Aurora Innovation has logged over 250,000 fully driverless miles hauling freight for FedEx, Schneider, and Werner Enterprises on Texas highways. No safety driver. No human behind the wheel. Just a truck, a load, and software.

If you own a trucking company and you have been thinking about selling, that sentence should change your timeline. Autonomous trucks are not a future possibility. They are hauling paid commercial freight right now, and the companies operating them plan to triple their networks by the end of 2026.

Meanwhile, trucking company owners face a brutal squeeze from three directions: insurance premiums hit a record $0.102 per mile in 2024 (up 36% since 2019), the driver shortage sits at 78,000 and is projected to hit 160,000 by 2028, and compliance costs keep climbing with new EPA emission standards adding $20,000 to $25,000 per truck starting in 2027.

The math is simple. Sell now while your company is valued as a going concern with contracted drivers and established routes. Wait, and you are selling into a market where autonomous alternatives are steadily eroding the premium buyers pay for driver dependent operations.

Autonomous Trucks Are Already on the Road

This is not science fiction and it is not a decade away. Commercial autonomous trucking crossed the threshold from testing to revenue generating operations in 2024 and 2025.

Aurora Innovation launched the first commercial driverless trucking service in April 2025 on the Dallas to Houston corridor. By October 2025, Aurora had surpassed 100,000 driverless miles with zero Aurora Driver attributed collisions. Their customer list reads like a who's who of freight: FedEx, Schneider, Werner Enterprises, Uber Freight, and Hirschbach Motor Lines. Aurora plans to deploy over 200 driverless trucks across 10 Sun Belt routes by the end of 2026, and all commercial capacity is already committed through Q3 2026.

Kodiak Robotics launched the first U.S. commercial driverless operations in December 2024, deploying autonomous trucks in West Texas for Atlas Energy Solutions. Kodiak takes a vehicle agnostic approach and aims to deploy on public roads for long haul trucking by end of 2026.

Waymo Via is leveraging the same technology that powers its consumer robotaxi service (over 14 million trips in 2025) for the freight sector. Waymo was in discussions to raise $15+ billion at a $100 to $110 billion valuation in late 2025.

The priority corridors are the Texas Triangle (Dallas, Houston, San Antonio) and the broader Sun Belt. Aurora's longest route, Fort Worth to Phoenix at roughly 1,000 miles, already exceeds Hours of Service limits, demonstrating a near 50% transit time reduction by eliminating mandatory rest breaks.

