Most sellers come to me after they've already decided to list. They want to be on the market in the next few weeks, sometimes sooner. And the first thing I have to tell them is: slow down by three months.

I know that sounds counterintuitive when you're ready to move. But the sellers who take 90 days to prepare before listing consistently get better offers, shorter due diligence periods, and fewer price reductions at closing. I've seen a focused 90 day preparation add $150,000 to a $700,000 business and $400,000 to a $2M business. The math on preparation is almost always in your favor.

The good news is that 90 days is enough time to make meaningful changes if you focus on the right things in the right order. This post gives you the week by week plan.

Why 90 Days Is the Sweet Spot for Pre-Sale Work

Twelve months of preparation gives you more runway, but most sellers don't have that. They've made the decision to sell and they want to move. Six months is better than nothing, but there's a certain category of changes, like financial cleanup and operational documentation, that can be done in 90 days and show up cleanly in your presentation.

The reason 90 days works is that buyers primarily evaluate your trailing twelve months of financial performance. The 90 day window lets you clean up how that history is presented, document what's been working, and fix the obvious problems a buyer would raise in due diligence. You're not trying to change the fundamentals of the business. You're trying to make sure the fundamentals you already have are clearly visible and well presented.

What you can accomplish in 90 days: financial recasting, operational documentation, minor revenue stabilization, physical and digital presence cleanup, and legal and compliance review. What you can't accomplish in 90 days: fundamentally rebuilding your customer base, putting a new management team through their paces, or changing your trailing revenue trend. Know the difference, and focus where the 90 days can actually deliver.

The sellers who take 90 days to prepare before listing consistently get better offers, shorter due diligence periods, and fewer price reductions at closing.

Curious what your business is worth before you start the 90 day process? Try our free business valuation calculators to get a baseline number so you know where you're starting from.

