If you're selling your business in 2026, there's a good chance the buyer is going to ask you to carry a note. That's not a bad thing. In fact, roughly 60 to 80% of small business transactions involve some form of seller financing. It's one of the most common deal structures out there, and for good reason.

But here's what I tell every seller I work with: the amount of the note matters far less than the terms. I've seen sellers agree to carry $200,000 on a $500,000 deal and walk away protected, earning solid interest income over three years. I've also seen sellers carry $150,000 on a similar deal and end up in a nightmare because the terms were poorly written and gave them almost no recourse when the buyer stopped paying.

The difference between those two outcomes? The specific terms in the promissory note.

This post is written for sellers. If you're going to finance part of your deal, I want you to know exactly what to negotiate, what numbers are reasonable, and how to protect yourself if things go sideways.

Why Buyers Ask for Seller Financing (and Why You Should Consider It)

Before we get into the specifics, let's talk about why this is worth your time.

Buyers ask for seller financing because banks are tough. SBA loans require 680+ credit scores, 10 to 20% down payments, and 60 to 90 days of underwriting. Many qualified buyers, people who would run your business well and make every payment on time, can't clear those hurdles. Seller financing fills that gap.

But the benefits for you as the seller are real too.

You'll get a higher price. Sellers who offer financing typically sell for 10 to 20% more than those who demand all cash at closing. On a $500,000 business, that's an extra $50,000 to $100,000 in your pocket. The math is simple: more buyers can afford your business when financing is available, which creates more competition and pushes up the price.

You'll sell faster. Businesses that require all cash or bank only financing can sit on the market for 12 to 18 months. When you offer seller financing, you expand the buyer pool dramatically. I've seen seller financed businesses go under LOI in 3 to 4 months compared to 10+ months for comparable businesses with no financing option.

You'll earn interest income. A $200,000 seller note at 8% interest over five years generates roughly $48,000 in interest. That's money you wouldn't see in an all cash deal.

You signal confidence. When you're willing to carry a note, buyers read that as you believing the business will continue to perform. It builds trust and reduces friction in negotiations.

Sellers who offer financing typically sell for 10 to 20% more than all cash sellers and close 2 to 3 times faster. The interest income on a $200,000 note at 8% over five years adds nearly $48,000 to your total proceeds.

The catch? You need to negotiate terms that actually protect you. Let's get into the specifics.

The Key Terms Every Seller Must Negotiate

A seller financing arrangement comes down to a promissory note, a legal document that spells out exactly how and when the buyer pays you. Here are the terms that matter most:

- Down payment amount (how much cash you get at closing)

- Interest rate (the cost of money over time)

- Term length (how long you'll be waiting for full payment)

- Payment structure (monthly, balloon, interest only periods)

- Security and collateral (what you can seize if the buyer defaults)

- Default provisions (what happens when payments are missed)

- Non compete terms (how your non compete ties to the note)

Each one of these is negotiable. Let's walk through them.

Down Payment: Why You Should Never Go Below 30%

The down payment is the single most important term in a seller financing deal. It determines how much skin the buyer has in the game, and it's your best protection against default.

Here's the reality: buyers who put down less than 30% of the purchase price default at significantly higher rates than buyers who put down 50% or more. When a buyer has $50,000 invested in a $500,000 business, it's much easier for them to walk away. When they have $250,000 invested, they'll fight to make it work.

