Selling a business is one of those things that has to happen quietly. The moment your employees find out you're selling, your best people start updating their resumes. The moment your competitors find out, they start calling your customers. And the moment your customers find out, they start wondering if they should find a new vendor.

I've seen deals fall apart because word got out too early. A restaurant owner told one too many people, and within a week the entire staff knew. Two key employees quit before the deal even closed. The buyer backed out because the business was no longer what they thought they were buying.

So how do you find someone willing to pay you hundreds of thousands or millions of dollars for your business while keeping the whole thing under wraps? That's what I'm going to walk you through in this post.

Why Confidentiality Matters So Much in a Business Sale

Let me put this in perspective. When a business goes up for sale, the information that gets shared with potential buyers includes revenue numbers, profit margins, customer lists, employee details, vendor contracts, and operational processes. This is essentially the playbook for running your business.

If that information gets into the wrong hands, the damage can be severe. A competitor could use your financial data to undercut your pricing. A key employee could leave and take clients with them. Customers could start looking for alternatives because they're worried about a change in ownership.

The average business sale takes 6 to 12 months from listing to closing. That's a long time to keep a secret. And during that time, you need to be running the business as if nothing is happening. Revenue needs to stay strong. Employees need to stay engaged. Customers need to stay loyal.

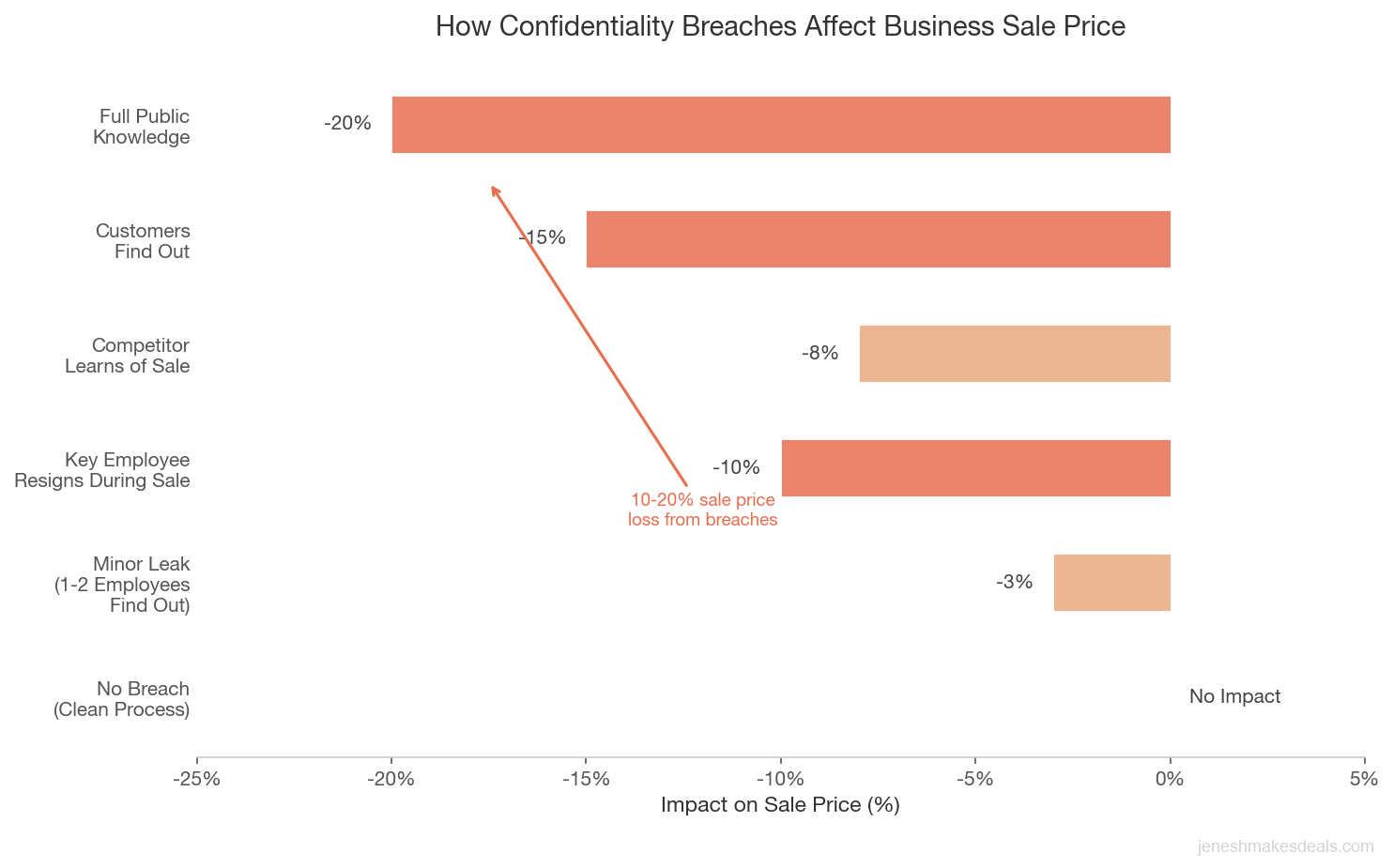

If any of those things slip because confidentiality was breached, the value of your business drops. I've seen sellers lose 10% to 20% of their sale price because the business deteriorated during the sales process.

The number one rule I give every seller on day one: run your business like you're going to own it for the next 20 years. The moment you mentally check out, people notice. And when people notice, they start asking questions you're not ready to answer.

Using a Business Broker to Shield Your Identity

The most common way sellers protect confidentiality is by working with a business broker. A broker acts as a buffer between you and the buyer pool. Your business gets marketed without your name, your company name, or any identifying details attached to it.

Here's how it typically works. The broker creates a listing that describes the business in general terms. Something like "established HVAC company in the Southeast with $1.2 million in annual revenue and $350,000 in seller's discretionary earnings." There's enough information for a buyer to determine if they're interested, but not enough to identify the specific business.

