending claims against the business" is very different from "There are no pending claims against the business."

Materiality thresholds. Push for materiality qualifiers on representations. Instead of warranting that "all vendor contracts are in good standing," negotiate to say "all material vendor contracts are in good standing." This prevents the buyer from making a claim over a minor vendor dispute that has no real impact on the business.

Disclosure schedules. Disclosure schedules are your safety net. They're appendices to the purchase agreement where you list every exception to your representations. If you know about a pending customer complaint, a minor tax dispute, or an equipment issue, you disclose it. Once something is on the disclosure schedule, the buyer can't later claim they didn't know about it.

Take disclosure schedules seriously. Your attorney should help you prepare them, and you should be thorough. Forgetting to disclose something that later becomes an issue is much worse than disclosing it upfront.

Survival periods. Reps and warranties don't last forever. The survival period defines how long after closing the buyer can make a claim based on a breach of your representations. Standard survival periods for general reps are 12 to 24 months. Some fundamental representations (like authority to sell and tax compliance) may survive longer, sometimes up to the statute of limitations.

As a seller, you want survival periods to be as short as reasonably possible. The buyer wants them as long as possible. The negotiation usually lands somewhere in the middle.

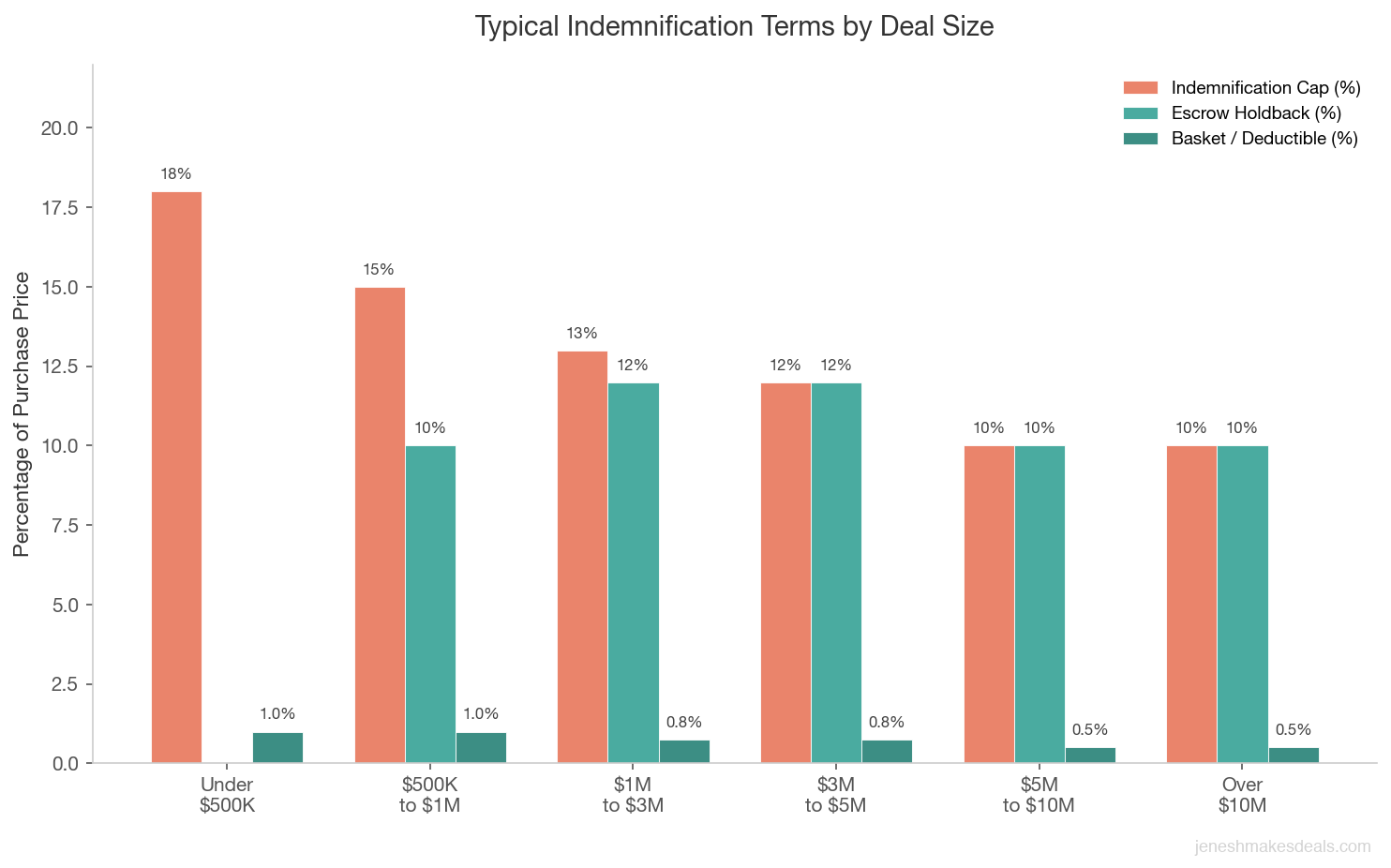

Indemnification caps. The indemnification section should include a cap on your total liability. A common cap is 10% to 20% of the purchase price. This means that even if your representations turn out to be wildly inaccurate, your maximum exposure is limited. Without a cap, you could theoretically owe more than you received for the business.

Baskets and deductibles. These work like insurance deductibles. A "basket" sets a minimum threshold for claims. The buyer can't make an indemnification claim until their total losses exceed the basket amount (often 0.5% to 1% of the purchase price). A "tipping basket" means once the threshold is crossed, the buyer can recover from dollar one. A "true deductible" means the buyer only recovers amounts above the threshold.

The Disclosure Schedule: Your Best Protection

I can't emphasize this enough: the disclosure schedule is the most important document you'll prepare as a seller. It's where you lay everything on the table, and it's what protects you from claims after closing.

Every representation in the purchase agreement that starts with something like "except as set forth in the disclosure schedule" gives you an opportunity to carve out known issues. Use it.

Here's how to approach your disclosure schedules:

Be comprehensive. When in doubt, disclose. It's better to over disclose than to leave something out. If you're unsure whether a customer complaint is "material," disclose it anyway with a note explaining why you don't consider it material.

