Here's something that surprises a lot of first time sellers: how the buyer pays for your business is almost as important as how much they pay. The financing structure affects how quickly the deal closes, how much risk you carry after closing, and whether the deal survives due diligence at all.

I've seen sellers focus entirely on getting the highest offer price, only to have that offer fall apart because the buyer couldn't secure financing. I've seen other sellers accept a slightly lower price from a buyer with strong financing and close smoothly in 60 days. The lesson is clear: understanding buyer financing isn't optional for sellers. It's essential.

When you evaluate offers on your business, you need to look beyond the number and understand the money behind it. Is the buyer paying cash? Are they using an SBA loan? Are they asking you to carry a note? Are they using a combination of these? Each option has different implications for you as the seller, and knowing what to expect helps you make better decisions.

The Main Ways Buyers Finance Business Acquisitions

Most business acquisitions are funded through one or a combination of these methods. Let me walk you through each one and explain what it means for you as the seller.

SBA Loans

SBA loans are the most common financing method for small business acquisitions under $5 million. The Small Business Administration doesn't lend money directly. Instead, it guarantees a portion of the loan made by a participating bank, which reduces the bank's risk and makes them more willing to lend for business purchases.

How it works for buyers. The buyer typically puts down 10% to 20% of the purchase price. The SBA guaranteed lender finances the rest, usually at a variable rate tied to the prime rate plus a spread. Loan terms can run up to 10 years for business acquisitions, sometimes 25 years if commercial real estate is included.

What it means for you as a seller.

SBA deals tend to be the most structured and the slowest to close. Expect 60 to 90 days from accepted offer to closing, sometimes longer. The lender will require extensive documentation: your tax returns, financial statements, customer information, lease details, and often a third party business valuation or quality of earnings report.

The good news is that SBA deals result in you getting most or all of your money at closing. The buyer's down payment plus the SBA loan covers the purchase price. There's typically no seller financing required, though some SBA deals include a small seller note on standby (more on that later).

The bad news is that SBA deals can fall apart if the buyer doesn't qualify, if the lender's underwriting reveals problems with your business, or if the appraisal comes in below the purchase price. You're somewhat at the mercy of the lender's timeline and requirements.

I tell sellers to think of SBA financing like a full body scan of your business. The lender will look at everything: your tax returns, your lease, your customer concentration, your cash flow. If anything is out of order, the deal stalls. The time to fix those issues is before you go to market, not after a buyer is waiting on loan approval.

Key things to watch for:

- SBA lenders have specific requirements for the business lease. You'll need at least 10 years of combined lease term remaining.

- The lender will want to see that the business can service the debt from existing cash flow. If your business earns $200,000 and the annual debt service would be $180,000, the lender may not approve because the debt service coverage ratio is too thin.

- SBA lenders typically require a minimum 1.25x debt service coverage ratio, meaning the business needs to earn at least 25% more than the annual loan payments.

Seller Financing

Seller financing means you, the seller, act as the bank. Instead of receiving the full purchase price at closing, you receive a portion upfront and the buyer pays the remainder over time, usually with interest, according to a promissory note.

