You've spent months preparing your business for sale. A buyer shows interest, tours the operation, reviews your financials, and then sends over a letter of intent.

This is the moment most sellers have been waiting for. But it's also the moment where I've seen the most costly mistakes. Sellers get excited about the number at the top of the page, sign the LOI without reading the fine print, and then spend the next 90 days stuck in a deal that slowly falls apart.

The letter of intent is one of the most important documents in the entire sale process. It sets the tone for everything that follows: due diligence, the purchase agreement, and closing. Getting it right matters more than most sellers realize.

I've worked with hundreds of sellers navigating LOIs, and I want to walk you through everything you need to know before you sign one.

What Is a Letter of Intent and Why It Matters

A letter of intent (LOI) is a written document from a buyer outlining the key terms and conditions under which they intend to purchase your business. Think of it as a formal handshake before the real paperwork begins.

The LOI isn't the final purchase agreement. It's a summary of the deal structure both sides agree to before moving into due diligence and drafting the definitive purchase agreement. Most LOIs are between 3 and 10 pages long, depending on the complexity of the deal.

Here's why the LOI matters so much:

- It establishes the deal framework. The price, payment structure, timeline, and key conditions are all laid out. Everything that follows is built on this foundation.

- It signals buyer seriousness. A buyer who puts together a detailed LOI with specific terms has done their homework. Vague or sloppy LOIs often signal a buyer who isn't ready.

- It creates exclusivity. Most LOIs include a no shop clause that prevents you from talking to other buyers for a set period. Once you sign, you're committed to that buyer.

- It sets the negotiation anchor. Whatever you agree to in the LOI becomes the starting point for the purchase agreement. Terms that aren't addressed in the LOI often get filled in by the buyer's attorney later, and rarely in your favor.

The LOI is where the real deal gets shaped. If you don't pay attention here, you'll be fighting uphill for the rest of the transaction.

The LOI is not just a piece of paper you sign to move things along. It is the blueprint for your entire transaction, and every term you agree to here becomes the foundation for the purchase agreement.

Binding vs. Non Binding Terms: Know the Difference

One of the biggest misunderstandings sellers have about LOIs is the distinction between binding and non binding terms. Most LOIs contain both, and confusing the two can cost you.

Non binding terms are provisions the buyer intends to follow but isn't legally obligated to honor. If negotiations change or due diligence reveals something unexpected, these terms can be renegotiated or dropped entirely.

Binding terms are legally enforceable. If either party violates a binding term, the other side has legal recourse.

What's Typically Non Binding

- Purchase price. The price in the LOI is almost always non binding. It's a strong indication of what the buyer will pay, but it can change based on what due diligence reveals.

- Payment structure. Whether the deal is all cash, includes seller financing, or involves an earnout, these terms can shift before closing.

- Due diligence contingencies. The buyer's right to inspect financials, operations, legal matters, and customer contracts is stated but subject to change.

- Transition period. How long the seller will stay to help after closing is typically negotiable throughout the process.

- Representations and warranties. The scope of what the seller guarantees about the business is usually finalized in the purchase agreement, not the LOI.

What's Typically Binding

- Exclusivity (no shop period). Once you sign, you can't entertain other offers for the duration specified. This is almost always binding and enforceable.

- Confidentiality. Both parties agree to keep deal details private. Violating this can result in legal action.

- Break up fees (if included). Some LOIs include penalties if one side walks away without cause. These are binding when present.

- Governing law. Which state's laws govern the agreement is typically binding from the LOI stage.

- Expense allocation. Who pays for what during due diligence (legal fees, accounting, environmental assessments) is often a binding provision.

The key takeaway: just because most of the LOI is non binding doesn't mean you can treat it casually. The binding provisions, especially exclusivity, have real consequences. And non binding terms set expectations that are difficult to change later without creating friction.