Be specific. Vague disclosures don't protect you. Instead of "There are some ongoing vendor disputes," write "ABC Supply Co. is disputing Invoice #1234 dated January 15, 2026, in the amount of $3,200. The seller believes this dispute will be resolved without material impact."

Organize by representation. Each disclosure schedule item should reference the specific representation it relates to. This makes it clear which exceptions apply to which promises.

Update through closing. Most purchase agreements require you to update your disclosure schedules between signing and closing. If you learn about a new issue after signing, disclose it promptly. Failing to update the schedules can be treated as a breach of your representations.

Work with your attorney. Preparing disclosure schedules is not a DIY project. Your M&A attorney will know what level of detail is needed and will help you frame disclosures in a way that protects you without alarming the buyer.

Key takeaway: When it comes to disclosure schedules, more is always better than less. I have never seen a seller get in trouble for disclosing too much. I have seen plenty of sellers face post closing claims because they left something off the list and assumed the buyer already knew about it.

Common Mistakes Sellers Make With Reps and Warranties

After working on many deals, I see the same mistakes come up repeatedly.

Not reading the purchase agreement carefully. Some sellers sign the purchase agreement without truly understanding what they're representing and warranting. They trust their attorney to handle it. While you should have a good attorney, you also need to personally understand every material representation you're making. If you don't understand something, ask.

Overpromising to close the deal. When you're eager to get the deal done, it's tempting to agree to broad, unqualified representations just to move things along. Resist this urge. Every representation is a potential liability. Take the time to negotiate appropriate qualifiers and limitations.

Incomplete disclosure schedules. The most common post closing disputes I've seen involve things the seller knew about but didn't disclose. Maybe it seemed minor at the time. Maybe they thought the buyer already knew. Maybe they just forgot. None of those are good defenses if the buyer suffers a loss.

Ignoring the survival period. Some sellers don't realize that their obligations continue after closing. They cash the check, take a vacation, and then get a call from the buyer's attorney 10 months later claiming a breach of representation. Understand how long your exposure lasts and plan accordingly.

Not setting aside an escrow or holdback. In many deals, a portion of the purchase price is held in escrow to cover potential indemnification claims. As a seller, you might resist this because you want all your money at closing. But an escrow actually protects both parties by providing a clear mechanism for resolving disputes without litigation.

Warning for sellers: The most expensive mistake in any deal is rushing through the reps and warranties to get to closing faster. A 10% to 15% escrow holdback for 12 to 18 months is standard and fair. Sellers who fight against reasonable escrow terms often signal to buyers that they are hiding something, which can erode trust and put the entire deal at risk.

