I've walked hundreds of buyers through acquisitions. Some went smoothly. Most hit problems that could have been caught earlier. The difference between a deal that works and one that destroys your savings isn't luck. It's seeing the red flags before you sign.

This post covers the warning signs I've watched derail good buyers, the questions most people don't think to ask, and how to tell whether a problem is a dealbreaker or just something to renegotiate.

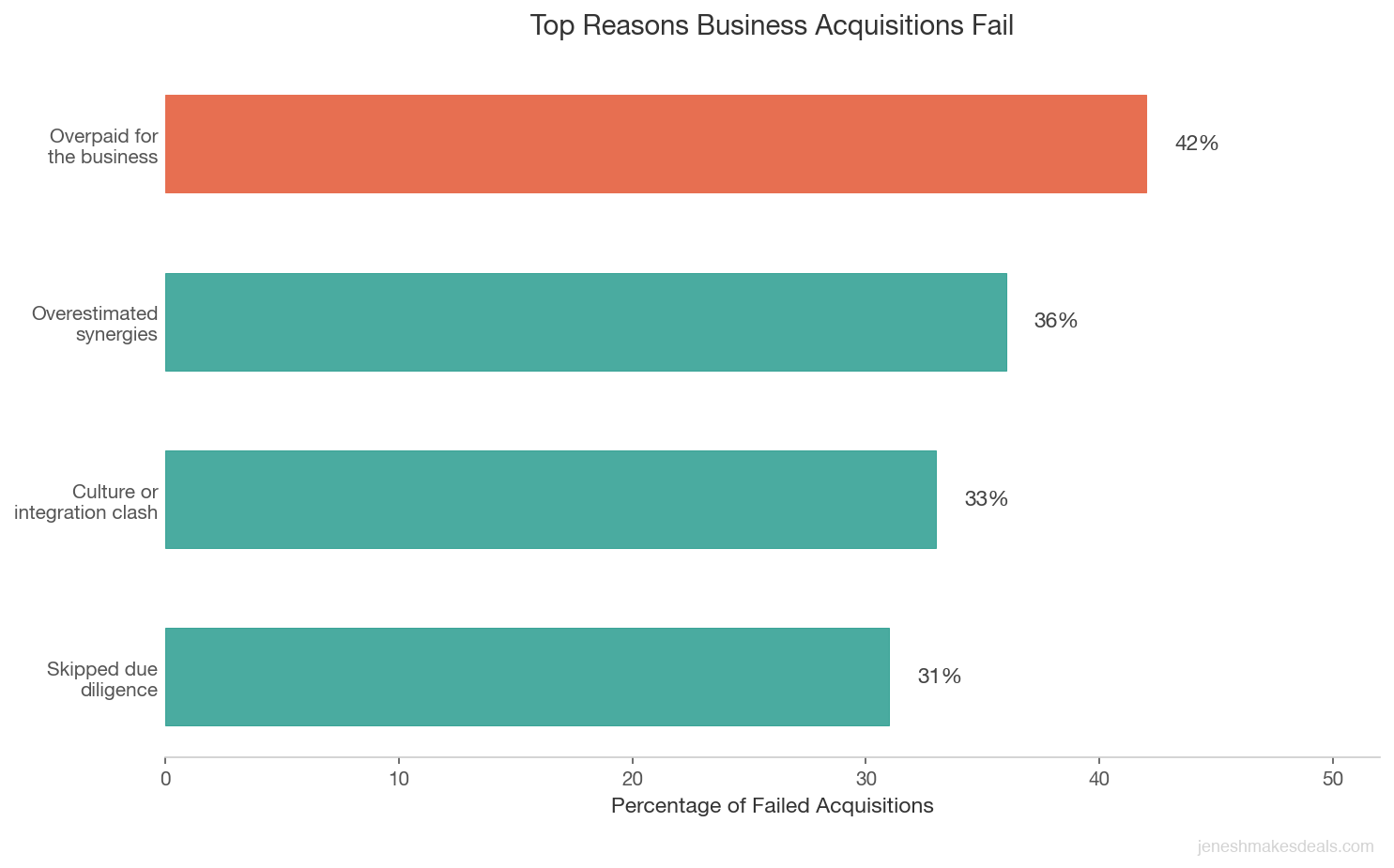

Most Acquisitions Fail. Here's Why Yours Doesn't Have To.