What the numbers look like

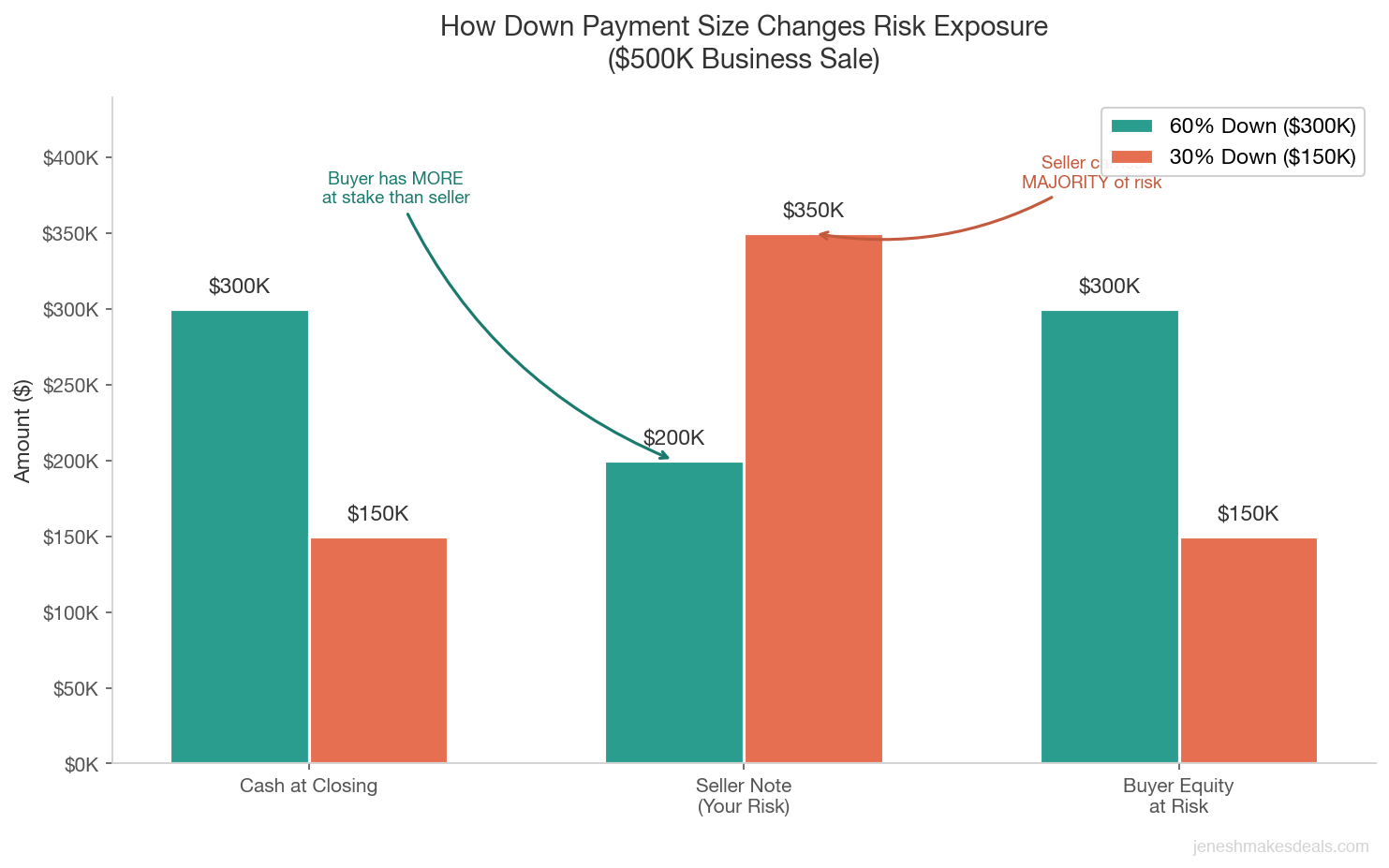

$500,000 business, 60% down ($300,000):

- You walk away from closing with $300,000 in cash

- Seller note: $200,000

- Your risk exposure: $200,000

- Buyer's equity at risk: $300,000 (they won't walk away from that)

$500,000 business, 30% down ($150,000):

- You walk away from closing with $150,000 in cash

- Seller note: $350,000

- Your risk exposure: $350,000

- Buyer's equity at risk: $150,000 (much easier to abandon)

See the difference? With a 60% down payment, the buyer has more at stake than you do. With a 30% down payment, you're carrying the majority of the risk.

My standard recommendation for sellers: push for 50% or more down. In practice, most deals land between 40 and 60% down. If a buyer can't bring at least 30% to the table, I'd question whether they're financially ready to own the business.

