I've seen more business sales delayed, renegotiated, or completely killed by lease issues than almost any other single factor. And the frustrating part is that most of these problems are preventable if the seller addresses them early enough.

Your lease is one of the most important assets in your business sale, especially if your business depends on its location. A restaurant, retail store, salon, laundromat, or any business where customers come to you is only as valuable as the lease that lets it operate from that spot. Lose the lease and you've potentially lost the business.

But even service businesses that operate from a warehouse or office need to handle the lease transfer properly. Buyers won't close on a business without knowing they have a secure place to operate. And lenders, especially SBA lenders, require proof of an assignable lease or a new lease before they'll fund a deal.

Here's everything you need to know about handling lease transfers when selling your business.

Why the Lease Matters So Much in a Business Sale

Think about it from the buyer's perspective. They're about to spend $300,000, $500,000, maybe $1 million to buy your business. They're going to take on debt, commit their savings, and bet their livelihood on this working out. And the whole thing depends on being able to operate from a specific location under terms they can afford.

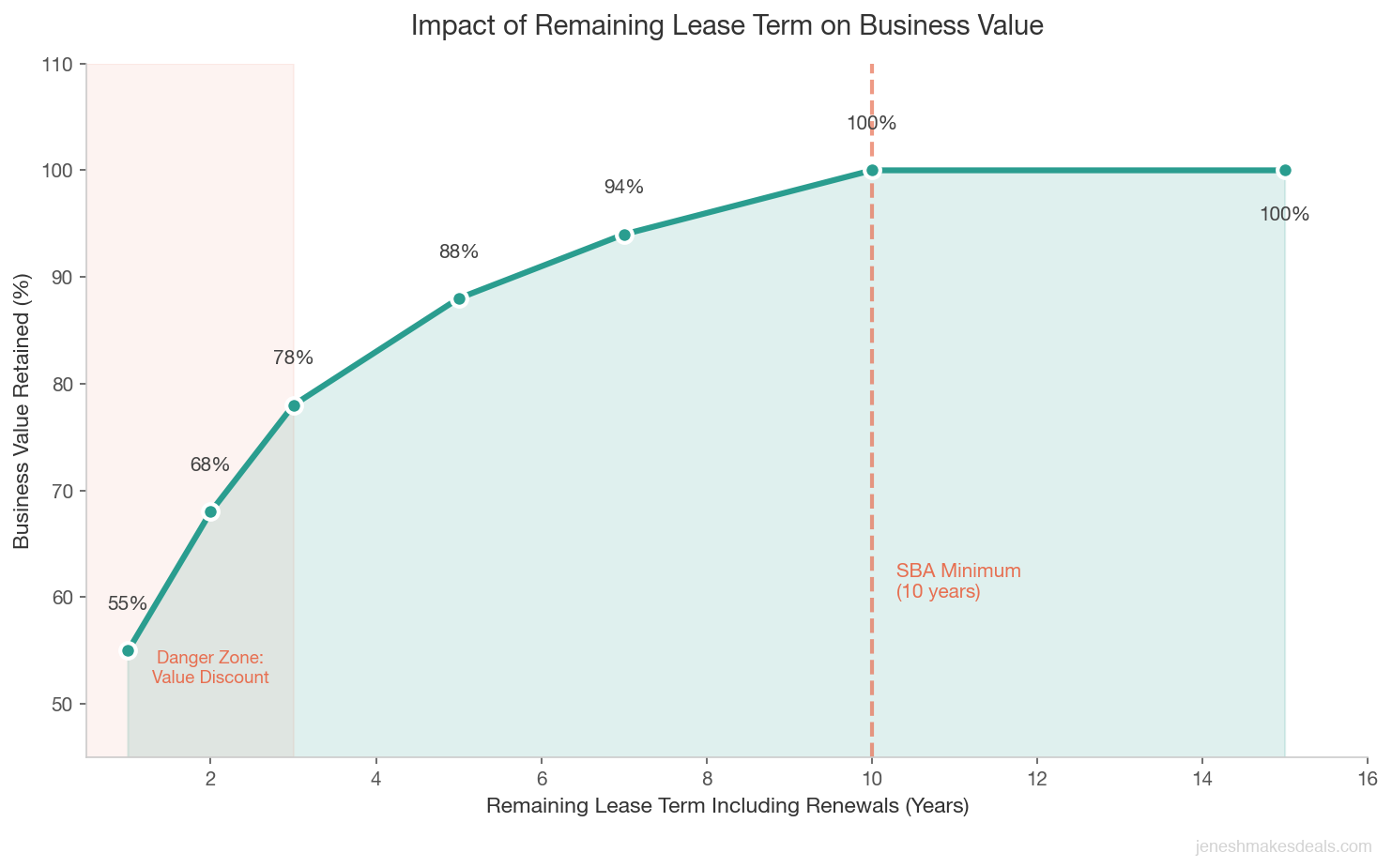

If the lease has only 18 months left with no renewal option, the buyer faces the risk of the landlord raising rent dramatically or not renewing at all. That risk alone can reduce a business's value by 20% to 30% or kill the deal entirely.

If the lease contains restrictions on transfer, the landlord has the power to approve or reject the new tenant. Some landlords use this as a bargaining chip to negotiate higher rent or extract other concessions. I've seen landlords demand a $50,000 "consent fee" just to approve a lease assignment.

And if the lease has provisions that you've never read carefully, there might be hidden clauses about permitted use, personal guarantees, or early termination that create problems during the sale process.

The bottom line: your lease situation directly affects your business value, and you need to address it long before a buyer shows up.

Broker's note: I tell every seller the same thing: start reviewing your lease at least six months before you plan to list. The problems you find early are fixable. The ones you discover during due diligence are deal killers.

Lease Assignment vs New Lease: Understanding Your Options

When you sell your business, the lease can be handled in two main ways. Understanding the difference is important because they have different implications for you, the buyer, and the landlord.

Lease assignment. This is the most common approach. You assign your existing lease to the buyer. The buyer takes over the same terms, same rent, same expiration date, and same renewal options. From the landlord's perspective, they're just getting a new tenant under the existing agreement.