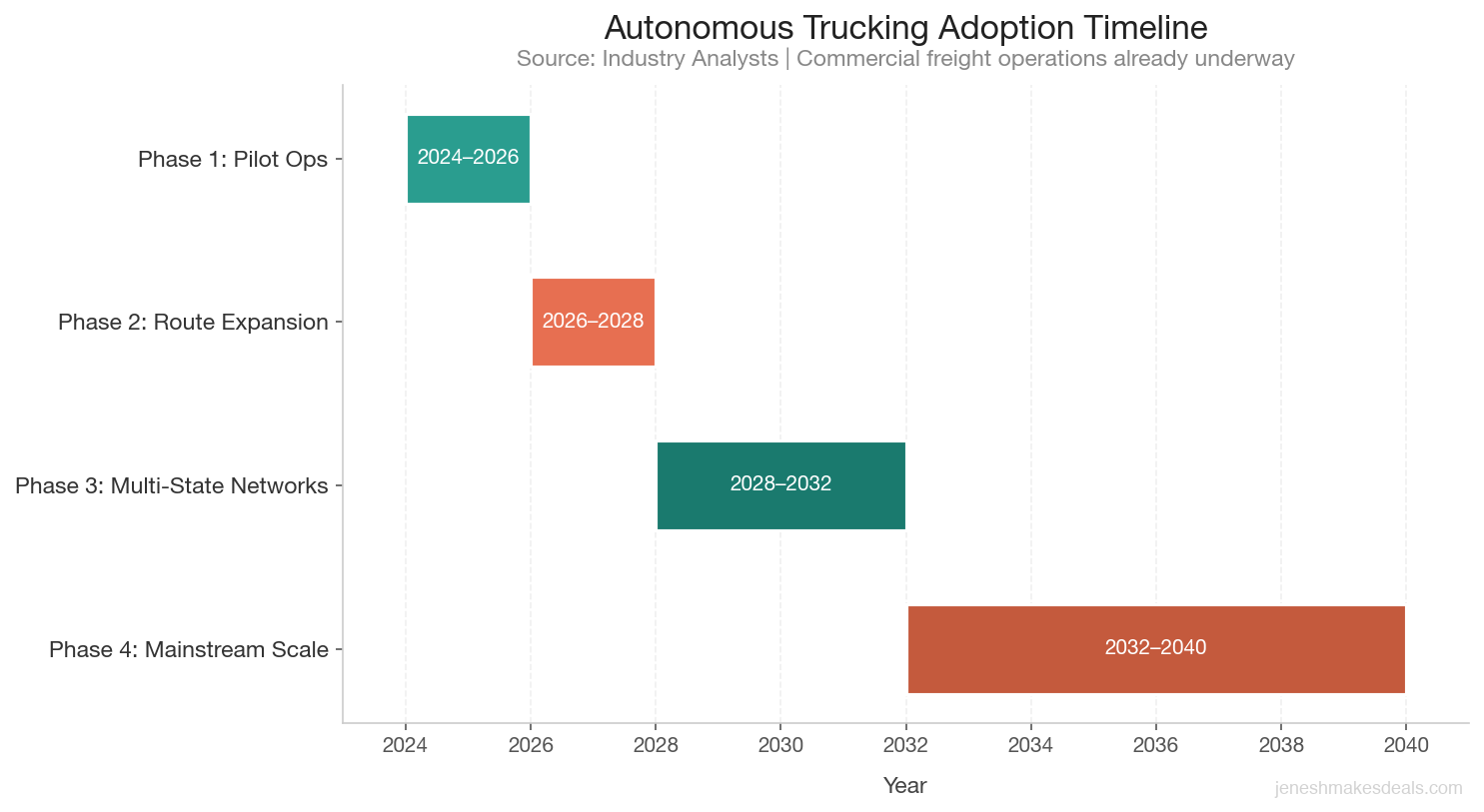

Autonomous trucking is advancing through four phases, with commercial deployments already underway in the Sun Belt. Source: Industry analysts.

Autonomous trucking is advancing through four phases, with commercial deployments already underway in the Sun Belt. Source: Industry analysts.

The Realistic Timeline for Autonomous Trucking

Industry analysts agree on a phased adoption timeline that is already underway.

| Phase | Period | What Happens |

|---|---|---|

| Phase 1: Pilot Operations | 2024 to 2026 | Corridor specific commercial services in U.S. Sun Belt, scaling from dozens to hundreds of trucks |

| Phase 2: Route Expansion | 2026 to 2028 | Additional routes, more sophisticated operations, driver as a service models |

| Phase 3: Multi State Networks | 2028 to 2032 | Major freight hub networks covering meaningful share of long haul linehaul miles |

| Phase 4: Mainstream Scale | 2032 to 2040+ | Double digit percent of new Class 8 sales, 30% by 2035 per WEF and BCG estimates |

Aurora expects to achieve revenue exceeding expenses by 2028. That is the inflection point where autonomous trucking starts meaningfully influencing traditional carrier valuations.

The optimistic scenario has autonomous trucks achieving majority status on major corridors by the late 2030s. The base case puts it in the early to mid 2040s. But here is what matters for sellers: you do not need to wait for majority status. Buyer psychology shifts long before that. Once autonomous trucks prove they can run a major corridor reliably and cheaply, every buyer starts discounting the value of driver dependent operations.

McKinsey projects autonomous trucking could reduce total cost of ownership by 42% per mile for long distance routes over 1,500 miles. That translates to $85 to $125 billion in annual savings for the U.S. trucking industry. When buyers can see that kind of cost reduction coming, they are not paying premium multiples for companies built around human drivers.

The Triple Squeeze: Insurance, Drivers, and Compliance

Even without autonomous trucks, 2026 is a difficult year to hold a trucking company. Three forces are compressing margins simultaneously.