There are exceptions. If you've had the business listed for a year and this is your best offer, a 30% down payment with strong protective terms might make sense. But I'd want to see an excellent personal guarantee, solid collateral, and a shorter note term to offset the risk.

Thinking about selling and wondering what your business might be worth? Start with our free valuation calculator to get a baseline number before you start negotiating terms.

Interest Rates: What's Fair in 2026

The interest rate on your seller note should compensate you for two things: the time value of money (you could invest that cash elsewhere) and the risk of buyer default (this is an unsecured or partially secured loan to someone running a small business).

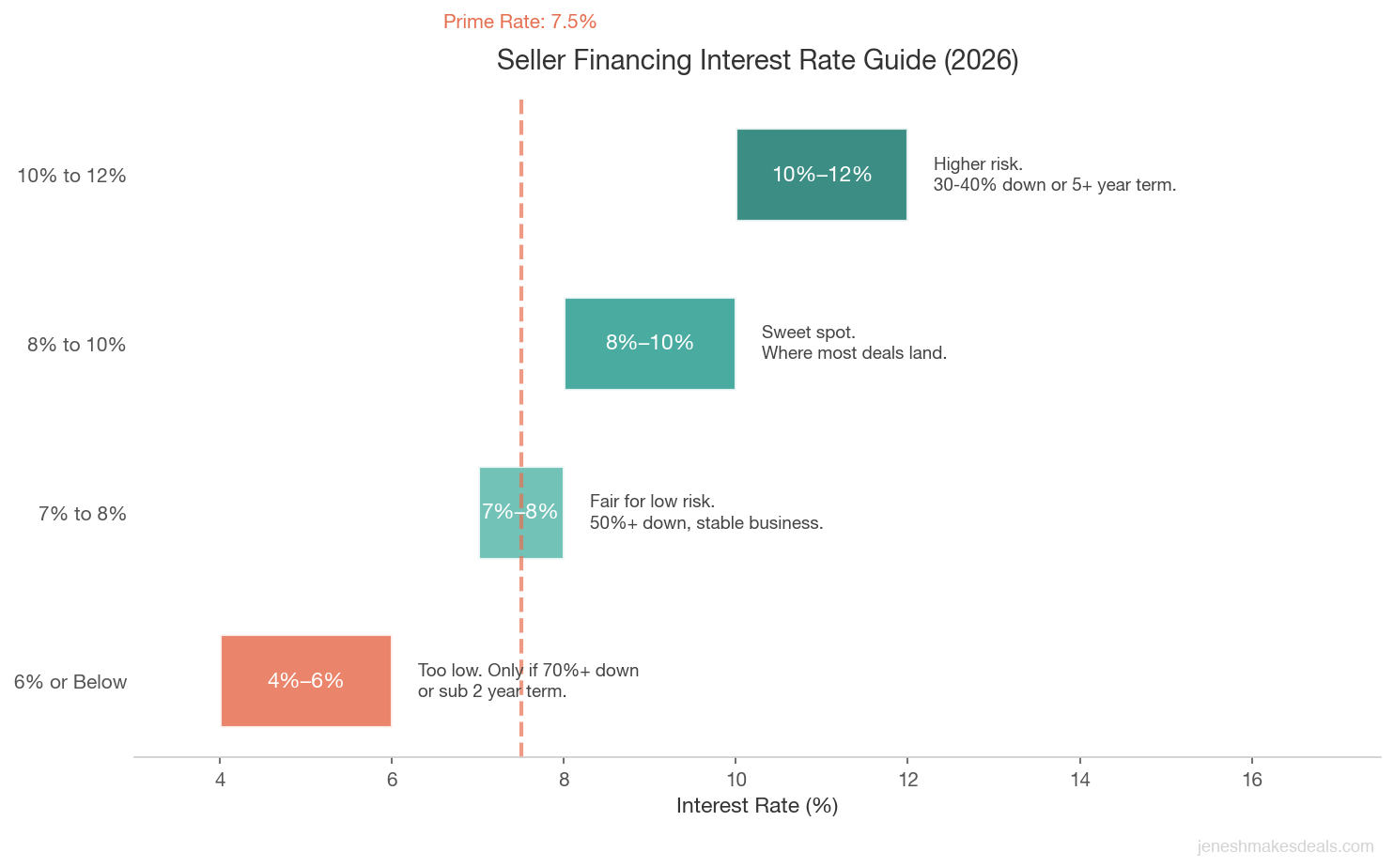

Current benchmarks

As of early 2026, the prime rate sits at around 7.5%. Most seller financing deals price between prime + 1% and prime + 3%, which puts the typical range at 8.5% to 10.5%.