The numbers are brutal. About 70 percent of acquisitions fail to meet their stated objectives. Almost 46 percent of S&P 500 M&A deals are eventually undone entirely. For smaller businesses, the picture is worse. Nearly 50 percent of all deals fall apart before closing.

Why? Most failures come down to two things: buyers overpay (42 percent of cases) or they skip proper due diligence (31 percent of cases). The buyers who succeed aren't smarter. They're more paranoid. They ask harder questions. They verify everything the seller tells them.

Here's what separates successful acquisitions from disasters: buyers who understand that sellers have incentives to present rosy pictures. That's not necessarily dishonest. It's human. When someone has built a business over a decade, they see the best in it. They've rationalized the problems. They downplay the risks because they've lived with them so long they seem normal.

Your job is to see what they can't. That means knowing which flags matter and which ones you can fix with the right price adjustment or working capital escrow.

Financial Red Flags That Should Stop You Cold

Let's start with the balance sheet. Most sellers will hand you financial statements that are, well, optimistic.

Watch for revenue that doesn't reconcile. Add up the monthly deposits in the bank statements and compare them to the revenue on the tax return. They should match closely (within 2-3 percent). If they don't, ask why. Maybe there are refunds, chargebacks, or revenue from other sources. But a gap of 10 percent or more? That's a problem.

I worked with a buyer who was about to close on a cleaning service doing $1.2 million in annual revenue. When we pulled the actual bank deposits, the real number was closer to $980,000. The seller had been using estimates and accrual accounting to paint a rosier picture. We renegotiated the price down by $80,000 based on that gap alone.

Declining revenue is the single biggest killer. If the business made $500,000 last year and $450,000 this year, that's a 10 percent drop. Sellers will tell you it's seasonal or tied to a single client leaving or COVID or the economy. Maybe that's true. But a declining trend means you're not buying a growing asset. You're buying a shrinking one.

Look at the last three years of tax returns side by side. Not adjusted EBITDA (sellers love to manipulate that). Actual revenue, actual expenses, actual profit. If the trend points down, the default assumption should be that it continues down unless you have very specific reasons to believe otherwise.

EBITDA manipulation is everywhere. The seller hands you an "adjusted EBITDA" that's 40 percent higher than their net income on the tax return. They're adding back the owner's salary, the owner's car, their spouse's "consulting fees," and a dozen other expenses that they claim are one-time or personal.

Some of that is legitimate. If the owner was paying themselves $200,000 and you can hire someone to do the job for $100,000, that's a real saving. But be skeptical. Ask for a detailed breakdown of every adjustment. Push back on anything vague.

I've seen sellers add back "excess rental payments" to the building (their brother owns it), "excess compensation" (they overpaid themselves for years), and "one-time items" that somehow appear every year. Those adjustments matter because that's what determines the purchase price. Get a quality of earnings report done before you trust any EBITDA numbers.

Unreconciled accounts are a huge warning sign. If the accounts receivable don't match the aging report. If the inventory count doesn't match the books. If the accounts payable have balances from vendors the business hasn't used in two years. These gaps almost always hide liabilities.

One buyer I worked with bought a manufacturing business that had $150,000 in accounts payable that nobody understood. Turned out the seller had disputed a large invoice three years earlier and just never resolved it. After the purchase, the vendor came after the new owner. That $150,000 suddenly became the buyer's problem.

