You've agreed on a price with a buyer. Maybe it's $750,000. You're feeling good. Then the buyer's attorney sends over the first draft of the purchase agreement and it says "asset purchase agreement" at the top.

You think, "What's the difference? A sale is a sale."

That assumption can cost you $50,000 to $200,000 or more. The structure of your deal, whether it's an asset sale or a stock sale, changes how much you actually keep after taxes. It affects what liabilities stay with you, what entity you walk away from, and how the closing process works.

Most sellers I work with don't know the difference until their accountant explains it mid deal and suddenly they're trying to renegotiate something that should have been discussed upfront. I want you to have this knowledge before you ever sit down at the table.

Important disclaimer: I'm a business broker, not a CPA or tax attorney. The tax rates and examples in this post are for educational purposes. Your specific situation depends on your entity type, income level, state, and a dozen other factors. Please work with a qualified tax professional when making decisions about your sale.

What Is an Asset Sale

In an asset sale, the buyer purchases individual assets from your business: equipment, inventory, customer lists, the business name, intellectual property, goodwill, and the right to operate going forward.

The key thing to understand: your legal entity stays with you. The buyer doesn't acquire your LLC or corporation. They form their own new entity and transfer the purchased assets into it.

Think of your business as a house. In an asset sale, the buyer is buying the furniture, appliances, and everything inside. You keep the house itself.

After closing, you still own the original entity and any remaining liabilities inside it. The purchase agreement lists every asset being transferred by name, serial number, or registration. Anything not specifically listed stays with you.