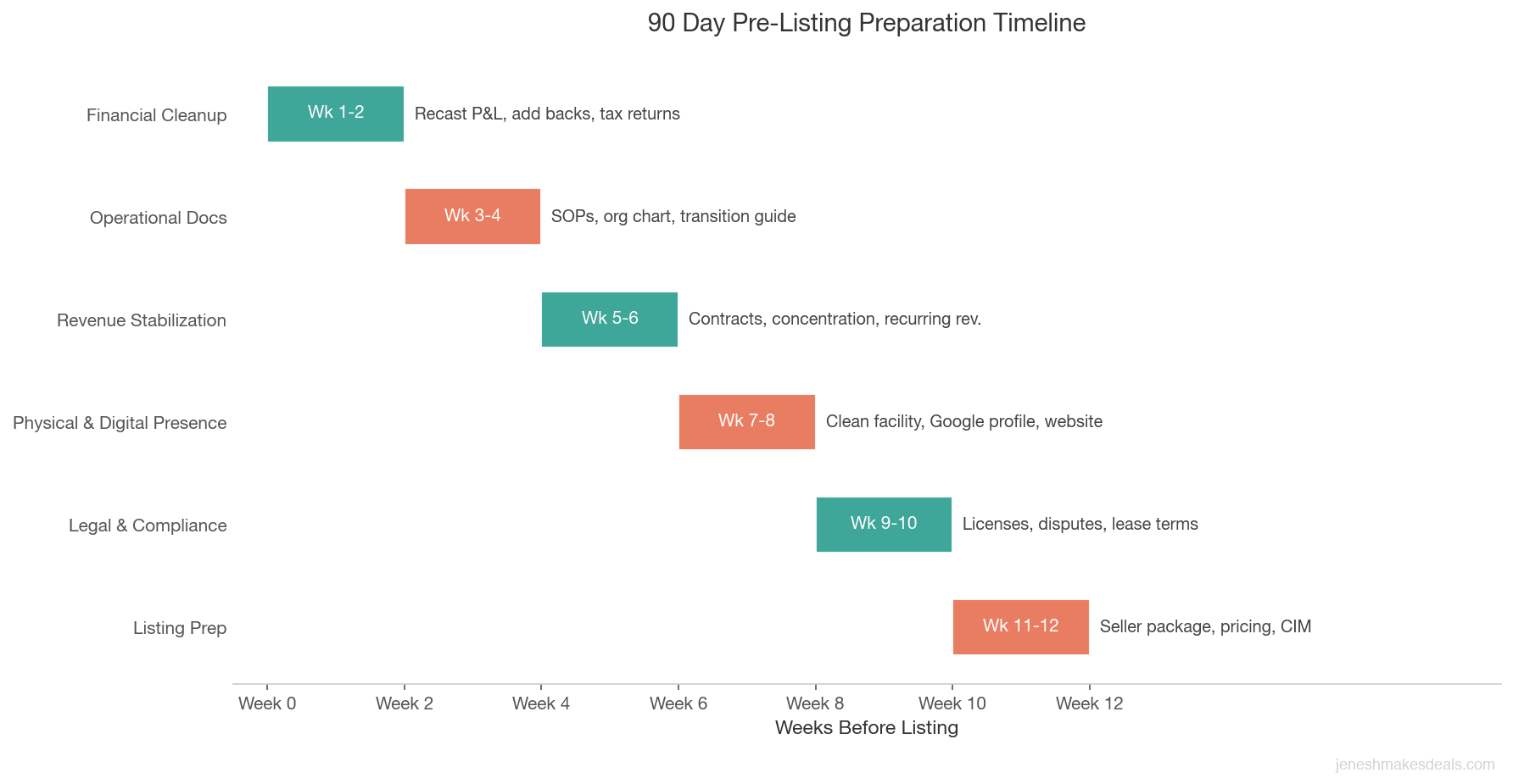

Week 1 to 2: Financial Cleanup Is Where You Win or Lose

The first two weeks should be entirely focused on your financials. This is where the most money is at stake, and it's the foundation everything else builds on.

The goal by the end of week two is a clearly recast profit and loss statement for the last 24 to 36 months that a buyer can read and understand without you explaining it. That means your SDE is documented, your add backs are itemized, and the numbers tie to your tax returns.

Use our seller due diligence checklist to see exactly which financial documents buyers will request so you can prioritize your cleanup efforts.

Recast Your P&L and Document Every Add Back

Recasting means going through your P&L and identifying every expense that is either personal, one time, or non-recurring under new ownership. Your salary and benefits. Your vehicle. Your cell phone. Your personal travel that ran through the business. Any one time legal costs, one time equipment purchases, or non-recurring expenses. These all become add backs that increase your stated SDE.

Most small business owners have $30,000 to $80,000 in legitimate add backs they've never documented clearly. On a 3x multiple, that's $90,000 to $240,000 in value that's been sitting in the books unclaimed.

| Add Back Category | Typical Range | At 3x Multiple |

|---|---|---|

| Owner salary and benefits | $60,000 to $150,000 | $180,000 to $450,000 |

| Personal vehicle expenses | $5,000 to $15,000 | $15,000 to $45,000 |

| Personal travel and meals | $3,000 to $12,000 | $9,000 to $36,000 |

| One time legal or equipment costs | $5,000 to $30,000 | $15,000 to $90,000 |

| Cell phone, insurance, other personal | $2,000 to $8,000 | $6,000 to $24,000 |

Get your bookkeeper or CPA to help you build a formal add back schedule. Every line item should have a category, dollar amount, explanation, and supporting documentation.

Clean Up the Books

If your books are behind, now is the time to get them current. Buyers want to see month by month financials for at least the past 24 months. Gaps or inconsistencies in the monthly data create doubt, and doubt costs you money at the negotiating table.

If you're running personal expenses through the business, separate them now and document them as add backs. If your expense categories are inconsistent or confusing, reclassify them into clean buckets a buyer can interpret without your commentary. If you're on spreadsheets instead of accounting software, get on QuickBooks or a comparable platform before you go to market.

Pull Three Years of Tax Returns

Buyers will ask for three years of tax returns. If any of those returns are unfiled or late, fix that now. If there are major discrepancies between your reported income and your actual cash flow, get your CPA to help you prepare a reconciliation document that explains the difference. Buyers use tax returns as the most reliable version of the financial truth because they're signed under penalty of perjury. A clean, consistent tax history communicates that you've run a legitimate business.

Not sure how to read your own financials the way a buyer will? Our post on how to read a business P&L statement when buying walks through exactly what buyers focus on and what flags they watch for.