Pull detailed aging reports for A/R and A/P. Reconcile the physical inventory to the books. Ask about any balances older than 90 days. These conversations take time, but they save you hundreds of thousands of dollars.

| Financial Red Flag | What to Check | Severity |

|---|---|---|

| Revenue doesn't match bank deposits | Compare monthly deposits to reported revenue on tax returns | High |

| Declining revenue over 2+ years | Review three years of tax returns side by side | High |

| Adjusted EBITDA far exceeds net income | Request itemized breakdown of every add back | Medium to High |

| Unreconciled accounts receivable | Match aging report to general ledger balances | Medium |

| Accounts payable with old balances | Investigate any payables older than 90 days | Medium |

| Inventory count doesn't match books | Conduct physical count and compare to financial records | Medium |

Broker insight: The seller's adjusted EBITDA is a sales pitch, not a financial statement. Always rebuild the numbers yourself from bank deposits and tax returns before you trust any valuation. The gap between what sellers present and what the source documents show is where the real price of the business lives.

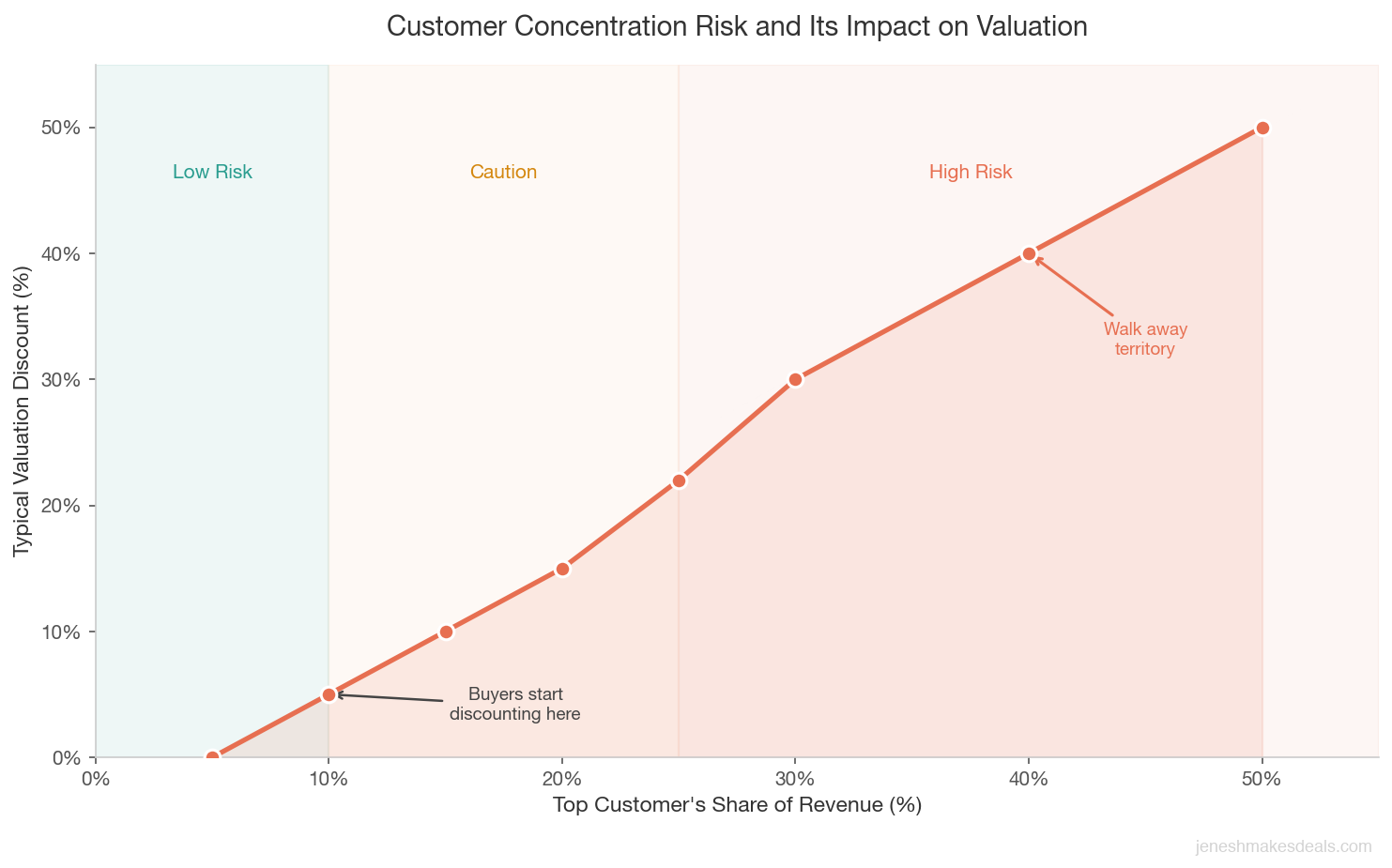

Customer Concentration: The Silent Deal Killer

Here's a rule: if one customer represents more than 10 percent of revenue, you have a problem. Not maybe. Definitely.

Think about it. You're buying a business for $2 million that does $1 million in revenue. That multiple assumes the revenue is stable. But if 15 percent ($150,000) comes from a single customer and that customer leaves, your business just lost 15 percent of its value overnight.

The top five customers should represent no more than 25 percent of revenue. If they do, the risk is too high. You're not really buying a business. You're buying a relationship with a few companies.

