I've spent the last decade watching business buyers make the same mistake over and over. They focus so hard on negotiating the purchase price that they completely blindside themselves with costs that show up later. A buyer will negotiate a $500,000 business down to $475,000 and feel like they won, then get hit with $80,000 in costs they didn't see coming.

The truth is brutal: the purchase price is maybe 70% of what you'll actually spend. Everything else gets tucked away in fine print, broker agreements, and loan documents. In this post, I'm breaking down every expense you need to budget for when buying a business. No fluff, no surprises.

The Purchase Price Is Just the Beginning

Let's start with the fundamentals. You've found a business listed at $500,000. That's what you're thinking about paying, right? Wrong. That $500,000 is the beginning of a much longer financial journey.

When I talk to buyers, they usually understand that they'll need to get a loan to cover most of the purchase price. What they don't understand is that getting the money costs money. A lot of money. The fees, closing costs, and professional services you'll need just to complete the transaction can add 15% or more to your total cost.

Let's say you negotiate that $500,000 business down to $480,000. You feel like you're winning. But the real cost to close that deal is going to be closer to $550,000 to $580,000 when you add everything up. That's not pessimism. That's math.

Broker's note: I tell every buyer the same thing: take your purchase price and multiply it by 1.4. That's your real budget. If you can't afford 140% of the asking price, you're looking at the wrong deal.

Here's what most buyers miss: they think about the down payment, the loan amount, and the monthly payments. But there are at least a dozen other costs between signing the offer and actually running your new business. Each one seems small. Together, they're significant.