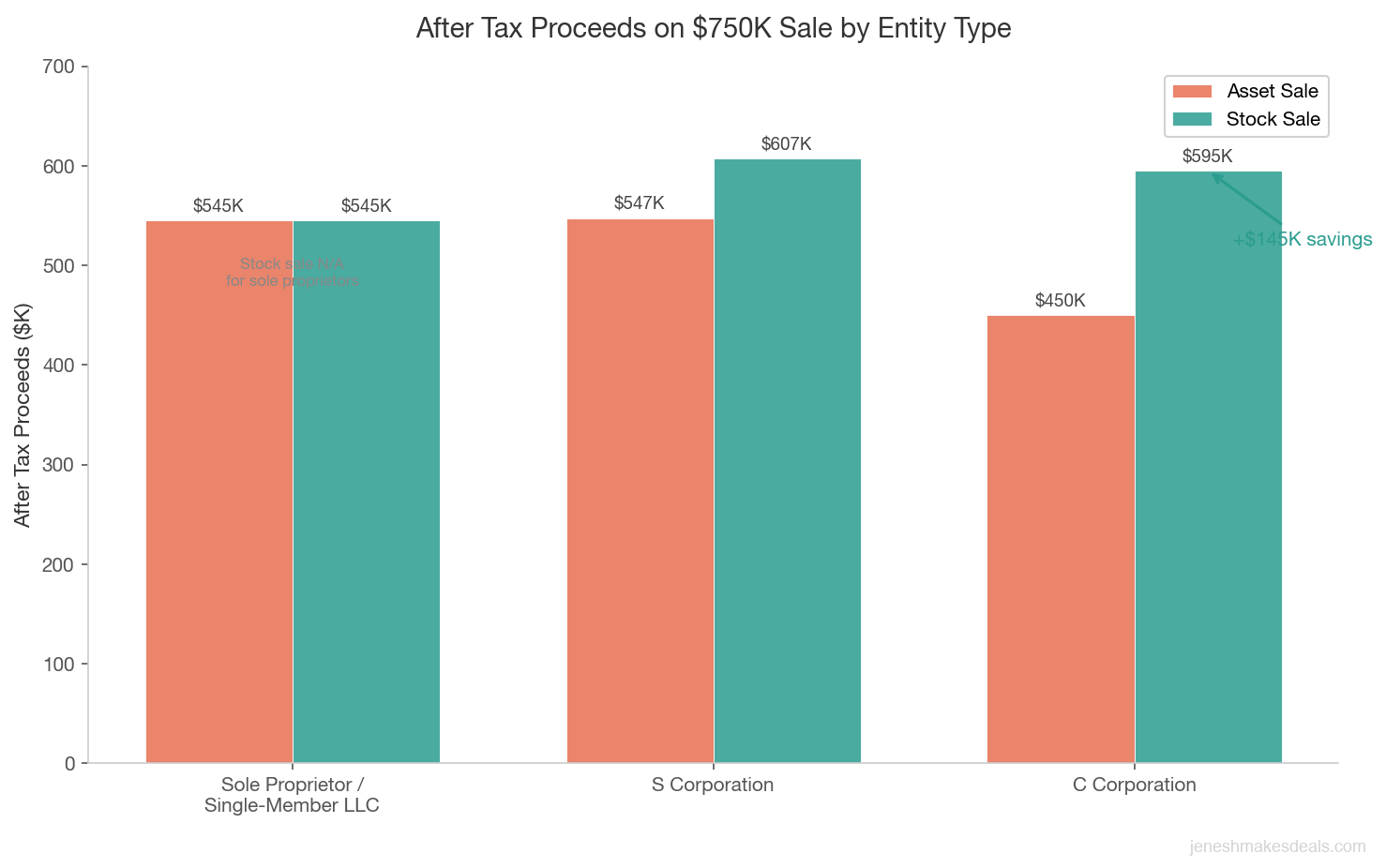

Asset sales are the most common structure for small businesses. About 80% to 90% of businesses under $5 million sell as asset sales. If you're a sole proprietor, single member LLC, or S corporation, your deal will almost certainly be structured this way.

What Is a Stock Sale

In a stock sale (sometimes called an equity sale or membership interest sale), the buyer purchases your ownership shares or membership interests in the entity itself. They're buying the entire legal entity, which happens to own all those assets.

Same house analogy: the buyer is purchasing the house itself, and everything inside comes with it.

Everything transfers: assets, liabilities, contracts, permits, licenses, pending lawsuits, tax history. The entity doesn't change. Only the owner changes. The EIN stays the same, contracts don't need reassignment (in most cases), and the entity's full history belongs to the buyer.

Stock sales are far less common for small businesses but do happen regularly in certain situations I'll cover below.

Why Buyers Almost Always Prefer Asset Sales

If you're a seller, you need to understand why buyers push for asset sales, because this is the starting point in almost every negotiation.

Step up in basis. This is the big one. When a buyer purchases assets, they get to "step up" the tax basis to the purchase price. They can then depreciate and amortize those assets from full value, creating tax deductions for years. A buyer paying $750,000 might allocate $200,000 to equipment (depreciated over 5 to 7 years), $50,000 to a non compete agreement (amortized over its term), and $400,000 to goodwill (amortized over 15 years).

In a stock sale, the buyer inherits the existing tax basis. If your equipment is already fully depreciated on your books, the buyer gets zero depreciation deductions even though they paid real money for it.

On a $750,000 acquisition, the step up in basis can be worth $150,000 to $250,000 in tax savings to the buyer over 15 years.

No hidden liabilities. In an asset sale, the buyer picks what they want and leaves everything else behind. Pending lawsuits, unknown tax obligations, environmental liabilities, and employee disputes stay with the seller's entity. In a stock sale, the buyer inherits all of that. That risk makes buyers nervous, and rightfully so.

Cherry picking assets. Buyers can exclude assets they don't want: old equipment, excess inventory, a money losing product line. In an asset sale, those items simply aren't included. In a stock sale, they get everything whether they want it or not.

Why Sellers Often Prefer Stock Sales

Now let's talk about your side. Here's why sellers, particularly C corporation owners, tend to prefer stock sales.

Capital gains treatment on the entire sale price. In a stock sale, you're selling ownership interests. The entire gain is treated as a long term capital gain (assuming you've held the interests for more than a year). The federal rate is 15% or 20% depending on your income level, plus the 3.8% net investment income tax if applicable.

