Selling your business is one of the most emotionally loaded decisions you'll make. And while you're busy getting financials together, fielding offers, and working through due diligence, there's a group of people who have no idea what's happening but will be directly affected by it: your team.

I've helped sellers through dozens of business transitions, and the ones that go sideways almost always have one thing in common. The seller waited too long to involve the right people, or they brought in the wrong people too early. Managing employee communication during a sale is its own skill set, and most business owners have never had to do it before.

This post walks you through everything, from who to tell first to how to structure stay bonuses, so your team lands safely when the deal closes.

Why Employee Retention Matters More Than You Think

Here's a number that should get your attention: studies consistently show that losing a key employee during or after a business sale can reduce the business's value by 10% to 25%. For a $1 million business, that's $100,000 to $250,000 walking out the door with whoever just quit.

Buyers aren't just buying your revenue. They're buying your operations, your customer relationships, and your institutional knowledge. A lot of that lives inside your team's heads. The office manager who knows every vendor quirk, the sales rep who has personal relationships with your top five accounts, the technician who can fix the machine no one else understands. These people are part of what makes the business worth buying.

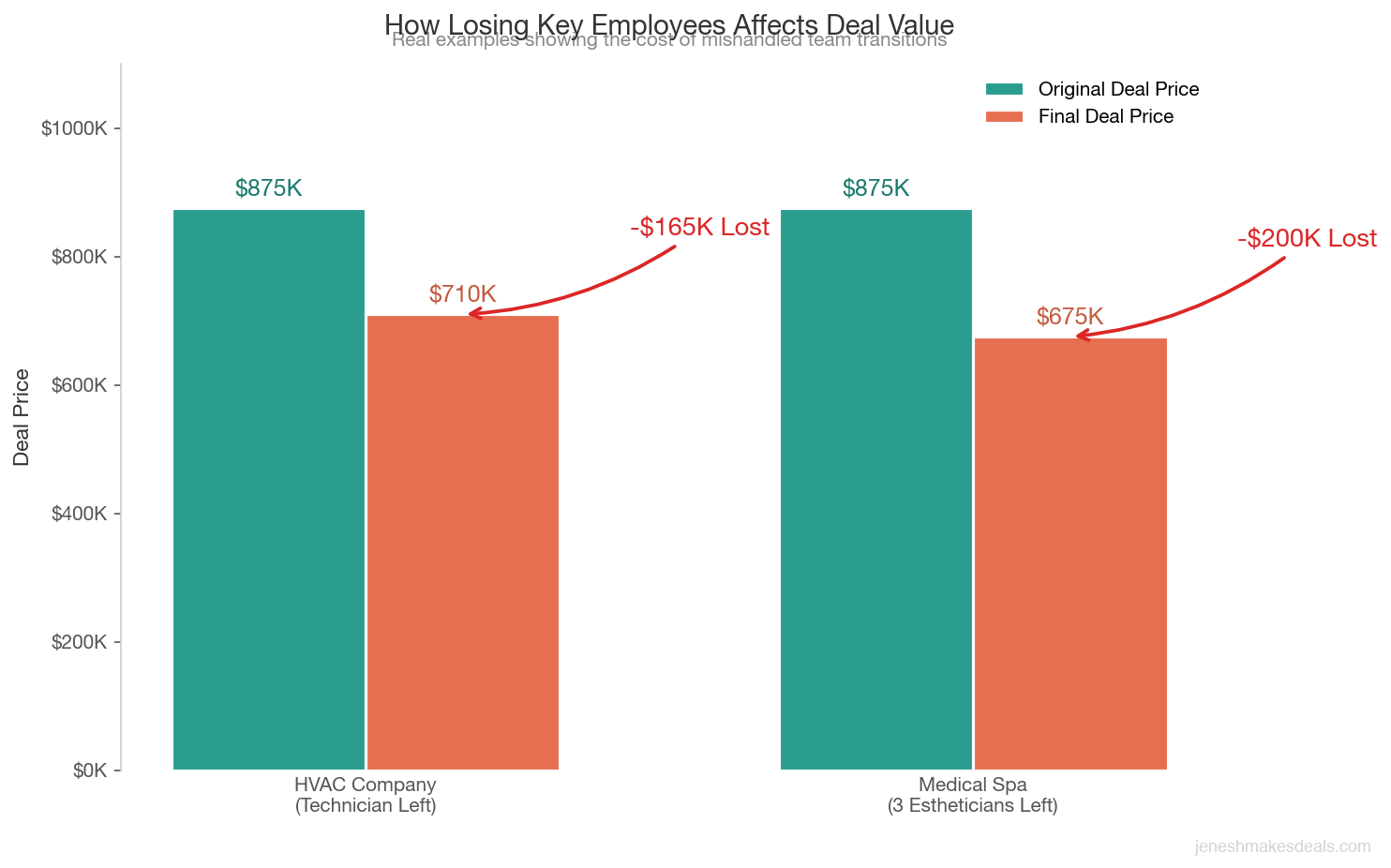

I had a client who ran a specialty HVAC company. Great business, solid margins. We got it under contract for $875,000. Three weeks before closing, his lead technician quit because a rumor spread through the shop. The buyer repriced the deal to $710,000 after finding out. That $165,000 gap is exactly the kind of thing that happens when team transitions are mishandled.

Losing a key employee during a business sale can reduce the deal price by 10% to 25%. For a $1 million business, that means $100,000 to $250,000 walking out the door.

Buyers will ask about your key employees during due diligence. They'll want to know who the critical people are, whether those people know about the sale, and whether there's any risk of them leaving. Your answers to those questions affect your final price.

Confidentiality First: Who Keeps the Secret

Before you tell anyone on your team anything, you need a confidentiality agreement with your buyer and your broker. This is standard. What's less standard is thinking clearly about who inside your business needs to know before closing, and who absolutely cannot know yet.

The risk is real. If employees find out the business is for sale before you're ready to announce it, you can expect a few things to happen. Some will start updating their resumes. Others will call your competitors. Word will get to customers. And then you're managing a fire instead of a sale.

