The sale isn't over when you sign the closing documents. In many ways, it's just beginning.

I've watched sellers spend months finding the right buyer, negotiating the perfect price, and getting through due diligence without a hitch. Then the deal closes, and everything falls apart in the first 60 days because there was no transition plan. Customers leave. Key employees quit. The buyer calls their attorney. Suddenly that $1.2 million sale is the subject of an earnout dispute, and everyone's pointing fingers.

A business transition plan is the document that prevents all of that. It spells out exactly how you'll hand the business over to the new owner, who's responsible for what, and how long you'll stick around to make sure the wheels don't come off. It's one of the most important parts of any business sale, and most sellers treat it as an afterthought.

Let me walk you through how to build a transition plan that actually works. This is based on hundreds of deals I've been involved in, and the patterns I've seen separate smooth transitions from total disasters.

Why Transition Plans Matter More Than Most Sellers Realize

Here's a number that should get your attention: buyers will discount their offer by 10% to 20% when there's no clear transition plan in place. I've seen it happen over and over again.

Think about it from the buyer's perspective. They're about to write a check for $800,000 to buy your business. They know the business works because of you, your relationships, your knowledge, your reputation. Without a plan for transferring all of that, they're basically hoping everything stays the same after you leave. That's a massive risk, and smart buyers price that risk into their offer.

A deal I worked on last year is a perfect example. The seller owned a commercial cleaning company doing $1.4 million in revenue. The business had great margins and a stable customer base. But when the buyer asked about the transition plan, the seller said, "I'll be around for a couple weeks if you need anything." The buyer's initial offer dropped from $950,000 to $780,000 because of that answer alone. The buyer was worried that the seller's relationships with building managers were the entire business, and without a proper handoff, those contracts would evaporate.

We ended up building a detailed 90 day transition plan. The buyer came back to $920,000. That transition plan was worth $140,000 in sale price.

A transition plan is not a courtesy to the buyer. It is a pricing tool. Every hour you spend documenting processes, introducing customers, and training the new owner has a direct dollar value attached to it. I tell every seller the same thing: if you want to protect your sale price, protect the transition.

Beyond the price impact, a weak transition plan creates legal risk. Most purchase agreements include provisions that tie a portion of the sale price to successful transition metrics. If you don't meet those benchmarks, you could lose money through earnout clawbacks or indemnification claims. I've seen sellers lose $50,000 to $200,000 in post closing disputes that a solid transition plan would have prevented.

Thinking about selling your business? Start by understanding what it's worth with our free valuation calculator.