The advantage for the buyer is that they inherit your lease terms, which may be more favorable than what they could negotiate today. If you signed your lease five years ago at $15 per square foot and current market rates are $22 per square foot, that below market lease is a valuable asset.

Most commercial leases require the landlord's written consent before assignment. The lease will typically state the conditions for consent, and in many states, the landlord cannot unreasonably withhold consent. But "reasonably" and "unreasonably" leave a lot of gray area.

New lease. Sometimes the landlord prefers to negotiate a brand new lease with the buyer rather than assign the existing one. This is more common when the current lease is close to expiring or when the landlord wants to update the terms.

A new lease can be good or bad for the deal depending on the terms. If the landlord offers a 10 year lease with reasonable rent increases, that can actually be more attractive to buyers than assuming an older lease with only 2 years remaining. But if the landlord uses this as an opportunity to significantly increase rent, it can blow up the deal economics.

Need help understanding how your lease affects your business value? Contact us for a free consultation and we'll walk you through your specific situation.

How to Review Your Lease Before Listing

Before you put your business on the market, read your lease carefully. Better yet, have your attorney read it. Here are the specific things to look for.

Assignment and transfer clause. This is the most important section. It tells you whether you can assign the lease, under what conditions, and what the landlord can require. Look for language about:

- Whether landlord consent is required (it almost always is)

- Whether the landlord can charge a fee for consent

- Whether you remain liable after assignment (this is common and important)

- Whether there are financial requirements the new tenant must meet

- Whether the landlord has the right of first refusal (the right to take the space back instead of approving the assignment)

Remaining term. How much time is left on the lease? Buyers want at least 3 to 5 years of remaining term, including renewal options. If your lease expires in 18 months with no renewal options, you need to address this before listing.

Renewal options. Does the lease include options to renew? At what rate? An option to renew at fair market value is less valuable than an option to renew at a fixed increase. Know exactly what your renewal terms are.

Personal guarantee. Did you personally guarantee the lease? If so, assignment may not release you from that guarantee. You could remain on the hook for rent even after selling the business. This is a big deal and needs to be addressed in both the lease assignment and the purchase agreement.

Change of use restrictions. Some leases restrict what the space can be used for. If the buyer plans to modify the business concept, this could be an issue. Even if they plan to keep the same business, make sure the permitted use is broad enough to cover future changes.