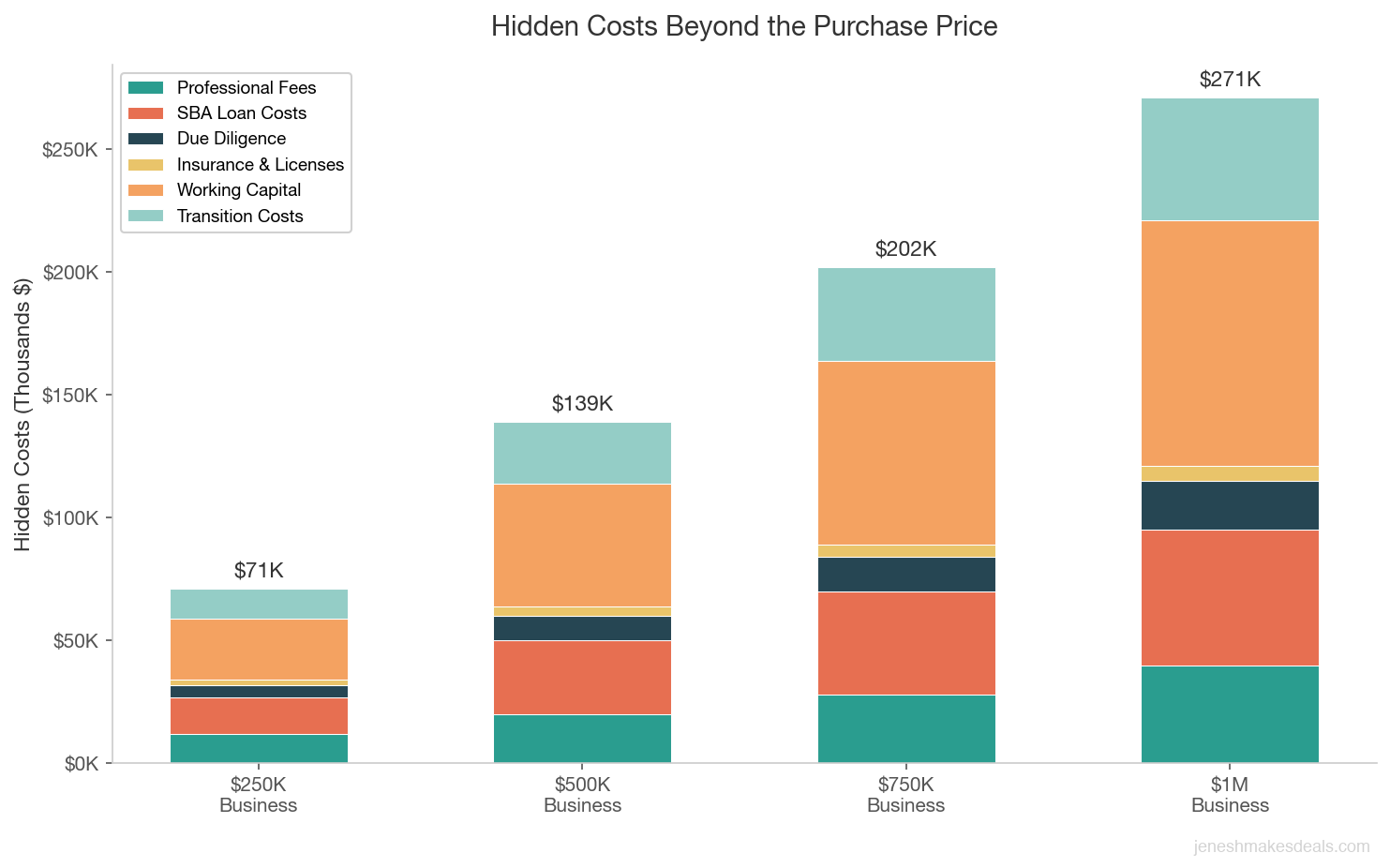

Professional Fees That Add Up Fast

The first place money disappears is in professional fees. You need lawyers. You need accountants. You probably need a business broker if you're buying through the market. These costs are real, and they're not negotiable.

Broker fees are typically 4-12% of the sale price. If you're buying a business under $1 million, expect to pay 8-12%. On a $500,000 purchase, that's $40,000 to $60,000. This fee is usually paid by the seller, but here's the thing: it gets built into the price. The seller factors in what they'll pay the broker when they list the business. So you're paying it either way.

Legal fees range from $5,000 to $15,000 for a small to mid market business purchase. Your attorney needs to review the sale agreement, look at contracts, check for liens and liabilities, and help you understand what you're actually buying. This isn't optional. A bad purchase agreement can cost you way more than you save by skipping the lawyer.

Accounting and CPA review typically runs $3,000 to $10,000. Your CPA needs to review the seller's tax returns, verify the financial statements you've been shown, and help you understand the real profitability. Many buyers skip this, and then they buy a business that's nowhere near as profitable as they thought.

Quality of Earnings reports (if the deal is large enough to warrant one) cost $10,000 to $30,000. These deep dives into the business's actual earnings are especially important if you're buying something that claims high profitability. A QoE report can save you from buying a business that's been artificially propped up.

When you add up legal, accounting, due diligence, and other professional services, you're looking at $15,000 to $25,000 for a smaller business purchase. For larger deals, this can push past 15% of the purchase price.

SBA Loan Costs Most Buyers Don't Budget For

About 60% of small business purchases are financed with SBA loans. If you're going the SBA route, you need to understand that the loan itself has costs built in.

SBA guarantee fees are 2% to 3.75% of the guaranteed portion of your loan. On a $400,000 SBA loan, that's $8,000 to $15,000. This fee is usually paid upfront and rolled into your loan, so you're paying interest on it for 10 years.

SBA closing costs typically run 2% to 5% of the total loan amount. On a $400,000 loan, that's $8,000 to $20,000. These cover appraisals, title searches, filing fees, and bank processing.

Lender origination fees and points vary by lender, but many charge 1% to 2% of the loan amount. That's another $4,000 to $8,000.

All of these fees are rolled into your monthly loan payment. They don't feel real in the moment because you're not writing a check. But you're paying them with interest over 10 years. On a $400,000 loan with these fees, you could be paying an extra $50,000+ in total cost.

If you're putting down 10% ($50,000) and getting seller financing for another 10% ($50,000), you're reducing the bank loan to $400,000. That changes the fee structure. But the SBA requires a minimum 10% equity injection, so you've got to have that cash.

Due Diligence Isn't Free

Before you even sign the papers, you need to know what you're buying. Due diligence costs money, and most buyers underestimate it.

Basic due diligence (reviewing contracts, customer lists, supplier agreements, and lease terms) costs $2,500 to $5,000 if you're doing it yourself with a lawyer's help. If you hire a dedicated due diligence firm, expect $10,000 to $30,000.

Environmental assessments (Phase I and sometimes Phase II) cost $1,500 to $3,000 for a basic check. If the business involves manufacturing or any chemical handling, Phase II can cost $5,000+. This is critical if you're buying a business with a physical location.

Background checks and litigation searches cost $500 to $1,500 but can uncover lawsuits, liens, or regulatory issues you didn't know about.