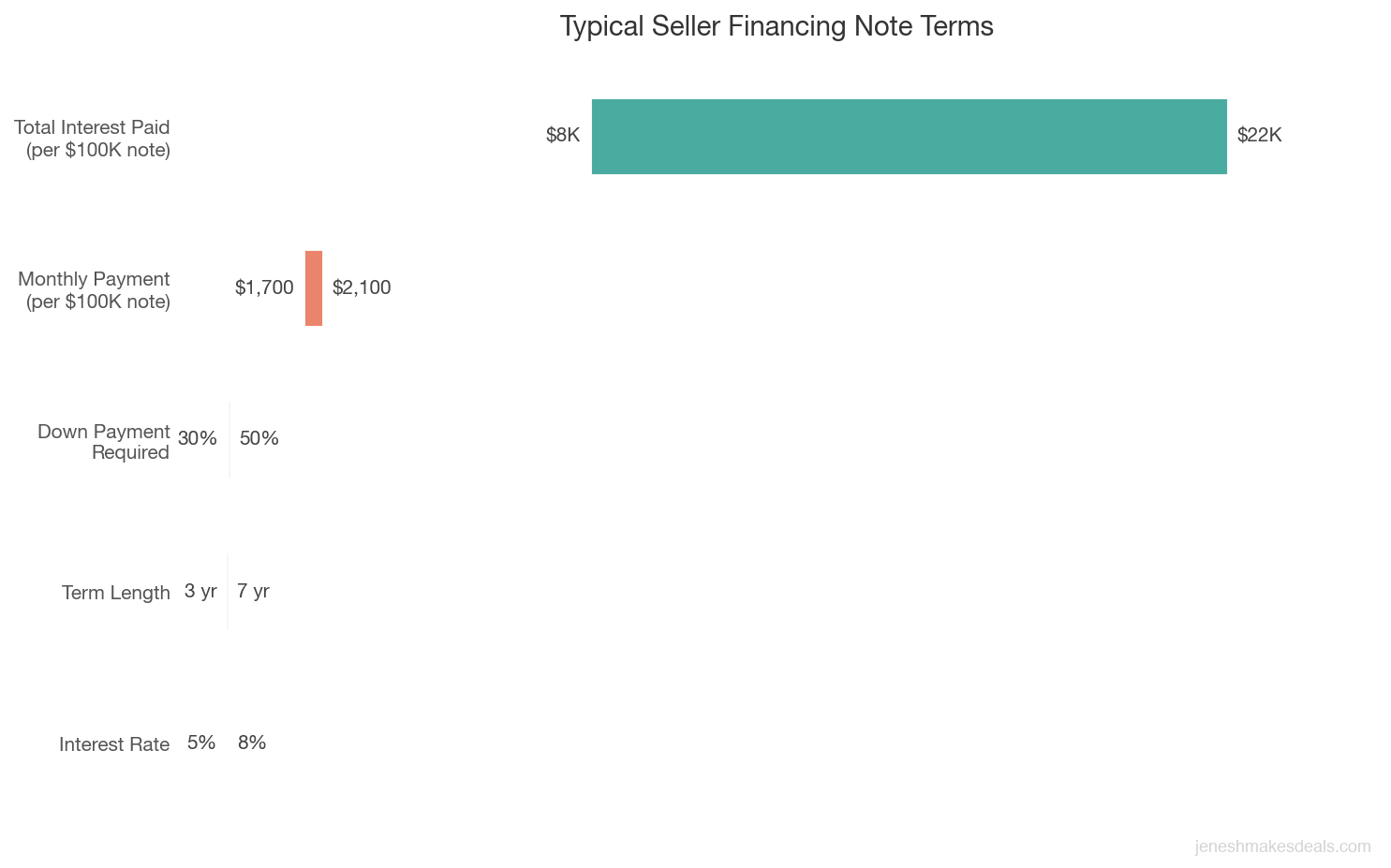

How it works. The buyer makes a down payment (typically 30% to 50% of the purchase price) and you carry a note for the balance. The note specifies the interest rate, payment schedule, term, and any security or collateral. Interest rates on seller notes typically range from 5% to 8%.

What it means for you as a seller.

Seller financing is extremely common in small business sales. In fact, many buyers expect some level of seller financing. From the buyer's perspective, your willingness to carry a note signals that you believe in the business's future. If you refuse all seller financing, some buyers will wonder what you know that they don't.

The advantage for you is that seller financing can help you sell faster, attract more buyers, and sometimes achieve a higher total purchase price because you're earning interest on the note. It can also provide tax benefits by spreading the gain over multiple years (installment sale treatment under IRS rules).

The risk is obvious: if the buyer fails to run the business successfully, they may default on your note. You could end up getting the business back in worse condition than when you sold it, or spending money on legal action to recover what you're owed.

The biggest mistake sellers make with seller financing is treating it as a handshake deal. Your promissory note is a real financial instrument. Get an attorney to draft it, secure it with a lien on the business assets, and include covenants that give you early warning if the buyer is struggling. A well structured seller note protects you. A sloppy one leaves you exposed.