In an asset sale, different chunks of the purchase price get taxed at different rates. Goodwill and long term capital assets get capital gains treatment, but inventory gets taxed as ordinary income. Depreciation recapture on equipment gets taxed at ordinary income rates (up to 37%). Non compete agreements are taxed as ordinary income. Depending on how the purchase price is allocated, a significant portion of your proceeds could be taxed at 37% instead of 20%.

For a $750,000 sale, the difference between all capital gains treatment and a mixed allocation can be $40,000 to $80,000 in additional taxes.

Avoiding double taxation for C corporations. This is the biggest reason C corporation owners fight for stock sales. In a C corporation asset sale, the corporation pays tax on the gains from selling the assets (at the 21% corporate rate). Then, when the remaining proceeds are distributed to you as a shareholder, you pay tax again on the distribution (at capital gains rates of 15% to 23.8%).

That's two layers of tax. On a $750,000 sale with $500,000 of gain, the combined effective tax rate can reach 40% to 50%. On a stock sale, you pay tax once at your personal capital gains rate. The savings can be enormous.

I worked with a C corporation owner selling a $900,000 business. His CPA ran the numbers both ways. Asset sale total tax burden: approximately $285,000. Stock sale total tax burden: approximately $155,000. That's a $130,000 difference on the same sale price. It's not hard to understand why he insisted on a stock sale.

If you own a C corporation, the single most important conversation you can have before listing your business is with your CPA about the asset sale vs stock sale tax difference. I've seen C corp owners lose over $100,000 simply because they didn't raise this issue until the deal was already in motion.

Cleaner exit. In a stock sale, you sell your ownership interests and walk away. You don't have to dissolve the entity, settle remaining liabilities, or deal with post closing cleanup of the shell corporation. The entity transfers whole, and your involvement ends.

The Tax Math: How Asset Allocation Changes Everything

Here's where things get specific. In an asset sale, the purchase price must be allocated across different asset categories, and each category has different tax consequences for you as the seller.

Let's walk through a $750,000 asset sale for an S corporation with these allocations:

Inventory: $75,000. Taxed as ordinary income. If you're in the 32% federal bracket plus state tax, you might pay 37% to 40% effective on this amount. Tax on this chunk: roughly $28,000 to $30,000.

Equipment: $125,000 (with $80,000 of depreciation recapture). The depreciation you claimed over the years gets "recaptured" and taxed as ordinary income. So $80,000 of this is taxed at ordinary rates (32% to 37%), and the remaining $45,000 of gain above original cost is taxed at capital gains rates. Tax on this chunk: roughly $35,000 to $38,000.

Non compete agreement: $50,000. Taxed entirely as ordinary income to you. The buyer loves allocating money here because they can amortize it. You hate it because it's taxed at your highest rate. Tax: roughly $16,000 to $19,000.

Goodwill: $400,000. Taxed as a long term capital gain if you've held the business for more than one year. At a 20% federal rate plus 3.8% NIIT, that's 23.8%. Tax: roughly $95,200.

Customer list and other intangibles: $100,000. Also long term capital gains if held more than one year. Tax: roughly $23,800.

Total estimated federal tax: $198,000 to $206,000. That leaves you with roughly $544,000 to $552,000 before state taxes.

Now compare that to a stock sale of the same business for $750,000. If your total basis in the stock is $100,000, you have a $650,000 long term capital gain taxed at 23.8%. Total federal tax: approximately $154,700. You keep roughly $595,300 before state taxes.

The difference: about $45,000 to $50,000 in this example. And this is for an S corporation. For a C corporation, the gap would be much larger because of double taxation on the asset sale. Run your own numbers through our seller net proceeds calculator to see how deal structure affects what you actually keep.

When a Stock Sale Makes Sense

Stock sales aren't just about tax preference. There are practical situations where a stock sale is clearly the better structure.

C corporations facing double taxation. As I covered above, the math usually makes a stock sale dramatically better for C corp shareholders. The double taxation problem on asset sales can increase the total tax burden by 15 to 25 percentage points. If you're a C corp owner, this should be the first thing you discuss with your tax advisor.

