One of the biggest fears buyers have when purchasing a business is that the customers will leave after the sale. And honestly, it's a valid concern. If you've built your business on personal relationships, and many small business owners have, those customers may be loyal to you personally, not to the business itself.

I've seen deals where the seller walked away on closing day and 30% of the customer base followed them out the door within six months. I've also seen transitions where the seller stayed involved for 90 days, introduced the buyer properly, and the business retained over 95% of its customers.

The difference isn't luck. It's planning. And that planning needs to start well before you close the deal.

Why Customer Retention Is a Deal Maker or Breaker

Customer retention directly affects the value of your business. When a buyer is evaluating your company, they're not just buying your revenue. They're buying the expectation that your revenue will continue.

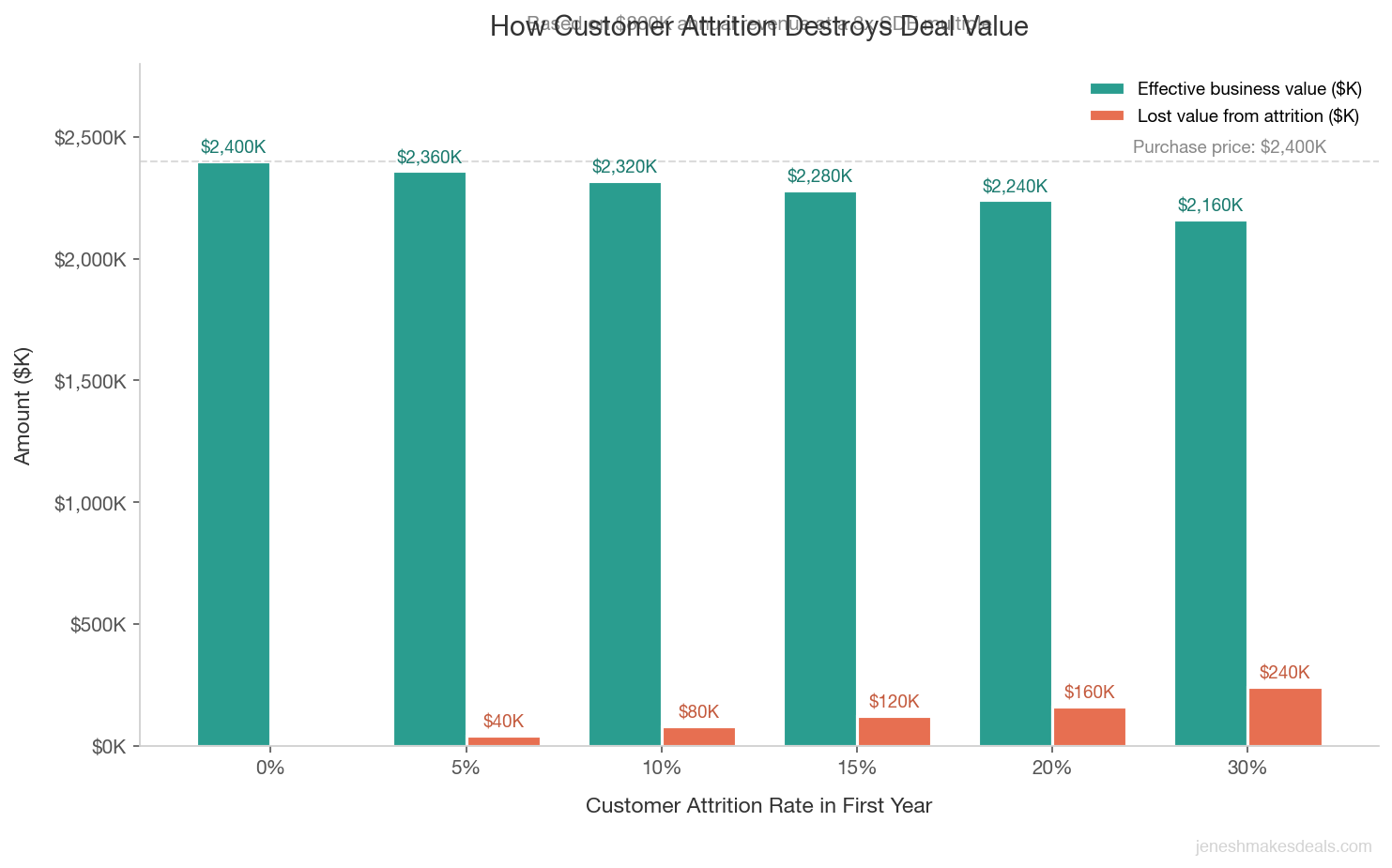

If your business generates $800,000 in annual revenue and you sell at a 3x multiple, the buyer is paying $2.4 million. But if 20% of your customers leave in the first year after the sale, the buyer effectively overpaid by $480,000. That's a problem for the buyer, and it's a problem for you if there's an earnout or any post closing adjustments tied to revenue performance.

A well planned customer transition can be the difference between retaining 95% of your customer base and losing 30% of it. That gap can translate to hundreds of thousands of dollars in deal value.

Buyers know this, which is why customer concentration is one of the first things they evaluate during due diligence. If 40% of your revenue comes from one client, that client relationship becomes the most important factor in the entire deal. If that client leaves, the deal economics fall apart.

Even if your customer base is well diversified, the transition period is still critical. Customers who feel ignored, confused, or uncertain about the future are much more likely to start exploring alternatives.

Assessing Your Customer Relationships Before Listing

Before you even put your business on the market, you should take an honest look at your customer relationships. Ask yourself these questions:

- How many customers do you have, and what does the concentration look like? If your top 5 customers account for more than 50% of revenue, that's a red flag for buyers and a transition risk you need to plan around.

- What's your customer retention rate? If you're already losing 15% to 20% of customers annually, the buyer will factor that into the price. But if your retention rate is 90% or higher, that's a strong selling point.

- Are your customer relationships personal or institutional? Do customers call you directly, or do they work with your team? The more institutional the relationships are, the easier the transition will be.