Here's a quick reference for which LOI provisions are typically binding versus non binding:

| Provision | Typically Binding? | Why It Matters |

|---|---|---|

| Purchase price | No | Can change based on due diligence findings |

| Payment structure | No | Seller notes, earnouts, and cash split are negotiable until closing |

| Due diligence contingencies | No | Scope and timeline often shift during the process |

| Transition period | No | Hours, duration, and compensation are finalized in the purchase agreement |

| Exclusivity (no shop) | Yes | You cannot talk to other buyers for the full duration |

| Confidentiality | Yes | Violating this can result in legal action from either side |

| Break up fee | Yes (when included) | Financial penalty if one party walks away without cause |

| Governing law | Yes | Determines which state's courts handle disputes |

| Expense allocation | Yes | Defines who pays for legal, accounting, and assessment costs |

Key Sections Every LOI Should Include

A well written LOI covers the essential deal terms clearly and specifically. Here's what I look for when reviewing an LOI on behalf of a seller.

Purchase Price and Payment Structure

The LOI should state the total purchase price and exactly how it will be paid. This includes:

- Cash at closing. The amount the seller receives on the day the deal closes.

- Seller financing. If the buyer expects you to carry a note, the LOI should specify the amount, interest rate, term length, and any collateral.

- Earnout provisions. Performance based payments tied to future revenue or profit targets. The LOI should outline the metrics, measurement period, and payment schedule.

- Escrow or holdback. Many deals include a portion of the purchase price held in escrow for 12 to 18 months to cover potential indemnification claims.

If the LOI just says "$1.5 million" without breaking down the payment structure, that's a problem. A seller note for $500,000 over five years at 5% interest is very different from $1.5 million cash at closing.

Due Diligence Period and Scope

The LOI should define how long the buyer has to complete due diligence and what areas they'll be reviewing. Standard due diligence periods run 30 to 60 days for small to mid size businesses.

Conditions to Closing

These are the things that must happen before the deal can close:

- Buyer secures financing (SBA loan approval, for example)

- Satisfactory completion of due diligence

- Landlord consent for lease assignment

- Key employee agreements

- Required regulatory approvals

Transition Period

The LOI should outline whether the seller is expected to stay post closing and for how long. Most deals require 30 to 90 days of transition support, though some buyers request 6 to 12 months for complex operations.

Non Compete Agreement

Nearly every LOI includes a non compete clause. The LOI should specify the geographic scope, duration, and restricted activities. Standard non competes run 3 to 5 years within a defined geographic area.

Timeline to Closing

The LOI should include a target closing date or a specific timeline from execution (e.g., "90 days from LOI signing"). Without a timeline, deals drift and momentum dies.

Thinking about selling your business? Get a free valuation estimate to understand where your business stands before you start fielding offers.