When a potential buyer wants to learn more, they have to sign a non disclosure agreement (NDA) before receiving any additional information. This creates a legal obligation to keep everything they learn confidential.

I always recommend working with a broker who has experience in your specific industry. They'll know how to describe your business in a way that attracts serious buyers without giving away too much. They also have established networks of pre qualified buyers who are already looking to acquire businesses like yours.

Thinking about selling your business? Contact us for a free consultation and we'll walk you through how we keep the entire process confidential from start to finish.

Creating a Blind Profile That Attracts the Right Buyers

A blind profile is your first marketing document. It's a one to two page summary of your business that gives enough information to generate interest without revealing who you are.

A good blind profile includes:

- Industry and general location (region, not specific city)

- Annual revenue range (not exact numbers)

- Years in business (approximate)

- Number of employees (approximate range)

- Type of ownership (owner operated vs. management in place)

- Reason for selling (retirement, new opportunity, etc.)

- Asking price or price range

- Growth opportunities (without giving away trade secrets)

What you should never include in a blind profile:

- Company name or DBA

- Exact address

- Names of customers or vendors

- Specific proprietary processes

- Exact employee count if it's very specific to your business

- Any photos that could identify the location

I've seen blind profiles that were so vague they attracted no interest, and I've seen profiles that gave away too much and compromised confidentiality within days. The key is finding that middle ground where you're sharing enough to get a qualified buyer excited but not enough for anyone to figure out who you are.

The Role of Non Disclosure Agreements

An NDA is not just a formality. It's your primary legal protection during the sales process. Every single person who receives detailed information about your business should sign one before getting access.

A solid NDA for a business sale should cover these key points:

- Definition of confidential information. This should be broad enough to include financial data, customer information, employee details, trade secrets, and any other sensitive information about the business.

- Duration of the obligation. Most business sale NDAs have a confidentiality period of 2 to 3 years after signing.

- Permitted use. The information can only be used for evaluating the potential purchase of the business. It cannot be shared with third parties, used to compete, or disclosed to anyone who doesn't need it for the evaluation.

- Return or destruction of materials. If the buyer decides not to proceed, they must return or destroy all confidential information.