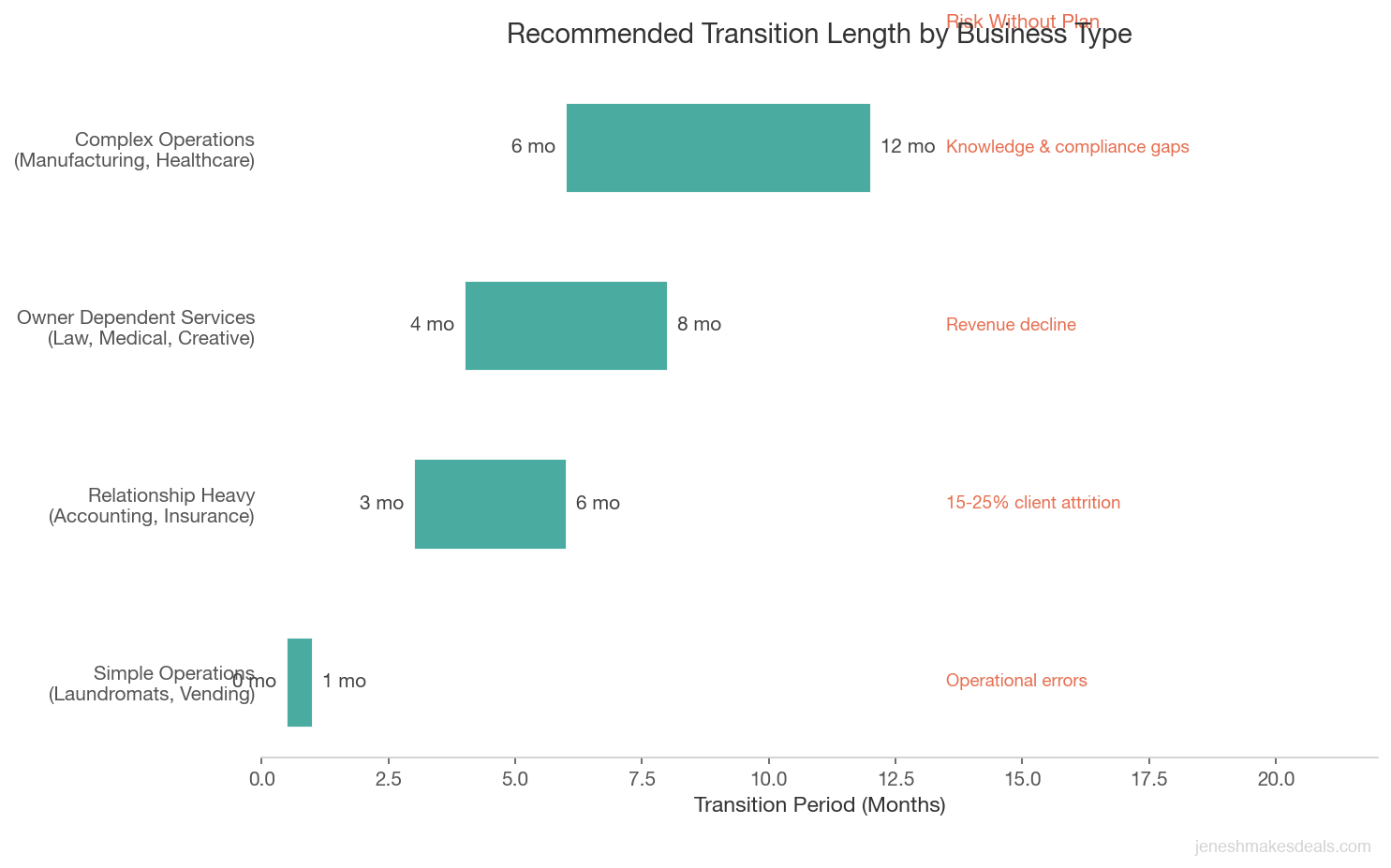

How Long Should the Transition Period Last?

Not every business needs the same transition timeline. The length depends on how complex your operation is and how dependent the business is on your personal involvement. Here's a general breakdown based on what I see in practice.

| Business Type | Transition Length | Examples | Primary Risk Without Plan |

|---|---|---|---|

| Simple operations | 2 to 4 weeks | Laundromats, vending routes, ecommerce stores | Operational errors from missed procedures |

| Relationship heavy businesses | 3 to 6 months | Accounting firms, insurance agencies, consulting | Client attrition of 15% to 25% or more |

| Complex operations | 6 to 12 months | Manufacturing, healthcare, construction | Loss of institutional knowledge, compliance gaps |

| Owner dependent service businesses | 4 to 8 months | Law practices, medical offices, creative agencies | Revenue decline as clients follow the seller |

Simple businesses (2 to 4 weeks): These are businesses with straightforward operations, minimal customer relationships, and documented processes. Think laundromats, vending routes, or ecommerce stores with established supply chains. The new owner can learn the systems quickly because the business doesn't rely on the seller's personal touch.

Relationship heavy businesses (3 to 6 months): If your business depends on client relationships, you'll need more time. This includes accounting firms, insurance agencies, marketing agencies, consulting practices, and any B2B service business where clients know you by name. The biggest risk here is client attrition, and you can't rush personal introductions.

Complex operations (6 to 12 months): Manufacturing companies, healthcare practices, construction firms, and businesses with specialized knowledge or regulatory requirements often need the longest transitions. There's too much institutional knowledge in the owner's head, and it takes months to transfer that to a new owner and their team.

I had a client who owned a specialty manufacturing business. He'd been running it for 22 years. He knew every machine's quirks, every supplier's contact, every customer's preferences. We structured a 9 month transition, and honestly, it could have been longer. The first 3 months were just him documenting processes that existed only in his head.

The transition length also affects your sale price. Buyers will typically pay more when the seller commits to a longer transition, because it reduces their risk. A seller who commits to 6 months of support is more valuable than one who's out the door in 2 weeks.

The Four Pillars of a Good Transition Plan

Every effective transition plan covers four areas. Miss any one of them, and you're leaving gaps that can hurt the buyer and cost you money. These are the pillars I build every transition plan around.

1. Customer introductions and retention. This is the number one concern for almost every buyer I work with. Customers are the business. If they leave when you leave, the buyer just paid full price for a fraction of the revenue.