How to Evaluate an LOI Beyond Just the Price

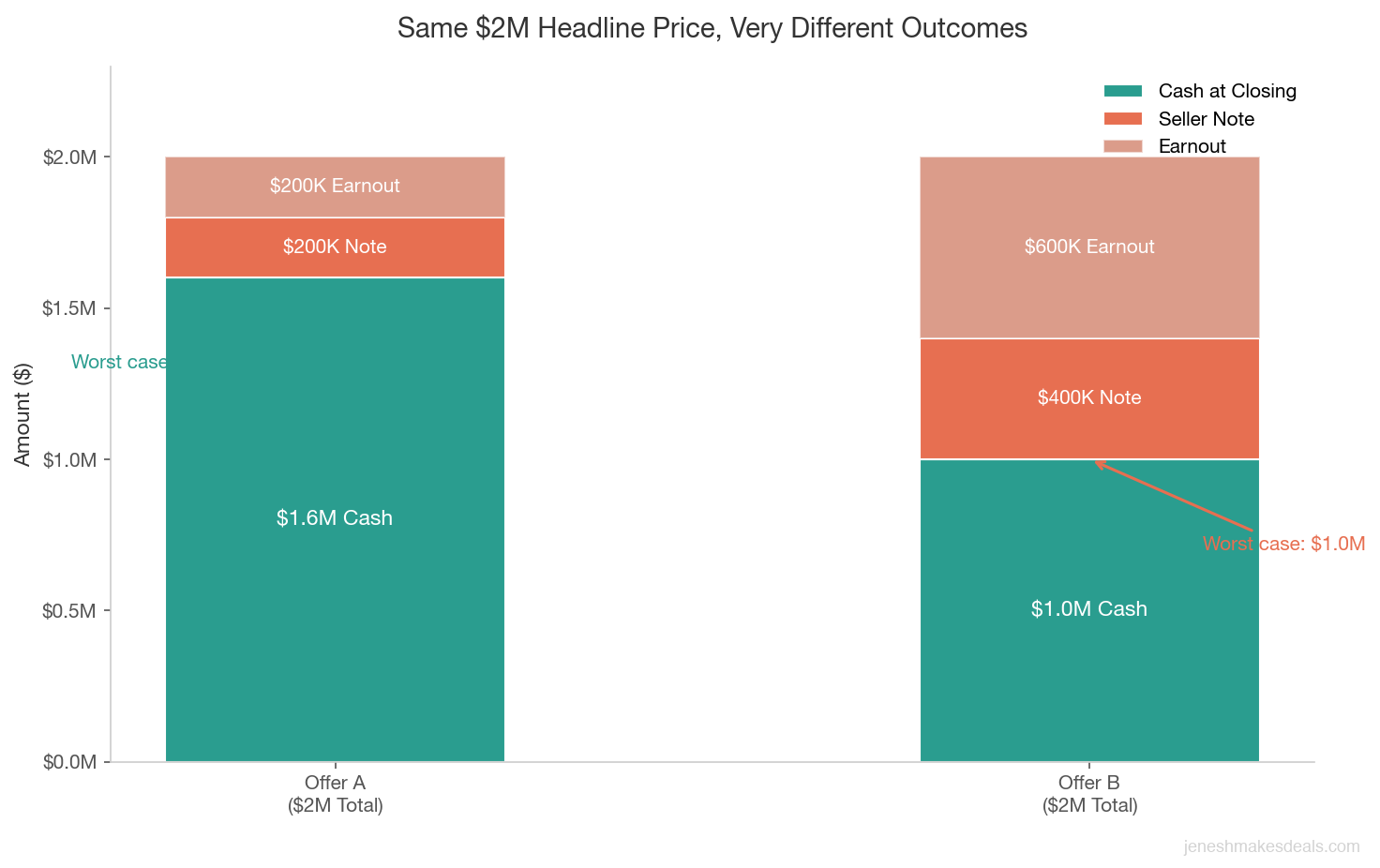

This is where most sellers go wrong. They see a big number and sign immediately. But two LOIs with the same headline price can deliver wildly different outcomes for the seller.

Here's what to look at beyond the purchase price.

The Actual Cash You'll Receive at Closing

Break the payment structure into what you'll get on day one versus what you might get later. A $2 million offer with $1.2 million cash at closing and an $800,000 earnout is not the same as $2 million cash at closing. Earnouts are uncertain. Seller notes carry risk. Escrow holdbacks can be clawed back.

I tell my clients to evaluate the "worst case scenario" of each LOI. If the earnout targets aren't met and the escrow gets claimed, what's the floor? That's the number you should compare across offers.

Earnout Terms

Earnouts can be fair or they can be traps. Look at:

- What metrics are used? Revenue based earnouts are better for sellers than profit based ones, because the buyer can manipulate expenses to reduce profit.

- Who controls the business during the earnout period? If the buyer makes operational changes that tank the metrics, you lose.

- How are disputes resolved? There should be a clear mechanism for disagreements about earnout calculations.

- Is there a cap? Make sure you know the maximum earnout amount.

Seller Note Details

If the buyer wants you to finance part of the deal, pay attention to:

- Interest rate. Current market rates for seller notes on small business acquisitions range from 5% to 8%. Anything below 5% is a red flag.

- Security/collateral. Is the note secured by business assets? Personal guarantee from the buyer?

- Subordination. Will the seller note be subordinate to the buyer's bank loan? SBA loans typically require this, which means the bank gets paid first if the business fails.

Transition Obligations

A 30 day transition at 20 hours per week is reasonable. A 12 month, full time commitment with no additional compensation is not. Make sure the LOI specifies hours, duration, and whether you'll be paid during the transition.

Non Compete Scope

A non compete that prevents you from opening the same type of business within 25 miles for 3 years is standard. A non compete that bars you from any business activity in your entire state for 10 years is unreasonable and potentially unenforceable.

