When you own both the business and the building it operates in, selling gets more complicated. You're not just selling a company anymore. You're selling two assets, each with its own valuation methodology, its own financing requirements, and its own set of buyers.

I've worked with restaurant owners who owned their building, HVAC companies with warehouses, and retail shop owners who had been in the same location for 20 years. In every case, the real estate component changed the dynamics of the deal in ways most sellers didn't expect.

The good news is that owning both the business and the property can actually increase your total sale proceeds. The challenge is structuring the deal correctly so that both assets are valued fairly and the right buyers can access the financing they need.

Should You Sell the Business and Real Estate Together or Separately

This is the first and most important question you need to answer, and there's no one size fits all answer. It depends on your specific situation.

Selling Together

Selling the business and real estate as a package deal is simpler from a logistical standpoint. One buyer, one transaction, one closing. But there are some significant considerations.

Pros:

- Simpler transaction with fewer parties and documents

- The buyer gets full control of both the business and the location

- No risk of losing the lease or having a difficult landlord

- Can be more attractive to owner operator buyers who want long term stability

- SBA loans can cover both the business and the real estate in certain programs

Cons:

- The total price tag is higher, which reduces the pool of qualified buyers

- The business and real estate may have very different values, making pricing complicated

- Some buyers want the business but don't want to own commercial real estate

- Financing can be more complex when two different assets are involved

Selling Separately

Selling the business and real estate as separate transactions gives you more flexibility, but it adds complexity.

Pros:

- Separate buyers can pay fair market value for each asset

- The business buyer can lease the property from the real estate buyer (or from you if you keep it)

- A real estate investor might pay more for the property than a business buyer would

- You can retain the real estate as an investment and collect rent from the new business owner

Cons:

- Two separate transactions, two sets of negotiations, two closings

- The business buyer needs a lease, which adds another negotiation

- If the real estate doesn't sell or the lease terms aren't favorable, the business sale could fall through

- Timing both sales to close simultaneously can be challenging

The Hybrid Approach

The most common approach I see is what I call the hybrid. You sell the business and lease the real estate to the buyer with an option to purchase later. This gives the buyer time to build equity and get financing for the property, while you collect rental income and retain a valuable asset.

This approach works well for sellers who want to maximize their long term income and for buyers who can't afford both the business and the building at once.

| Approach | Best For | Complexity | Buyer Pool |

|---|---|---|---|

| Sell together | Owner operators who want full control | Low | Smaller (higher price tag) |

| Sell separately | Maximizing value from each asset | High | Larger (two separate buyers) |

| Hybrid (lease + option) | Sellers who want ongoing income | Medium | Moderate (lower upfront cost for buyer) |

The hybrid approach is often the smartest play. You get rental income, you keep a hard asset, and you give the buyer room to grow into the deal.

Thinking about selling your business? Contact us for a free consultation and we'll help you figure out the best approach for your specific situation.

How to Value a Business With Real Estate

Valuing a business that includes real estate requires separating the two assets and valuing each one independently.

Valuing the Business

The business should be valued using standard business valuation methods, typically a multiple of seller's discretionary earnings (SDE) for smaller businesses or a multiple of EBITDA for larger ones.

Here's the key point: when you calculate the business earnings, you need to include a market rate rent expense, even if you currently don't pay rent because you own the building. This is called normalizing the rent.

For example, if your business generates $400,000 in SDE and comparable businesses rent their space for $60,000 per year, your normalized SDE would be $340,000 ($400,000 minus $60,000 in rent). If the business sells at a 3x SDE multiple, the business value would be $1,020,000.

If you don't normalize the rent, the business earnings look inflated because they don't include one of the most significant operating expenses. Buyers and their advisors will catch this, and it can lead to disagreements about the business value.