2. Employee retention and communication. Your employees are the second most important asset. If key staff members quit during the transition, the buyer loses operational capacity and institutional knowledge at the worst possible time.

3. Vendor and supplier relationships. These relationships often come with favorable credit terms, volume discounts, and priority service that took years to build. They need to be transferred properly.

4. Operational knowledge transfer. This is everything in your head that isn't written down. The workarounds, the shortcuts, the seasonal patterns, the things you just know after years of running the business.

Let's dig into each one.

Customer Transition: How to Introduce the New Owner Without Losing Accounts

Customer attrition is the biggest fear buyers have, and for good reason. Studies from the International Business Brokers Association show that businesses lose an average of 10% to 15% of their customer base during an ownership transition. For relationship heavy businesses, that number can climb to 25% or higher if the transition is handled poorly.

Your customers didn't sign up for a new owner. They signed up for you, your responsiveness, your reliability, your way of doing things. The introduction process is where you transfer that trust. Rush it, and you're handing the buyer a business with a ticking clock on its revenue.

Here's the approach I recommend to every seller I work with.

Personal meetings with top accounts. Your top 10 to 20 accounts (the ones that represent 60% to 80% of your revenue) deserve face to face meetings. Schedule a lunch or coffee with each one. Bring the new owner. Frame the conversation around continuity: "The business is going to keep running the same way, and I wanted you to meet the person who's going to take it to the next level." Don't apologize for selling. Don't make it seem like you're abandoning them. Position it as a positive change.

One of my sellers owned a staffing agency. She had 14 major clients that accounted for 72% of her revenue. Over a 6 week period, she personally introduced the buyer to every single one. She didn't just do a quick handshake. She spent 30 to 60 minutes with each client, reviewing their account history, their preferences, and any open issues. The result: zero client attrition in the first year after the sale.

Joint phone calls for mid tier accounts. For clients who are important but don't warrant an in person visit, schedule 15 to 20 minute phone calls. You call the client, introduce the new owner, and let them have a brief conversation. This personal touch goes a long way.

Transition letters for smaller accounts. For your remaining customer base, send a professionally written letter (on company letterhead) announcing the transition. The letter should emphasize continuity of service, introduce the new owner by name, and provide their contact information. Do not send a mass email blast. Make it feel personal, even if it's a template.

The timing matters. Don't announce the transition too early. If you tell customers 3 months before closing, some of them will start shopping for alternatives immediately. The best approach is to begin introductions in the 2 weeks before closing and continue through the first month after.

Create a customer knowledge document. For each major account, write a one page summary that includes their order history, communication preferences, key contacts, any special pricing or terms, and important dates (contract renewals, seasonal peaks). This document is gold for the new owner.

Employee Transition: Keeping Key Staff Through the Ownership Change

Employees are scared when a business sells. They're worried about layoffs, pay cuts, new management styles, and changes to their roles. If you don't address those fears proactively, your best people will start updating their resumes the day the sale is announced.

Identify key employees early. Before the sale even closes, make a list of the 3 to 5 employees who are critical to the business. These are the people whose departure would cause real operational problems. The buyer needs to know who these people are.

Retention bonuses. The most effective tool for keeping key employees is a simple retention bonus. Typical structures I see: $5,000 to $25,000 per key employee, paid out at 6 or 12 months after the sale. The money usually comes from the buyer's budget, but sometimes it's split between buyer and seller. Either way, it's cheap insurance. Losing a key employee and having to recruit, hire, and train a replacement costs 50% to 200% of that person's annual salary.

Communication timing and messaging. Don't tell employees about the sale until you have a signed purchase agreement and are within 1 to 2 weeks of closing. The longer the gap between announcement and closing, the more anxiety builds. When you do tell them, be honest. Explain that the new owner is committed to the team and the business. Introduce the buyer in person. Let employees ask questions.

I've seen sellers make the mistake of telling one trusted employee early, assuming they'll keep it quiet. They almost never do. Within a week, the entire staff knows, and half of them are panicking. Control the narrative by controlling the timing.

Role clarity from day one. Employees need to know, immediately, who they report to after the sale. Will you still be around? For how long? What decisions does the new owner make versus what stays the same? Ambiguity creates anxiety, and anxious employees leave.

Non solicitation protections. Your purchase agreement should include a clause preventing you from hiring away employees after the sale. This protects the buyer and is standard in most deals. Typical terms are 2 to 3 years.