LOI Red Flags vs. Green Flags: A Comparison

Here's a quick reference table I share with my clients. Use this to evaluate the LOI you receive.

| Section | What to Look For (Green Flag) | Red Flag |

|---|---|---|

| Purchase Price | Clear breakdown: cash, notes, earnout | Single number with no structure details |

| Payment Structure | 70%+ cash at closing | Less than 50% cash, heavy earnout reliance |

| Earnout Metrics | Revenue based, clear targets, capped | Profit based, vague targets, no cap |

| Seller Note | 5-7% interest, secured, 3-5 year term | Below market interest, unsecured, 7+ year term |

| Due Diligence Period | 30-60 days, defined scope | 90+ days, open ended scope |

| Exclusivity Period | 45-60 days | 90+ days with no milestones |

| Non Compete | 3-5 years, 25 mile radius, specific industry | 10+ years, statewide, all business activity |

| Transition Period | 30-90 days, defined hours, paid | 6-12 months, full time, unpaid |

| Financing Contingency | Pre approved or proof of funds | No mention of how deal will be funded |

| Conditions to Closing | Specific, reasonable, finite list | Vague ("satisfactory to buyer in their sole discretion") |

| Timeline | Target closing date within 90 days | No closing date or open ended timeline |

| Escrow/Holdback | 5-10% for 12 months | 20%+ for 18+ months |

If you see multiple red flags in a single LOI, it doesn't necessarily mean you should walk away. But it does mean you need to negotiate those terms before signing.