Worse, what happens when you take over? That big customer might have a personal relationship with the current owner. Maybe the owner's brother-in-law works there. Maybe the decision maker loves the founder. When the ownership changes, loyalty changes. I've seen companies lose their largest client within 90 days of acquisition, and suddenly a deal that looked solid is underwater.

Ask to see the contracts with the top 10 customers. Do they have renewal dates? Are there price locks? Can the customer terminate without cause? Many commercial relationships run month-to-month with either party able to walk away.

Here's another angle: what happens if your largest customer demands a price cut? That's a common play after acquisition. The buyer has already committed capital. They want the deal to work. The customer knows it. Suddenly that big account becomes a negotiating chip, and you're forced to accept lower margins.

Customer concentration also affects your ability to raise capital or get a loan against the business. Most lenders will value concentrated revenue at a huge discount or not at all. That manufacturing business with three customers representing 80 percent of revenue? It's worth maybe half what a diversified customer base would be.

Before you make an offer, map out the top 20 customers by revenue. Understand the contract terms. Call a few of them (with the seller's permission) and ask if they plan to stay once ownership changes. If the top five customers represent more than 25 percent of revenue, either negotiate the price way down or walk away.

Key takeaway: Customer concentration isn't just a risk factor. It's a valuation factor. A business where no single customer exceeds 5% of revenue is worth meaningfully more than one where a handful of accounts drive the majority of sales. Price accordingly or walk away.