There's also a hybrid option called a Section 338(h)(10) election. This lets the buyer treat a stock purchase as if it were an asset purchase for tax purposes, giving them the step up in basis they want while structuring the deal as a stock sale. But this election is only available for S corporations and certain subsidiary situations, not standalone C corporations. If you're an S corp, ask your CPA about this because it can give both sides what they want.

Businesses with non transferable contracts, licenses, or permits. Some businesses operate under government licenses, franchise agreements, or contracts that can't be assigned to a new entity. Liquor licenses, government contracts with anti assignment clauses, and franchise agreements all fall into this category. In a stock sale, the entity doesn't change, so these stay intact.

I worked with a seller who had a commercial cleaning company with three government contracts, each requiring six months notice and agency approval for assignment. A stock sale let the buyer take over without triggering those clauses, saving months on the timeline.

Businesses with favorable leases or hard to replicate permits. If your lease is below market rent, an asset sale could force renegotiation with the landlord. Environmental permits, health department certifications, and professional licenses held by the entity can take months or years to reapply for. A stock sale avoids both problems.

When an Asset Sale Makes Sense

For most small business sellers, the asset sale structure works just fine, even if it's not your first choice.

Sole proprietors and single member LLCs. If you don't have a formal entity, or your entity is a disregarded LLC, a stock sale isn't really an option. You're selling assets by default.

S corporations and LLCs taxed as partnerships. These pass through entities don't face the double taxation problem that makes C corp asset sales so painful. The tax difference between an asset sale and stock sale still exists (because of the allocation issue), but it's much smaller. Often small enough that it's not worth the fight.

Businesses with potential hidden liabilities. If there's any chance of environmental contamination, pending litigation, employee claims, or tax issues, a buyer won't agree to a stock sale regardless of what tax benefit you offer. They're not going to inherit your problems.

Most businesses under $5 million in value. SBA lenders strongly prefer asset sales because they create a cleaner collateral picture. Buyers at this level are often first time owners who aren't comfortable inheriting unknown risks. The legal and accounting costs of structuring a stock sale are also higher, which matters more on smaller deals.

When you want to retain certain assets. Maybe you want to keep the real estate and lease it to the buyer, or collect accounts receivable yourself. An asset sale lets you carve these out easily. In a stock sale, you'd need to distribute them out of the entity before closing, which creates its own tax consequences.

How the Purchase Price Gets Allocated in an Asset Sale

If your deal is structured as an asset sale, one of the most important negotiations is the purchase price allocation. This determines how much of the $750,000 (or whatever your price is) gets assigned to each asset category.

The IRS requires this allocation under Section 1060, and it must be consistent between buyer and seller. You both file Form 8594 with your tax returns, and the numbers need to match.

The IRS groups assets into seven classes, and the purchase price is allocated in order:

Class I: Cash and cash equivalents. Allocated at face value.

Class II: Actively traded securities. Allocated at fair market value.

Class III: Accounts receivable, mortgages, credit card receivables. Allocated at fair market value. Often excluded from the sale entirely.

Class IV: Inventory. Allocated at fair market value. This is taxed as ordinary income to you, so you want this number as low as defensible.

Class V: All other tangible and intangible assets not in other classes. This includes equipment, furniture, fixtures, land, buildings, and similar assets. Depreciation recapture applies to equipment.

Class VI: Section 197 intangibles except goodwill and going concern value. This includes customer lists, non compete agreements, trade names, patents, and similar intangibles. Non compete amounts are taxed as ordinary income to you.

Class VII: Goodwill and going concern value. This is the residual, meaning whatever is left over after allocating to all other classes goes here. Taxed as long term capital gains.

Here's the tension. You, the seller, want as much as possible allocated to Class VII (goodwill) because it gets capital gains treatment. The buyer wants more allocated to Class V (equipment they can depreciate quickly) and Class VI (intangibles they can amortize over shorter periods, particularly non compete agreements).

A buyer might propose allocating $150,000 to a non compete agreement. That's great for them because they amortize it over the agreement's term (usually 3 to 5 years) and get a faster deduction. But for you, that $150,000 is taxed at ordinary income rates of up to 37% instead of the 20% to 23.8% capital gains rate it would have received as goodwill.