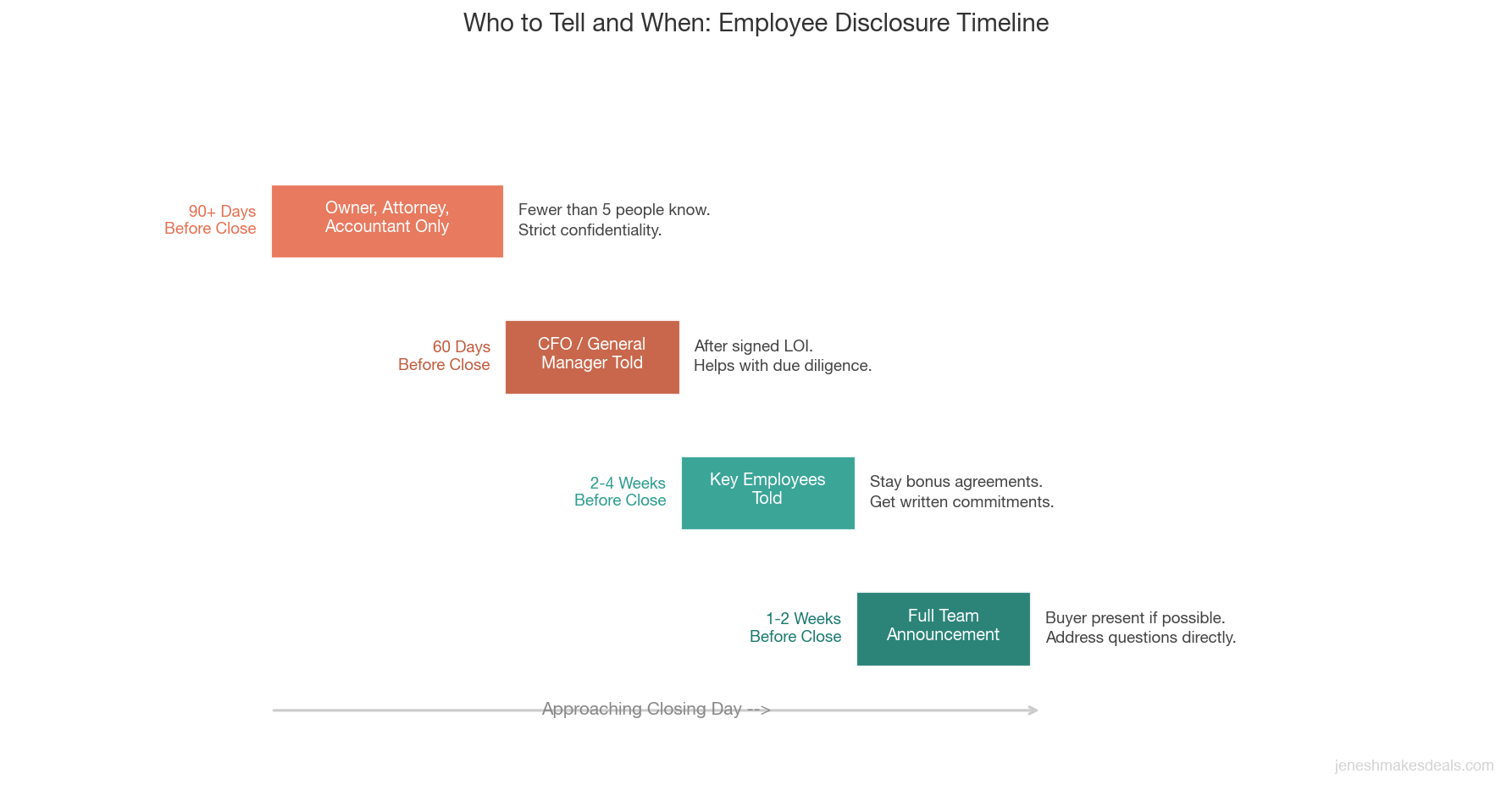

A good rule of thumb: fewer than five people should know about a pending sale until you're within 30 days of closing. That group usually includes the owner, the accountant, the attorney, and maybe one trusted lieutenant who needs to help pull due diligence materials together.

If your bookkeeper or office manager needs to compile financial documents for the buyer, give them a narrow explanation. Tell them you're doing financial planning or preparing for a potential financing event. It's not the full picture, but it buys you time without lying outright. Most sophisticated advisors will give you scripts for these situations.

Who to Tell First: The Key Employee Conversation

There's a hierarchy here, and skipping steps causes problems.

Your CFO or General Manager typically needs to know early if they're involved in due diligence or buyer meetings. These conversations should happen after you have a signed letter of intent and a solid sense that the deal will close. Not before.

Your key employees should be told 2 to 4 weeks before closing. Key employees are people the business genuinely cannot function without. Think about who you'd be most worried about losing. That's your list.

General staff should be told 1 to 2 weeks before closing, after key employee agreements are in place and the deal is essentially done. This is a planned announcement, not a rumor control session.

Why this order? Because key employees hold real power in this process. If a buyer finds out that your operations depend heavily on one person and that person doesn't know the business is being sold, it creates real deal risk. Some buyers will require written commitments from key employees as a condition of closing.

Key Employee Retention Agreements and Stay Bonuses

This is the tool most sellers forget about, and it's one of the most effective things you can do to protect your deal.