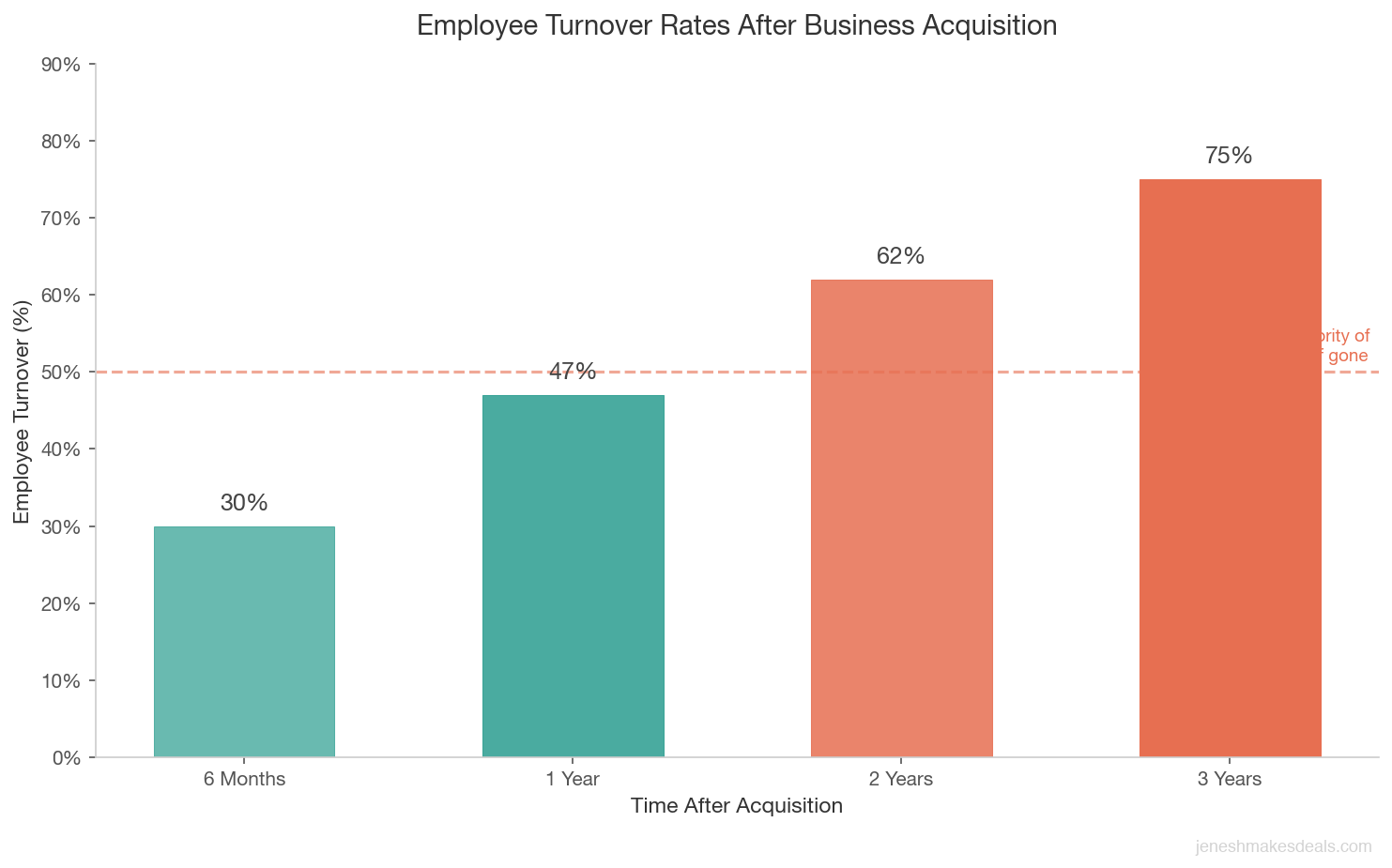

Key Person Dependency and Employee Risk

About 71 percent of small businesses depend on one or two key individuals to run. When you buy that business, those people become your biggest problem.

Why? Because employees leave. A lot. Studies show 47 percent of acquired employees leave within the first year. That number climbs to 75 percent by year three. If those employees are the ones running the business, you just inherited massive disruption risk.

This is especially true if the business owner is the key person. Maybe they're the only one who knows how to service clients. Maybe they have the relationships. Maybe they're the face of the company. When they stay as an owner or consultant for a year or two post-acquisition, that works. But it's temporary. Eventually they want to go fishing. Or they move. Or they decide they don't like the new owner. Then you're stuck.

I worked with a buyer who acquired a consulting firm for $3 million. The founder agreed to stay for two years. Twelve months in, he got bored and went back to his old job at a competing firm. Suddenly the buyer had a firm with no consultants (they'd left with the founder), angry clients, and zero revenue. The non-compete couldn't prevent what happened because the founder's consulting wasn't the same business.