Here's how I think about it:

| Rate Range | Risk Level | When It Makes Sense |

|---|---|---|

| 6% or below | Too low | Only if 70%+ down payment or note term under 2 years |

| 7% to 8% | Low risk | Buyer puts 50%+ down, strong financials, stable business |

| 8% to 10% | Sweet spot | Where most deals land. Fair compensation for risk |

| 10% to 12% | Higher risk | Down payment is 30 to 40%, longer term, or business risk factors |

Fixed vs variable

I almost always recommend a fixed rate for seller notes. Here's why: a variable rate introduces uncertainty for both you and the buyer. If rates drop, your income decreases. If rates spike, the buyer's payments may become unmanageable, increasing the risk of default. A fixed rate gives both parties predictability.

If you do go variable, cap it. A rate floor of 7% and a ceiling of 12% is reasonable. That way you're protected on the downside and the buyer isn't crushed if rates spike.

The interest rate as a negotiation tool

Interest rate and purchase price often trade off against each other. A buyer might accept a higher purchase price if you offer a lower interest rate, because their monthly payment stays manageable. Conversely, you might accept a slightly lower price in exchange for a higher rate that generates more interest income over the life of the note.

I worked on a deal last year where the seller wanted $600,000. The buyer countered at $550,000. We settled at $585,000 with a 7.5% interest rate instead of the 9% the seller originally wanted. Both sides felt good about it. The seller got closer to their price, and the buyer's monthly payment was nearly identical to what they'd have paid at $550,000 and 9%.

Term Length and Payment Structure

The term length determines how long you'll be tied to this deal, receiving monthly payments and hoping the business keeps generating enough cash to cover them.

Typical term lengths

- 2 to 3 years: Short and seller friendly. You get paid off quickly. Best for deals with high down payments (60%+) where the note amount is relatively small.

- 3 to 5 years: The most common range. Balances the buyer's cash flow needs with the seller's desire to get paid off.

- 5 to 7 years: Buyer friendly. Monthly payments are lower, but you're exposed to risk for a longer period. I'd only recommend this if the interest rate is high enough to compensate and the collateral is strong.

- 7+ years: Avoid this. Too much can go wrong over seven or more years. The buyer could mismanage the business, the industry could shift, or personal circumstances could change. I'd push back hard on anything beyond seven years.

Monthly payments

Most seller notes use standard amortization, meaning equal monthly payments that include both principal and interest. On a $200,000 note at 8% over five years, the monthly payment is about $4,055. That's straightforward and predictable for both sides.

Balloon payments

A balloon payment means the buyer makes smaller monthly payments for a set period, then pays the remaining balance in a lump sum. For example: monthly payments based on a 10 year amortization, with a balloon payment of the remaining balance due at year five.

Balloon payments can work well for sellers. They reduce the buyer's monthly obligation (making the deal easier to close) while still getting you fully paid by a specific date. The assumption is that the buyer will refinance the balloon with a bank loan once they have a track record running the business.

The risk? If the buyer can't refinance when the balloon comes due, you could be stuck renegotiating or pursuing legal action. If you agree to a balloon, make sure the note includes clear default provisions for missed balloon payments.

Interest only periods

Some buyers ask for 6 to 12 months of interest only payments to ease the cash flow burden during the transition period. On a $200,000 note at 8%, that's about $1,333 per month in interest only payments versus $4,055 for fully amortizing payments.

I'm OK with a short interest only period (6 months max) if the buyer has a legitimate reason, like they need time to stabilize operations during the transition. Beyond six months, I'd push back. Interest only payments mean you're not getting any principal back, and the buyer isn't building equity in the note.