Exclusivity clauses. Some commercial leases include exclusivity provisions that prevent the landlord from renting to a competitor in the same property. These clauses are valuable and should transfer with the assignment.

CAM charges and escalation. Common area maintenance charges, property taxes, and insurance pass throughs can significantly increase the total cost of the lease. Make sure the buyer understands the full cost, not just the base rent.

When and How to Approach Your Landlord

Timing your conversation with the landlord is critical. Too early and you risk word getting out that you're selling. Too late and the landlord's response can delay or kill the deal.

The general rule: approach the landlord after you have a signed letter of intent (LOI) from a buyer but before you enter the formal due diligence period. This gives you a real buyer to present to the landlord and enough time to resolve any issues before closing.

Key takeaway: Never approach your landlord empty handed. Showing up with a qualified buyer's financial package signals that this is a real transaction, not a hypothetical. Landlords respond better when they see the deal is already in motion.

Some sellers prefer to have a preliminary conversation with the landlord even earlier, perhaps during the preparation phase, without disclosing specific plans. You might say something like, "I'm doing some long term planning and want to understand our options if we ever needed to assign this lease." This can reveal the landlord's general attitude without tipping your hand.

Here's a practical approach to the landlord conversation:

Step 1: Gather the buyer's financial information. Before approaching the landlord, have the buyer prepare a personal financial statement, business plan or resume, and proof of funds or financing commitment. Landlords approve tenants based on financial strength, and presenting a well qualified buyer makes consent much easier to obtain.

Step 2: Submit a formal assignment request. Put it in writing. Include the buyer's qualifications, proposed assignment effective date, and a copy of the relevant lease provisions. Your attorney should draft or review this letter.

Step 3: Respond promptly to landlord questions. The landlord may have questions about the buyer's experience, financial capacity, or business plans. Respond quickly and completely. Delays here delay your closing.

Step 4: Negotiate any new terms. If the landlord wants to modify terms as a condition of consent, negotiate reasonably. Common requests include a security deposit from the buyer, updated insurance requirements, or minor lease modifications. Pick your battles.

Step 5: Get it in writing. The landlord's consent to assignment must be in writing. Don't proceed to closing based on a verbal agreement. Get a signed consent letter or amendment that clearly states the assignment is approved and the terms that apply.