Valuing the Real Estate

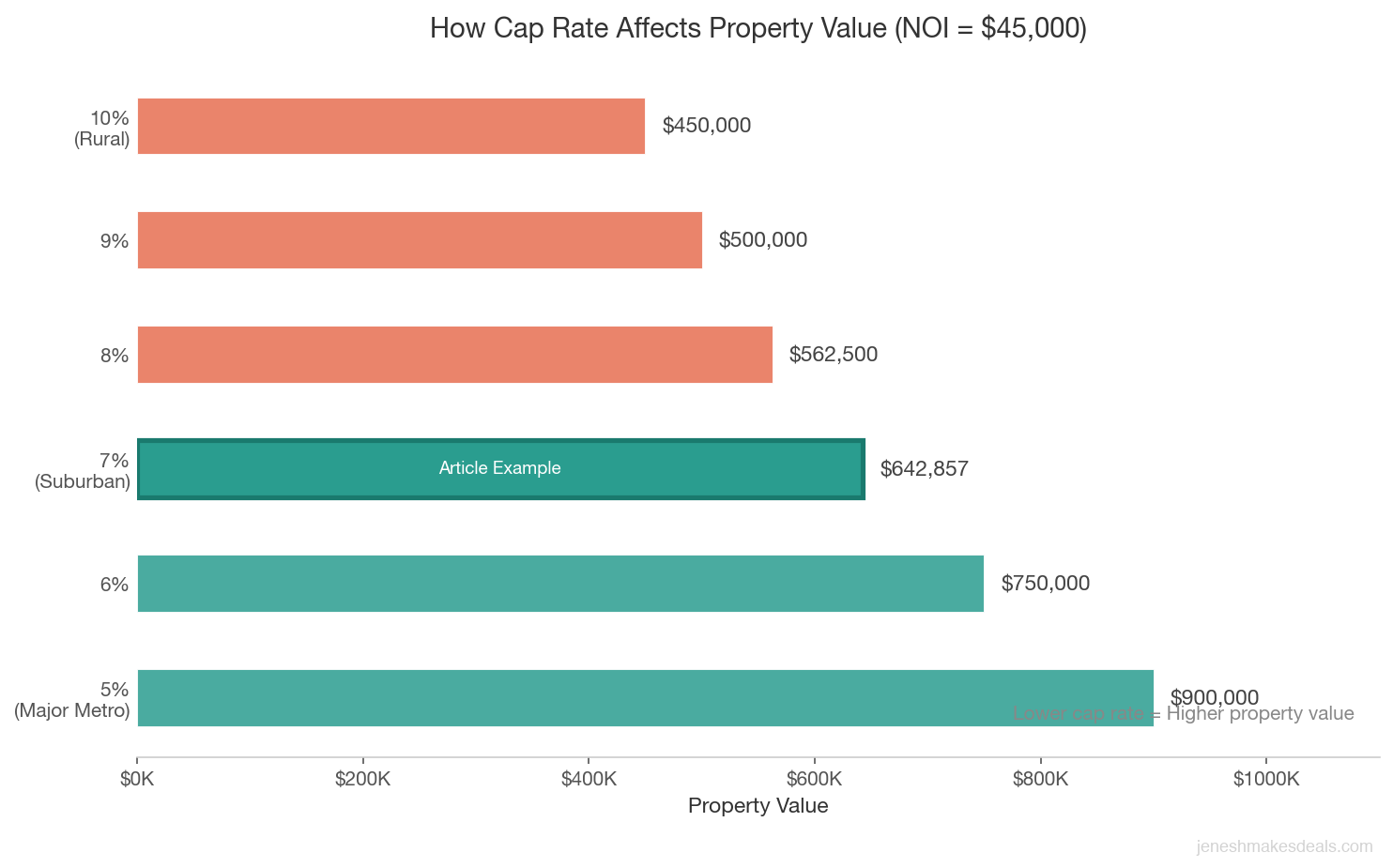

The real estate should be valued using standard commercial real estate appraisal methods. The most common approach for properties occupied by a business is the income approach, which values the property based on its rental income potential.

The income approach works like this:

- Determine the market rent for the property (what a tenant would pay on the open market)

- Calculate the net operating income (NOI) by subtracting operating expenses from the gross rental income

- Apply a capitalization rate (cap rate) to determine the property value

For example, if the property could rent for $60,000 per year, operating expenses are $15,000, the NOI is $45,000. If the cap rate for similar properties in the area is 7%, the property value would be approximately $643,000 ($45,000 divided by 0.07).

Cap rates vary by location, property type, and market conditions. In major metro areas, cap rates might be 5% to 6%, resulting in higher property values. In rural areas or secondary markets, cap rates might be 8% to 10%, resulting in lower values.

The Total Package

Using the numbers from the examples above:

- Business value: $1,020,000

- Real estate value: $643,000

- Total package: $1,663,000

This is a much different picture than if you simply applied a business multiple to the total earnings without normalizing rent. That approach would have valued the business at $1,200,000 (3x $400,000) and ignored the real estate value entirely, or worse, double counted the benefit of owning the building.