The 3 to 5 year term is the sweet spot for most seller notes. Anything beyond 7 years exposes you to too many variables: industry shifts, buyer mismanagement, and changing personal circumstances. Keep it short and protect yourself.

Want to model different financing scenarios? Use our deal structuring calculators to see how down payment, interest rate, and term length affect your total proceeds.

Security and Collateral: What Protects You if the Buyer Defaults

This is where many sellers make their biggest mistake. They negotiate the price, down payment, and interest rate, but they don't pay enough attention to what happens if the buyer stops paying.

UCC lien on business assets

At minimum, you should have a UCC (Uniform Commercial Code) lien on all business assets. This means if the buyer defaults, you have a legal claim on the equipment, inventory, accounts receivable, and other business assets. Your attorney will file a UCC-1 financing statement to establish this lien.

If there's also an SBA loan involved, the bank will have a first position lien. Your seller note will be in second position, meaning the bank gets paid first from any liquidated assets. This is important to understand because in a default scenario, there may not be enough asset value to cover both the bank and your note. That's one more reason to insist on a strong down payment.

Personal guarantee

Always require a personal guarantee from the buyer. A personal guarantee means the buyer is personally liable for the note, not just the business entity. If the business fails and the assets aren't worth enough to cover your note, you can pursue the buyer's personal assets.

A personal guarantee without assets behind it isn't worth much, so ask your attorney to have the buyer provide a personal financial statement. You want to know they have assets (home equity, savings, other investments) that give the guarantee teeth.

Stock pledge or membership interest pledge

If you're selling the business as a stock or membership interest sale (rather than an asset sale), the buyer should pledge their ownership interest in the company as collateral. This means if they default, you can take back ownership of the business.

This is powerful protection, but it requires careful legal structuring. Make sure your attorney includes specific provisions about how the ownership transfer works in a default scenario.

Life and disability insurance

Here's one that sellers often overlook. If the buyer dies or becomes disabled, who pays the note? Require the buyer to maintain a life insurance policy and disability insurance policy with you as the beneficiary, at least equal to the outstanding balance of the note.

A $200,000 term life policy for a healthy 40 year old costs roughly $25 to $40 per month. That's a small expense for the buyer and critical protection for you.

Default Provisions: What Happens When Payments Are Late

Your promissory note needs crystal clear language about what constitutes a default, what grace period the buyer gets, and what your remedies are.

Defining default

Default isn't just about missed payments. Your note should define default to include:

- Missing a monthly payment by more than 10 to 15 days (grace period)

- Failing to maintain required insurance coverage

- Filing for bankruptcy

- Selling or transferring the business without your consent

- Material breach of the non compete agreement (if applicable)

- Failing to pay the balloon payment when due

- Allowing liens or judgments to attach to the business assets

Cure period

A cure period gives the buyer a window to fix the default before you can take action. Typical cure periods are 10 to 30 days. I recommend 15 days for missed payments. That's enough time for a buyer who simply forgot or had a processing delay, but not so long that a struggling buyer can string you along.

Acceleration clause

An acceleration clause is your most important remedy. It states that if the buyer defaults and fails to cure within the specified period, the entire remaining balance of the note becomes due immediately. Without an acceleration clause, you'd have to sue for each missed payment individually, which is expensive and time consuming.

With acceleration, you demand full payment. If the buyer can't pay, you pursue foreclosure on the collateral or exercise your other remedies.

Late payment penalties

Include a late payment fee of 5% of the monthly payment amount for any payment received more than 10 days after the due date. On a $4,055 monthly payment, that's a $203 late fee. It's not punitive, but it creates an incentive for the buyer to pay on time.

Right to inspect

Your note should give you the right to inspect the business's financial records (quarterly or annually) to verify that the business is performing adequately. If you see revenue declining 30% or more, you want to know about it before the buyer starts missing payments.

Have questions about structuring your deal? Schedule a free consultation and I'll walk you through the terms that make sense for your specific situation.