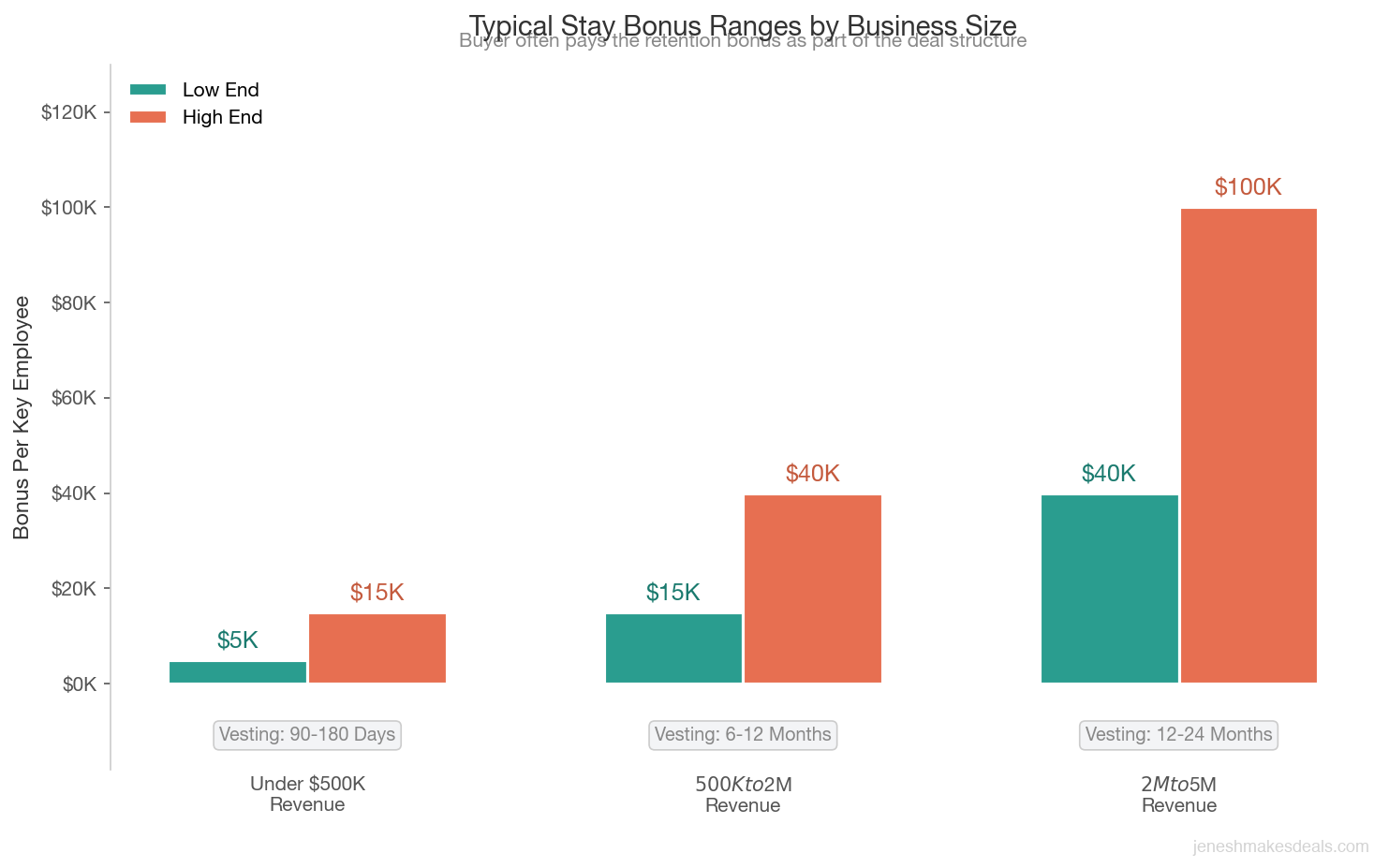

A stay bonus, sometimes called a retention bonus, is a cash payment offered to key employees in exchange for staying through the transition period. Here's how they typically work:

| Business Size | Typical Stay Bonus | Vesting Period |

|---|---|---|

| Under $500K revenue | $5,000 to $15,000 per key employee | 90 to 180 days post-close |

| $500K to $2M revenue | $15,000 to $40,000 per key employee | 6 to 12 months post-close |

| $2M to $5M revenue | $40,000 to $100,000+ per key employee | 12 to 24 months post-close |

The buyer often pays the stay bonus, not the seller. You can negotiate this into the deal structure, especially if retaining those employees is a condition the buyer cares about. I've seen deals where the buyer agreed to fund a $75,000 retention pool because the three people in that pool represented the entire operational knowledge of the business.

Stay bonuses work because they give employees a financial reason to stay through the uncertain period instead of bailing at the first sign of instability. The key is making the bonus large enough to matter. A $2,500 bonus won't keep someone who has a competing job offer on the table.