If you skip rent normalization, you either leave money on the table by ignoring the real estate value or you inflate the business price and scare buyers away. Separate the two assets and value each one on its own merits.

Want to see what your business might be worth? Try our free business valuation calculator to get a quick estimate based on your industry's typical multiples.

Financing Considerations for Buyers

One of the biggest practical challenges when selling a business with real estate is financing. The buyer needs to finance two different types of assets, and the lending options are different for each.

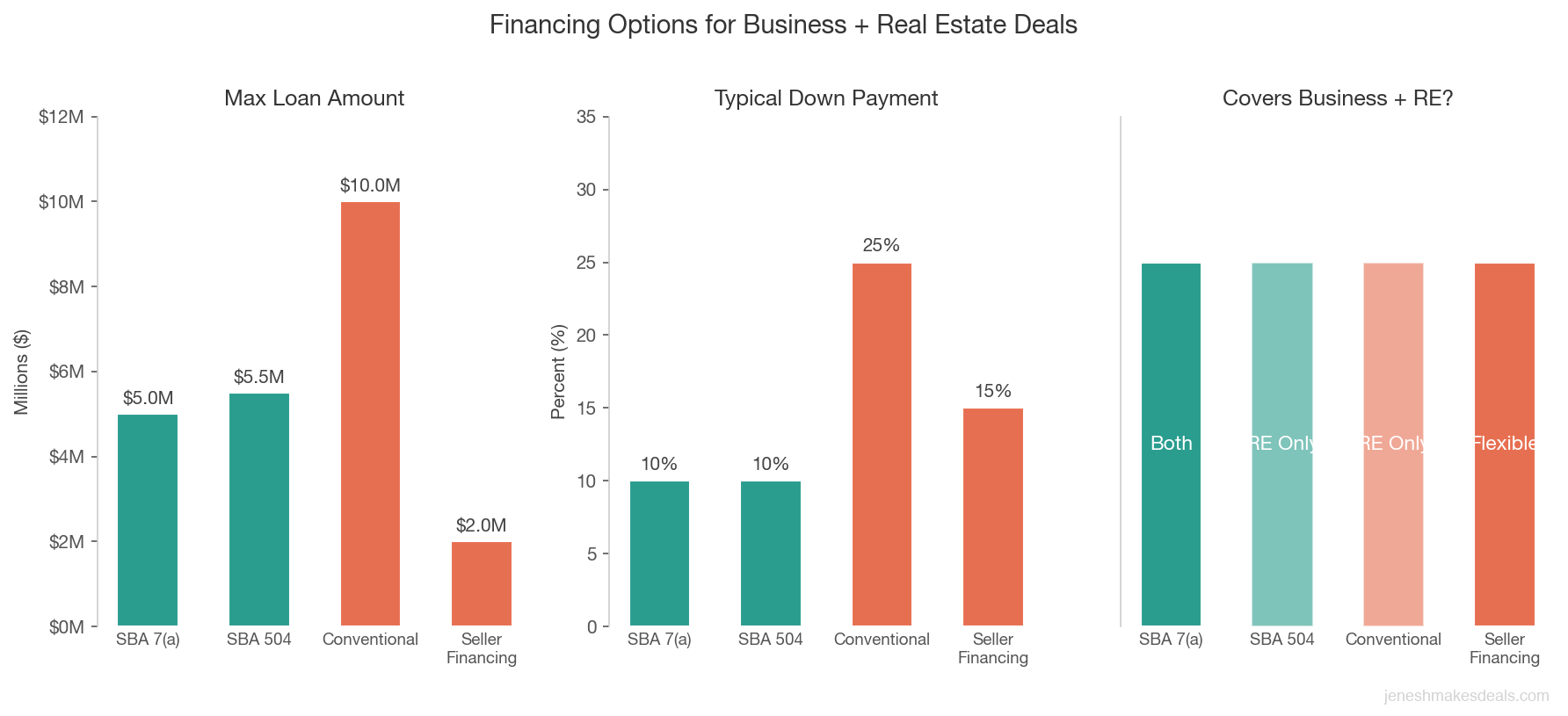

| Financing Option | Max Amount | Down Payment | Covers Business + RE | Best For |

|---|---|---|---|---|

| SBA 7(a) | $5M | 10% | Yes (both in one loan) | Small businesses under $5M total |

| SBA 504 | $5.5M | 10% | RE only (need separate loan for business) | Larger property acquisitions |

| Conventional | $10M+ | 20% to 30% | RE only | Buyers who don't qualify for SBA |

| Seller financing | Varies | Negotiable | Flexible | Gap financing or full seller carry |

SBA Loans

SBA 7(a) loans can finance both business acquisitions and commercial real estate in a single loan, up to $5 million. This is one of the reasons SBA financing is so popular for small business purchases that include property.