Non Compete Considerations Tied to Seller Financing

Nearly every business sale includes a non compete agreement from the seller. Typically, the seller agrees not to compete in the same industry within a defined geographic area for a set number of years (usually 3 to 5 years).

Here's what most sellers don't think about: what happens to your non compete if the buyer defaults on the seller note?

If the buyer stops paying you, are you still bound by a non compete that prevents you from earning a living in your industry? That doesn't seem fair, and it shouldn't be.

Tie the non compete to the note

I always recommend including language in both the non compete agreement and the purchase agreement that ties the non compete to the seller note. Specifically: if the buyer defaults on the promissory note and fails to cure within the specified period, the non compete agreement terminates automatically.

This creates a powerful incentive for the buyer to keep paying. They know that if they default, not only will you pursue the collateral, but you'll also be free to compete directly with them.

Common non compete terms with seller financing

- Duration: 3 to 5 years from closing, but terminates if the buyer defaults on the note

- Geographic scope: Reasonable radius (typically 25 to 50 miles for local businesses)

- Activity scope: Narrowly defined. Covers the specific type of business sold, not your entire professional life

- Carve outs: If you have other business interests that aren't directly competitive, make sure they're explicitly excluded

Your attorney should draft the non compete with these seller financing considerations in mind. Don't rely on a generic template.

Two Real Scenarios: How Different Terms Change Everything

Let's look at the same $500,000 business sale structured two different ways to see how much the terms matter.