Want to understand how deal structure affects your outcome? Contact us for a free consultation and we'll explain the key terms that matter most.

How Reps and Warranties Vary by Deal Size

The scope and complexity of reps and warranties tends to scale with deal size.

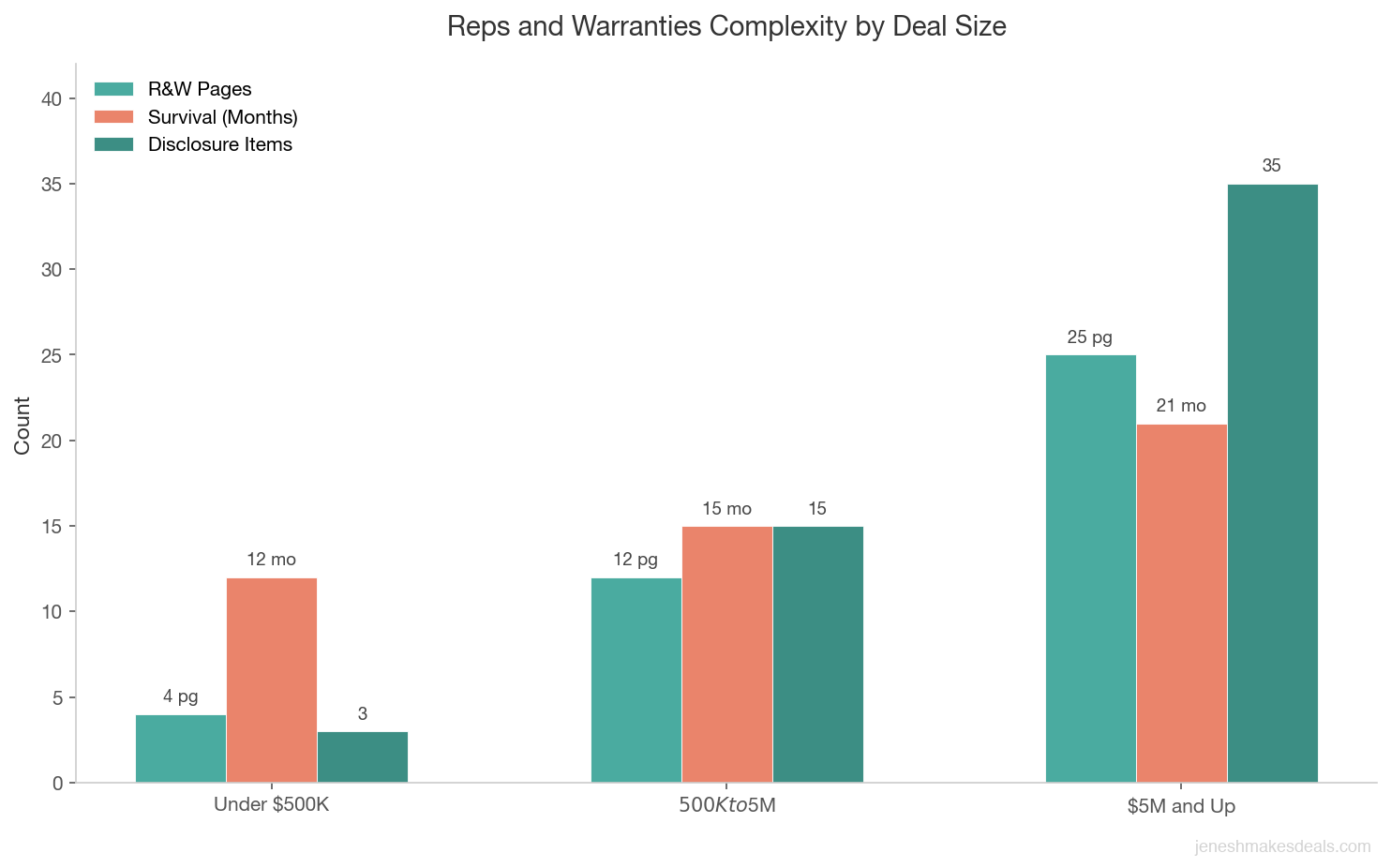

Small deals (under $500,000). The reps and warranties section is usually shorter and more straightforward. There may be fewer carve outs and simpler disclosure schedules. But the fundamentals, financial accuracy, no undisclosed liabilities, legal compliance, should still be there.