How to protect yourself with seller financing:

- Require a meaningful down payment. The more the buyer has at stake, the less likely they are to walk away. A 30% to 50% down payment is reasonable.

- Secure the note against the business assets. Your promissory note should be secured by a lien on the business assets, and ideally by a personal guarantee from the buyer.

- Include default provisions. Your note should clearly state what constitutes a default and what remedies you have, including acceleration of the full balance and the right to take back the business assets.

- Require financial reporting. Include a covenant in the note that requires the buyer to provide you with periodic financial statements so you can monitor the business's performance.

- Consider a non compete carve out. If the buyer defaults and you take the business back, you need to be able to operate it. Make sure your non compete agreement has an exception for this scenario.

Need help understanding how financing affects your sale price? Use our free business valuation calculator to see what your business is worth and model different deal structures.

Conventional Bank Loans

Some buyers finance acquisitions through conventional bank loans that aren't backed by the SBA. These are more common for larger transactions or buyers with strong banking relationships.

How it works. The buyer borrows from a bank based on their own creditworthiness, the business's cash flow, and available collateral. Terms vary widely but generally require more equity from the buyer than SBA loans, often 25% to 40% down.

What it means for you as a seller. Conventional loans can close faster than SBA deals because they don't have the same bureaucratic requirements. But the buyer needs stronger credit and more equity, which narrows the buyer pool. If a buyer tells you they're using a conventional loan, make sure they've already been pre approved or at least had preliminary conversations with their banker.

All Cash Deals

An all cash buyer pays the full purchase price at closing without any financing. This is the dream scenario for most sellers, but it's less common than you might think for small business purchases.

What it means for you. Cash deals close fastest, carry the least risk of financing failure, and give you complete certainty about the proceeds. There's no note to worry about, no lender to satisfy, and no ongoing financial relationship with the buyer.

The trade off is that all cash buyers are rare for businesses priced above $200,000 to $300,000. And cash buyers often expect a discount because they're eliminating financing risk and providing certainty. Whether that discount is worth it depends on your priorities. If speed and certainty matter more than maximizing every dollar, a cash deal at a 5% to 10% discount might be the right call.

ROBS (Rollover for Business Startups)

Some buyers use their retirement funds to purchase a business through a ROBS structure. This involves creating a C corporation, rolling 401(k) or IRA funds into it, and using that capital for the business purchase.

What it means for you. ROBS deals function like cash from your perspective. The buyer has the money available and doesn't need lender approval. However, ROBS structures take time to set up (usually 3 to 6 weeks) and require specialized legal and financial advisors. If a buyer mentions ROBS, verify that they're working with a qualified provider and that the process is underway.

Private Equity and Strategic Buyers

If your business is large enough to attract private equity (PE) buyers or strategic acquirers (companies in your industry buying competitors), the financing dynamics are different.

PE buyers typically use a combination of equity from their fund and bank debt. They're sophisticated buyers with established lending relationships. Financing is rarely an issue, but their due diligence process is thorough and their deal terms may include earnouts, management retention requirements, and other conditions.

Strategic buyers often fund acquisitions from their own cash reserves or existing credit facilities. These can be the simplest deals from a financing perspective, but strategic buyers may have more negotiating power because they're usually the most qualified buyers for your specific business.

How Financing Affects Your Deal Structure

The buyer's financing method directly shapes the deal structure. Here's how to think about the most common scenarios.