Here's what you need to know: How many people are absolutely critical to the business? For each one, ask the seller how long they've been there, what their salary is, whether they've received offers from competitors, and whether they want to stay post-acquisition.

Then hire a recruiter to get a replacement cost. If you have three key people and replacing each one costs 100-200 percent of their annual salary (recruiting, training, lost productivity), factor that into your offer. If it's a $2 million business and key person dependency puts you at $400,000 in replacement risk, that's not a small thing.

Also check whether the business has documented processes. If everything lives in one person's head, you have a problem bigger than just turnover. You have a business that doesn't scale. You're buying a job, not a system.

The other angle is non-competes. Ask to see the employment agreements with key people. Do they have non-competes? Are they enforceable? In 2025 and 2026, the FTC has been cracking down on non-competes, making them harder to enforce in some states. A non-compete that was airtight five years ago might not hold up now.

Seller Behavior That Should Make You Nervous

Sometimes the red flag is the seller themselves.

Sellers who won't provide documents. If the owner says "I don't keep detailed records" or "Most of this is handshake deals" or "You don't need to see the customer contracts," that's a massive red flag. Honest sellers are proud to show you everything. They want you to feel confident.

Sellers who hide documents are hiding problems. Maybe they're not technically breaking the law. But they know you won't like what you find. So they make it hard to find.

I worked with a buyer on a construction company once. The seller said customer contracts were "all over the place" and didn't want to compile them. We pushed anyway. Turns out the company had a major contract with a government agency that required certain certifications. The seller had let those certifications lapse. The contract was about to be terminated. That's why the seller didn't want us to see the contracts.

Unrealistic valuations. If the seller is asking for a valuation that's way above market, they either don't understand what they own or they're testing you. Either way, be skeptical.

I get asked often what multiples look like. For service businesses, it's typically 1.5x to 3x revenue or 4x to 8x EBITDA, depending on growth, consistency, and margins. For product businesses, it's 2x to 4x revenue or 6x to 12x EBITDA. If a seller is asking for 6x revenue on a declining, service based business, they're not being realistic about what they own.

Sellers in a hurry. People sell businesses for good reasons and bad reasons. Bad reasons include financial distress, health problems, or problems they want to escape. If the seller is rushing to close, ask why. Maybe they have a medical issue. Maybe they got a job offer. Maybe they're running out of cash.

Any of those reasons should make you slow down, not speed up. A seller with a gun to their head is a seller who might agree to something they can't deliver or who's hiding problems they hope you won't find before closing.

Warning: When a seller refuses to share documents, rushes timelines, or gets hostile about basic questions, that tells you more about the deal than any financial statement will. The way a seller behaves during due diligence is a direct preview of how honest the numbers are.

Aggressive accounting. Look at the tax returns carefully. Are they filing the same return year to year, or are numbers changing retrospectively? Are they using aggressive depreciation schedules or unusual expense categories?

I'm not saying sellers are criminals. But I am saying that businesses on the edge of profitability sometimes use aggressive accounting to appear more profitable. That works for banks and investors. But if you buy the business and the IRS decides those accounting practices were too aggressive, you inherit the problem.

Lease, Legal, and Environmental Land Mines

Most buyers focus on the business assets and ignore the lease. That's a mistake.

The lease is everything. If you're buying a retail business or a restaurant or anything location dependent, the lease is half the value. A great location with a terrible lease is not a great location. And a great lease is non-transferable.

When you buy a business, you don't automatically have the right to keep the premises. The landlord can recapture the space. They can deny the transfer. They can require you to sign a new lease at new market rates. If the seller had a sweetheart deal ten years ago and the landlord decides to triple the rent, suddenly your acquisition economics don't work.