On $150,000, the difference between 37% and 23.8% is roughly $19,800 in additional tax. That's real money that comes directly out of your pocket.

Want to understand how your business value breaks down? Use our free business valuation calculator to get a starting estimate of what your business is worth.

Negotiating the Structure: Finding Middle Ground

In most deals, the buyer wants an asset sale and the seller wants a stock sale (or at least a more favorable allocation). Here's how the negotiation typically plays out.

Adjust the price to account for tax differences. If a stock sale would save you $80,000 in taxes but the buyer insists on an asset sale, negotiate a higher purchase price to bridge the gap. The buyer might agree to $780,000 instead of $750,000, knowing they'll recoup the premium through step up in basis tax benefits over several years. It doesn't always work dollar for dollar, but it's a productive starting point.

Negotiate the allocation within an asset sale. Even if the structure is an asset sale, fight for a favorable allocation. Push for more goodwill and less allocation to inventory, non compete agreements, and equipment. The allocation needs to reflect fair market values, but there's often a range of defensible positions for each category.

I tell my sellers: the allocation negotiation is where you really fight. Most sellers spend all their energy on the purchase price and barely look at the allocation. A $750,000 sale with a seller friendly allocation can net you more than a $770,000 sale with a buyer friendly allocation.

The purchase price gets all the attention, but the allocation is where sellers quietly win or lose tens of thousands of dollars. Every dollar shifted from a non compete agreement to goodwill is money that gets taxed at capital gains rates instead of ordinary income rates. Never sign an allocation without your CPA reviewing it first.

Use indemnification to make stock sales acceptable. If the buyer's concern is hidden liabilities, strong indemnification language can help. You agree to indemnify the buyer for any pre closing liabilities that weren't disclosed, backed by 10% to 15% of the purchase price held in escrow for 12 to 18 months. This reduces the buyer's risk enough that some will agree to a stock sale when the tax benefit to you is significant.

Consider the Section 338(h)(10) election for S corps. This election can give both parties what they want. The deal is structured as a stock sale, but both sides elect to treat it as an asset sale for tax purposes. The buyer gets the step up in basis. The tax consequences flow through to your personal return as if assets were sold. Your CPA needs to run the specific numbers, but this election eliminates the structural conflict in many S corp deals.

Thinking about selling your business? Schedule a free consultation to discuss how deal structure affects your net proceeds.

Real Example: $750,000 Business, Two Structures Compared

Let me walk through a concrete example. Sarah owns a commercial printing business structured as an S corporation. She's held the business for 12 years. Her basis in the S corp stock is $150,000. The business has $125,000 of equipment (with a depreciated book value of $40,000), $60,000 of inventory, and the rest of the value is goodwill and customer relationships.

A buyer offers $750,000. Let's compare what Sarah keeps under each structure.