- Are there contracts in place? Customers under multi year contracts are much less likely to leave after a sale than customers who buy on a transactional basis with no commitment.

- How long have your customers been with you? Long term customers who've been with you for 5 or 10 years are generally more stable than new customers you acquired last quarter.

This assessment will help you identify which customers are at risk during a transition and develop specific strategies for retaining them.

Want to understand how customer concentration affects your valuation? Try our free business valuation calculator to see how your customer metrics impact what your business is worth.

Building Institutional Relationships Before You Sell

If your customers are primarily loyal to you and not to your company, you need to start changing that dynamic long before you list the business. This is one of the most valuable things you can do to increase the value of your business and make the transition smoother.

Here's how to start institutionalizing your customer relationships:

Introduce a team member as the primary point of contact. If you've been the one answering every call and handling every issue, start transitioning those responsibilities to a trusted employee. Let customers get to know someone else on your team. Over time, they'll build a relationship with that person, and the transition to a new owner will feel less jarring.

Standardize your service delivery. If your service varies based on your personal involvement, document and standardize your processes. Create standard operating procedures for how customers are onboarded, how orders are fulfilled, how complaints are handled, and how follow ups are conducted. When the service is consistent regardless of who's delivering it, customers are less concerned about ownership changes.

Implement a CRM system. If you don't already have one, set up a customer relationship management system that tracks every interaction, preference, and detail about each customer. This gives the buyer a roadmap for maintaining those relationships. They'll know which customers like a quarterly check in call, which ones prefer email, and which ones need special attention.

Lock in contracts where possible. If you have customers on handshake agreements, try to convert those into formal contracts before you sell. A customer who's committed to a two year contract is much more valuable to a buyer than one who could walk away at any time.

The Transition Assistance Agreement

Most business purchase agreements include a transition assistance provision, also called a transition services agreement or consulting agreement. This is where you, the seller, agree to help the buyer learn the business and maintain customer relationships for a period after closing.