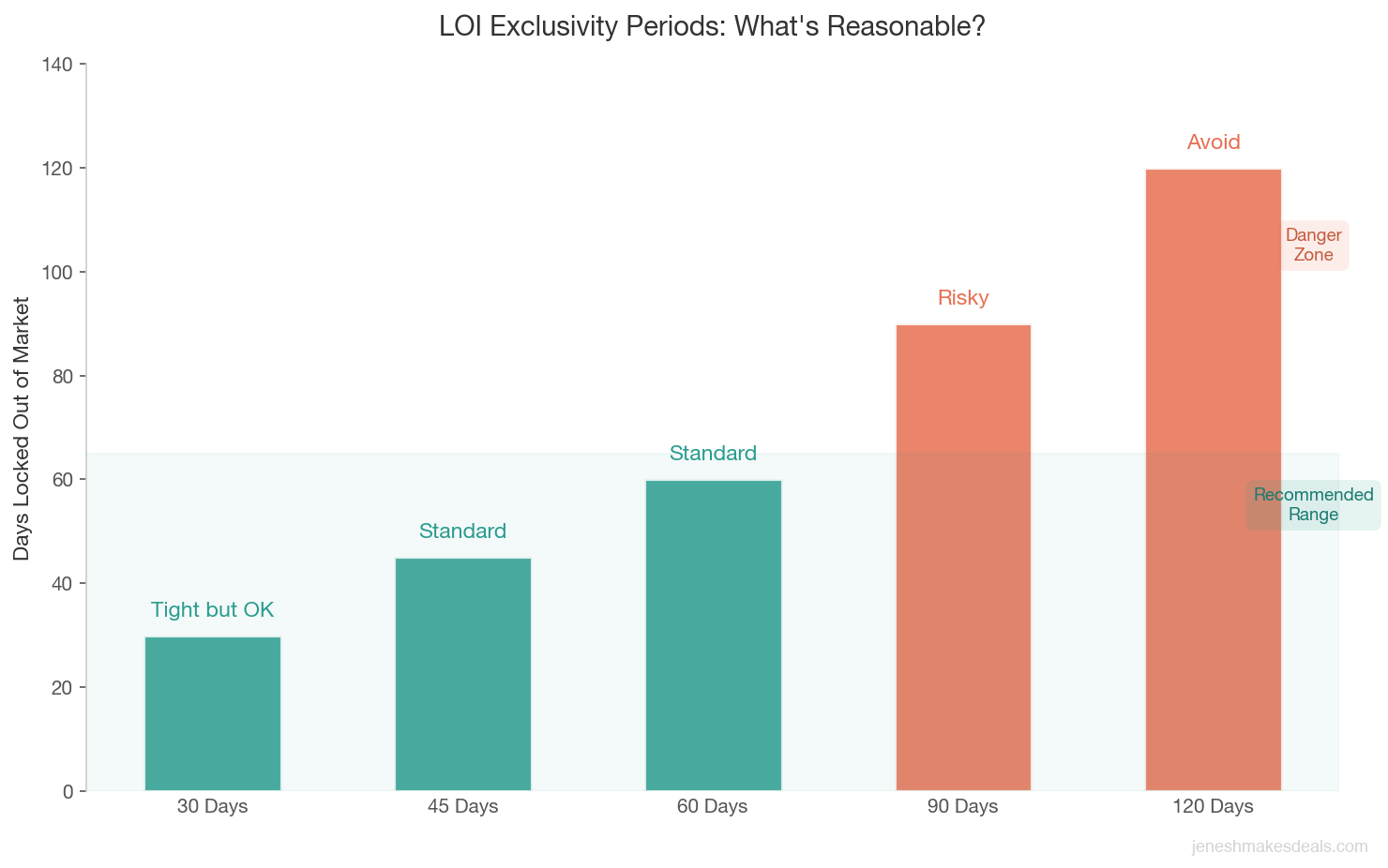

Exclusivity Periods: How Long Is Reasonable?

The exclusivity period (also called a no shop clause) is one of the most important binding provisions in the LOI. Once you sign it, you can't market your business, talk to other buyers, or accept competing offers for the duration.

Here's what I recommend:

- 45 to 60 days is standard and reasonable for most small to mid size business transactions. This gives the buyer enough time to complete due diligence without locking you out of the market for too long.

- 30 days is tight but acceptable if the buyer already has financing lined up and the business is straightforward.

- 90+ days should raise concerns. That's three months where you can't talk to anyone else. If the deal falls apart on day 85, you've lost an entire quarter.

How to Protect Yourself with Long Exclusivity Periods

If a buyer insists on a longer exclusivity period, negotiate protections:

- Milestone based extensions. Grant 45 days initially, with an option to extend by 30 days if the buyer has met specific milestones (financing application submitted, key due diligence items reviewed).

- Automatic termination triggers. If the buyer hasn't submitted a financing application within 21 days, the exclusivity expires.

- Break up fee. If the buyer walks away without cause after a long exclusivity period, they pay a fee (typically 1% to 3% of the purchase price) to compensate you for the lost time and market exposure.

The exclusivity period is where sellers have the most negotiating power. Once you sign the LOI, that power shifts to the buyer. Use it wisely.

Once you sign the exclusivity clause, your negotiating power shifts entirely to the buyer. The exclusivity period is the single most important binding term to get right before you put pen to paper.

Want to understand how deal structures affect your net proceeds? Try our free business valuation tools to model different scenarios.

How to Negotiate LOI Terms Without Killing the Deal

Negotiating an LOI is a balancing act. Push too hard and the buyer walks. Don't push at all and you end up with a bad deal. Here's how I coach my clients through it.

Pick Your Battles

You can't fight every term. Choose the 3 to 5 issues that matter most to you and focus your energy there. For most sellers, these are:

- Cash at closing amount

- Exclusivity period length

- Earnout structure and metrics

- Non compete scope

- Transition period obligations

Use "What If" Language

Instead of saying "I reject this term," try "What if we structured it this way instead?" This keeps the conversation collaborative rather than adversarial. Buyers are more likely to compromise when they feel like you're problem solving together.

Get Everything in Writing

Verbal agreements during LOI negotiations mean nothing. If the buyer agrees to shorten the exclusivity period or adjust the earnout metrics, it needs to be in the written LOI before you sign. I've seen deals where buyers agreed to changes over the phone but the written LOI stayed the same. Always verify the final document.

Don't Counter on Price Unless You Have Data

If you think the offer is too low, back it up with numbers. Show comparable sales in your industry, your trailing twelve months financials, and the growth trajectory. "I want more" isn't a negotiation strategy. "Businesses in my industry with my revenue and growth rate are selling at 3.2x SDE, and your offer is at 2.4x" gives the buyer something to respond to.