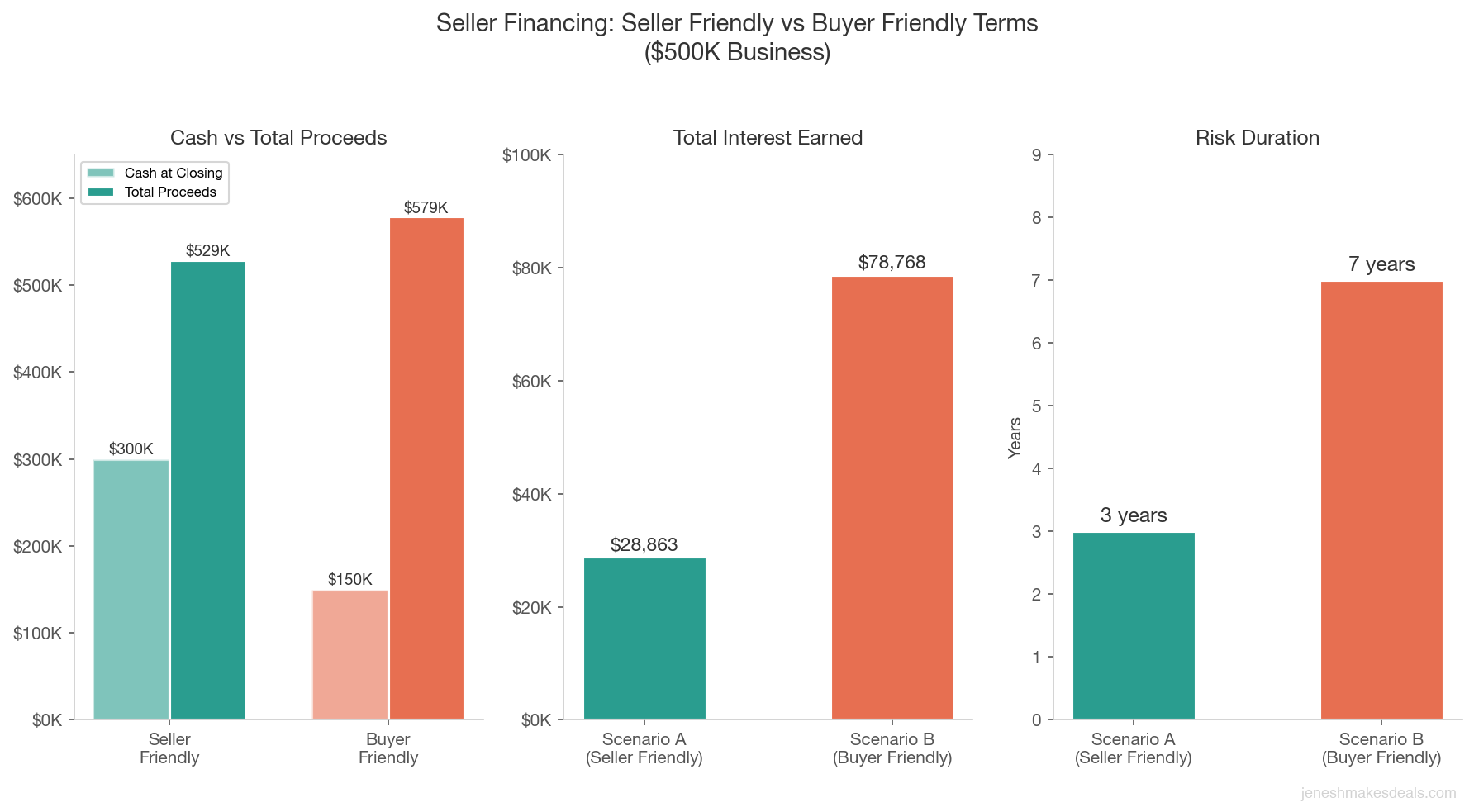

Scenario A: Seller Friendly Terms

- Purchase price: $500,000

- Down payment: $300,000 (60%)

- Seller note: $200,000

- Interest rate: 9% fixed

- Term: 3 years, fully amortizing

- Monthly payment: $6,357

- Total interest earned: $28,863

- Total proceeds: $528,863 ($300,000 at closing + $200,000 principal + $28,863 interest)

- Security: UCC lien (first position), personal guarantee, life insurance on buyer

In this scenario, you get $300,000 at closing. The buyer has significant skin in the game. The note is paid off in three years. The 9% rate is fair. And you have strong collateral protection. This is a well structured deal.

Scenario B: Buyer Friendly Terms

- Purchase price: $500,000

- Down payment: $150,000 (30%)

- Seller note: $350,000

- Interest rate: 6% fixed

- Term: 7 years, interest only for the first year, then amortizing over remaining 6 years

- Monthly payment (year 1): $1,750 (interest only)

- Monthly payment (years 2 to 7): $5,822 (amortizing)

- Total interest earned: $78,768

- Total proceeds: $578,768

- Security: UCC lien (second position behind SBA loan), personal guarantee

Yes, you earn more total interest in Scenario B ($78,768 vs $28,863). But look at the risk. You only got $150,000 at closing. The buyer has less equity at risk. You're exposed for seven years. The first year is interest only, so you're getting no principal back. And your UCC lien is in second position, meaning the bank gets paid before you if things go wrong.

Here's how the two scenarios stack up side by side:

| Term | Scenario A (Seller Friendly) | Scenario B (Buyer Friendly) |

|---|---|---|

| Down payment | $300,000 (60%) | $150,000 (30%) |

| Seller note | $200,000 | $350,000 |

| Interest rate | 9% fixed | 6% fixed |

| Term length | 3 years | 7 years (1 year interest only) |

| Monthly payment | $6,357 | $1,750 then $5,822 |

| Total interest | $28,863 | $78,768 |

| Total proceeds | $528,863 | $578,768 |

| UCC lien position | First | Second (behind SBA) |

On paper, Scenario B pays more. In practice, Scenario A is the better deal for most sellers because your money is at risk for a shorter period and the buyer is more motivated to succeed.

The hybrid approach

In my experience, the best deals usually land somewhere between these two extremes. A structure like 50% down, 8% interest, 4 year term with full amortization and strong collateral gives both sides something to work with. The buyer gets reasonable payments. The seller gets solid protection and a manageable timeline.

Working with Your Attorney and Broker on the Promissory Note

You can negotiate the general terms (price, down payment, rate, term length) through your broker. But the actual promissory note, the legal document that governs the seller financing, needs to be drafted by an attorney who specializes in business transactions.