Insurance Costs at Record Highs

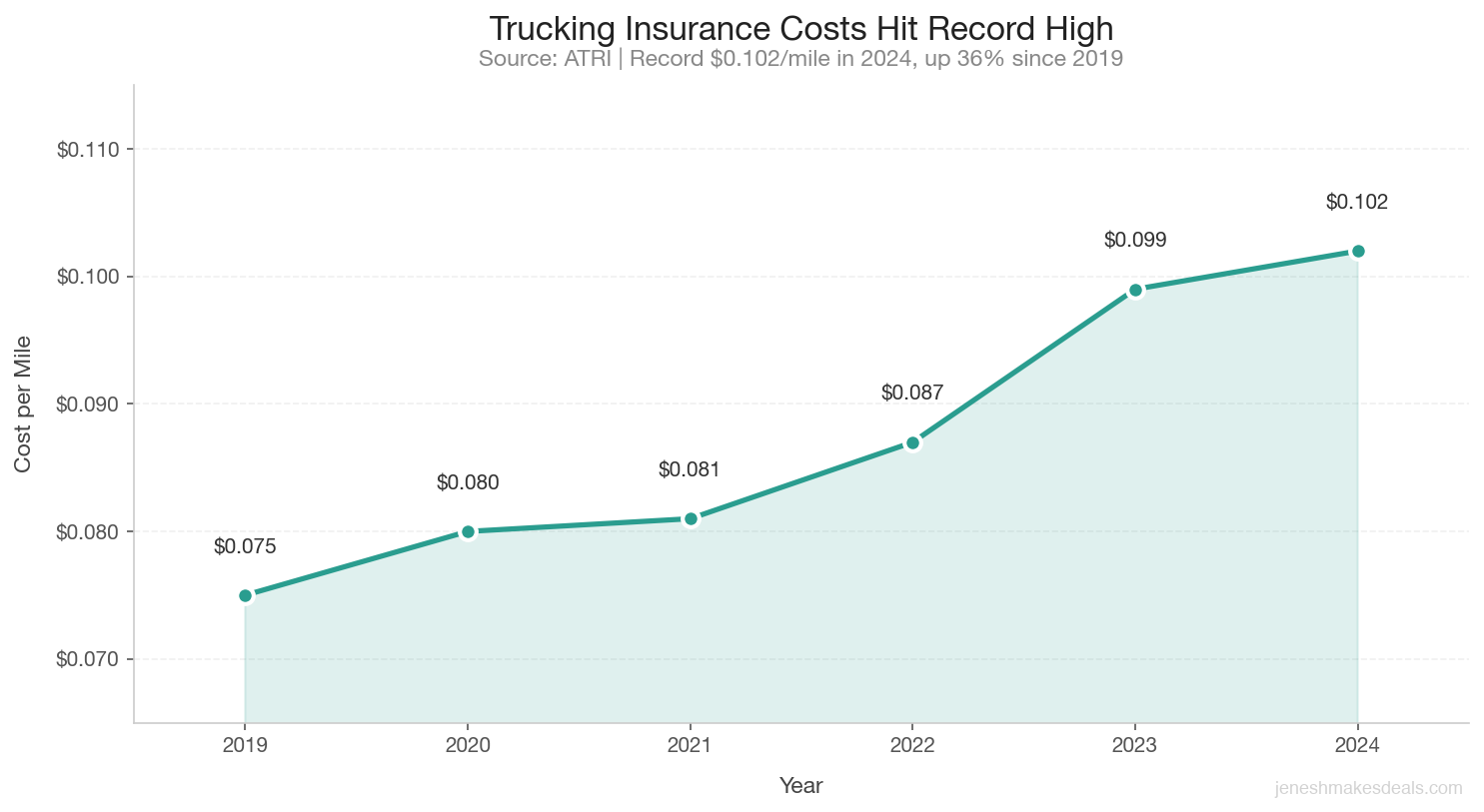

Trucking insurance premiums hit a record $0.102 per mile in 2024. Nuclear verdicts are the primary driver. Source: ATRI.

Trucking insurance premiums hit a record $0.102 per mile in 2024. Nuclear verdicts are the primary driver. Source: ATRI.

Insurance premiums hit $0.102 per mile in 2024, a record high. They rose another 5.8% in Q1 2025. Owner operators now pay $11,000 to $17,000 annually, and carriers with new authority face $14,000 to $22,000 or more. Insurance now represents roughly 10% of total operating costs.

The primary driver is nuclear verdicts. In 2024, there were 135 nuclear verdicts against corporations (up 52% from 2023), totaling $31.3 billion (up 116%). The median nuclear verdict reached $51 million, up from $21 million in 2020. The FMCSA has proposed increasing minimum liability requirements from $750,000 to $2 million, which would further squeeze smaller operators.

Renewal projections for 2025 and 2026 show no relief: auto liability up 7% to 20%, umbrella and excess up 12% to 30%, and physical damage flat to up 10%.

The Driver Shortage Is Not Getting Better

The driver shortage sits at roughly 78,000 heading into 2025, and the ATA projects it could reach 160,000 by 2028 if structural conditions do not improve. The demographics are brutal: the average truck driver is 46 to 47 years old, 31.6% of drivers are over 55, and only 6.5% are under 25 (declining 5.8% year over year). The minimum interstate driving age of 21 eliminates the immediate post high school pipeline, and most employers require 12 to 24 months of experience.

The industry needs 237,600 new drivers per year through 2034 just to keep up with retirements and growth. Globally, 3.4 million drivers across 36 countries are expected to retire by 2029.