In my experience, the sellers who negotiate the best outcomes are the ones who come to the table with data, not emotions. A well researched counter offer backed by comparable sales and clear financials earns buyer respect and moves the deal forward faster.

Set a Response Deadline

LOIs shouldn't sit on your desk for weeks. Respond within 5 to 7 business days. If you need more time, communicate that to the buyer. Silence kills deals faster than tough negotiations.

Handling Multiple LOIs and Competing Offers

If you've done a good job marketing your business, you might receive multiple LOIs. This is ideal but needs careful management.

How to Compare Multiple Offers

Create a simple comparison matrix. For each LOI, line up:

- Total purchase price

- Cash at closing

- Seller note terms

- Earnout amount and likelihood of achievement

- Exclusivity period

- Due diligence timeline

- Non compete restrictions

- Transition requirements

- Buyer's financing status (pre approved vs. contingent)

- Cultural fit (will this buyer take care of your employees and customers?)

The highest price isn't always the best offer. An LOI at $1.8 million with 80% cash at closing from a pre approved SBA buyer is often better than a $2.2 million LOI with 50% cash and a 2 year earnout from a buyer who hasn't started the financing process.

Managing the Process

- Don't disclose specific competing terms. You can tell buyers you have multiple offers. You shouldn't share the specific price or terms of other LOIs. This keeps the process fair and avoids potential legal issues.

- Set a deadline for final offers. Give all buyers the same deadline to submit their best and final LOI. This creates urgency and ensures you can compare offers side by side.

- Consider a "best and final" round. If two offers are close, go back to both buyers and ask for their best and final terms. Be specific about what matters to you.

When to Accept and When to Wait

If you have one strong LOI that meets your goals, don't wait for a perfect offer that may never come. Deals have shelf lives. A buyer who is excited today might cool off in two weeks. I've seen sellers lose great deals because they held out for an extra $50,000 that never materialized.

Ready to start the selling process? Schedule a free consultation to discuss your business and what kind of offer you should expect.

What Happens After You Sign the LOI

Signing the LOI is not the finish line. It's the starting gun for the most intensive phase of the transaction.