- Remedies for breach. This section should specify that a breach of the NDA could result in legal action, including injunctive relief and monetary damages.

One thing I'll mention is that an NDA is only as strong as your willingness to enforce it. Most buyers who sign NDAs are legitimate and will respect the agreement. But if someone does violate it, you need to be prepared to take legal action. That's why it's important to have an attorney review your NDA before you start using it.

Qualifying Buyers Before Sharing Sensitive Information

Not every interested party deserves to see your financial statements. Before sharing detailed information about your business, you should qualify potential buyers to make sure they're serious and capable of completing the purchase.

Here's what I look for when qualifying a buyer:

Financial capacity. Can they actually afford your business? I ask for proof of funds or a pre qualification letter from a lender. If someone can't demonstrate that they have the financial resources to complete the deal, there's no reason to share your sensitive information with them.

Relevant experience. Do they have experience in your industry or in running a business? While this isn't always a requirement, buyers with relevant experience are more likely to close the deal. They understand the industry, they know what they're looking at in the financials, and they're less likely to get cold feet.

Motivation and timeline. Why are they looking to buy a business, and when do they want to close? Someone who's casually browsing is very different from someone who's ready to make an offer in the next 60 days. I prioritize buyers who have clear timelines and strong motivations.

Track record. Have they been through this process before? Repeat buyers often move faster and are easier to work with. First time buyers can be great too, but they may need more hand holding, which means more people get involved and more opportunities for leaks.

The qualification process isn't just about protecting confidentiality. It's also about not wasting your time on buyers who aren't a good fit.