You should also consider non solicitation agreements at this stage. These are separate from non compete agreements. A non solicitation agreement prevents a departing employee from poaching your customers or other staff. They're typically 1 to 2 years in duration and are enforceable in most states when written correctly. Your attorney should draft these.

Non Compete Agreements: What Sellers Need to Know

A lot of sellers are focused on signing their own non compete with the buyer. That's the big one, and it typically runs 3 to 5 years, restricted to your industry and geographic area. But there's a whole other layer that doesn't get enough attention: key employee non competes.

If your top sales rep leaves the day after closing and goes to work for your direct competitor, the buyer has a serious problem. And if that was foreseeable, it can become your problem too through deal warranties and reps.

The question of whether employee non competes are enforceable has gotten complicated in recent years. The FTC attempted to ban most non competes in 2024, though that rule faced legal challenges. State law varies significantly. California essentially doesn't enforce them. Texas and Florida generally do. If you're in a state that enforces them, your key employee agreements should include reasonable non compete language.

Talk to your attorney about what's enforceable in your state before promising the buyer anything about this. What I tell my clients is this: a well structured stay bonus combined with a clear non solicitation agreement is often more effective than a non compete that an employee will challenge in court.

How to Frame the Conversation With Your Team

Most employees hear "the business is being sold" and immediately think: will I have a job? Will my pay change? Will my benefits get cut? Will the new owner be a nightmare?

Your job in this conversation is to address those fears directly, not to give a motivational speech about the exciting future ahead. People see through that and it makes them more anxious, not less.

Employees would rather have a hard truth than a comfortable vagueness. If you don't know the answer yet, say so honestly and tell them when they will know more.

Here's what I recommend telling your team:

Start with facts. Tell them the sale is happening, who the buyer is at a high level (a local operator, a private equity firm, a strategic acquirer), and when the transition is expected to happen.

Address job security directly. If the buyer has committed to retaining staff, say so. If there will be changes, be honest about what you know and what you don't yet know. Employees would rather have a hard truth than a comfortable vagueness.

Explain the process. Tell them what the next 30 to 60 days look like. Who will they be meeting? What should they expect? When will they hear more?

Give them a direct line. Designate someone, whether it's you, your HR person, or a manager, who employees can ask questions without judgment. Uncertainty breeds rumor. Giving people a legitimate channel for their questions cuts that off.

One thing I've seen go really well: sellers who scheduled one on one conversations with each of their 10 to 15 person team before the general announcement. It takes more time, but it signals respect and tends to produce much better outcomes in the weeks after the announcement.

What Employees Worry About Most

I've sat in on a lot of these transition meetings. The questions employees ask, once they feel comfortable enough to ask them, are pretty consistent.

Will I keep my job? This is number one, full stop. If you can give a clear yes or a clear no, do it. If it's uncertain, say so honestly and tell them when they'll know more.

Will my pay change? Buyers generally don't cut pay as a first move. It's bad for morale and creates turnover. But employees don't know that. Reassure them that compensation changes, if any, will be communicated in advance.

What happens to my PTO and accrued benefits? This is a legal question that depends on your state and how the deal is structured. In an asset sale, the buyer is typically not required to honor accrued PTO, but many will as a goodwill gesture. In a stock sale, the buyer generally inherits all existing obligations. Know the answer to this before the meeting, because someone will ask.

What about health insurance? If the new owner plans to change carriers or coverage, employees should know that before it happens. Last minute benefit changes during a transition are a top reason employees quit.

Will the culture change? This is harder to answer and honestly you can't promise anything. What you can do is speak honestly about what you know about the buyer and their style.

| Employee Concern | What to Prepare Before the Meeting |

|---|---|

| Job security | Get written confirmation from buyer on staffing plans |

| Pay changes | Confirm whether buyer will honor current compensation |

| PTO and benefits | Review deal structure (asset vs. stock) with attorney |

| Health insurance | Ask buyer about carrier and coverage plans |

| Culture changes | Learn buyer's management style and share what you know |

The Buyer's Perspective on Your Team

Smart buyers do something sellers often forget to prepare for: they assess your team as part of due diligence. They'll ask who are the key people, what do they do, how long have they been there, and whether they've been told about the sale.