Scenario A: Asset Sale

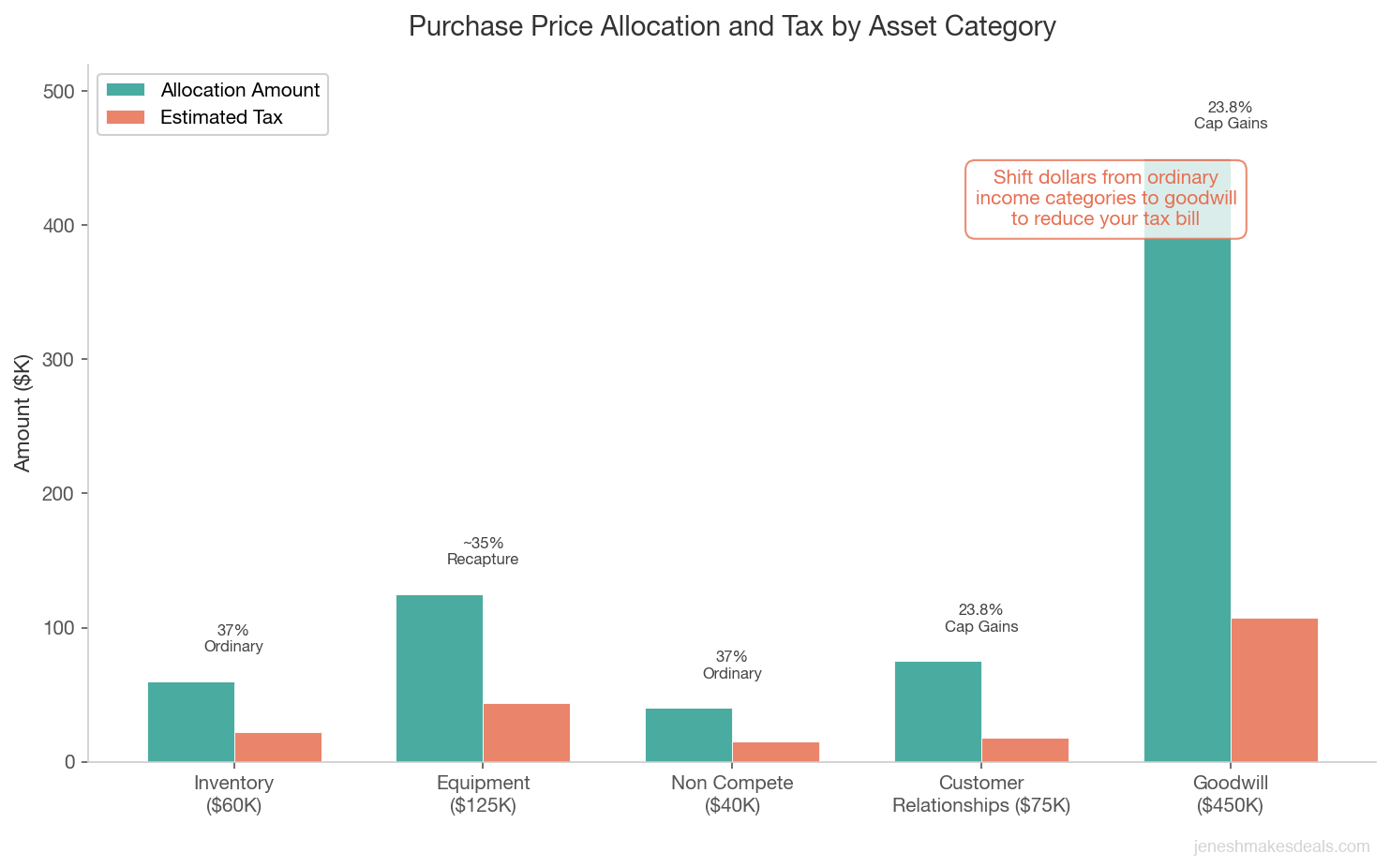

The purchase agreement allocates the $750,000 as follows:

| Asset Category | Amount | Tax Treatment | Estimated Tax |

|---|---|---|---|

| Inventory | $60,000 | Ordinary income (37%) | $22,200 |

| Equipment | $125,000 ($85,000 recapture) | Recapture at 37%, gain at 23.8% | $41,000 |