Common Landlord Roadblocks and How to Handle Them

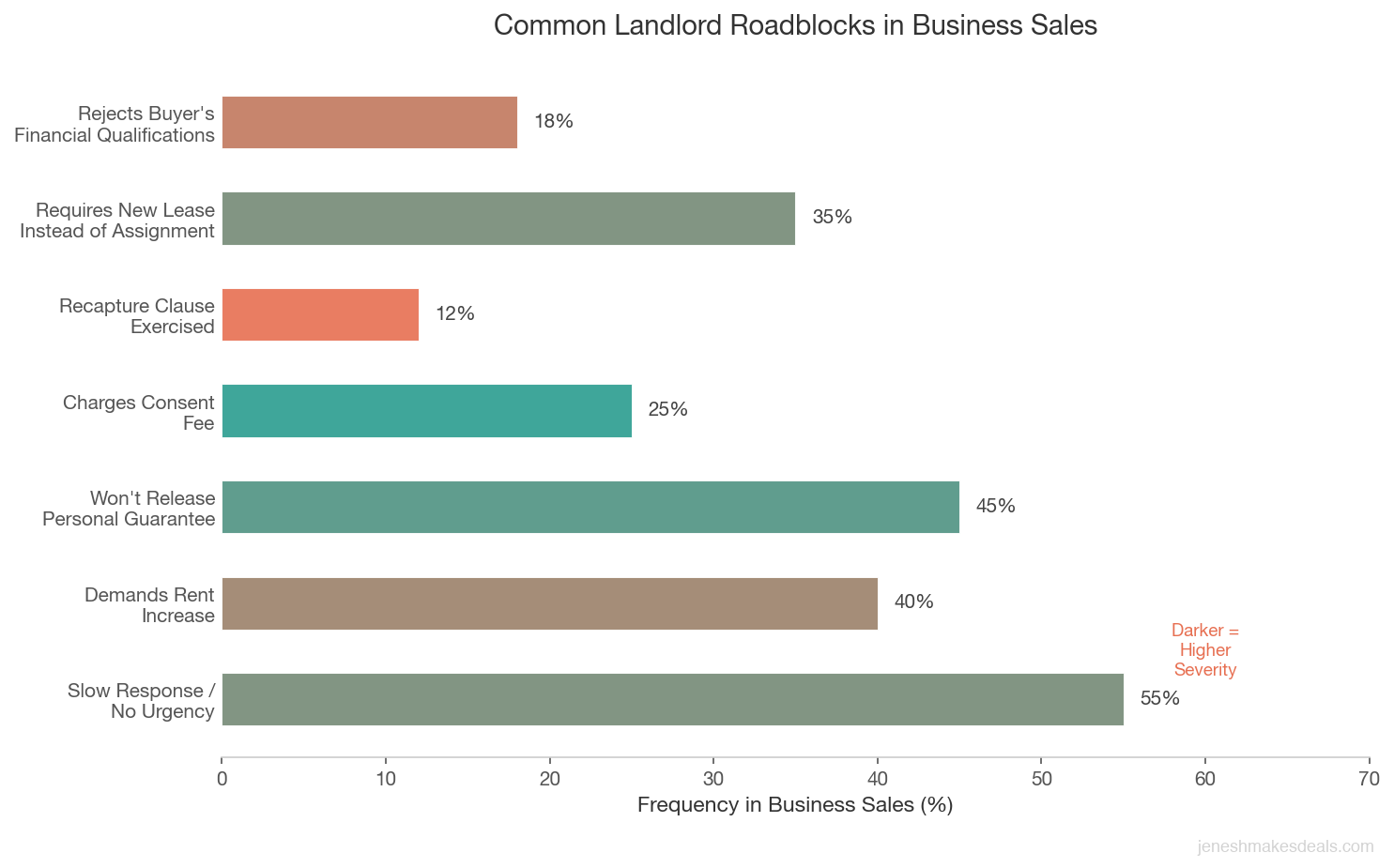

Landlords don't always make this easy. Here are the most common problems and how to deal with them.

The landlord demands higher rent. Some landlords see a business sale as an opportunity to increase rent. If your lease allows assignment, the landlord generally cannot condition consent on a rent increase. But if the lease is silent on this point, or if the landlord is offering a new lease instead of an assignment, you may need to negotiate.

If the rent increase is modest (5% to 10%), it might be worth accepting to keep the deal moving. If it's dramatic (30% or more), it changes the deal economics and you'll need to work with the buyer to determine whether the business still works at the higher rent.

The landlord wants to recapture the space. Some leases include a recapture clause that allows the landlord to take the space back instead of approving an assignment. This is the landlord's way of getting a valuable tenant out so they can re lease at higher rates. If your lease has a recapture clause, understand the timeline and process. Sometimes just knowing the clause exists is enough to negotiate around it.

The landlord is slow to respond. Unfortunately, not all landlords prioritize lease assignments. Some are slow because they're disorganized. Others are slow strategically because they know the sale depends on their approval. Put deadlines in your communications. Follow up consistently. Have your attorney send a formal request referencing the lease provisions that require the landlord to respond within a reasonable time.

The landlord won't release you from the personal guarantee. This is common and often non negotiable from the landlord's side. If the landlord insists that your personal guarantee remain in place even after assignment, negotiate protections in your purchase agreement with the buyer. Specifically, the buyer should indemnify you for any lease obligations arising after the closing date.

The landlord demands a consent fee. Some leases allow the landlord to charge a fee for processing the assignment. If your lease includes this, you'll need to pay it. The question is who pays: you or the buyer. This is negotiable as part of the purchase agreement.

How Lease Issues Affect SBA Financed Deals

About 70% of small business acquisitions involve SBA financing, and SBA lenders have specific requirements about the lease. Understanding these requirements helps you prepare and avoid surprises.

Minimum lease term. SBA lenders generally require a remaining lease term (including renewal options) of at least 10 years or the term of the loan, whichever is greater. If your lease has 4 years remaining with one 5 year renewal option, you have 9 years total, which may not meet the requirement.