Want to make sure your business is positioned for the best possible sale? Schedule a free consultation to discuss your exit strategy.

Vendor and Supplier Relationships: Transferring What Took Years to Build

Your vendor relationships are more valuable than most sellers realize. That net 60 payment term you negotiated with your main supplier? The priority scheduling you get from your key contractor? The volume discount that saves you $40,000 a year? None of that transfers automatically.

Make a complete vendor list. Document every vendor and supplier relationship, including contact names, account numbers, credit terms, volume commitments, and contract expiration dates. I recommend organizing this by importance: critical vendors (without them, operations stop), important vendors (significant cost or quality impact), and standard vendors (easily replaceable).

Personal introductions for critical vendors. Just like with customers, your most important vendor relationships deserve a personal introduction. Call your main suppliers, explain the transition, and introduce the new owner. Vendors want to know they'll still get paid and that the relationship will continue.

Contract assignments. Review every vendor contract to see if it includes an assignment clause. Many contracts require the vendor's written consent before they can be transferred to a new entity. Start this process early because some vendors take weeks to process assignment requests. If a vendor won't assign the contract, the buyer may need to negotiate a new agreement, which could mean worse terms.

Credit term negotiation. The new owner probably won't get the same credit terms you have on day one. If you've been getting net 60 because of a 15 year relationship and a strong payment history, the vendor might put the new owner on COD or net 15 until trust is established. Prepare the buyer for this and help them negotiate the best starting terms possible.

Introduce key contacts. Vendors are relationships, not just contracts. Make sure the new owner knows who to call when there's a problem, who the decision makers are, and what communication style works best with each vendor. A quick "they prefer email over phone" or "always call Mike, not the main line" can save the new owner weeks of frustration.

Operational Knowledge Transfer: Getting What's in Your Head on Paper

This is the part that takes the most work and the part most sellers skip. After running a business for 10 or 20 years, you've accumulated an enormous amount of knowledge that lives only in your head. The daily routines, the seasonal adjustments, the workarounds for that one piece of equipment that acts up in cold weather. All of that needs to be documented and transferred.

Standard operating procedures (SOPs). Write down the step by step process for every major business function. How do you open the store? How do you process a new order? How do you handle a customer complaint? How do you run payroll? What's the monthly close process for bookkeeping? If your business doesn't have written SOPs, creating them should be the first thing you do when you decide to sell.

I tell my sellers to start documenting SOPs at least 3 months before listing the business. It takes longer than you think, and having clean documentation in place when buyers start asking questions makes your business look professional and well run. Buyers pay more for businesses that don't depend on the owner's memory.

Training schedule. Build a structured training plan for the new owner. Week 1 covers daily operations and opening/closing procedures. Weeks 2 and 3 cover financial management, vendor ordering, and employee scheduling. Weeks 4 through 8 cover advanced topics like seasonal planning, marketing execution, and customer relationship management. Map it out in writing so both parties know what's being covered and when.

Shadow periods. The most effective knowledge transfer happens when the new owner works alongside you in the business. During the first 2 to 4 weeks after closing, plan for the buyer to shadow you through every aspect of operations. They should see how you handle the morning rush, how you deal with a difficult customer, how you troubleshoot equipment problems. Reading a manual is one thing. Watching someone do it is completely different.

Create a "tribal knowledge" document. This is the stuff that doesn't fit into SOPs. Write down everything a new owner would need to know that isn't obvious. Things like: the health inspector always comes in March, the AC unit needs to be serviced before summer or it breaks down, our best employee is thinking about going back to school next year, the parking lot floods when it rains hard and you need to put out cones. This kind of information is invaluable and impossible for a buyer to discover on their own.

Technology access and passwords. Create a master document with login credentials for every system the business uses. POS system, accounting software, email accounts, social media profiles, website hosting, domain registrar, security cameras, alarm systems. I've seen transitions stall for weeks because the seller forgot the password to a critical system and the recovery email was tied to a personal account they'd already changed.

Ready to start preparing your business for sale? Use our business valuation tools to understand your numbers before you begin the exit process.

What to Include in the Transition Agreement

The transition plan should be formalized as part of your purchase agreement. This isn't a handshake deal. Every detail should be in writing and signed by both parties. Here's what a good transition agreement covers.