Before you make an offer, get a copy of the lease. Have your attorney review it. Make absolutely sure you understand the terms, the renewal options, the assignment restrictions, and what happens if the landlord decides not to let you stay.

One buyer I worked with was acquiring a laundromat for $800,000. The lease looked fine until we realized it had only six months left and the landlord had already said they were doubling the rent. The buyer's return on investment dropped from 25 percent to 8 percent. He walked away.

Environmental liability is strict. If the property has ever been used for manufacturing, dry cleaning, auto repair, or any industrial use, you could inherit massive environmental cleanup costs. And here's the kicker: you're liable regardless of who caused the contamination.

CERCLA (Comprehensive Environmental Response Compensation and Liability Act) holds the current property owner strictly liable for environmental cleanup. Even if you had nothing to do with causing the contamination, you own the problem now.

Get an Phase I environmental assessment done on any property-dependent business. It costs $2,000-$5,000 and could save you hundreds of thousands of dollars.

Existing lawsuits and liens. Ask the seller directly: Are there any pending lawsuits? Any liens on the business or property? Any customer complaints or regulatory issues? Get a UCC search done to see if anyone has a claim against the business assets.

One buyer I know thought he was buying a clean plumbing business for $500,000. Turned out the previous owner had left without paying a supplier. The supplier had a lien against the business equipment. The buyer had to pay off that lien before he could actually own the equipment.

Regulatory compliance. If the business requires licenses, permits, or regulatory approval, verify that everything is current. Health permits. Business licenses. Professional certifications. Industry-specific compliance. If any of these lapse, you might not be able to operate the business legally.

For some industries, regulators have to approve ownership changes. You might not actually be able to take over immediately, or regulators might impose new conditions.

What a Quality of Earnings Report Actually Tells You

Here's a report that separates smart buyers from everyone else: the Quality of Earnings (QoE) report. It costs $10,000 to $30,000 but commonly finds problems that save you hundreds of thousands.

A QoE report has accountants rebuild the financial statements from scratch based on bank records, tax returns, and source documents. They're looking for revenue recognition errors, unrecorded liabilities, aggressive accounting, and unreconciled balances.

What do they find? Almost always something.

Wrong period revenue. Seller records $500,000 in sales in December, but the customer didn't pay until February. Or they record refunds in the wrong year. When you rebuild the statements based on actual cash, the numbers shift.

Unrecorded liabilities. A supplier invoice that was logged but not paid. A payroll liability. A tax penalty. These show up when you trace every dollar.

Aggressive expense allocation. The seller allocated 30 percent of their mortgage payment to the business because they used their home office. Or they capitalized a repair that should have been expensed. When the QoE people rebuild, these adjustments change profitability.

Unreconciled data. Bank deposits don't match invoiced sales. Expense reports don't have receipts. Inventory counts are different from the books.

I always recommend a QoE report on any acquisition over $1 million. For anything smaller, at least have your accountant rebuild the last two years of financials from source documents. It's not glamorous work. But it's the work that protects you.

When to Walk Away vs. When to Renegotiate

Red flags don't automatically mean you should walk. Sometimes the flag just means you need a price adjustment.

Walk away if: The business has declining revenue with no credible explanation for why that trend reverses. A customer concentration risk you can't mitigate. Key person dependency without documented processes. Environmental liability. Seller dishonesty. Material non-compliance with regulatory requirements.

Those problems don't get better after you own the business. They get worse. You're adding your capital and your time to a business that had problems the previous owner couldn't fix.