The Post LOI Timeline

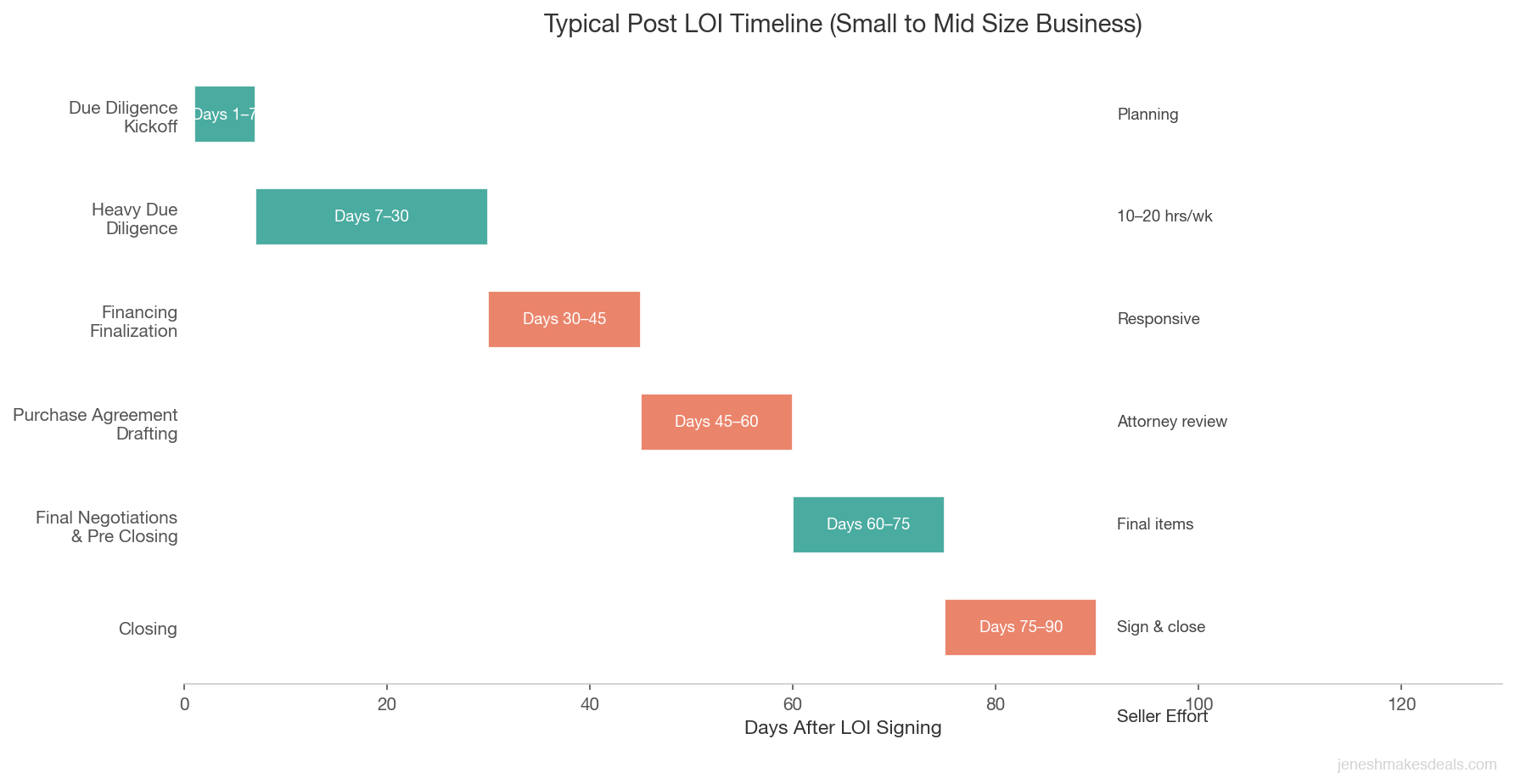

Here's what a typical post LOI timeline looks like for a small to mid size business:

Days 1 to 7: Due Diligence Kickoff The buyer's team (accountant, attorney, sometimes a business analyst) will send a due diligence request list. This typically includes 50 to 150 items: tax returns, P&L statements, balance sheets, customer contracts, vendor agreements, employee records, lease documents, insurance policies, and more.

Days 7 to 30: Heavy Due Diligence The buyer's team reviews your financials, visits the business, interviews key employees (with your permission), and analyzes the customer base. This is the most time consuming phase for you as the seller. Expect to spend 10 to 20 hours per week gathering documents and answering questions.

Days 30 to 45: Financing Finalization If the buyer is using SBA financing, the bank completes its underwriting process. The bank may request additional documentation or a third party business valuation.

Days 45 to 60: Purchase Agreement Drafting The buyer's attorney drafts the definitive purchase agreement based on the LOI terms. Your attorney reviews and redlines it. Expect 2 to 3 rounds of revisions.

Days 60 to 75: Final Negotiations and Pre Closing Any remaining issues get resolved. The closing date is confirmed. A closing checklist is created and executed. This includes lease assignments, license transfers, and bulk sale notices (if required by your state).

Days 75 to 90: Closing Both parties sign the definitive purchase agreement and all ancillary documents. Funds are wired. Ownership transfers. You hand over the keys.

What Can Go Wrong

The most common reasons deals fall apart after the LOI:

- Due diligence reveals problems. Revenue is declining, a key customer is leaving, or the financials don't match what was represented. This is the number one deal killer.

- Financing falls through. The buyer can't get approved for an SBA loan or the bank's valuation comes in lower than the purchase price.

- Lease issues. The landlord won't assign the lease or demands unreasonable terms for a new lease.

- Renegotiation. The buyer uses due diligence findings to try to reduce the price. Some retrades are legitimate. Others are tactics.

The best way to prevent post LOI surprises is to be transparent about your business from the start. If there's a known issue, disclose it before the LOI stage. Surprises during due diligence destroy trust and kill deals.

Common Mistakes Sellers Make with LOIs

After working on hundreds of transactions, here are the mistakes I see sellers make over and over.