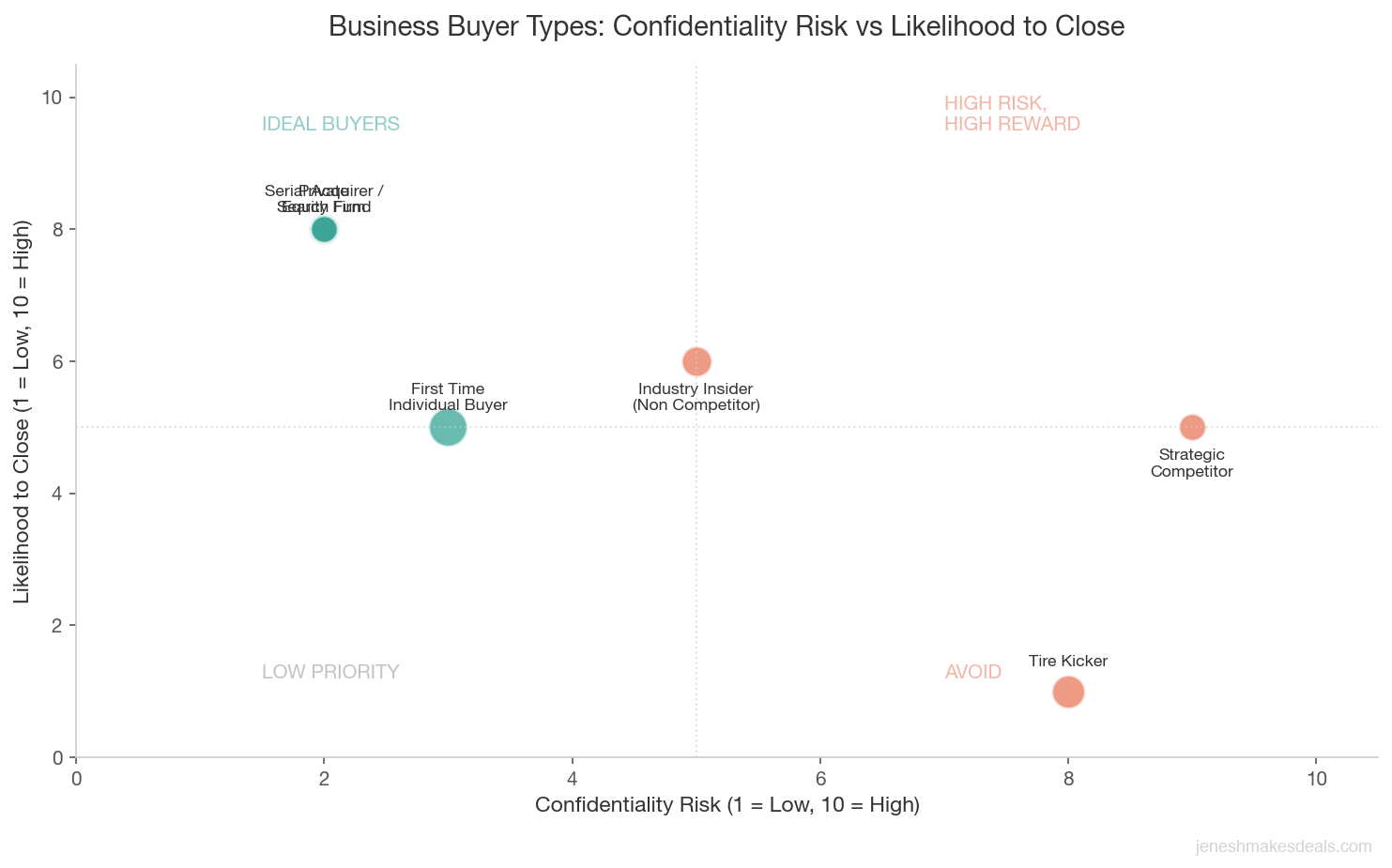

| Buyer Type | Confidentiality Risk | Likelihood to Close | Information to Share Before NDA | Key Screening Question |

|---|---|---|---|---|

| Strategic competitor | High, may use intel against you | Moderate | Blind profile only, no financials | Do they have a history of closed acquisitions? |

| First time individual buyer | Low | Moderate | Blind profile, general industry data | Can they show proof of funds or SBA pre qualification? |

| Serial acquirer or search fund | Low | High | Blind profile, summary financials after NDA | What is their acquisition timeline and funding source? |

| Private equity firm | Low | High | Blind profile, teaser deck after NDA | Does your business fit their stated investment criteria? |

| Industry insider (non competitor) | Moderate | Moderate to High | Blind profile, general terms | Are they in a different geographic market or adjacent niche? |

| Tire kicker or unqualified browser | High, no accountability | Very Low | Nothing beyond blind profile | Can they provide any financial documentation at all? |

Be especially cautious with buyers who are already in your industry and your market. They may be legitimate acquirers, but they could also be competitors looking for intelligence. Always verify financial capacity before sharing anything beyond the blind profile.

Using a Confidential Information Memorandum

Once a buyer has signed an NDA and passed your qualification process, the next step is usually sharing a Confidential Information Memorandum, also called a CIM or offering memorandum. This is a detailed document that gives the buyer everything they need to decide whether to make an offer.

A typical CIM includes:

- Detailed financial statements for the past 3 to 5 years

- Tax returns

- A description of the business, its history, and its market position

- Information about the management team and employees

- Details about the customer base and vendor relationships

- Growth opportunities and risks

- The asking price and deal structure

The CIM is where the real confidential information lives. This is the document that, if leaked, could cause the most damage. That's why it's critical to only share it with qualified, NDA signed buyers.

Some brokers watermark their CIMs with the buyer's name so that if the document is leaked, they can trace it back to the source. I think this is a smart practice, and I recommend it for any deal.

Want to understand what your business might sell for? Try our free business valuation calculator to get a quick estimate based on your industry multiples.

Controlling Information Flow During Due Diligence

Due diligence is the riskiest phase for confidentiality. The buyer and their team of advisors, including accountants, attorneys, and lenders, will be asking for detailed documents and potentially visiting your business.

Here are some strategies for maintaining confidentiality during due diligence:

Use a virtual data room. Instead of emailing documents back and forth, set up a secure online data room where you can upload documents and control who has access. Most data rooms have features like watermarking, download restrictions, and activity tracking that help you monitor who's viewing what.