Landlord subordination. Some lenders require the landlord to sign a subordination agreement that gives the lender certain rights if the buyer defaults. Not all landlords will agree to this, and it can become a sticking point.

Assignment approval timing. SBA lenders won't fund the loan until the lease assignment is approved in writing. This means any delay from the landlord directly delays your closing. Build this timeline into your expectations.

Lease term negotiation. If the existing lease doesn't meet SBA requirements, you may need to negotiate a lease extension or new lease with the landlord as part of the sale process. This adds complexity but is often achievable with good communication.

Warning for sellers: If your lease term plus renewal options totals less than 10 years, start negotiating an extension with your landlord before going to market. An SBA buyer who can't get financing because of a short lease will walk away, and SBA buyers make up the majority of the small business acquisition market.

Looking for more information about SBA loan requirements? Check out our funding resources for details on what lenders look for.

Protecting Yourself in the Purchase Agreement

Regardless of how smooth the landlord approval goes, there are provisions that should be in your purchase agreement to protect both you and the buyer.

Lease contingency. The purchase agreement should include a contingency that allows the deal to be cancelled if the lease cannot be assigned or a new lease cannot be negotiated on acceptable terms. Both parties need this protection.

Landlord consent deadline. Set a specific date by which landlord consent must be obtained. If the deadline passes without consent, either party should be able to extend or terminate the agreement.

Personal guarantee release. If the landlord won't release your personal guarantee, include an indemnification provision in the purchase agreement. The buyer agrees to cover any lease costs or liabilities that arise after the closing date.

Rent responsibility during transition. Clarify who pays rent during the transition period and what happens if there's a gap between closing and the effective date of the assignment.

Security deposit transfer. Your security deposit should be transferred to the buyer or credited against the purchase price. Make sure the purchase agreement addresses this clearly.