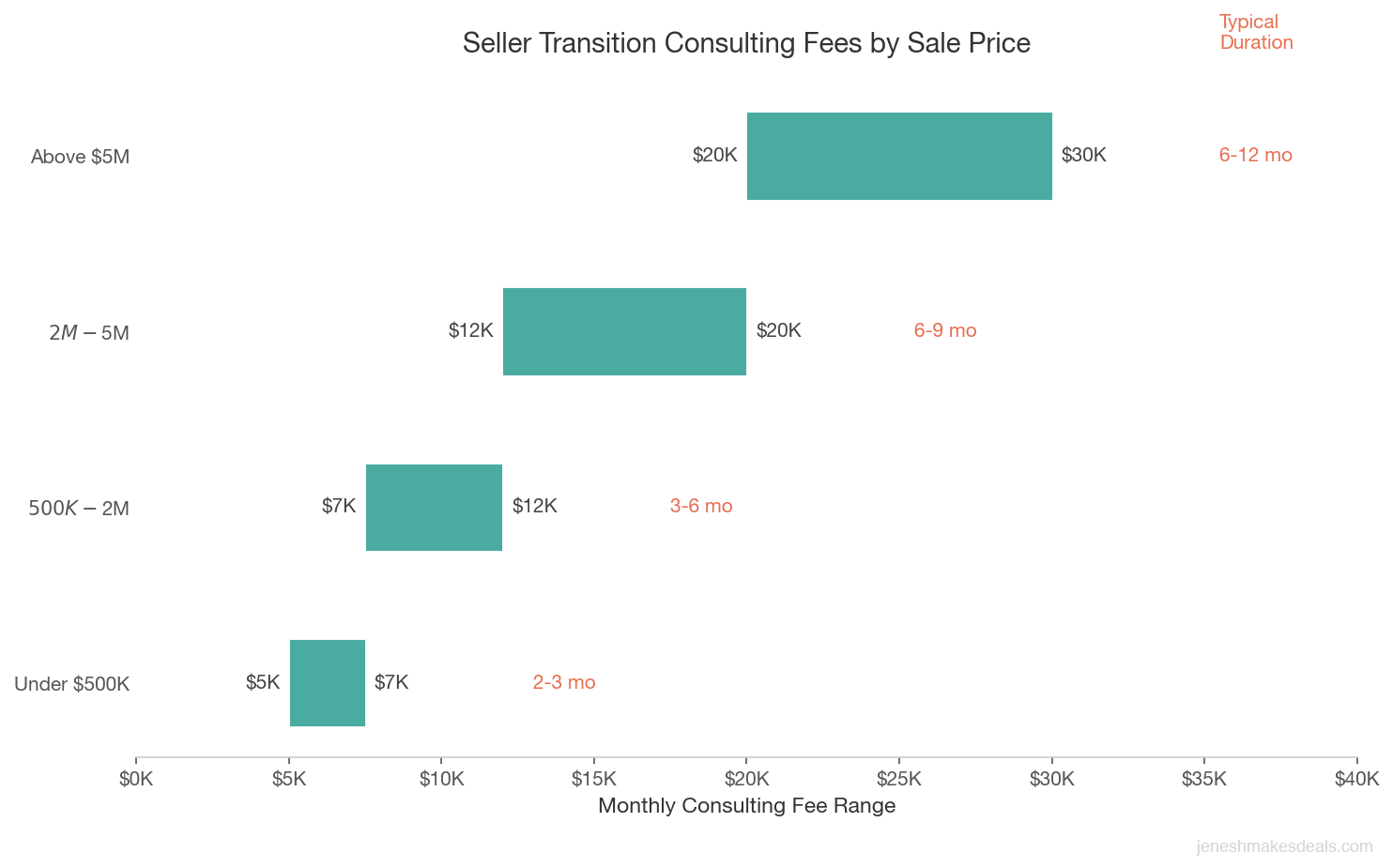

Hours per week. Be specific about your time commitment. I typically see sellers agree to 40 hours per week for the first month, 20 hours per week for months 2 and 3, and 5 to 10 hours per week (phone/email availability) for months 4 through 6. The gradual reduction is important. You don't want to go from 40 hours to zero overnight.