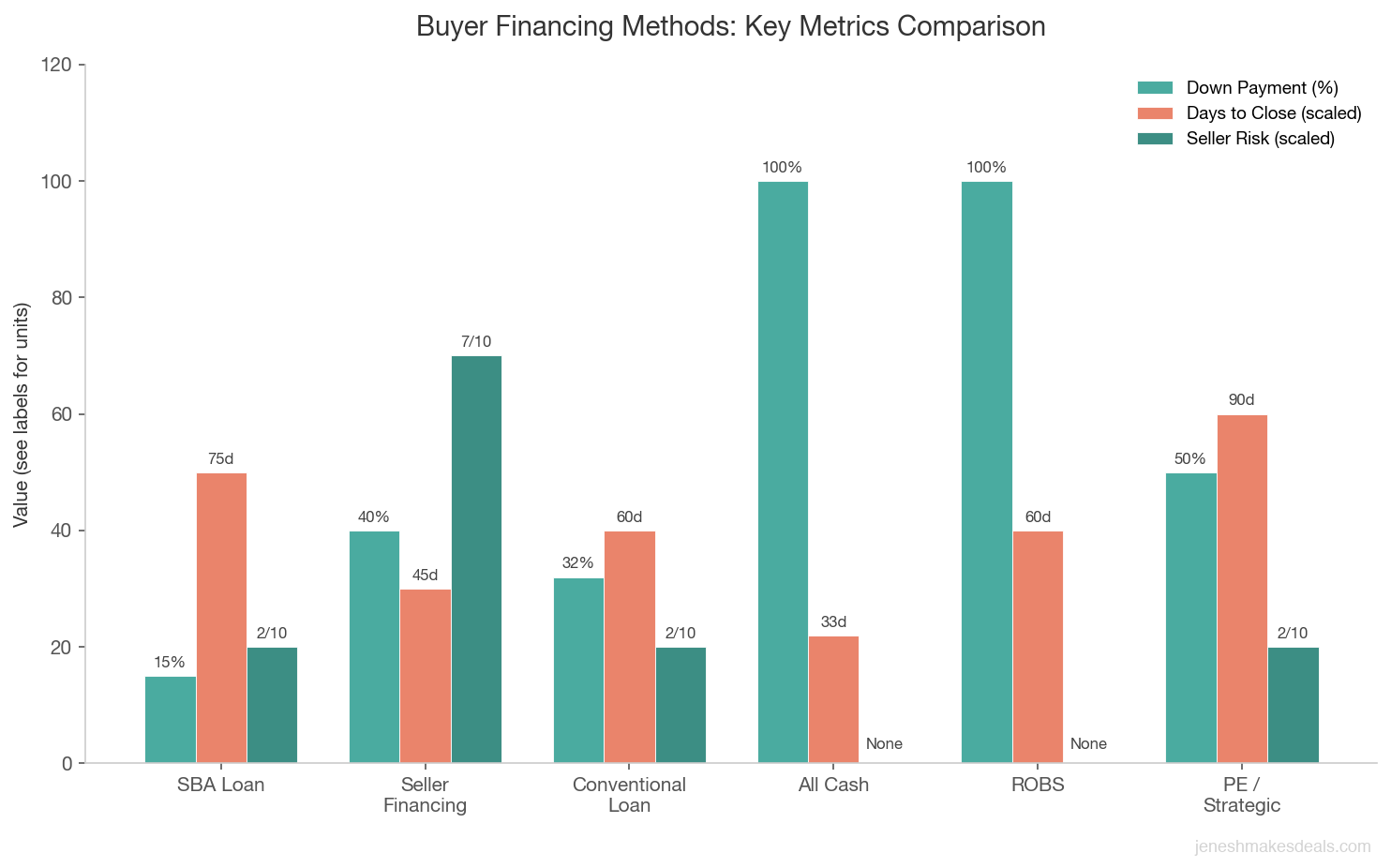

| Financing Method | Typical Down Payment | Seller Note | Time to Close | Seller Risk Level |

|---|---|---|---|---|

| SBA Loan | 10% to 20% | Sometimes (standby) | 60 to 90 days | Low (full payout at close) |

| Seller Financing | 30% to 50% | Yes (primary) | 30 to 60 days | Medium to high |

| Conventional Loan | 25% to 40% | Sometimes | 45 to 75 days | Low |

| All Cash | 100% | No | 21 to 45 days | None |

| ROBS | 100% (from retirement) | No | 45 to 75 days | None |

| PE/Strategic | Varies | Rarely | 60 to 120 days | Low |

SBA with seller note on standby. This is a common hybrid structure. The SBA lender provides the primary financing, but the lender may require a small seller note (typically 5% to 10% of the purchase price) that goes on "standby." This means the seller note payments don't start until the SBA loan is fully repaid or for a defined waiting period (usually 2 to 3 years). The standby note essentially increases the buyer's effective equity in the deal.