Mid market deals ($500,000 to $5 million). This is where reps and warranties get more detailed. Expect separate schedules for customer lists, vendor contracts, employee details, intellectual property, and environmental issues. Survival periods and indemnification caps are negotiated more carefully.

Larger deals ($5 million and up). At this level, the reps and warranties section can be 20 to 30 pages long. There are usually separate representations for every material aspect of the business, extensive disclosure schedules, and a dedicated indemnification section with complex basket and cap structures. Representation and warranty insurance (RWI) may also come into play.

| Deal Element | Under $500K | $500K to $5M | $5M and Up |

|---|---|---|---|

| Reps and Warranties Length | 3 to 5 pages | 8 to 15 pages | 20 to 30 pages |

| Typical Survival Period | 12 months | 12 to 18 months | 18 to 24 months |

| Indemnification Cap | 15% to 20% of price | 10% to 15% of price | 10% of price or RWI policy |

| Basket / Deductible | 1% of price | 0.5% to 1% of price | 0.5% of price |

| Escrow Holdback | Rare | 10% to 15% for 12 months | 10% for 12 to 18 months |

| RWI Insurance | Not available | Occasionally | Common |

| Disclosure Schedules | Simple, 2 to 5 items | Detailed, 10 to 20 items | Extensive, 30+ items |

Representation and Warranty Insurance

For larger deals, there's a product called representation and warranty insurance (RWI) that's become increasingly popular. Here's how it works.

The buyer purchases an insurance policy that covers losses arising from breaches of the seller's representations and warranties. If the seller's financial statements turn out to be inaccurate, or if an undisclosed liability surfaces, the insurance pays the claim instead of the seller.

RWI benefits both parties:

- For sellers: It limits your post closing exposure. Instead of having indemnification claims hanging over your head for 18 months, the insurance handles it. This allows you to receive more of the purchase price at closing rather than having it held in escrow.

- For buyers: It provides a well capitalized source of recovery. Instead of chasing a former owner who may have already spent the sale proceeds, the buyer makes a claim against a well funded insurance company.

RWI is most common in deals above $10 million, but it's becoming available for smaller transactions. The premium is typically 2% to 4% of the coverage limit. For a $5 million deal with $1 million in coverage, expect a premium of $20,000 to $40,000.

Working With Your Attorney on Reps and Warranties

Your M&A attorney earns their fee in the reps and warranties negotiation more than anywhere else. Here's how to work with them effectively.

Be completely honest with your attorney. Tell them everything, even the embarrassing stuff. Your attorney can't protect you from problems they don't know about. Attorney client privilege protects your conversations, so there's no reason to hold back.

Provide all requested documents promptly. Your attorney needs to review contracts, financial statements, employee records, and other documents to help you prepare accurate representations and thorough disclosure schedules. Delays from you create delays in the deal.

Participate in the negotiation process. Don't just hand it off to your lawyer. Understand what's being negotiated and why. Some points are worth fighting for. Others aren't. Your business judgment should inform the legal strategy.

Don't try to save money on legal fees here. This is not the place to cut corners. An experienced M&A attorney who negotiates strong protections in your reps and warranties section can save you far more than their fee. An attorney who misses something can cost you far more than you saved.

The Bottom Line

Representations and warranties are the legal backbone of your business sale. They define what you're promising about your business, how long those promises last, and what happens if something you said turns out to be wrong.

The key takeaways for sellers are simple:

- Read and understand every representation you make. Don't sign anything you don't fully comprehend.

- Negotiate appropriate qualifiers. Knowledge qualifiers, materiality thresholds, and reasonable survival periods protect you from unfair claims.

- Take disclosure schedules seriously. Disclose everything you know about. Over disclosure is always better than under disclosure.

- Set reasonable indemnification limits. Caps, baskets, and escrow terms should reflect the size of the deal and the actual risk involved.

- Work with an experienced M&A attorney. This is not a place for general practitioners or online templates.

The goal isn't to avoid making any representations. That's not realistic and no buyer would agree to it. The goal is to make honest, accurate representations with appropriate protections that let you sleep well after the deal closes.

Ready to start the selling process? Contact us for a free consultation and we'll connect you with the right professionals to protect your interests at every step.

Want to know what your business is worth? Try our free business valuation calculator to get a starting estimate.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.