Typical transition periods last 60 to 180 days, though some deals extend to 12 months or longer for businesses with complex customer relationships.

| Factor | Short Transition (60 to 90 days) | Standard Transition (90 to 180 days) | Extended Transition (6 to 12+ months) |

|---|---|---|---|

| Best for | Well diversified customer base | Mixed personal and institutional relationships | Personal service firms, one person operations |

| Seller time commitment | 10 to 15 hours per week | 5 to 15 hours per week | 5 to 10 hours per week |

| Typical compensation | Included in deal | $5,000 to $10,000/month | $8,000 to $15,000/month |

| Customer retention risk | Low (institutional relationships) | Moderate (some personal ties) | High (deeply personal relationships) |

| Common in | Retail, e commerce, franchise | Professional services, B2B | Consulting, medical, legal practices |

During the transition, the seller typically:

- Introduces the buyer to key customers, either in person or by phone

- Trains the buyer on customer preferences, history, and relationship dynamics

- Remains available to answer questions about specific accounts

- Helps resolve any customer issues that arise during the handover

- Participates in joint meetings or calls as needed

The compensation for transition assistance varies. Some sellers provide it as part of the deal. Others negotiate a monthly consulting fee, typically $5,000 to $15,000 per month depending on the size of the business and the intensity of the involvement.

I always recommend sellers negotiate clear boundaries for their transition role. Define the number of hours per week, the types of tasks you'll assist with, and the end date. Without these boundaries, some buyers will lean on you indefinitely, which defeats the purpose of selling the business in the first place.

The transition assistance agreement is your insurance policy. Without clear boundaries on hours, tasks, and an end date, you risk becoming an unpaid employee of the business you just sold.

Introducing the Buyer to Customers

The customer introduction is one of the most important events in the entire transition. How you handle it sets the tone for the buyer's relationship with your customers going forward.

Here's my recommended approach for introducing the buyer:

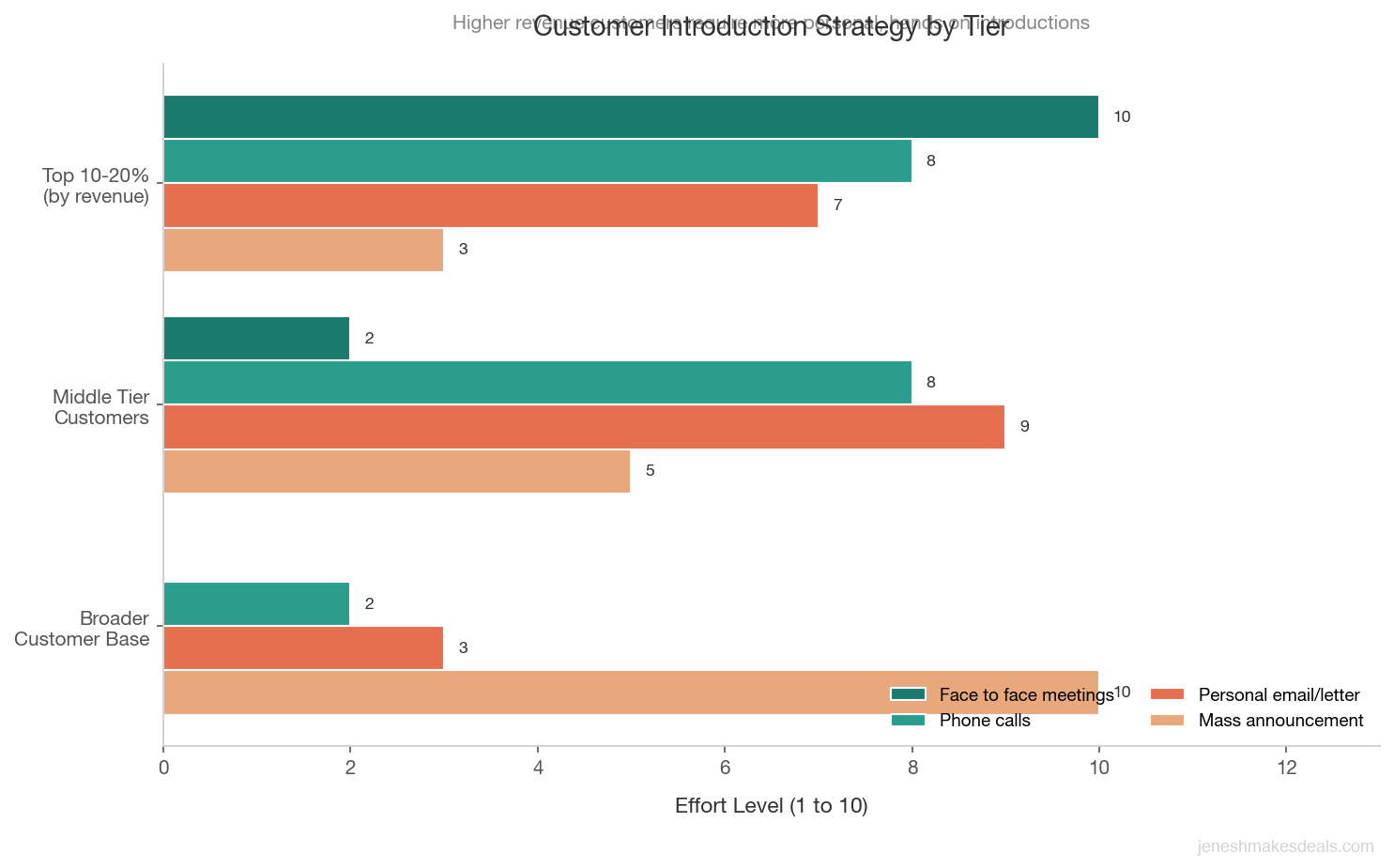

For Your Top 10 to 20% of Customers (by Revenue)

These are your most important accounts. They deserve personal, face to face introductions.

Schedule individual meetings. Call each key customer personally and let them know that you're transitioning the business to a new owner. Be positive and enthusiastic. Frame it as good news for the customer, not as you abandoning them.

Bring the buyer to the meeting. Introduce the buyer, share their background and vision for the business, and let them start building rapport. You should be there to facilitate, but let the buyer do most of the talking.

Reassure the customer. Address their concerns directly. Will the pricing change? Will the service quality remain the same? Will the team stay in place? The more specific you can be in your reassurances, the better.

Follow up. After the meeting, send a personal note to the customer thanking them for their loyalty and expressing your confidence in the new owner. The buyer should also follow up with a note of their own.

For Your Middle Tier Customers

These are customers who are important but don't warrant individual face to face meetings.

Send a personal letter or email. Write a thoughtful message introducing the new owner, explaining the transition, and reassuring them about continuity.

Make phone calls. The buyer should personally call each of these customers within the first week or two after closing. A quick 10 minute call to introduce themselves and ask about the customer's needs goes a long way.

Invite them to an event. Some businesses host a "meet the new owner" event, whether it's a lunch, an open house, or a webinar. This gives customers a chance to meet the buyer in a low pressure setting.

For Your Broader Customer Base

For customers who represent a smaller portion of revenue, a well crafted announcement is usually sufficient.

Send a professional announcement. A letter or email from both you and the buyer, co signed, that explains the transition and emphasizes continuity. Include the buyer's contact information and encourage customers to reach out with any questions.

Update your website and social media. Post an announcement that introduces the new owner and highlights the exciting future ahead for the business.

Thinking about selling your business? Contact us for a free consultation and we'll help you plan a customer transition strategy that protects your deal value.

Managing Customer Concerns During the Transition

No matter how well you plan the introduction, some customers will have concerns. Here are the most common ones and how to address them:

| Customer Concern | Risk Level | Best Response Strategy |

|---|---|---|

| Price changes | Medium | Commit to maintaining current pricing for a set period (6 to 12 months) |

| Service quality decline | High | Point to documented processes, retained team members, and buyer's track record |

| Staff turnover | Medium | Introduce key employees early and confirm retention agreements |

| Reason for selling | Low | Share a genuine, personal reason (retirement, new chapter) |

| Contract renegotiation | High | Confirm contracts survive ownership change; review assignment clauses |

"Will the prices change?" Be honest. If the buyer plans to maintain current pricing, say so. If adjustments are planned, address them proactively with a clear explanation of the value the customer will continue to receive.

"Will the same people be working on my account?" If key employees are staying, make that clear. If there will be changes, introduce the new team members early and ensure a smooth handoff.

"Why are you selling?" Customers want to know that you're not abandoning a sinking ship. Share your genuine reason for selling, whether it's retirement, pursuing a new opportunity, or wanting to spend more time with family. Make it personal and relatable.

"What if the quality goes down?" This is the big one. The best way to address it is to demonstrate that the systems and processes are in place to maintain quality regardless of who owns the business. Point to the team, the procedures, and the buyer's commitment to maintaining standards.