Renegotiate if: There's a lease issue but you can get the landlord to agree to new terms. Employee turnover risk that you can mitigate with retention bonuses. One-time adjustments to EBITDA that are reasonable. A customer loss that was specific to the previous owner's relationship.

| Red Flag | Walk Away | Renegotiate |

|---|---|---|

| Revenue declining 2+ consecutive years with no clear cause | Yes | No |

| Single customer over 25% of revenue | Yes | No |

| Key person dependency, no documented processes | Yes | No |

| Environmental contamination liability | Yes | No |

| Lease expiring soon but landlord willing to renew | No | Yes, adjust price for new lease terms |

| Key employee flight risk | No | Yes, budget for retention bonuses |

| One time EBITDA adjustments that are verifiable | No | Yes, recalculate valuation |

| Lost customer tied to previous owner's personal relationship | No | Yes, discount by lost revenue amount |

For renegotiation items, drop your offer. If you were offering $2 million and you uncover a $150,000 problem, your offer becomes $1.85 million. Or you ask for that amount held in escrow. Or you ask the seller to stay on as an employee at a specific salary to manage customer relationships.

The goal isn't to beat down the seller. It's to make sure the economics still work for you after you account for the risk you've discovered.

Common Mistakes Buyers Make During Due Diligence

Let me tell you the mistakes I see most often.

Only looking at the seller's numbers. Always verify with independent sources. Bank records. Tax returns. Customer references. Contract agreements. The seller isn't lying, necessarily. But they're presenting information in a way that makes the business look good. That's their job.

Skipping customer calls. Contact the top 10 customers yourself. Not the ones the seller introduces you to. Find the actual decision maker and ask if they plan to stay after the acquisition. You'll be surprised how honest customers are about the relationship.

Not getting an accountant involved early. Some buyers try to save money by skipping the accountant until closing. Wrong move. Get your CPA involved in the initial offer stage. They'll ask questions you don't think of.

Assuming the business can grow revenue. Buyers often buy a business doing $1 million in revenue and assume they can grow it to $1.5 million. Maybe. But that growth might require capital investments, process changes, or key person effort that weren't part of the plan. Don't assume growth. Plan on flat or declining revenue and be pleasantly surprised if it grows.

Not understanding the industry. Talk to other operators in the same industry. Ask them about the trends, the customer dynamics, the regulatory landscape. What looks like an opportunity to you might be a sunset industry to someone who's been in the space for 20 years.

Underestimating transition costs. You're going to need to hire people. Train them. Update systems. Replace equipment that's about to fail. Buyers often underestimate these costs by 30-50 percent. Build in a buffer.

What To Do Next

If you're seriously considering buying a business, here's the order of operations:

First, run the numbers yourself. Don't take the seller's word for anything. Pull the tax returns. Get the bank records. Build your own model of profitability. That takes a weekend. Do it before you make an offer.

Second, get a team. You need a CPA, an attorney, and someone who understands the industry. These people will cost you $5,000-$15,000. That's 1-2 percent of a typical acquisition cost. It's the best money you'll spend.

Third, do a deep dive on customer concentration, key person dependency, and lease terms. Those three things kill more deals than anything else. Understand them fully before you're emotionally committed to the deal.

Fourth, get the offer in writing. Make it conditional on due diligence. Make it clear what you're buying (the business, the equipment, the inventory, the customer list). Make it clear what you're not buying (the seller's liabilities, pending lawsuits, environmental issues).

Fifth, do the due diligence. It's tempting to skip this when you're excited about the deal. Don't. Spend the money on the QoE report. Spend the time on customer calls. Verify everything.

Want to check if a business is worth what the seller claims? Use our free business valuation calculator to run your own numbers before you even start negotiations.

Need guidance on spotting red flags specific to the industry you're looking at? Contact us for a free consultation and we'll help you build a due diligence checklist customized to the deal.

Looking for funding once you've found the right business? Check out our unsecured funding programs that can provide up to $500,000 with no collateral required, letting you move fast when you find the right opportunity.

The difference between a good acquisition and a disaster is discipline. It's asking hard questions when you're excited. It's walking away from bad deals. It's verifying what the seller tells you. None of it is complicated. Most of it is just work. But that work is what separates the buyers who build wealth from the ones who buy expensive lessons.

Verify everything. Trust no one. Check your assumptions. That's how you win.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.