| Sale Price Range | Monthly Consulting Fee | Typical Transition Length | Common Structure |

|---|---|---|---|

| Under $500,000 | $5,000 to $7,500 | 2 to 3 months | Flat monthly rate |

| $500,000 to $2 million | $7,500 to $12,000 | 3 to 6 months | Monthly rate or hourly ($100 to $175/hr) |

| $2 million to $5 million | $12,000 to $20,000 | 6 to 9 months | Hourly ($150 to $250/hr) with monthly cap |

| Above $5 million | Negotiated, often $20,000+ | 6 to 12 months | Retainer plus performance bonuses |

Compensation. Sellers are typically compensated for transition work beyond the first 2 to 4 weeks. Standard consulting rates I see in the market range from $5,000 to $15,000 per month, depending on the size of the business and the seller's level of involvement. For a business selling for under $500,000, $5,000 to $7,500 per month is typical. For businesses selling between $500,000 and $2 million, $7,500 to $12,000 per month is common. Above $2 million, I've seen consulting fees as high as $15,000 to $20,000 per month.

Some deals structure this as an hourly rate ($100 to $250 per hour) with a minimum and maximum monthly commitment. Others include transition consulting as part of the purchase price with no additional compensation. It depends on the deal structure and what both parties agree to.

Scope of work. Define exactly what you will and won't do during the transition. Are you making sales calls? Training employees? Running the books? Attending client meetings? The more specific you are, the fewer disagreements you'll have later. I've seen disputes arise when the buyer expected the seller to bring in new business during the transition period, but the seller understood their role as limited to introducing existing customers.

Non compete terms. Almost every purchase agreement includes a non compete clause, and the transition agreement should reference it. Standard non competes are 3 to 5 years within a 25 to 50 mile radius of the business (varies by state law). The non compete protects the buyer's investment and gives them confidence that you won't take your customer relationships and open a competing business down the street.

Termination provisions. What happens if the transition isn't working? The agreement should spell out how either party can end the arrangement early, what notice is required, and what the financial implications are. You don't want to be locked into a 6 month consulting agreement if the relationship deteriorates.

Performance benchmarks. For deals with earnout components, define clear metrics that determine whether the transition is successful. Customer retention rate, revenue targets, employee retention. Make these measurable and objective. "The business is doing well" is not a benchmark. "The business retains at least 85% of trailing 12 month revenue through the transition period" is.

Common Transition Mistakes Sellers Make

After seeing hundreds of transitions, I can predict which ones will go sideways based on the seller's behavior in the first few weeks. Here are the mistakes I see most often.

Checking out too early. Some sellers are so relieved the deal closed that they mentally check out on day one. They show up late, leave early, and give vague answers when the buyer asks questions. The buyer feels abandoned, customers notice the lack of energy, and the whole transition suffers. You agreed to a transition period. Honor it. Your reputation and potentially your remaining sale proceeds depend on it.

The transition period is the last impression you leave on your business. Buyers talk to each other, brokers remember who was easy to work with, and earnout payments depend on the results you help create. Treat the first 90 days after closing with the same seriousness you brought to the first 90 days when you started the business.

Bad mouthing or undermining the buyer. This is more common than you'd think. The seller disagrees with one of the buyer's early decisions and tells an employee, "I wouldn't have done it that way." Or they make offhand comments to customers like, "Things might be different around here soon." Whether intentional or not, this kind of commentary undermines the buyer's authority and poisons the transition. Once you sell the business, it's not yours anymore. Bite your tongue and let the new owner run it their way.

Not documenting anything. I've had sellers tell me, "I'll just show them how everything works." That's not a transition plan. That's hoping you remember everything, hoping the buyer absorbs it all in real time, and hoping nothing comes up later that you forgot to mention. Document everything in writing. If it's not written down, it doesn't exist.

Surprising the buyer with problems. Some sellers wait until after closing to mention that the biggest customer has been threatening to leave, or that the main piece of equipment needs a $30,000 repair, or that there's a pending lawsuit they "forgot" to disclose. This isn't just a transition mistake. It's potential fraud. Disclose everything before closing. Surprises after the sale destroy trust and lead to lawsuits.

Being possessive about relationships. You spent years building relationships with customers, employees, and vendors. It's hard to hand those over. But that's exactly what you agreed to do. Some sellers unconsciously (or consciously) keep themselves as the primary point of contact, making the buyer feel like an outsider. Introduce the new owner, step back, and let them build their own relationships.

Failing to set boundaries. On the opposite end, some sellers are too available. They answer calls at midnight, come in on weekends they're not scheduled, and insert themselves into decisions they have no role in. This creates dependency instead of independence. The goal is to make yourself unnecessary, not indispensable.