"Can I get out of my contract?" Some customers may use the ownership change as an excuse to renegotiate or exit their agreements. Check your contracts carefully. Most include a provision that the contract survives a change of ownership. If it doesn't, this is something to address before the sale.

Structuring Earnouts Around Customer Retention

In some deals, the purchase price includes an earnout component that's tied to post closing performance. If customer retention is a concern, the earnout might be specifically linked to revenue retention or customer retention metrics.

For example, the deal might be structured as $1.5 million at closing plus $500,000 payable over 24 months, contingent on the business retaining at least 80% of its revenue.

If you're agreeing to an earnout, make sure the terms are clear and fair:

- Define the metrics precisely. What counts as retained revenue? Does it include price increases? What about new customers acquired by the buyer?

- Establish baseline numbers. Use a specific, agreed upon revenue figure as the baseline for measuring retention.

- Define the measurement period. Is retention measured monthly, quarterly, or annually?

- Protect against buyer sabotage. Include provisions that prevent the buyer from intentionally driving away customers to reduce the earnout payment. For example, require the buyer to maintain minimum service levels and staffing during the earnout period.

- Get professional help. Earnouts are one of the most disputed aspects of business sales. Have your attorney review the terms carefully.

What to Do in the First 90 Days After Closing

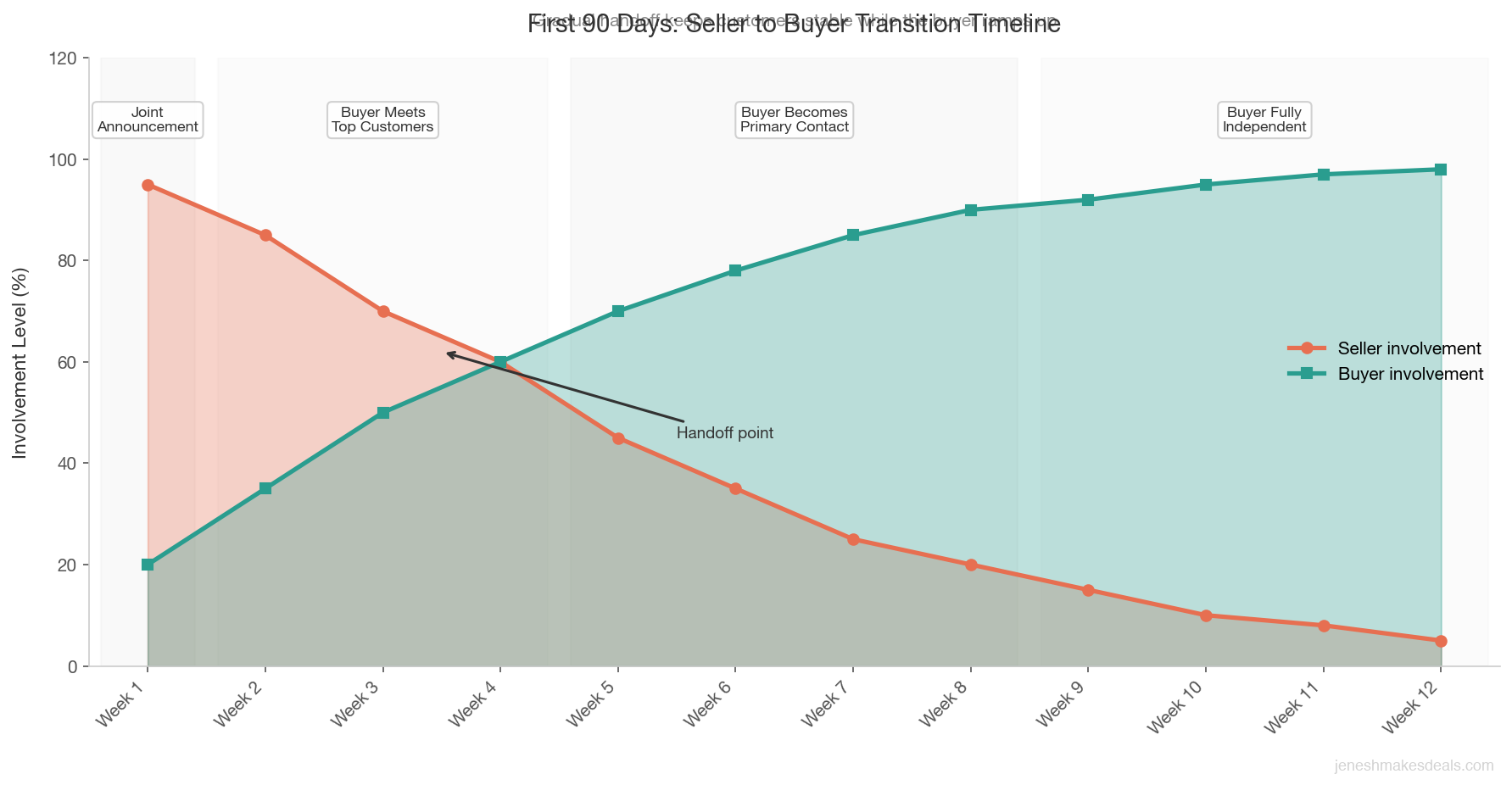

The first 90 days after closing are critical for customer retention. Here's a timeline of what should happen:

Week 1: The seller and buyer jointly announce the transition to all customers. Top accounts get personal calls. The seller begins introducing the buyer to key relationships.

Weeks 2 to 4: The buyer meets with all top tier customers, either in person or by phone. The seller is available for joint calls or meetings as needed. The buyer starts learning customer preferences, pain points, and relationship dynamics.

Weeks 5 to 8: The buyer takes over as the primary point of contact for most accounts. The seller is available in an advisory capacity but is not initiating customer contact. The buyer focuses on quick wins, like resolving any outstanding issues or delivering on promises made during introductions.

Weeks 9 to 12: The buyer is fully independent in managing customer relationships. The seller is available for occasional questions but is largely out of the picture. The buyer assesses which customers are stable, which need extra attention, and which might be at risk.

Throughout this period, the buyer should be tracking customer engagement, satisfaction, and any signs of potential churn. If a customer starts ordering less, responding more slowly, or expressing concerns, that's a signal to intervene immediately.

When Customer Relationships Can't Be Transferred

Let's be honest. There are some situations where customer relationships are very difficult to transfer:

Professional services firms. If you're a consultant, attorney, financial advisor, or other professional where the client relationship is deeply personal, some clients will follow you regardless of what you do.

Businesses built on charisma. If your personal brand is the business, such as a popular restaurant owner, a local celebrity, or a social media personality, the customer relationship is with you, not the entity.

One person operations. If you are the entire business, every customer relationship is personal by definition. Transitioning these relationships is possible but requires a longer, more gradual handoff.

If your personal brand is the business, start building institutional systems at least one to two years before you plan to sell. The longer customers interact with your team and processes instead of just you, the easier the eventual handoff becomes.

In these cases, you have a few options:

- Stay involved longer. A 6 to 12 month transition period, or even longer, may be necessary.

- Reduce the asking price. If customer attrition is likely, the deal should reflect that risk.

- Structure the deal with a larger earnout. This aligns your interests with the buyer's because you only get paid if the customers stick around.

- Train a successor before selling. Spend a year or two developing someone who can take over the customer relationships before you even think about listing the business.

The Bottom Line

Customer relationships are often the most valuable asset in a small business. How you handle the transition of those relationships can mean the difference between a successful sale and one that ends in disputes, earnout clawbacks, and regret.

Start planning the transition early. Build institutional relationships before you sell. Negotiate a clear transition assistance agreement. Introduce the buyer to your customers with care and enthusiasm. And stay involved long enough to ensure stability.

The goal isn't just to close the deal. It's to close a deal that works for everyone, including your customers.

Need help figuring out what your business is worth? Use our free business valuation calculator to get a quick estimate based on your industry's typical multiples.

Ready to start planning your exit? Contact us for a free consultation and we'll help you develop a transition strategy that maximizes your sale price and protects your customer relationships.

Related Articles

April 29, 2026

Selling a Franchise Business vs an Independent Business

Selling a franchise is a fundamentally different process than selling an independent business. Here is what every franchise owner needs to know.

April 21, 2026

What Is a Management Buyout and Is It Right for Your Business?

A management buyout lets your team buy the business. Learn how MBOs work, what they cost, and when they make sense for sellers.

April 13, 2026

How to Find the Right Business Broker for Your Industry

Not all brokers know your industry. Here's how to find one who actually understands your business and can get you top dollar.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.