Customer concentration analysis is crucial. If 30% of revenue comes from one customer, you need to know that. Analyzing customer data and retention risk costs $2,000 to $5,000.

For a typical $500,000 business purchase, I'd budget $5,000 to $15,000 for due diligence. This is not the time to cut corners. A bad due diligence process is how you end up buying a business with hidden problems.

Key takeaway: The buyers who get burned aren't the ones who overspend on due diligence. They're the ones who skip it to save $5,000 and end up losing $50,000 on problems they could have caught.

Insurance, Licenses, and Permits

Once you own the business, you need insurance. Immediately. Not the insurance the old owner had. New insurance for you as the owner.

General liability insurance typically costs $500 to $2,000 per year depending on the industry. A law firm or consulting business might be $800/year. A construction or retail business could be $2,000+.

Errors and omissions insurance (if you're in a professional services business) averages around $88 per month, or $1,056 per year. This is critical for consultants, brokers, and professional service providers.

Property insurance (if you own the building or have significant equipment) varies wildly. Budget at least $1,000 to $3,000 annually.

Workers' compensation insurance is mandatory if you have employees. The cost depends on the industry and payroll, but expect $2,000 to $5,000 annually for a small business with 3-5 employees.

Business licenses and permits can cost $25 to $150+ depending on your industry and state. Some businesses need health permits ($200-$500), liquor licenses ($500-$5,000+), or contractor licenses ($200-$1,000).

For the first year, budget $2,000 to $5,000 in insurance and licensing costs. Some of this was paid by the previous owner, so you're not inheriting their policies. You need new ones in your name.

Working Capital and Day One Cash Needs

Here's where I see buyers get really surprised. You buy a business, and then you run out of cash in month three.

Most small businesses operate on razor thin margins. You've got customer receivables (money owed to you), inventory, accounts payable, and payroll. If you don't have enough cash to bridge the gap between when you pay for inventory or payroll and when customers actually pay you, you're in trouble.

Minimum working capital should be 10% to 20% of your first year revenue. If the business does $500,000 in annual revenue, you need $50,000 to $100,000 in liquid cash reserves just to operate.

Inventory is a killer. Most retail and product based businesses have inventory that's 28% to 30% of total company assets. If you buy a $500,000 business and 30% of assets is inventory ($150,000), you need to be ready to maintain that inventory. If inventory turns every 60 days and you need to reorder before customers pay you, you need working capital.

Accounts receivable float is the cash you need to bridge the gap between buying inventory and getting paid by customers. If your customers pay in 30 days, you need to float 30 days of inventory and payroll costs.

A common structure is this: you put down 10% of the purchase price, seller financing covers another 10%, and the bank covers 80%. But you still need to bridge working capital. Many buyers find out they need to overfund their down payment or set aside additional capital just to operate the business.

Budget an extra 5% to 10% of the purchase price in working capital on day one. For a $500,000 business, that's $25,000 to $50,000 in cash reserves.

The First Year Surprises Nobody Warns You About

You've closed. You own the business. Now the real costs start.

Transition and training costs are usually built into the seller's time commitment. The seller typically stays for 4 to 12 weeks helping you transition (and sometimes up to 12 months). During this time, you're paying their wage, sometimes a bonus, and you're probably overstaffed.

Seller transition bonus often runs 5% to 10% of the purchase price, paid over the transition period. On a $500,000 purchase, that could be $25,000 to $50,000 in additional transition costs.

Rebranding costs are huge if you want to change the business's name or brand. A basic rebrand (new logo, updated website) costs $10,000 to $75,000. A full rebrand with new signage, uniforms, and marketing materials costs $50,000 to $100,000+.

Software and system changes to your point of sale, accounting, or customer management systems can cost $5,000 to $20,000 depending on complexity.

Increased payroll during transition because you're learning the business, you might need to hire a consultant or bring in a manager temporarily. Budget $2,000 to $5,000 per month for 2-3 months.

Customer acquisition if you lose customers during the transition. The average customer acquisition cost is around $29 per customer in 2025, but this varies wildly by industry. If you lose 20 customers during transition at an $8,000 lifetime value each, you're out $160,000 in lifetime revenue.

In your first year, expect $10,000 to $50,000 in unexpected transition and operational costs beyond your normal operating expenses.