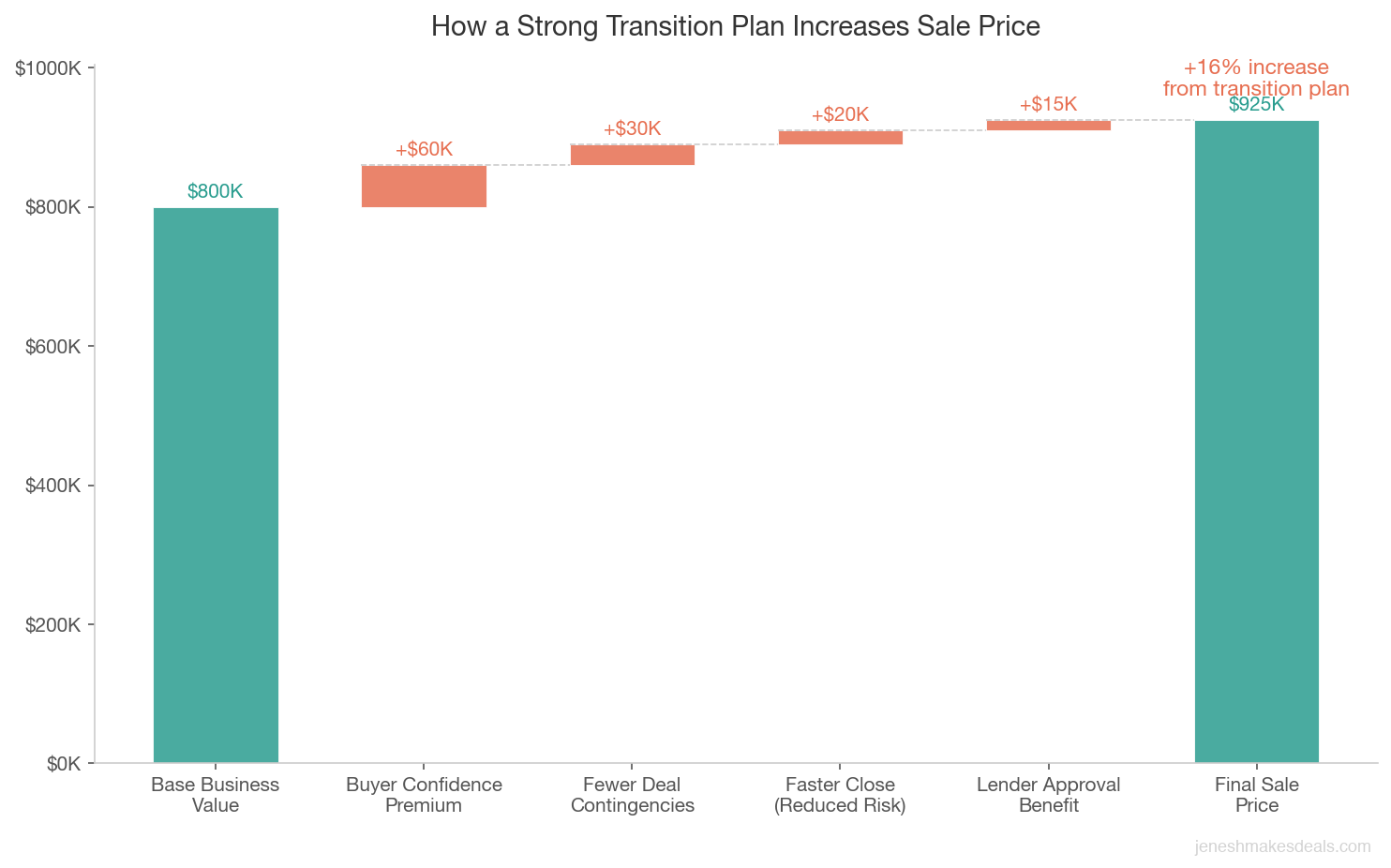

How a Strong Transition Plan Increases Your Sale Price

Let me put specific numbers on this because I think it's the most compelling reason to take transition planning seriously.

In my experience, businesses with detailed transition plans sell for 5% to 15% more than comparable businesses without one. On a $1 million sale, that's $50,000 to $150,000. Here's why.