For trucking company owners, this means every year you hold the business, your driver recruitment and retention costs go up. That directly compresses your margins and your valuation.

Compliance Costs Keep Climbing

The trucking industry faces rising costs from multiple directions while autonomous alternatives gain ground.

The trucking industry faces rising costs from multiple directions while autonomous alternatives gain ground.

The EPA's 2027 model year standards reduce allowable NOx emissions by more than 80%, adding an estimated $20,000 to $25,000 per new truck. A pre buy surge of 2026 model year trucks is already expected as fleets try to avoid higher cost 2027 compliant vehicles. Extended warranty requirements and more complex after treatment systems increase lifetime maintenance costs as well.

ELD compliance costs $300 to $1,200 per truck in the first year, with ongoing costs of $180 to $500 per year. One in four carriers received at least one ELD related violation in 2024, with average fines of $12,000. Add it all up, and the average cost of operating a truck in 2024 was $2.26 per mile, with marginal costs (excluding fuel) hitting a record $1.779 per mile.

For a typical truck running 100,000 to 120,000 miles annually, total operating costs are approximately $225,000 to $270,000. When the ATA's chief economist warns that operational costs are 26% higher than freight rates, you know the industry is in trouble. Truckload carriers operated at an average operating ratio of negative 2.3% in 2024, meaning most were losing money on operations.

Current Trucking Company Valuations

Despite the headwinds, trucking company valuations remain relatively strong in early 2026, particularly for specialized carriers. But there is a clear bifurcation forming between commodity haulers and specialized operators.