Seller financing with bank debt. Sometimes the buyer combines a conventional bank loan with a seller note. The bank takes the first lien position and the seller note is subordinated. This means if the buyer defaults, the bank gets paid first and you get whatever's left. Understand your position in the capital stack before agreeing to this structure.

Ready to explore your options? Contact us for a free consultation and we'll help you evaluate offers and understand the financing behind them.

Evaluating Offers Based on Financing

When you receive multiple offers on your business, comparing them isn't as simple as looking at the price. Here's a framework for evaluating offers with different financing structures.

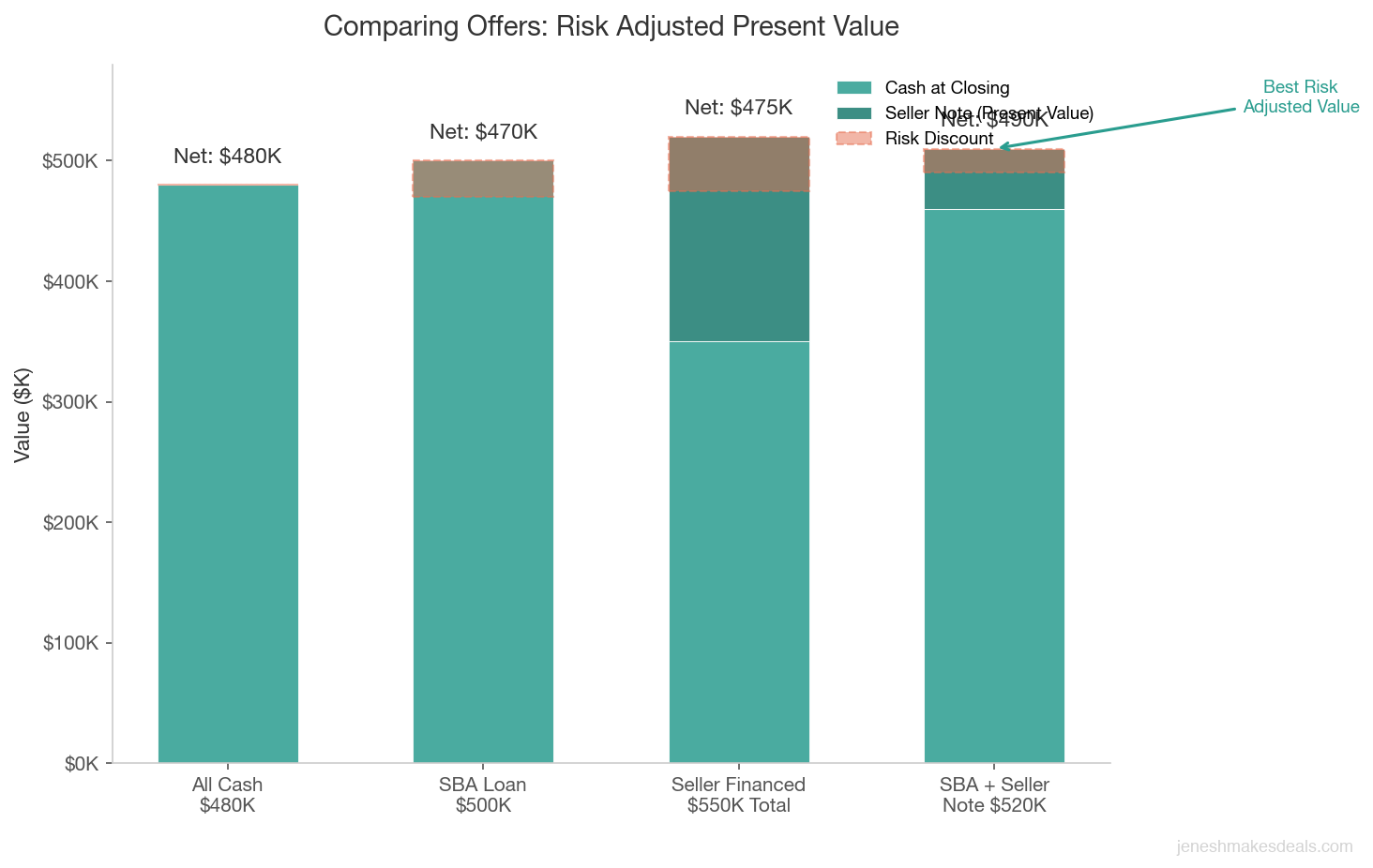

Certainty of close. An all cash offer at $480,000 is often worth more to you than an SBA financed offer at $500,000 because the cash deal is almost certain to close. The SBA deal has a 20% to 30% chance of falling through due to underwriting issues, appraisal shortfalls, or buyer qualification problems.

Time value of money. If one offer pays you $500,000 at closing and another pays $400,000 at closing plus $150,000 over five years with interest, the second offer has a higher total value on paper. But receiving $500,000 today is worth more than $550,000 spread over five years, especially when you factor in the risk that the buyer might default on the note.

Present value calculation. To compare offers with different financing structures, discount future payments back to present value. If the seller note carries 6% interest and you could earn 8% investing the proceeds, the present value of the seller financed portion is less than face value. Your accountant can run these calculations for you.

Buyer qualification. An offer from a buyer with 20 years of industry experience, strong credit, and SBA pre approval is worth more than an offer from a first time buyer with minimal savings and no financing commitment. The experienced buyer's offer is more likely to close.

Deal terms beyond price. Consider the non compete duration, transition period requirements, earnout provisions, and any other conditions. A clean, simple deal at a slightly lower price can be worth more than a complicated deal at a higher price when you factor in the time, stress, and risk of the complex structure.

What Sellers Can Do to Facilitate Financing

Making your business easier to finance expands your buyer pool and increases the likelihood of closing a deal. Here are practical steps.