Buyer confidence reduces negotiation pressure. When a buyer sees a detailed transition plan, they feel safer. They're less likely to push for a lower price, ask for larger earnout holdbacks, or demand extended escrow periods. The transition plan answers their biggest fear: "What happens when the current owner leaves?"

Lender approval becomes easier. SBA lenders review the transition plan as part of their underwriting process. A strong plan signals lower risk, which can mean better loan terms for the buyer. If the buyer can get better financing, they can afford to pay more for the business. I've seen deals where a weak transition plan caused the SBA lender to require a larger down payment, which made the buyer renegotiate the price downward by $75,000.

Fewer deal contingencies. Without a transition plan, buyers protect themselves by adding contingencies to the purchase agreement. Revenue holdbacks, extended earnout periods, larger escrow amounts. All of these reduce the amount of cash you receive at closing. A strong transition plan eliminates many of these contingencies because the buyer has confidence that the business will perform after the sale.

Faster closing timeline. Deals with clear transition plans close faster because there are fewer open questions during due diligence. Every week a deal drags on increases the risk it falls apart. The average business sale takes 6 to 9 months from listing to closing. A well prepared seller with a solid transition plan can shave 1 to 2 months off that timeline.

Multiple offer advantage. When you have multiple interested buyers (which a good broker should help you generate), the transition plan becomes a differentiator. Buyers who are competing for the business will offer more when they see a seller who's committed to a thorough handoff. It signals that you're serious, professional, and invested in the business's long term success.

Building Your Transition Plan: A Practical Timeline

Here's a timeline I give to every seller I work with. Start this process well before you list your business.

6 months before listing:

- Begin documenting SOPs for all major business functions

- Create the customer knowledge document for your top 20 accounts

- Compile the complete vendor list with contract details and key contacts

- Identify key employees and start thinking about retention strategies

- Organize all technology access credentials in a secure document

3 months before listing:

- Finish all SOP documentation

- Review vendor contracts for assignment clauses

- Work with your broker to draft the transition plan framework

- Determine your transition commitment (duration, hours, compensation expectations)

During due diligence:

- Share the transition plan with the buyer as part of the deal package

- Negotiate transition terms and include them in the purchase agreement

- Finalize retention bonus structures for key employees

2 weeks before closing:

- Begin personal introductions with your top 10 customers

- Prepare the employee announcement and schedule the team meeting

- Contact critical vendors to start the assignment process

First 30 days after closing:

- Full time involvement in the business

- Complete customer introductions (all tiers)

- Structured training with the new owner (daily shadowing)

- Announce the transition to employees and vendors

Days 31 through 90:

- Reduce to part time involvement (20 hours per week)

- New owner handles day to day operations with your support

- Available for questions and problem solving

- Continue vendor introductions and contract assignments

Days 91 through 180:

- Phone and email availability only (5 to 10 hours per week)

- New owner runs the business independently

- You're a resource for unusual situations, not daily operations

Considering selling your business in the next 6 to 12 months? The earlier you start planning, the better your outcome. Let's talk about your exit strategy.

The Bottom Line

A business transition plan isn't a formality. It's the difference between a sale that holds together and one that falls apart. It directly impacts your sale price, your legal exposure, and your reputation.

The sellers who do this well share a few traits. They start planning early, they document everything, they commit to making the buyer successful, and they know when to step back. They treat the transition period as the final chapter of their ownership story, not an inconvenience to rush through.

The sellers who do this poorly lose money, burn relationships, and end up in disputes that could have been avoided with a few months of planning.

I've been through this process hundreds of times, and the pattern is always the same. Sellers who invest 20 to 30 hours in building a proper transition plan earn tens of thousands of dollars more on their sale. That's the best hourly rate you'll ever earn.

Ready to start planning your exit? Reach out for a free consultation and we'll build a transition strategy that protects your sale price and sets the new owner up for success.

For a complete walkthrough of every stage of the sale, from preparation through closing and transition, download our free Complete Guide to Selling Your Business in 2026.

Related Articles

May 1, 2026

What Happens to Accounts Receivable When You Sell

AR is one of the most negotiated items in any business sale. Here's exactly how it's handled, valued, and who collects it after closing.

April 28, 2026

What Is Representations and Warranties Insurance

R&W insurance protects buyers and sellers in business sales by covering breaches of reps in purchase agreements. Here's how it works.

April 27, 2026

How to Handle Inventory in a Business Sale

Inventory can make or break a business sale. Here's how to value it, negotiate it, and avoid the disputes that kill deals at closing.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.