Mistake 1: Accepting the Highest Price Without Reading the Terms

A $2 million offer sounds great until you realize $800,000 is tied to a 3 year earnout based on profit targets the buyer can manipulate, the non compete prevents you from working in your industry for a decade, and the transition period is 12 months of full time, unpaid work.

Always read the entire LOI. Every single page. If you don't understand something, ask your broker or attorney to explain it.

Mistake 2: Not Having an Attorney Review the LOI

The LOI may be "mostly non binding," but the binding provisions (exclusivity, confidentiality, break up fees) have real legal weight. Spending $1,000 to $2,000 on attorney review at the LOI stage can save you $50,000 or more down the road.

I have never seen a seller regret spending money on legal review at the LOI stage. But I have seen plenty of sellers regret skipping it. The binding provisions alone, especially exclusivity and break up fees, justify every dollar of that legal bill.

Mistake 3: Signing an LOI with No Financing Contingency Details

If the buyer is using a loan to fund the purchase, the LOI should address it. What type of financing? Have they been pre approved? What happens if the loan gets denied? Without this information, you could spend 60 days in exclusivity only to find out the buyer can't actually close.

Mistake 4: Ignoring the Exclusivity Period

I've seen sellers sign 120 day exclusivity periods without blinking. That's four months where you can't market your business or talk to other buyers. If the deal falls through on day 100, you've lost nearly half a year.

Mistake 5: Not Negotiating

The first LOI a buyer sends is their opening position. It's designed to favor them. That's not bad faith. That's how negotiations work. Sellers who accept the first draft without changes almost always leave money on the table or agree to terms they'll regret.

The first LOI is never the final deal. Sellers who treat it as a take it or leave it document almost always leave money on the table or agree to terms they will regret during due diligence.

Mistake 6: Treating the LOI as the Final Deal

The LOI is a framework, not the finished product. Terms will evolve during due diligence and purchase agreement drafting. Don't panic if things shift slightly. But do pay attention if the buyer tries to make major changes to terms you already agreed on. That's a retrade, and it's a red flag.

Want to draft a professional letter of intent for your deal? Use our free LOI generator tool to create a customized LOI in minutes.

Using an LOI Generator to Get Started

If you're on the other side of this conversation, meaning you're a buyer drafting an LOI, or a seller who wants to understand what a standard LOI looks like, we've built a free tool to help.

Our LOI generator walks you through the key terms step by step and produces a professional, customizable letter of intent. It covers purchase price, payment structure, due diligence timeline, exclusivity, non compete terms, and transition details.

Even if you don't use the output directly, it's a great way to understand what a complete LOI should include. I've seen too many LOIs that miss critical sections. Knowing what to expect helps you spot what's missing from the buyer's version.

Final Thoughts

The letter of intent is where deals are made or broken. It's not just a piece of paper you sign to move forward. It's the blueprint for your entire transaction.

Here's what I want every seller to remember:

- Read every word. Don't let excitement override diligence.

- Look beyond the headline price. Cash at closing, earnout terms, seller notes, and transition obligations all affect what you actually walk away with.

- Negotiate the binding terms hard. Exclusivity, confidentiality, and break up fees have real consequences.

- Get professional help. An experienced broker and attorney at the LOI stage will save you time, money, and stress.

- Stay organized and responsive. Once the LOI is signed, the clock starts. Being prepared for due diligence makes everything smoother.

The sellers who get the best outcomes aren't the ones who get the highest initial offer. They're the ones who understand the terms, negotiate wisely, and stay engaged through the entire process.

Have questions about an LOI you've received? Contact me directly for a free, no obligation conversation about your situation. I'll help you understand the terms and figure out the best path forward.

Related Articles

April 29, 2026

Selling a Franchise Business vs an Independent Business

Selling a franchise is a fundamentally different process than selling an independent business. Here is what every franchise owner needs to know.

April 21, 2026

What Is a Management Buyout and Is It Right for Your Business?

A management buyout lets your team buy the business. Learn how MBOs work, what they cost, and when they make sense for sellers.

April 13, 2026

How to Find the Right Business Broker for Your Industry

Not all brokers know your industry. Here's how to find one who actually understands your business and can get you top dollar.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.