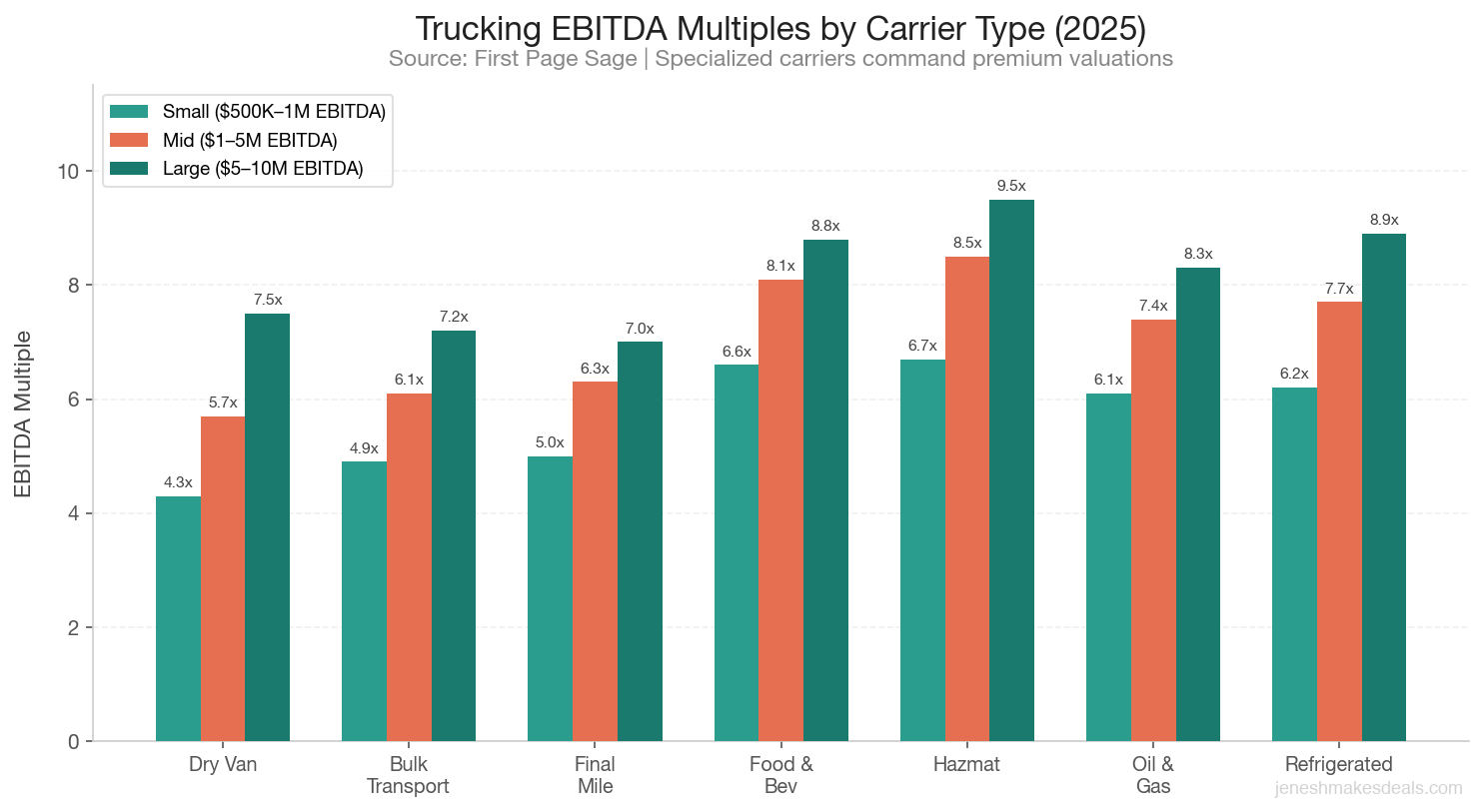

Specialized carriers command significantly higher multiples than commodity haulers. The gap is widening. Source: First Page Sage, Q1 2025.

Specialized carriers command significantly higher multiples than commodity haulers. The gap is widening. Source: First Page Sage, Q1 2025.

EBITDA Multiples by Carrier Type

| Carrier Type | Small ($500K to $1M EBITDA) | Mid ($1M to $5M EBITDA) | Large ($5M to $10M EBITDA) |

|---|---|---|---|

| Dry Van (Long Haul) | 4.3x | 5.7x | 7.5x |

| Bulk Transport | 4.9x | 6.1x | 7.2x |

| Final Mile | 5.0x | 6.3x | 7.0x |

| Refrigerated | 6.2x | 7.7x | 8.9x |

| Hazardous Materials | 6.7x | 8.5x | 9.5x |

| Food and Beverage | 6.6x | 8.1x | 8.8x |

| Oil and Gas | 6.1x | 7.4x | 8.3x |

For smaller, owner operated businesses valued on SDE, multiples range from 2.44x to 3.45x. Short haul small carriers trade at 3x to 5x adjusted EBITDA.

The key takeaway: specialized carriers (hazmat, refrigerated, food grade) command 40% to 70% higher multiples than commodity long haul carriers. This gap is expected to widen as autonomous trucks target the simplest freight first, which is point to point dry van long haul.

Wondering what your trucking company might be worth? Get a free confidential valuation to see where you stand in today's market.

What Autonomous Trucking Does to Your Company's Value Over Time

The near term (2025 to 2028) impact on traditional trucking valuations is minimal. Autonomous trucks represent a tiny fraction of total miles. But the meaningful valuation pressure begins in the early 2030s as autonomous fleets scale to cover significant corridor miles.

Here is what happens to different types of trucking companies:

Most vulnerable: Long haul truckload carriers dependent on human drivers for simple point to point hauls. Their current 4.3x to 7.5x EBITDA multiples could compress significantly as autonomous alternatives scale on the exact corridors they operate.

Moderately at risk: Regional carriers that operate on major highway corridors in the Sun Belt, where AV deployment is leading. These companies have more route complexity than pure long haul but still face competition from autonomous alternatives.

More insulated: Specialized carriers (hazmat, refrigerated, food grade) face less near term disruption due to complex loading and unloading requirements, specialized regulatory needs, and last mile complexity that autonomous technology is not yet designed to handle.

Least at risk: Last mile and urban delivery carriers. Current AV technology is focused on highway hub to hub operations, not navigating city streets, docking bays, or customer deliveries.

The global autonomous trucking technology market is projected at $400 to $600 billion by 2035. The North American market alone is expected to reach $65.4 billion within a decade. When that kind of capital flows into replacing what your company does, it is time to exit.