Keep clean, organized financial records. Lenders base their decisions on your financials. Clean books with clear documentation of add backs make underwriting easier and faster. Messy or incomplete financials slow everything down and can cause loan denials.

Maintain a strong debt service coverage ratio. If your business generates enough cash flow to comfortably cover loan payments, more buyers can qualify for financing. A business that barely covers its debt service will struggle to attract financed buyers.

Secure a favorable lease. SBA lenders want to see a long term lease. Work with your landlord to extend your lease or negotiate renewal options before going to market. A lease with 10 or more years of remaining term eliminates one of the most common SBA deal killers.

Be open to seller financing. Offering some seller financing expands your buyer pool significantly. Many buyers, especially those who can't quite qualify for full SBA financing, need a seller note to bridge the gap. Your willingness to carry 10% to 20% of the purchase price can be the difference between selling and sitting on the market.

Prepare a comprehensive CIM. A well prepared confidential information memorandum gives lenders everything they need to evaluate the loan quickly. The more complete and professional your CIM, the faster the financing process moves.

Price the business appropriately. An overpriced business won't appraise at the asking price, which kills SBA deals. Price realistically based on comparable sales and industry multiples.

Seller Financing Negotiation Tips

If you're going to carry a seller note, negotiate smart terms that protect you.

Interest rate. Seller notes typically carry interest rates of 5% to 8%. Don't go below market rates. Your note is a real financial instrument and the interest should reflect the risk you're taking. In 2026, with prevailing rates where they are, 6% to 7% is a reasonable range.

Term length. Most seller notes run 3 to 7 years. Shorter terms mean you get paid back faster but create higher monthly payments for the buyer. Find a balance that the buyer can comfortably afford while not stretching the repayment too far into the future.

Amortization vs balloon. Some seller notes are fully amortizing (equal payments over the full term). Others have a shorter amortization schedule with a balloon payment at the end. A 7 year note with a 5 year amortization means the buyer makes payments as if the loan were being paid off over 7 years, but the remaining balance comes due in a lump sum after 5 years. Balloons give buyers lower payments but carry refinancing risk.