Week 3 to 4: Operational Documentation

Buyers pay a premium for businesses that run on systems rather than on the owner's memory and presence. The problem is most small business owners have never written down how anything works. It's all in their head. Week three and four are about getting it out of your head and onto paper.

This isn't about creating an impressive binder to show buyers. It's about proving that the business can function after you leave. That proof changes your multiple.

Build Your Core SOPs

Start with the five to ten processes most critical to delivering value for customers. For a service business, that's probably client intake, service delivery, quality review, billing, and customer communication. For a retail business, it's inventory management, vendor ordering, staffing, and point of sale reconciliation. For a restaurant, it's prep schedules, recipe standards, opening and closing procedures, and vendor ordering.

An SOP doesn't need to be long. A one page document with numbered steps, the person responsible for each step, and what a successful outcome looks like is enough. The goal is that a competent new employee could follow the process without asking questions. Write these in plain language, not corporate speak.

Document Your Org Structure

Create a simple org chart that shows every role in the business, who is in each role, and what they're responsible for. If you're a solo operator with part time help, that's fine. Document it anyway. Buyers want to understand the human infrastructure before they make an offer.

If there's a key employee who carries significant operational responsibility, document their role in detail. Buyers will want to meet this person during due diligence. Having a clear job description and performance record for them strengthens your position.

Prepare a Transition Training Guide

This doesn't have to be a full manual. A 10 to 15 page document that covers: how you find and onboard customers, who your key vendors are and how those relationships work, how you handle the most common problems that come up, and the three to five things a new owner absolutely needs to know in the first 30 days. Buyers value this more than most sellers realize. It signals confidence and professionalism.

Week 5 to 6: Revenue Stabilization

By week five, your financials are clean and your operations are documented. Now you need to make sure the revenue you're presenting is as stable and transferable as possible.

Revenue instability scares buyers. Even if your total revenue looks good on paper, buyers worry about what happens to that revenue after you're gone. Week five and six are about reducing that fear.

Lock In Contracts Where You Can

If you have customers you've been serving on a handshake basis, now is a good time to formalize those relationships with a written service agreement. Even a simple one or two page agreement that establishes ongoing service terms and a notice period for cancellation makes those customer relationships more transferable and more bankable in the buyer's eyes.

You're not going to be able to put all your customers on contract in two weeks. Focus on your top five to ten customers who represent your most significant revenue. A contract with a customer who pays you $50,000 per year is worth materially more than no contract, because it gives a buyer confidence that $50,000 will show up in year one of their ownership.

Address Customer Concentration

If one customer represents more than 25% of your revenue, that's a valuation problem you need to at least acknowledge and begin addressing. You can't fix concentration in 90 days, but you can show buyers a trend toward improvement.

Are there two or three customers you've been underserving who could be expanded? Is there a referral source you haven't been activating? Even if you grow another $30,000 to $50,000 from existing relationships in the next 90 days, that reduces the concentration percentage and shows buyers the direction is improving. Document these efforts so you can discuss them honestly during your listing.

Our post on customer concentration risk and business valuation breaks down exactly how buyers discount for concentration and how to model the impact on your asking price.

Review Your Recurring Revenue

Every dollar of SDE you can document and defend clearly gets multiplied by your industry multiple at closing. For most small businesses, the difference between messy financials and clean recast financials is $50,000 to $200,000 in deal value.

Recurring revenue, meaning revenue that renews automatically through contracts, subscriptions, or long term agreements, commands higher multiples than one time revenue. Make a list of every revenue source that recurs. Calculate the total. Calculate what percentage of your trailing twelve month revenue it represents.

If recurring revenue is less than 20% of your total, think about whether there are simple ways to add it. Could your best customers move to an annual service agreement? Could you offer a maintenance retainer to existing clients? Even modest recurring additions improve how buyers see the stability of the business.

Week 7 to 8: Physical and Digital Presence

This is where sellers often overspend. I've seen business owners dump $50,000 into office renovations right before listing, and it doesn't move the price one dollar. Buyers base offers on earnings, not aesthetics.

That said, there are legitimate improvements in week seven and eight that do affect how seriously buyers engage with your listing. The goal is credibility, not cosmetics.