Which Trucking Segments Are Buyers Still Paying Premium For

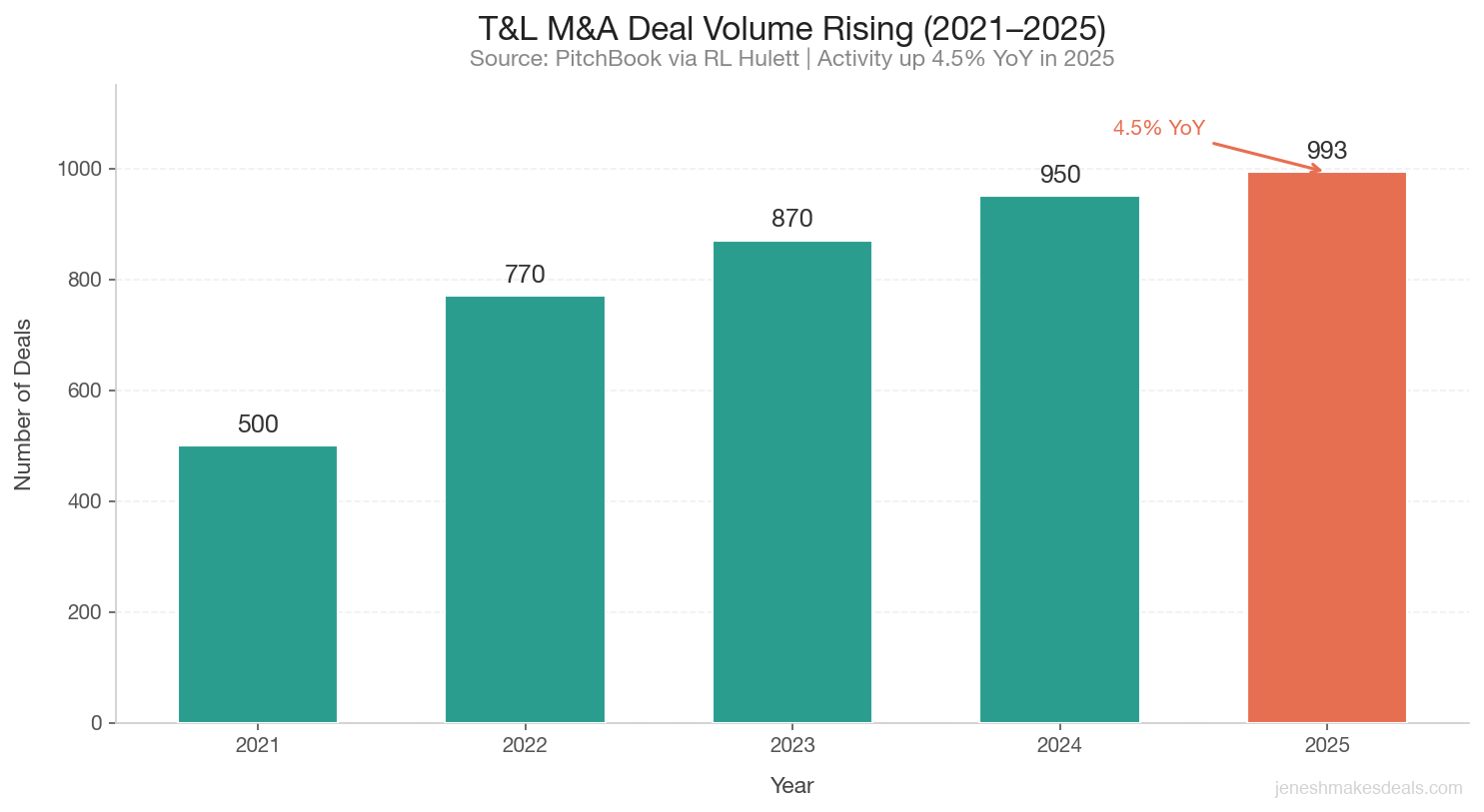

Private equity represented 38.7% of transportation and logistics deal volume in 2025, up from 37.2% in 2024. Deal volume is increasing, with PitchBook reporting 993 deals in 2025 (up 4.5% from 2024), and recovery is expected to continue through Q4 2026 and into 2027.

T&L deal activity continues to grow, with PwC expecting further increases in 2026 as interest rates drop. Source: PitchBook via RL Hulett.

T&L deal activity continues to grow, with PwC expecting further increases in 2026 as interest rates drop. Source: PitchBook via RL Hulett.

But PE firms are being selective about what they buy. According to Lincoln International and Tenney Group's 2026 outlook, here is where the money is going:

What PE is buying:

- Specialty logistics providers and niche carriers

- Technology enabled models and aggregator platforms

- Low risk, high margin companies with add on acquisition potential

- Carriers with specialized fleets and adjacent service offerings

- Contracted, recurring revenue businesses

What PE is avoiding:

- Pure spot truckload businesses

- Generic freight brokerages

- Standalone freight technology platforms without proprietary data

- Commodity long haul carriers with no differentiation

Notable recent transactions include Werner Enterprises acquiring FirstFleet for $245 million, Enterprise Mobility acquiring Hogan Transportation Companies, and Stonepeak Partners acquiring SeaCo for $1.75 billion.

Thinking about your exit options? Contact us for a confidential conversation about how your trucking company compares to what buyers are actively looking for.

The Freight Rate Problem

The trucking industry has endured a prolonged freight recession from 2023 through mid 2025. Current spot rates paint a tough picture: dry van at $1.63 per mile, reefer at $1.92 per mile, and flatbed at $2.18 per mile.