The SBA 504 loan program is specifically designed for commercial real estate and can provide up to $5.5 million for property acquisition and improvement. However, 504 loans typically can't be used for the business acquisition itself, so the buyer might need a 7(a) loan for the business and a 504 loan for the property.

Conventional Commercial Mortgages

For larger deals or buyers who don't qualify for SBA financing, a conventional commercial mortgage can finance the real estate component. These typically require 20% to 30% down and have higher interest rates than SBA loans, but they're more flexible in terms of deal size and structure.

Seller Financing

Seller financing is common in deals that include real estate, especially when the buyer can't get traditional financing for the full amount. The seller might carry a note on the real estate portion while the buyer uses an SBA loan for the business.

For example, if the total deal is $1.6 million and the buyer gets a $1.1 million SBA loan, the seller might carry a $300,000 note on the real estate, with the buyer putting down $200,000 in cash.

Seller financing on real estate is generally secured by the property itself (a mortgage or deed of trust), which gives the seller strong collateral if the buyer defaults.

Seller financing on the real estate portion is one of the safest forms of carry back you can offer. You hold a lien on a hard asset that isn't going anywhere. If the buyer defaults, you get the property back and you've already collected months of payments.

Lease With Option to Purchase

If the buyer can't finance the real estate at closing, a lease with a purchase option lets them acquire the business now and buy the property later. The lease should include clear terms for the purchase option, including the purchase price (or how it will be determined), the timeframe for exercising the option, and any rent credits that will apply toward the purchase price.

Structuring the Deal

The structure of a real estate inclusive deal requires careful attention to several key areas.

Asset Allocation

When you sell a business with real estate, the total purchase price needs to be allocated between the business assets and the real estate. This allocation affects taxes for both the buyer and the seller.

The allocation should be based on fair market values. If the total price is $1.6 million and the real estate is appraised at $640,000, the business allocation would be $960,000. Within the business allocation, you'll further allocate between inventory, equipment, goodwill, non compete agreements, and other assets.

Work with your accountant on this. The allocation has significant tax implications, and the IRS requires that the buyer and seller use consistent allocations on their respective tax returns (reported on IRS Form 8594).

Tax Implications

Selling real estate as part of a business sale creates different tax treatment for different portions of the proceeds:

- Real estate gains are typically taxed as capital gains (long term if you've owned the property for more than a year), but depreciation recapture is taxed at a higher rate (up to 25%)

- Business goodwill is taxed as long term capital gains

- Inventory is taxed as ordinary income

- Equipment may be subject to depreciation recapture

If you're doing a 1031 exchange on the real estate portion (exchanging it for another investment property to defer capital gains taxes), the transaction becomes even more complex. You'll need to close the real estate portion as a separate transaction and work with a qualified intermediary to handle the exchange.

Lease Terms if Selling Separately

If you're selling the business but keeping the real estate, the lease you offer to the business buyer is critical. Here's what to think about:

- Lease term: A 5 to 10 year initial term with renewal options is standard. Shorter terms make the business less valuable because the buyer could lose their location.

- Rent: Set the rent at fair market value. If you charge above market rent to inflate your real estate returns, it'll reduce the business earnings and depress the business sale price.

- Rent escalation: Include annual rent increases, typically tied to CPI or a fixed percentage (2% to 3% per year).

- Assignment clause: Make sure the lease allows the buyer to assign or sublease. This is important for the buyer's future exit strategy.

- Maintenance responsibilities: Clearly define who's responsible for structural maintenance, HVAC, roof, parking lot, and other major systems. Triple net (NNN) leases are common for commercial properties.

Due Diligence Specific to Real Estate

Beyond the standard business due diligence, a deal that includes real estate requires additional investigation:

Property appraisal. An independent commercial appraisal is essential for determining fair market value and is typically required by lenders.