Limit physical visits. If the buyer needs to visit your location, schedule it during off hours when employees aren't around. If that's not possible, introduce them as a consultant, insurance inspector, or some other plausible cover story. I know this feels deceptive, but it's standard practice in business sales.

Control the narrative with employees. At some point during due diligence, the buyer may want to meet key employees. This is one of the trickiest parts of the process. I recommend delaying this as long as possible, ideally until after a purchase agreement is signed and the deal is likely to close. When you do introduce the buyer to employees, frame it positively and reassure them about their job security.

Separate sensitive data. Not every document the buyer asks for needs to include customer names or employee personal information. Where possible, redact identifying details and provide summary data instead. A buyer can evaluate customer concentration without knowing the actual customer names until later in the process.

Establish a single point of contact. Limit the number of people involved in the sale. The fewer people who know, the less likely a leak. Designate one person, usually you or your broker, as the primary contact for all buyer communications.

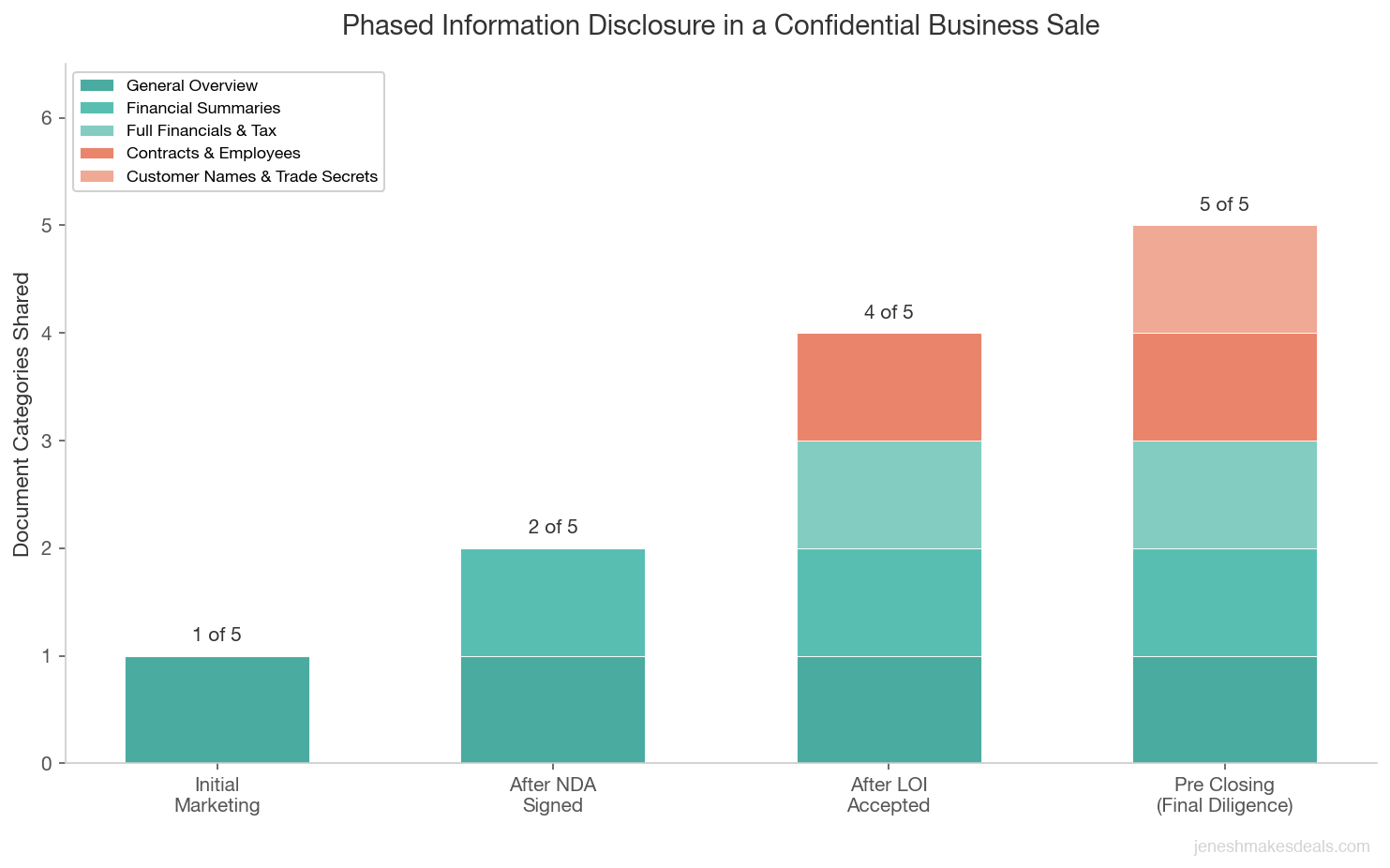

| Sale Stage | What the Buyer Sees | Who Knows About the Sale | Primary Confidentiality Tool |

|---|---|---|---|

| Initial marketing | Blind profile with no identifying details | Broker and seller only | Anonymous listing, no company name |

| Buyer inquiry | Blind profile plus general Q&A through broker | Broker, seller, prospective buyer | Signed NDA before any details shared |

| Qualification | Proof of funds request, background screening | Broker, seller, qualified buyer | Financial verification before CIM access |

| CIM review | Full financials, operations, customer data | Broker, seller, qualified buyer, buyer's advisor | Watermarked CIM, virtual data room |

| Due diligence | Detailed documents, site visits, employee info | Broker, seller, buyer, buyer's legal and accounting team | Redacted documents, off hours visits, single point of contact |

| Post signing (pre close) | Key employee introductions, vendor notifications | Inner circle plus select employees and vendors | Purchase agreement with confidentiality clause |

Digital Security During the Sales Process

In today's world, confidentiality breaches don't just happen through word of mouth. Digital security is a real concern during a business sale.

Here are some basic but important precautions:

- Use encrypted email for all communications about the sale. Standard email is not secure enough for sensitive financial documents.

- Don't discuss the sale on your regular business phone or email. Set up a separate email address and phone number for deal related communications.