Some buyers want to meet key employees before closing. Some will make employment agreements with specific people a condition of the deal. I've seen buyers walk away from deals because the entire operation was run by one person who hadn't agreed to stay.

From the buyer's standpoint, they're inheriting not just a business but a set of relationships and operational expertise. They want to know that expertise will still be there when they take over. The more you can document your team's roles, responsibilities, and knowledge, the more confidence a buyer has.

I recommend creating a basic org chart and role summary document as part of your sale prep. It doesn't need to be elaborate. A one page document showing who does what, who reports to whom, and who the client facing people are does a lot to calm buyer anxiety.

If you want to understand what a buyer is looking at when they evaluate your business, use our business valuation calculator to see how different factors affect your price.

Training and Transition Planning

Once the deal closes, the transition period begins, and this is where a lot of sellers check out mentally right when they're most needed.

Most deals include a transition period where the seller stays on to train the buyer. This is typically 30 to 90 days for businesses under $2 million in revenue, and can run 3 to 12 months for larger or more complex operations. You may be compensated for this time through a consulting agreement, or it may be built into the deal structure at no additional cost.

During transition, your job is to transfer knowledge, introduce relationships, and troubleshoot problems. Key items to document and hand off include:

- Vendor contacts and relationship history

- Customer account notes and preferences

- Standard operating procedures for recurring tasks

- Software logins and system documentation

- Payroll and HR processes

- Any informal arrangements with employees or customers that aren't in writing

| Business Revenue | Typical Transition Period | Seller Compensation | Key Focus Areas |

|---|---|---|---|

| Under $1M | 30 to 60 days | Often built into deal price | Customer introductions, daily operations |

| $1M to $2M | 60 to 90 days | Consulting agreement common | Vendor relationships, staff training |

| $2M to $5M+ | 3 to 12 months | Paid consulting agreement | Strategic relationships, management coaching, systems |

One practical tip: start writing these things down at least 90 days before you expect to close. Doing it in the two weeks after signing is stressful and results in gaps. The more systems you document in advance, the smoother the handoff goes and the faster the buyer gains confidence.

What Happens to Employee Benefits, PTO, and Contracts

This section trips up a lot of sellers because the answer depends heavily on deal structure.

Asset sale vs. stock sale is the key distinction. In an asset sale (the most common structure for small to mid size businesses), the buyer is technically creating a new employment relationship with your employees. They can choose to hire all, some, or none of your team. They're also generally not required to honor accrued PTO or existing employment contracts unless they specifically agree to do so.

In a stock sale, the buyer assumes ownership of the entire legal entity. Existing employment agreements, PTO balances, and benefit obligations generally transfer with the company. This is better for employees but comes with more risk for buyers, which is partly why stock sales are less common at the lower end of the market.

What does this mean practically? Before you make any promises to your team about their benefits, PTO, or job security, talk to your attorney and the buyer. Get clarity on what will be honored and what won't. Then communicate clearly with your team before they find out from someone else.

I've seen deals close where the seller promised employees their PTO would carry over, the buyer disagreed, and the seller ended up writing personal checks to employees to make good on the promise. That situation is entirely avoidable with a clear conversation during due diligence.

Ready to think through what your business might sell for and how to structure the deal? Reach out here and we can walk through your specific situation.

Common Mistakes Sellers Make With Their Team

I've seen the same mistakes over and over. Knowing them doesn't prevent them by itself, but it helps to recognize the pattern before you repeat it.

Telling employees too early. I worked with a seller who told his entire team on day one of listing. Four months later, two key people had left, one customer had been poached, and the business had declined enough that we had to reprice. Confidentiality exists for a reason.

Telling key employees too late. The flip side is sellers who reveal the sale at closing and then act surprised when the operations manager quits out of resentment for being the last to know. Timing the key employee conversation correctly matters.