What your attorney should include

- The exact loan amount, interest rate, and payment schedule

- Maturity date and any balloon payment provisions

- All security interests (UCC liens, personal guarantees, stock pledges)

- Default definitions and cure periods

- Acceleration clause

- Late payment penalties

- Insurance requirements (life, disability, hazard insurance on business assets)

- Right to inspect financial records

- Non compete tie in language

- Subordination terms (if an SBA loan is also involved)

- Governing law and dispute resolution (mediation before litigation saves everyone money)

What your broker should do

A good broker will help you evaluate whether the buyer's proposed terms are reasonable for the market, push back on terms that expose you to unnecessary risk, and structure the overall deal so the financing component fits with the purchase price and transition plan.

I've talked sellers out of accepting terms that looked good on the surface but were terrible once you dug into the details. And I've helped buyers present proposals that initially scared sellers but were actually well structured and fair.

Ready to sell your business with the right financing structure? Let's talk about your situation. I'll help you evaluate offers and negotiate terms that protect your interests.

Common attorney costs

Expect to pay $2,000 to $5,000 for an attorney to draft a solid promissory note and related security documents. If the deal involves more complex structures (SBA loan plus seller note, stock sale, earn out provisions), legal costs might run $5,000 to $10,000.

This is not the place to cut corners. A $3,000 legal bill is nothing compared to the $200,000+ you have at stake in the note.

Mistakes Sellers Make with Seller Financing

I've seen these mistakes enough times to know they're worth calling out directly.

Every seller financing deal that went wrong in my experience had the same root cause: the down payment was under 30% and the promissory note lacked proper default provisions. Get those two things right and you avoid 90% of the problems.

Accepting too little down payment. I said it earlier, but it bears repeating. Every time I've seen a seller get burned on a note, the down payment was under 30%. Push for more.

Not requiring a personal guarantee. Some buyers will ask to sign the note through their LLC only. Don't allow it. If the LLC goes under, you have no recourse without a personal guarantee. The buyer personally needs to stand behind the debt.

Skipping the life insurance requirement. If the buyer dies, their estate may not prioritize your note. A life insurance policy naming you as beneficiary solves this problem for $30 a month.

Using a generic promissory note template. I've seen sellers download a promissory note template from the internet and use it for a $400,000 transaction. These templates miss critical provisions specific to business sales. Pay an attorney.

Not tying the non compete to the note. If the buyer defaults and you're still bound by a non compete, you've lost the business and you can't compete. Always tie them together.

Agreeing to a standby period without understanding it. When an SBA loan is involved, the bank may require the seller note to be on "full standby" for 24 months, meaning the buyer makes no payments to you for two years. If you agree to this, make sure the interest rate and down payment compensate you for the added risk and delay.

Conclusion: Get the Terms Right and Seller Financing Works for Everyone

Seller financing isn't something to fear. When structured properly, it's one of the best tools available for getting your business sold at a strong price, to a motivated buyer, within a reasonable timeline. The interest income is a bonus.

But "structured properly" is doing a lot of work in that sentence. The difference between a good seller note and a bad one comes down to a few key numbers: 50%+ down payment, 8 to 10% interest rate, 3 to 5 year term, first position UCC lien, personal guarantee, life insurance, and a solid promissory note drafted by an experienced attorney.

Get those right, and seller financing becomes a win for both sides.

Wondering what your business is worth before you start negotiating? Use our free business valuation calculator to get a starting point.

Want to talk through your specific situation? Reach out for a free consultation. I've helped dozens of sellers structure financing terms that protect their interests while getting deals closed. I'm happy to do the same for you.

For a full walkthrough of every stage of the sale, including financing and deal structure, download our free Complete Guide to Selling Your Business in 2026.

Related Articles

April 19, 2026

What Sellers Need to Know About Buyer Financing Options

How your buyer pays for your business directly affects your deal. Here's what every seller should understand about financing.

March 28, 2026

The Real Cost of Buying a Business in 2026

The purchase price is just the start. Here's every hidden cost buyers miss, from SBA fees to working capital, and how to budget right.

March 20, 2026

Can You Use Your 401k to Buy a Business? How ROBS Works

ROBS lets you use retirement funds to buy a business without early withdrawal penalties or taxes. Here's exactly how it works and what it costs.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.