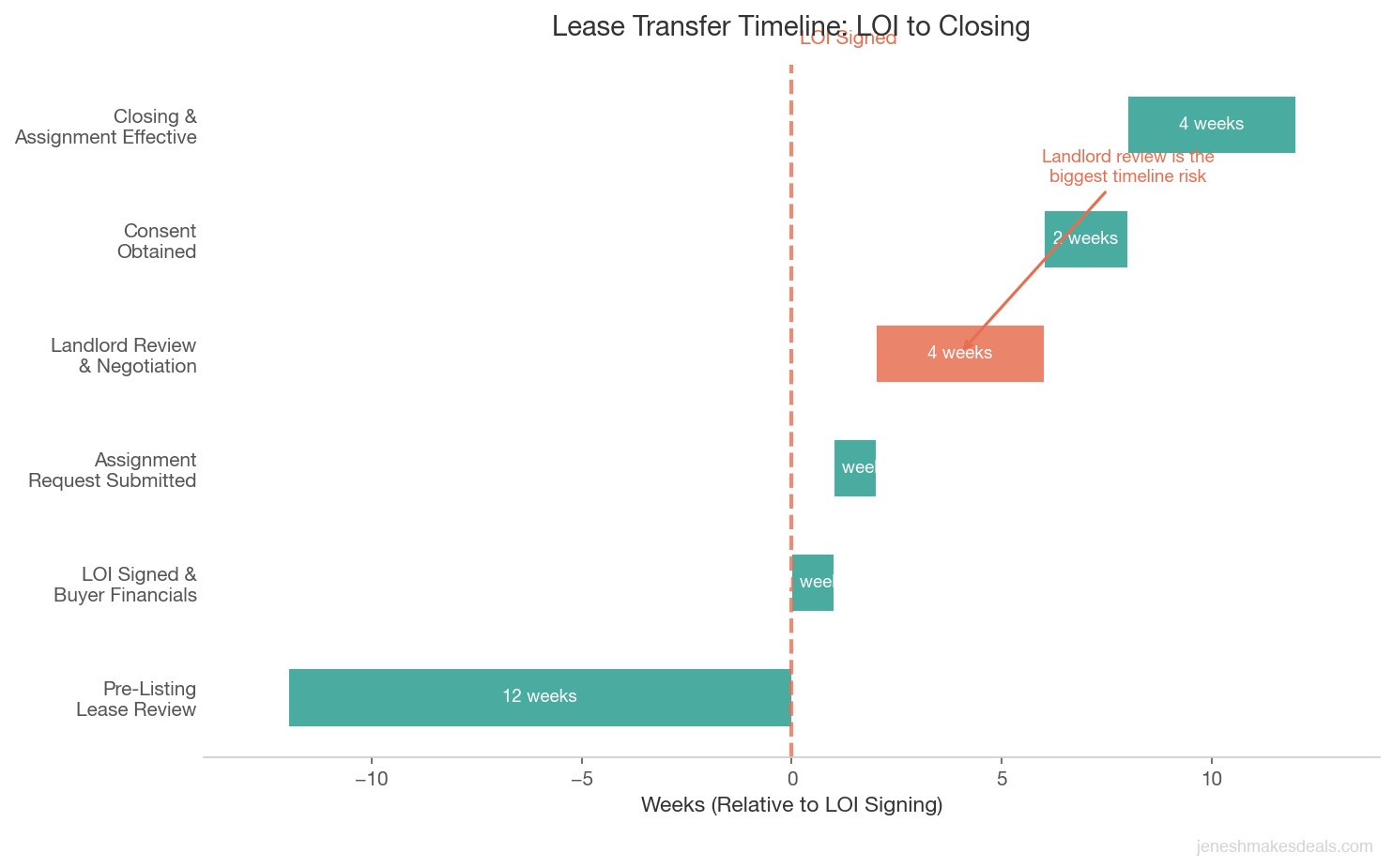

Lease Transfer Timeline: What to Expect

Here's a realistic timeline for the lease transfer process:

| Phase | Timeline | Key Actions |

|---|---|---|

| Pre listing review | 3 to 6 months before listing | Review lease, identify issues, preliminary landlord conversation if needed |

| LOI signed | Day 1 | Begin preparing assignment request and buyer financials |

| Assignment request submitted | Week 1 to 2 | Formal request to landlord with buyer qualification package |

| Landlord review | Week 2 to 6 | Landlord evaluates buyer, asks questions, negotiates terms |

| Consent obtained | Week 4 to 8 | Written consent or assignment agreement signed |

| Closing | Week 8 to 12 | Assignment effective date, deposit transfer, guarantee release (if applicable) |

Total timeline from LOI to lease resolution: 4 to 12 weeks. Build this into your deal timeline, especially if you know your landlord tends to move slowly.

Special Situations

Some lease scenarios are more complex and require additional attention.

Multiple locations. If your business has several leased locations, each lease needs to be addressed separately. Different landlords, different terms, different timelines. Coordinate early and track each one independently.

Sublease situations. If you're subleasing your space from another tenant rather than directly from the landlord, the transfer is more complicated. You need consent from both the master tenant and the property owner. Start this process early.

Month to month leases. If your lease has expired and you're operating month to month, you have no guarantee of continued occupancy. This is a major red flag for buyers. Before listing, try to negotiate a new lease with a meaningful term.

Ground leases. If you own the building but lease the land, the ground lease needs to transfer or at least allow the building sale. Ground lease assignments can be complex and often require different legal analysis than standard commercial lease assignments.

The Bottom Line

Your lease is one of the most valuable, and most vulnerable, assets in your business sale. Handle it proactively and strategically, and it becomes a selling point that strengthens your deal. Ignore it or handle it poorly, and it can delay your closing by months or kill the deal entirely.

Start by reading your lease carefully. Understand the assignment provisions. Know your landlord's likely concerns. And address any problems long before a buyer is sitting across the table asking questions you can't answer.

The sellers who handle lease transfers best are the ones who treat the landlord as a stakeholder in the deal, not an adversary. Communicate early, present a qualified buyer, and negotiate in good faith. Most landlords want a reliable tenant paying rent on time. If you can show them that's what the buyer will be, the approval process usually goes smoothly.

Ready to sell your business? Contact us for a free consultation and we'll help you evaluate your lease situation and prepare for a smooth transfer.

Want to see what your business is worth? Use our free business valuation calculator to get a quick estimate based on your industry.

For a step by step walkthrough of the entire selling process, including lease and contract transfers, download our free Complete Guide to Selling Your Business in 2026.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.