| Non compete | $40,000 | Ordinary income (37%) | $14,800 |

| Customer relationships | $75,000 | Capital gains (23.8%) | $17,850 |

| Goodwill | $450,000 | Capital gains (23.8%) | $107,100 |

| Total | $750,000 | $202,950 |

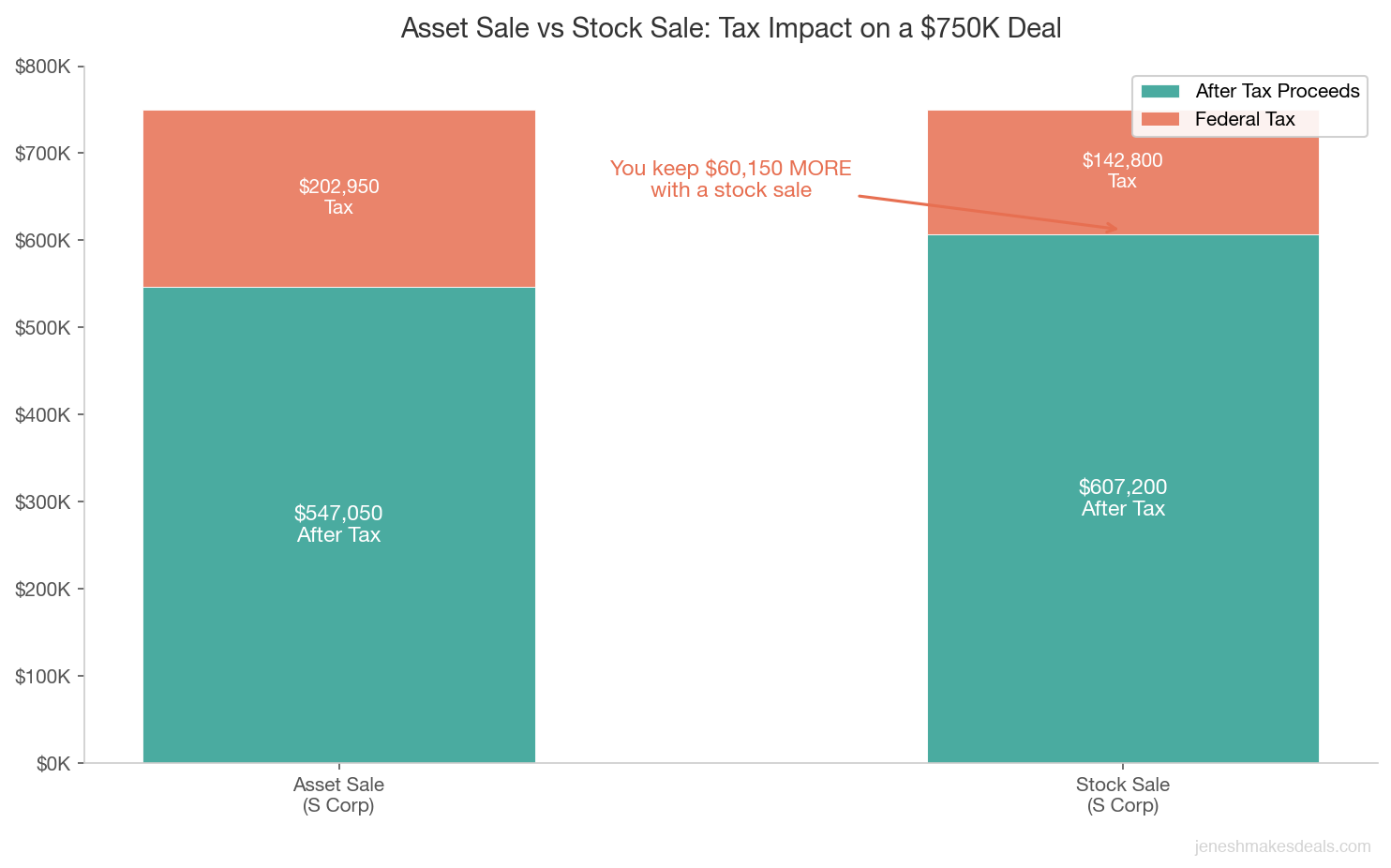

Sarah's after tax proceeds (federal only): approximately $547,050.

Scenario B: Stock Sale

Sarah sells her S corp shares for $750,000. Her basis is $150,000. The entire $600,000 gain is treated as a long term capital gain.

| Amount | Tax Treatment | Estimated Tax | |

|---|---|---|---|

| Stock sale gain | $600,000 | Capital gains (23.8%) | $142,800 |

| Total | $750,000 | $142,800 |

Sarah's after tax proceeds (federal only): approximately $607,200.

The Difference

Sarah keeps $60,150 more with a stock sale. That's 8% of the total sale price, and it's purely a structural decision.