- Be careful with cloud storage. If you're uploading documents to a shared drive, make sure the permissions are set correctly and that only authorized people have access.

- Watch your browser history and search activity. If you're researching business valuations or contacting brokers from your office computer, anyone who accesses that computer could see what you've been doing.

- Secure your physical documents. If you've printed any sale related documents, keep them locked up. Don't leave them on your desk or in a common area.

These might seem like small things, but I've seen deals where confidentiality was compromised because someone left a document on a printer or sent an email from the wrong account.

Confidentiality doesn't fail because of one big mistake. It fails because of a dozen small ones. A browser tab left open, an email sent from the wrong account, a phone call taken at the office. Treat every piece of deal related communication like it could end up on your competitor's desk, because it might.

What to Do If Confidentiality Is Breached

Despite your best efforts, breaches can happen. An employee overhears a phone call. A buyer mentions something to a mutual contact. A document gets forwarded to someone who wasn't supposed to see it.

If confidentiality is breached, here's how to handle it:

Assess the damage immediately. Who knows? What do they know? How far has the information spread? The answers to these questions will determine your response.

Address it directly with employees. If your employees have found out, don't try to deny it. That will only make things worse. Instead, get ahead of the narrative. Explain that you're exploring options for the business's future, that nothing is certain, and that their jobs are a top priority in any transition. Reassure them that you'll keep them informed as things develop.

Talk to your customers. If key customers have found out, reach out to them personally. Reassure them that any transition will be smooth and that the quality of service they've come to expect will continue under new ownership.

Review your legal options. If the breach was caused by someone who signed an NDA, you may have grounds for legal action. Consult with your attorney about your options.

Adjust your strategy. A breach doesn't necessarily mean the deal is dead. But it may mean you need to move faster, adjust your asking price, or change your approach. Work with your broker to assess the impact and adapt.

Ready to sell your business the right way? Contact us for a free consultation and we'll help you build a confidential marketing strategy that protects your business throughout the entire process.

Working With Professional Advisors Who Understand Discretion

Your team of advisors during a business sale typically includes a broker, an attorney, an accountant, and sometimes a financial advisor or wealth planner. Every single one of these people needs to understand that confidentiality is non negotiable.