For 2026, forecasts vary depending on trade policy:

| Scenario | Rate Outlook |

|---|---|

| Base case (mild growth) | 2% to 4% freight rate increases |

| Trade policy improves | 4% to 7% growth, led by long haul and reefer |

| Trade policy stays volatile | Rates flat to negative, capacity continues exiting |

The ATA's chief economist warned in February 2026 that operational costs are 26% higher than freight rates. That is not sustainable. Only LTL maintained healthy profitability at 11.6% operating ratio. Truckload carriers were losing money.

When you combine thin or negative margins with rising insurance, driver costs, compliance costs, and the approaching autonomous truck competition, the case for selling becomes clear. You are not selling at the bottom. You are selling before the structural shift hits.

How 95% of Carriers Are Small Fleets (And Why That Matters)

There are approximately 1.86 million companies operating trucks in the U.S., with about 580,000 active motor carriers registered with FMCSA. The fleet size distribution tells an important story:

| Fleet Size | Number of Operators | Percentage |

|---|---|---|

| Single truck | 1,156,728 | 60.5% |

| Small fleet (2 to 10 trucks) | 668,962 | 35.0% |

| Medium fleet (11 to 50 trucks) | 71,383 | 3.7% |

| Large fleet (50+ trucks) | 14,292 | 0.7% |

95.5% of carriers operate 10 or fewer trucks. About 70% are one or two truck operations. And small fleets are already shrinking: roughly 1,500 small carriers exit the market every month, a correction from the 2020 to 2022 boom when high spot rates drew thousands of unprepared operators into the market.

If you are a small to midsize fleet owner, this matters because McKinsey anticipates "some industry consolidation" as smaller fleets struggle to finance the capital expenditures required for autonomous truck infrastructure. The companies that survive the transition will be the ones with the capital to invest. If you do not plan to be one of them, selling now gets you maximum value for what you have built.

Want to see how your business valuation compares to industry benchmarks? Check out our 2026 business valuation multiples by industry for the latest data.

How to Position Your Trucking Company for Maximum Value

If you have decided to sell, here is how to position your company to attract top dollar from today's buyers. These strategies apply across industries, but I have tailored them specifically for trucking. For a broader look, see our guide on maximizing your business value before selling.

Emphasize Specialization

Specialized carriers (hazmat, temperature controlled, food grade) earn 40% to 70% higher multiples than commodity haulers. If you have any specialized capabilities, make sure they are front and center in your financials and marketing materials. Highlight the certifications, training, equipment, and customer relationships that commodity carriers cannot replicate.

Lock in Contracted Revenue

Buyers pay more for predictable revenue. If you are running a mix of spot and contract freight, work to shift the balance toward contracted revenue before going to market. Multi year contracts with creditworthy shippers are gold to PE buyers.

Clean Up Your Safety Record

A clean safety record is table stakes for premium valuations. Invest in driver training, camera systems, and compliance monitoring. Every accident on your record reduces your multiple and increases the risk premium buyers apply.

Modernize Your Fleet

Buyers discount companies with aging equipment because they see deferred capital expenditure. If your fleet average age is high, consider strategic replacement of the oldest units. This does not mean buying a whole new fleet, but addressing the worst units shows buyers you have been reinvesting.

Reduce Owner Dependency

If the business cannot run without you in the cab or on the phone every day, buyers see risk. Build out your dispatcher team, driver management processes, and customer relationships so the company operates without you being the center of every decision.

Common Mistakes Trucking Company Owners Make When Selling

Waiting for rates to recover. Many owners tell themselves they will sell "when freight rates come back." But rates may never return to 2021 to 2022 levels, and every year you wait, autonomous trucks gain more ground.

Ignoring the autonomous truck timeline. Some owners dismiss AV as "always five years away." It is not. Aurora is hauling commercial freight today, and their capacity is booked through Q3 2026. The timeline is real.

Not preparing financials. Buyers want 3 years of clean financials with proper add backs. If your books are a mess, you are leaving money on the table or killing deals entirely.

Overvaluing equipment. Your trucks and trailers have book value, but buyers are buying cash flow, not iron. An aging fleet with strong contracts and great drivers is worth more than a new fleet running spot loads.

Trying to sell without help. Trucking M&A has unique complexities around operating authority, safety ratings, equipment liens, and customer contract transferability. A broker who understands the industry will get you a higher price and a smoother close. Not sure what a broker costs? Here is a full breakdown of how much business brokers charge.

What to Do Next

The autonomous trucking transition is not going to reverse. Insurance costs are not going to drop. The driver shortage is not going to fix itself. And compliance costs are only going in one direction. If you have built a trucking company that has value today, the smartest move is to capture that value while the market still pays a premium for what you have.