Environmental assessment. A Phase I Environmental Site Assessment is standard for any commercial property transaction. If the Phase I identifies potential issues, a Phase II assessment with soil and groundwater testing may be needed.

Title search and title insurance. The buyer's attorney should conduct a thorough title search to identify any liens, encumbrances, easements, or other issues that could affect ownership. Title insurance protects the buyer against title defects that weren't discovered in the search.

Survey. A current survey confirms the property boundaries and identifies any encroachments, easements, or setback violations.

Building inspection. A commercial building inspection covers the structure, roof, HVAC, plumbing, electrical, and other major systems. The cost of deferred maintenance should be factored into the deal.

Zoning verification. Confirm that the current use of the property is permitted under local zoning regulations. Also check whether the buyer's planned use (if different from the current use) is allowed.

Lease review. If there are any tenants other than the business being sold, review all existing leases for terms, expiration dates, and any unusual provisions.

Property tax review. Check the current property tax assessment and any pending reassessments. In some jurisdictions, a property sale triggers a reassessment that could significantly increase property taxes.

Insurance review. Verify current insurance coverage and get quotes for the buyer's insurance needs. Property insurance costs can vary significantly based on the building's condition, location, and use.

Common Mistakes When Selling a Business With Real Estate

After working on these types of deals, I've seen the same mistakes come up again and again.

Not separating the valuations. Some sellers try to sell everything as one lump sum without breaking out the business and real estate values. This makes it harder for buyers to get financing and often leads to disagreements during negotiations.

Overvaluing the real estate. Sellers who built or improved their property often have an emotional attachment to it and believe it's worth more than the market says. Get an independent appraisal and be prepared to accept the results.

Undervaluing the real estate. Some sellers focus so heavily on the business value that they undercount the property. If you've owned the property for decades and it's in a good location, the real estate might actually be worth more than the business.

Ignoring the rent normalization. If you don't charge yourself rent and don't normalize the business earnings to include market rate rent, the business valuation will be inflated and buyers will push back.

Not considering the tax implications. The difference between selling the business and real estate together versus separately can have major tax consequences. Talk to your accountant before deciding on a structure.

Neglecting property maintenance. A building with deferred maintenance, like a leaking roof, aging HVAC system, or cracked parking lot, will reduce the property value and give buyers negotiating power. Fix major issues before listing.

Forgetting about the lease. If you're keeping the real estate and leasing it to the buyer, the lease terms need to be finalized before the business sale closes. Don't leave this for the last minute.

Skipping the environmental assessment. Even if you've operated the same business in the same location for 30 years and never had an issue, an environmental assessment is essential. Previous owners or neighboring properties could have created problems you don't know about.

The most expensive mistake I see is sellers who skip the environmental assessment. One contamination finding after closing can cost more than the entire property is worth.

Ready to sell your business? Contact us for a free consultation and we'll help you structure the deal, whether you're selling the real estate with the business or keeping it as an investment.

Working With the Right Team

Selling a business with real estate requires a broader team of advisors than a business only sale:

- Business broker who understands both business valuation and commercial real estate

- Commercial real estate appraiser for an independent property valuation

- M&A attorney or business transaction attorney for the purchase agreement

- Real estate attorney for the property transfer, title, and any lease agreements

- CPA or tax advisor for tax planning and asset allocation

- Environmental consultant for the Phase I assessment

- Commercial lender who understands SBA and conventional financing for combined deals

Make sure your advisors are communicating with each other. A deal that includes real estate has a lot of moving parts, and if your broker, attorney, and accountant aren't on the same page, things can fall through the cracks.

Do not try to save money by using the same attorney for both the business sale and the real estate transfer. These are two different specialties, and an attorney who is great at M&A may miss critical property issues, and vice versa. The cost of two attorneys is far less than the cost of one missed problem.

The Bottom Line

Selling a business with real estate is more complex than a business only sale, but it can also be more lucrative if you structure it correctly. The key decisions are whether to sell or lease the property, how to value each asset independently, and how to structure the deal so that buyers can get financing.

Start by getting independent valuations for both the business and the real estate. Normalize your business earnings to include market rate rent. Decide whether selling together, separately, or via a lease with option makes the most sense for your situation. And build a team of advisors who have experience with these types of transactions.

Need a quick estimate of what your business is worth? Use our free business valuation calculator to run the numbers.

Want to discuss your options? Contact us for a free consultation and we'll help you figure out the best approach for maximizing your total proceeds.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.