Making promises you can't keep. Sellers want to ease the anxiety in the room, so they say things like "everyone's job is safe" or "nothing's going to change." If those things aren't true, or if you don't yet know whether they're true, don't say them. Broken promises destroy trust faster than anything else.

A well structured stay bonus combined with a clear non solicitation agreement is often more effective than a non compete that an employee will challenge in court.

Not involving the buyer in employee communication. The buyer is going to be working with these people. Having them participate in the transition announcement, even briefly, gives employees a face for the change and starts the relationship on the right foot.

Ignoring the informal leaders. Every team has someone who isn't in management but whose opinion everyone follows. If that person is anxious or negative about the sale, it spreads. If you can bring them along, the rest of the team tends to follow.

Real World Examples: Transitions That Went Right and Wrong

The Landscaping Company That Kept Every Employee

A landscaping business owner I worked with had 14 full time employees when he decided to sell. His general manager had been with him for 11 years. We structured a deal that included a $35,000 stay bonus for the GM, payable in two installments at 6 months and 12 months post close. The buyer paid it. The GM stayed. Every other employee stayed too, partly because the GM communicated confidence in the new owner from day one. The business sold for $1.1 million and the transition was essentially invisible to customers.

The Medical Spa That Lost Three Key People

A medical spa came to me after a deal fell apart. The owner had been in due diligence with a buyer for three months. During that time, a rumor spread among the staff, likely through the accountant's office. Three of the six estheticians quit, two of them going to a competitor. The original buyer walked. We got a second buyer, but the reduced headcount and revenue drop meant the final price came in $200,000 below the first offer.

The Restaurant Group That Handled It Well

A restaurant owner selling two locations told his two general managers six weeks before closing, after LOI was signed. He offered them each a $20,000 retention bonus, 50% payable at close and 50% at 90 days. He gave them a script to use with staff and scheduled a full team meeting for two weeks before closing. Both GMs stayed, most staff stayed, and the buyer completed the purchase without any pricing adjustments tied to personnel.

The pattern in the success stories: early identification of key people, financial incentives structured properly, honest and clear communication, and a buyer who was willing to show up and be present in the transition.

Putting It All Together: A Timeline for Sellers

Here's a rough timeline you can adapt to your situation:

90+ days before closing: Identify your key employees. Begin documenting roles, processes, and institutional knowledge. Consult your attorney about non solicitation and non compete enforceability in your state.

60 days before closing: Work with your broker and attorney to design the retention plan. Determine which employees will receive stay bonuses and what the amounts will be. Draft the agreements.

30 days before closing: Have the key employee conversation. Present stay bonus agreements if applicable. Get signatures before the general announcement.

2 weeks before closing: Announce to general staff. Have the buyer present if possible. Address questions directly.

At closing and after: Execute transition plan. Begin formal training period. Keep communication channels open.

The businesses that sell well, and whose employees land well, are the ones where the seller treated the team as a core part of the deal, not an afterthought.

Final Thoughts

Your team built this business with you. How you handle this transition is a reflection of how much you value that. Beyond the ethics of it, the practical reality is that a well managed team transition directly affects your sale price, your deal risk, and your reputation in your industry after you exit.

If you're getting ready to sell and you're not sure how to structure these conversations or whether your business is ready, I'd be glad to walk through it with you. Contact me directly and we'll talk through your specific team situation, deal structure, and what buyers in your industry typically expect.

You can also check out our free valuation calculator to get a baseline sense of what your business might be worth before we talk.

Most sellers only do this once. Getting the people part right is just as important as getting the numbers right.

When you're ready to explore selling, tell us about your business and we'll help you plan the transition from day one.

Related Articles

April 16, 2026

Preparing Your Business for Sale: The 12 Month Checklist

The best time to start preparing your business for sale is 12 months out. Here's exactly what to do each quarter.

April 12, 2026

How to Handle Multiple Offers on Your Business

Multiple offers are a great problem to have. But picking the wrong one can cost you months and thousands. Here's how to evaluate them.

April 9, 2026

Best Time of Year to List Your Business for Sale

Timing your listing right can mean more buyers, better offers, and a faster close. Here's what the data says about when to go to market.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.