Security and collateral. Your note should be secured by a lien on the business assets. If the SBA has the first lien, you'll have a second lien. Also consider requiring a personal guarantee from the buyer.

Financial covenants. Include covenants that require the buyer to maintain insurance, provide regular financial statements, and not take on additional debt without your consent. These give you early warning if the business starts struggling.

Acceleration clause. If the buyer defaults, misses payments, or violates covenants, you should have the right to accelerate the entire remaining balance, making it due immediately.

The Tax Angle on Seller Financing

Seller financing has a significant tax benefit that many sellers overlook. Under IRS installment sale rules (Section 453), you can spread the recognition of capital gains over the years you receive payments. Instead of paying tax on the entire gain in the year of sale, you pay tax only on the portion of each payment that represents gain.

For example, if you sell your business for $1 million with $400,000 in cost basis, your gain is $600,000. If you receive $500,000 at closing and $500,000 over five years, you recognize $300,000 of gain in year one and $300,000 over the following five years (proportionally with each payment).

This can keep you in a lower tax bracket and reduce your overall tax liability compared to receiving the full amount in one year. Talk to your CPA about whether installment sale treatment makes sense for your situation.

Red Flags in Buyer Financing

As a seller, watch for these warning signs that the buyer's financing might not come through.

No pre approval or commitment letter. If the buyer says they're "working on financing" without a pre approval or term sheet from a lender, they may not be as far along as they claim. Request proof of financing before accepting an offer or at least make financing a contingency with a tight deadline.

Unrealistic financing assumptions. If the buyer's plan depends on getting a 90% LTV loan with below market rates and minimal documentation, the plan may not be realistic. Experienced buyers know what lenders require and set realistic expectations.

Multiple financing contingencies. If the buyer needs their house to sell, their investor to commit, and their SBA loan to close, that's three contingencies that could each kill the deal. Simpler financing structures are more likely to close.

The buyer keeps changing their financing plan. First they said cash, then SBA, then seller financing. Buyers who can't settle on a financing method may be struggling to qualify and testing different options. This is a yellow flag at minimum.

No down payment or equity. A buyer who wants 100% financing from you or from a lender is a high risk buyer. They have nothing at stake. If the business underperforms, they can walk away with no skin in the game. Insist on meaningful equity from the buyer.

When a buyer's financing plan keeps shifting, that is one of the clearest signs the deal is in trouble. Serious buyers have their financing figured out before they make an offer. If you are three weeks into due diligence and the buyer still cannot confirm how they are paying, it is time to have a direct conversation or start talking to your backup buyers.

The Bottom Line

The financing behind an offer is just as important as the number on the page. As a seller, you need to understand how SBA loans work, when seller financing makes sense, what risks different structures create, and how to evaluate offers that look different on paper but may end up being worth the same.

The best approach is to work with a broker and attorney who can help you evaluate each offer's financing structure and assess the likelihood of closing. Don't just take the highest number. Take the best deal, which means the right combination of price, terms, financing certainty, and post closing risk.

And if you're open to carrying some seller financing, you're making yourself attractive to a much larger pool of qualified buyers. Just make sure you negotiate the terms carefully and protect yourself with proper security, covenants, and default provisions.

Ready to sell? Contact us for a free consultation and we'll help you evaluate buyer offers and understand the financing behind each one.

Want to see what your business might be worth? Try our free business valuation calculator to get a quick estimate based on your industry's typical multiples.

Looking for more on funding options? Check out our funding resources for details on SBA loans and other financing programs.

Related Articles

April 8, 2026

How to Negotiate Seller Financing Terms That Protect You

Seller financing can get you a higher price and faster sale. But the terms matter more than the amount. Here's how to structure it right.

March 28, 2026

The Real Cost of Buying a Business in 2026

The purchase price is just the start. Here's every hidden cost buyers miss, from SBA fees to working capital, and how to budget right.

March 20, 2026

Can You Use Your 401k to Buy a Business? How ROBS Works

ROBS lets you use retirement funds to buy a business without early withdrawal penalties or taxes. Here's exactly how it works and what it costs.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.