When selecting your advisory team, ask these questions:

- How do you handle confidential client information?

- What systems do you use to protect sensitive documents?

- Who on your team will have access to my deal information?

- Can you provide references from past clients who can speak to your discretion?

I've worked with attorneys who casually mentioned deals to colleagues, and I've worked with accountants who were incredibly tight lipped. The difference matters. Your advisors are an extension of your confidentiality strategy, and a weak link in that chain can cause serious problems.

Also, make sure your advisory agreements include confidentiality clauses. This isn't just about trust. It's about creating legal obligations that protect you.

Timing the Market While Keeping Things Quiet

One of the challenges of a confidential sale is that you can't market the business as aggressively as you might want to. You can't put a "For Sale" sign on the building. You can't post about it on social media. You can't tell your industry contacts that you're looking for a buyer.

This means the sales process may take longer than a non confidential sale. The buyer pool is smaller because you're relying on targeted outreach rather than broad marketing.

Here are some ways to speed things up without compromising confidentiality:

- Work with a broker who has an active buyer database. Good brokers have hundreds or thousands of pre qualified buyers already in their network. They can reach out to potential matches without ever publicly listing your business.

- Target strategic buyers. Companies in your industry that might benefit from acquiring your business can be approached directly by your broker under strict confidentiality.

- Consider private equity. PE firms are always looking for acquisition targets, especially in industries like HVAC, plumbing, landscaping, and professional services. They're accustomed to confidential deal processes and typically move quickly.

- Use industry specific marketplaces. Some industries have private listing services that cater specifically to business buyers and sellers. These platforms require NDA signatures before revealing any details.

The key is to balance speed with secrecy. You want to find the right buyer as quickly as possible, but not at the expense of confidentiality.

Common Mistakes That Blow Confidentiality

After working on dozens of deals, I've seen the same mistakes over and over. Here are the most common ways sellers accidentally reveal that their business is for sale:

Telling "just one person." There's no such thing as telling just one person. Everyone who finds out will tell at least one other person. Within a week, half your industry knows.

Being careless with documents. Leaving financial printouts on your desk. Forwarding emails from your business account. Using your office printer for sale related documents. These are small things that add up.

Changing your behavior. If you suddenly start leaving early, delegating everything, and acting detached from the business, people will notice. Keep running the business the same way you always have.

Not vetting buyers properly. Some "buyers" are actually competitors fishing for information. Others are tire kickers with no real intention or ability to buy. Qualifying buyers before sharing anything is essential.

Using social media carelessly. Connecting with business brokers on LinkedIn. Joining "businesses for sale" groups. Liking posts about selling a business. People notice these things.

Talking to the wrong advisors. Not every accountant or attorney understands the confidentiality requirements of a business sale. Make sure your advisors are experienced in M&A transactions.

The Bottom Line

Finding a buyer for your business without compromising confidentiality is absolutely possible, but it requires planning, discipline, and the right team. Start by working with an experienced broker who can market your business anonymously. Use NDAs and buyer qualification processes to control who gets access to your information. Set up secure systems for sharing documents. And above all, keep running your business like you plan to own it forever.

The best deals happen when the business is still performing at its peak. And the business only performs at its peak when employees, customers, and competitors don't know it's for sale.

Need help figuring out what your business is worth? Use our free business valuation calculator to get a quick estimate before you start the selling process.

Ready to explore your options? Contact us for a free consultation and let's talk about how to sell your business confidentially.

Related Articles

April 29, 2026

Selling a Franchise Business vs an Independent Business

Selling a franchise is a fundamentally different process than selling an independent business. Here is what every franchise owner needs to know.

April 21, 2026

What Is a Management Buyout and Is It Right for Your Business?

A management buyout lets your team buy the business. Learn how MBOs work, what they cost, and when they make sense for sellers.

April 13, 2026

How to Find the Right Business Broker for Your Industry

Not all brokers know your industry. Here's how to find one who actually understands your business and can get you top dollar.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.