Now, if Sarah's buyer insists on an asset sale, she could try to negotiate the price up to $810,000 to offset the tax difference. Or she could push for a more favorable allocation. Moving $40,000 from the non compete to goodwill alone would save her about $5,280 in taxes.

If Sarah's business were a C corporation instead of an S corp, the gap would be even wider. In a C corp asset sale, the corporation pays 21% on the gain, then Sarah pays another 23.8% when she distributes the after tax proceeds. The combined effective rate pushes toward 40% to 45%, compared to 23.8% on a stock sale. On a $750,000 deal, that could mean $100,000 or more in additional taxes.

Not sure what your business is worth? Run the numbers with our business valuation tools to get a starting estimate before you talk to buyers.

Common Mistakes Sellers Make on Deal Structure

I've seen these mistakes cost sellers real money. Don't make them.

Ignoring the structure until the LOI is signed. By the time you've signed a letter of intent specifying an asset sale, you've given up your best negotiating position. Discuss structure early so it's part of the overall negotiation, not an afterthought.

Letting the buyer control the allocation. Buyers will propose allocations that maximize their tax benefit. If you just sign what they put in front of you, you're leaving money on the table. Your CPA should review every proposed allocation and push back where the numbers aren't defensible, especially on non compete agreement allocations that buyers tend to inflate.

Not involving a CPA early enough. Your accountant should be involved before you sign anything. Running the tax projections on different structures and allocations takes time. If you find out mid closing that the proposed allocation costs you $50,000 more in taxes, it's very difficult to change course.

Confusing entity type with sale type. I hear sellers say "I have an LLC, so it has to be an asset sale." That's not correct. If your LLC has multiple members, the buyer can purchase membership interests (the equivalent of a stock sale).

Forgetting about state taxes. State rates vary dramatically. California adds up to 13.3%. Texas has no income tax. State taxes can add $30,000 to $75,000 to the bill on a $750,000 sale, and the treatment of asset vs stock sales can differ by state.

What You Should Do Before Your Sale

Here's my practical advice for any business owner thinking about selling in the next 12 to 24 months.

Know your entity type and its implications. If you're a C corporation, talk to your CPA about converting to an S corporation. The IRS requires five years to avoid the BIG tax on built in gains, so this isn't a last minute decision. For some sellers, converting well ahead of a sale saves six figures.

Get a tax projection before you list. Have your CPA model after tax proceeds under both structures. Know the dollar difference so you can negotiate from real numbers, not guesses.

Understand what your buyer will want. Most buyers below $5 million will want an asset sale. Fighting it too hard can kill deals. Know your bottom line, fight for the allocation, and use price adjustments to bridge the gap.

Clean up your liabilities. If you want any chance at a stock sale, the buyer needs to feel comfortable inheriting your entity. Resolve pending disputes, clean up tax issues, and get current on all obligations.

Build the allocation into your pricing strategy. Factor in the after tax number, not just the gross price. A $750,000 sale with a bad allocation might net you less than a $720,000 sale with a favorable one.

The sellers who plan 12 to 24 months ahead almost always walk away with more money. Entity conversions, liability cleanup, and tax projections all take time. If you're even thinking about selling in the next two years, start these conversations with your CPA now, not when an offer lands on your desk.

Ready to get a clear picture of what you'd walk away with? Let's talk through your specific situation so you're not guessing at the tax numbers.

The Bottom Line

Asset sale vs stock sale isn't an academic question. It's a decision that directly affects how much money you keep from the biggest financial transaction of your life.

For most small business sellers, the deal will end up as an asset sale. That's the market reality. But knowing the difference gives you the ability to negotiate the allocation, push for price adjustments when the structure costs you money, and plan your entity structure years in advance.

The sellers who do best aren't the ones who get the highest price. They're the ones who keep the highest percentage of whatever price they get. And that comes down to structure, allocation, and having the right advisors in your corner from the start.

Want help figuring out the best structure for your sale? Reach out for a free consultation and we'll walk through your specific entity type, estimated value, and tax situation together.

For a full walkthrough of the selling process, including deal structure and tax planning, download our free Complete Guide to Selling Your Business in 2026.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.