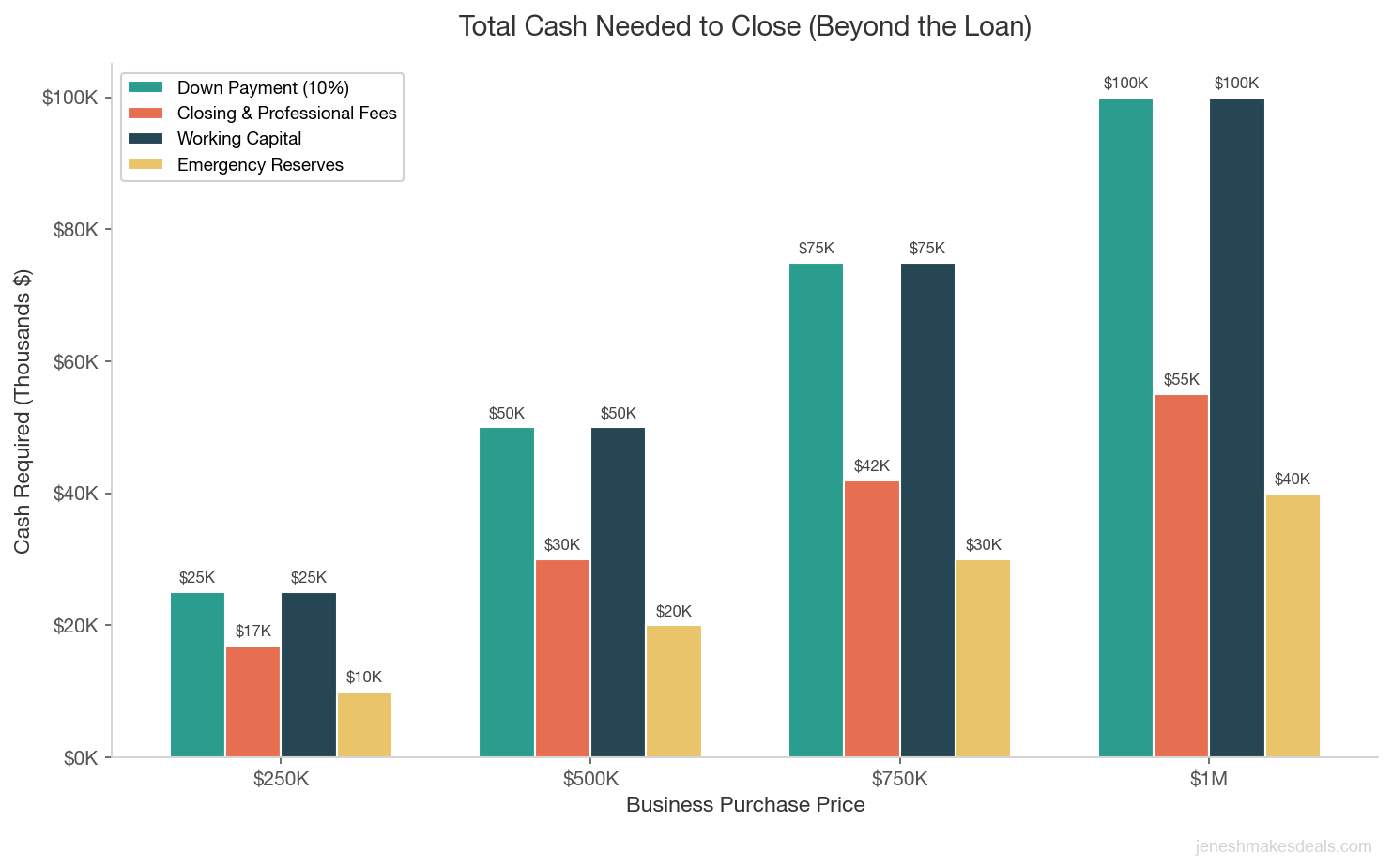

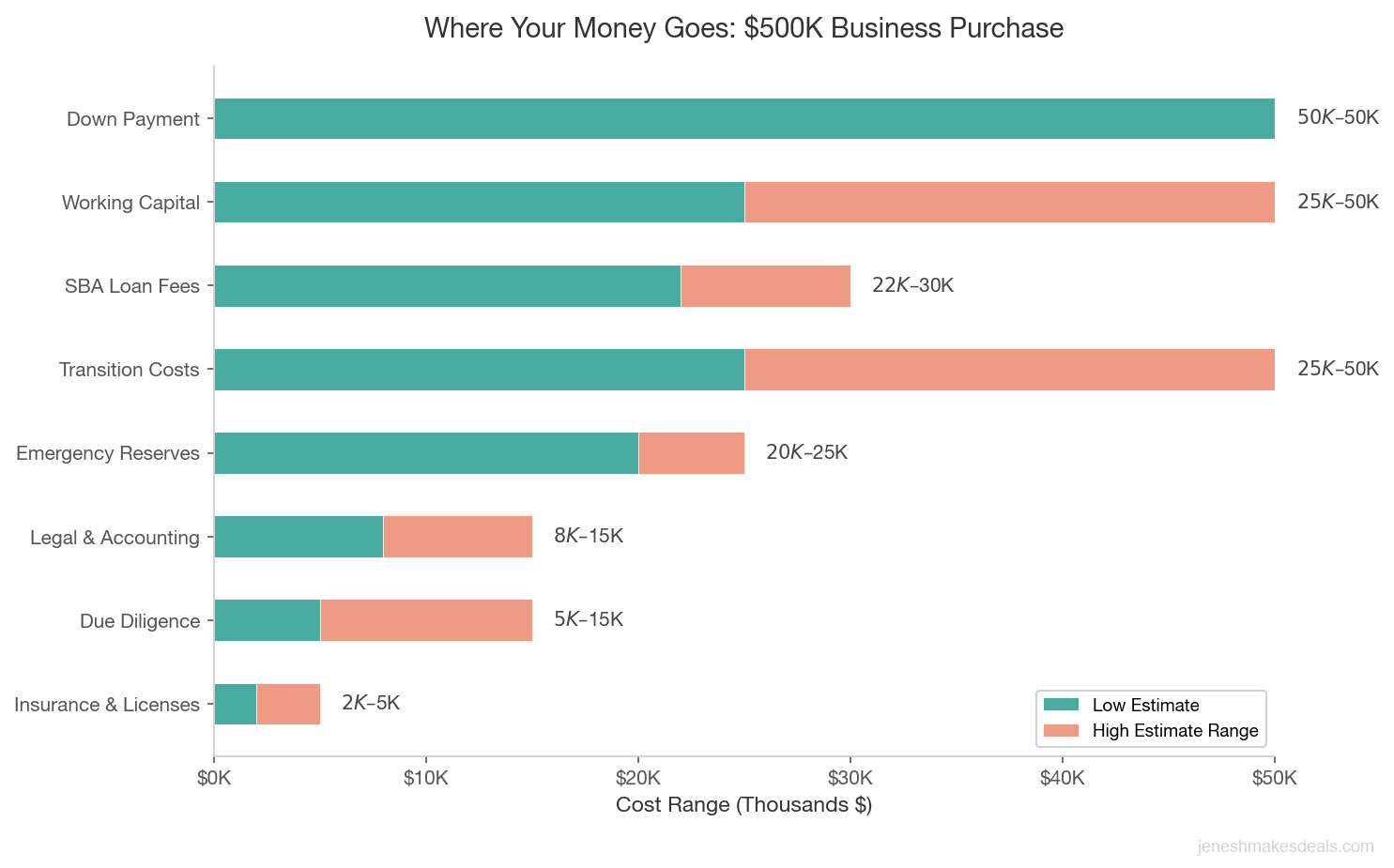

A Real Cost Breakdown: Buying a $500K Business

Let me put real numbers to this. Here's what it actually costs to buy a $500,000 business:

| Cost Category | Low Estimate | High Estimate |

|---|---|---|

| Purchase Price | $500,000 | $500,000 |

| Down Payment (10%) | $50,000 | $50,000 |

| Broker Commission (8%) | $40,000 | $40,000 |

| Legal & Accounting | $8,000 | $15,000 |

| Due Diligence | $5,000 | $15,000 |

| SBA Guarantee Fee (2.5%) | $10,000 | $10,000 |

| SBA Closing Costs (2%) | $8,000 | $8,000 |

| Lender Fees (1%) | $4,000 | $8,000 |

| Insurance & Licenses (first year) | $2,000 | $5,000 |

| Working Capital (5%) | $25,000 | $25,000 |

| Transition Bonus (5%) | $25,000 | $25,000 |

| Rebranding (if needed) | $0 | $50,000 |

| Emergency Fund (10%) | $20,000 | $25,000 |

| TOTAL CASH NEEDED | $197,000 | $276,000 |

| TOTAL COST (with financing) | $677,000 | $776,000 |

You're buying a $500,000 business, but your total cost is $677,000 to $776,000. That's 35% to 55% more than the purchase price.