Here is what I recommend:

- Get a professional valuation. Understand what your company is worth in today's market, not what you think it is worth or what your neighbor's company sold for three years ago. Our guide on how to value a business walks through the three proven methods.

- Clean up your financials. Get 3 years of tax returns and financial statements organized with proper add backs calculated.

- Identify your strengths. What makes your company attractive to buyers? Specialization, contracts, driver retention, geography, safety record? Lead with those.

- Talk to a broker who knows trucking. Not every business broker understands the nuances of trucking M&A. Find one who does.

Ready to find out what your trucking company is worth? Get a free confidential valuation and I will walk you through your options. No pressure, no obligation.

Need capital to strengthen your business before selling? Explore our unsecured funding programs that can provide up to $500,000 with no collateral required.

Sources

- Aurora Innovation. "Aurora Triples Driverless Network to 10 Routes." Aurora IR, January 2026.

- Telemetry Agency. "Waymo Dominates as Autonomous Driving Reaches Commercial Tipping Point." 2025.

- Fifth Level Consulting. "Top 5 Autonomous Trucking Companies in the US." 2025.

- GM Insights. "Autonomous Long Haul Trucking Market Size, 2025 to 2034 Report." 2025.

- Breakbulk News. "Autonomous Trucking Developers Accelerate Commercial Launches." 2026.

- First Page Sage. "Trucking Company EBITDA and Valuation Multiples, 2025 Report." Q1 2025.

- Peak Business Valuation. "Freight Trucking Company Valuation Multiples." 2025.

- ATRI. "2025 Operational Costs of Trucking Analysis." 2025.

- AtoB. "Owner Operator Truck Insurance Cost Statistics for 2026." 2026.

- Trucking Dive. "How Trucking Costs Are Changing, in 4 Charts." 2025.

- ATA. "Updated Driver Shortage Report and Forecast." 2025.

- IRU. "Widening Age Chasm Compounds Truck Driver Shortage Crisis." 2025.

- RL Hulett. "Transportation and Logistics M&A Update Q4 2025." January 2026.

- Lincoln International. "Transportation and Logistics M&A in 2025 and Why 2026 Matters More." 2026.

- Tenney Group. "2026 M&A Report: Policy Volatility Slowed 2025 Transportation M&A Activity." 2026.

- McKinsey. "Will Autonomy Usher in the Future of Truck Freight Transportation?" 2025.

- CLA Connect. "Transportation, Logistics Transitions: Private Equity's Role." 2025.

- FreightWaves. "ATRI Report: Rising Costs Continue to Squeeze Trucking Industry." 2025.

- Heavy Duty Journal. "Autonomous Trucking Investment: Complete Fleet Guide." 2025.

- Traffic Safety Store. "When Will Driverless Trucks Rule the Highways?" 2025.

Frequently Asked Questions

How much is my trucking company worth in 2026?

Trucking company valuations depend on size, type, and specialization. Owner operators typically see SDE multiples of 2.44x to 3.45x. Small to midsize fleets ($1M to $5M EBITDA) trade at 5.5x to 8.5x EBITDA depending on carrier type. Specialized carriers like hazmat and refrigerated command the highest multiples (up to 9.5x), while commodity dry van long haul carriers trade lower at 4.3x to 7.5x. Get a free valuation to see where your company falls.

Will autonomous trucks really replace trucking jobs?

Not all of them, and not overnight. Autonomous trucks are targeting long haul highway corridors first, with commercial operations already running in Texas. The realistic timeline puts multi state networks in the 2028 to 2032 range and mainstream scale by 2032 to 2040. Last mile, urban delivery, and specialized carriers (hazmat, refrigerated) face much less near term disruption.

Is 2026 a good time to sell a trucking company?

Yes. Despite the freight recession, valuations for specialized and well run carriers remain strong. PE deal volume in transportation and logistics increased 4.5% in 2025, and analysts expect recovery to continue through 2026 and 2027. Selling now means capturing value before autonomous trucks put downward pressure on long haul carrier multiples and before insurance and compliance costs further erode margins.

What do buyers look for when buying a trucking company?

Buyers prioritize contracted recurring revenue over spot market dependence, specialized capabilities (hazmat, temperature controlled, food grade), clean safety records, modern fleet equipment, strong driver retention, and minimal owner dependency. PE firms specifically target technology enabled models and low risk, high margin companies with add on acquisition potential.

How long does it take to sell a trucking company?

The typical trucking company sale takes 6 to 12 months from listing to close. Companies with clean financials, transferable operating authority, clear equipment titles, and strong customer contracts tend to sell faster. Specialized carriers attract more buyer interest than commodity haulers, which can also speed up the process.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.