The down payment and cash needed is $197,000 to $276,000. Most buyers plan for $50,000 down and think they're set. In reality, they need another $147,000 to $226,000 in accessible capital.

Common Mistakes Buyers Make When Budgeting

I see these mistakes constantly. Learn from others' pain.

Mistake #1: Only budgeting for the down payment. Buyers think "I need 10% down, that's $50,000." They don't realize they need another $100,000+ in accessible capital for closing costs, working capital, and first year surprises. You can't borrow most of these costs from the bank. You need cash.

Mistake #2: Assuming the seller's insurance covers your transition. Insurance policies don't transfer. You need your own policy effective on day one of ownership. Many buyers have a 30-day gap where they're uninsured.

Mistake #3: Not budgeting for working capital. Buyers assume they can operate on thin margins the same way the seller did. But you don't have the seller's relationships and cash flow history. You need a buffer.

Mistake #4: Forgetting about accounts payable transitions. If the business has 30-day payment terms with suppliers, you'll need to float that cash yourself until the system adjusts.

Mistake #5: Underestimating transition time and cost. The seller says "two weeks, I'll help you out." Reality: it's two to three months minimum, and you're overstaffed the whole time.

Mistake #6: Not factoring in customer turnover during transition. Some customers leave when ownership changes. Some suppliers demand payment upfront instead of net 30. Budget for this.

Mistake #7: Skipping professional help to save money. Buyers skip the CPA review or the attorney and then buy a business that's been cooked. This costs more than the $5,000 you saved.

Mistake #8: Not including an emergency fund. Life happens. A key employee quits. Equipment breaks. You need 10-20% of total costs in reserve.

Warning for buyers: If you're stretching to afford the down payment alone, you're not ready to buy. The down payment is less than half of the cash you'll actually need. Go in underfunded and you'll be forced to make bad decisions in month three.

What To Do Next

Now you know what you're really up against. Here's how to move forward.

First, calculate your actual capital needs. Don't just think about the down payment. Use the breakdown above to calculate what you actually need for your target business. If you're looking at a $300,000 business, multiply the percentages. If you're looking at a $1,000,000 business, adjust accordingly.

Second, talk to a lender before you start shopping. Your bank or SBA lender can tell you exactly what your total cost will be with their rates and fees. They can model out different scenarios (10% down vs. 15% down, different seller financing amounts, etc.). Getting pre-approval isn't just about getting a number. It's about understanding the real cost.

Third, work with a broker or advisor who understands the full cost picture. A good business broker or M&A advisor has done this a hundred times. They know what the real costs are in your industry. They can help you negotiate a purchase price that accounts for transition costs and working capital needs.

Want to see what a business is actually worth before you commit? Use our free business valuation calculator to get a quick estimate and understand the real numbers.

Ready to talk numbers? Contact us for a free consultation and we'll walk you through the real costs for your deal. I'll show you the exact breakdown for your target business.

Need funding to cover all these costs? Check out our unsecured funding programs that provide up to $500,000 with no collateral. Many buyers use this to bridge the gap between their down payment and their total working capital needs.

The real cost of buying a business is higher than most people think. But if you budget for it correctly and have the capital to support it, you're setting yourself up for success. I've seen hundreds of buyer succeed because they went in with eyes open about the real costs. I've seen just as many struggle because they were underfunded and surprised.

Don't be the buyer who gets blindsided. Do the math. Have the conversations with your lender and your advisor. Get the capital you actually need. The difference between success and failure in the first year often comes down to this simple step.

Related Articles

April 19, 2026

What Sellers Need to Know About Buyer Financing Options

How your buyer pays for your business directly affects your deal. Here's what every seller should understand about financing.

April 8, 2026

How to Negotiate Seller Financing Terms That Protect You

Seller financing can get you a higher price and faster sale. But the terms matter more than the amount. Here's how to structure it right.

March 20, 2026

Can You Use Your 401k to Buy a Business? How ROBS Works

ROBS lets you use retirement funds to buy a business without early withdrawal penalties or taxes. Here's exactly how it works and what it costs.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.