Tidy the Physical Space Without Renovating It

If your facility looks like it hasn't been cleaned in six months, clean it. Fix broken equipment, replace burned out lights, organize storage areas, patch any obvious maintenance issues that would come up in a facility walkthrough. Buyers will tour your location. A sloppy or neglected space raises questions about management standards.

Do not paint the lobby. Do not replace the furniture. Do not remodel the bathroom. These things cost money and don't change your multiple. Clean and organized is enough.

Clean Up the Digital Presence

Check your Google Business profile. Make sure the hours, address, phone number, and website are correct. Look at your recent reviews. If you have unanswered negative reviews, respond to them professionally now. Buyers check online reviews during initial research, before they even reach out. A three star average with a bunch of unanswered complaints is a turn off.

Update your website if it's significantly outdated or broken. A functional, professional website doesn't need to be fancy. It needs to load, look current, and represent the business accurately. If your website has dead links, broken contact forms, or a copyright date from 2019, fix those things. This is a $500 to $2,000 fix, not a $20,000 redesign.

Make sure your business has an accurate and complete LinkedIn page if you're a B2B business. Many buyers use LinkedIn to research businesses and verify the staff structure before engaging with a broker.

Week 9 to 10: Legal and Compliance Cleanup

Legal and compliance issues are deal killers. Buyers find them in due diligence, and when they find them, two things happen. First, they wonder what else you haven't disclosed. Second, they use the issue as a reason to reduce the price. Addressing these issues before you list is almost always cheaper than the discount they create at closing.

Audit Your Licenses and Permits

Make a list of every license and permit required to operate your business. Check the expiration date on each one. Renew anything that's lapsed or expiring in the next six months. If there's a license you're supposed to have and don't have, get it or get a clear legal opinion about whether it's actually required.

For regulated industries such as healthcare, food service, transportation, or childcare, buyers will scrutinize your compliance record carefully. Any active violations or citations need to be resolved or formally documented as being in the process of resolution.

Resolve Outstanding Disputes

If you have any pending legal disputes, unpaid tax obligations, or unresolved vendor or customer disagreements, now is the time to address them. A $12,000 tax lien is not a deal killer on its own. A $12,000 tax lien discovered by a buyer's attorney that you never disclosed creates a trust problem that can collapse a multi-million dollar transaction.

The rule is simple: disclose everything and show that it's being handled. Buyers expect imperfection. They don't expect dishonesty.

Buyers who find undisclosed issues in due diligence are far more likely to walk or demand steep price reductions than buyers who are told about problems upfront with a clear resolution plan.

Check Your Lease Terms

If your business is location dependent, confirm the remaining term on your lease and whether it includes an assignability clause. Buyers need to know they can take over the lease. If the lease expires within 18 months of your planned closing, talk to your landlord now about an extension or renewal.

Buyers who finance through the SBA may be required to have lease terms that extend beyond the loan repayment period. If you're expecting an SBA buyer, your broker can tell you exactly what the lender will need to see. Our post on what to check in a business lease before closing covers the key terms to review.

Week 11 to 12: Final Positioning and Listing Prep

You've cleaned the financials, documented the operations, stabilized the revenue, addressed the legal issues, and tidied the presence. Week eleven and twelve are about putting together the materials that will go in front of buyers.

Prepare Your Seller's Package

The documents you'll need ready before your broker can list you include: three years of tax returns, recast P&L with add back schedule, current year financials year to date, copies of any major customer contracts, current equipment list with age and condition, copies of leases and key vendor agreements, and an org chart with brief role descriptions.

Having all of this organized before your broker lists you saves weeks of back and forth and signals to buyers that you're a serious seller who has their act together. Deals move faster when the seller is prepared.

Decide on Your Asking Price Rationally

Your asking price should be based on your recast SDE and the typical multiple for businesses like yours in your industry. Not what you need from the sale. Not what your neighbor got for his business three years ago. The actual market multiple applied to your documented earnings.

Work with your broker to look at comparable transactions in your industry. If your recast SDE is $280,000 and businesses in your sector are selling at 2.5x to 3x, your realistic range is $700,000 to $840,000. Starting at $1.2M because that's how much you want in retirement is a great way to sit on the market for a year and sell for less than you would have gotten if you'd priced it right from the start.

Want to see how your preparation has moved the value of your business? Contact me for a free consultation and we'll run through your numbers together before you list.

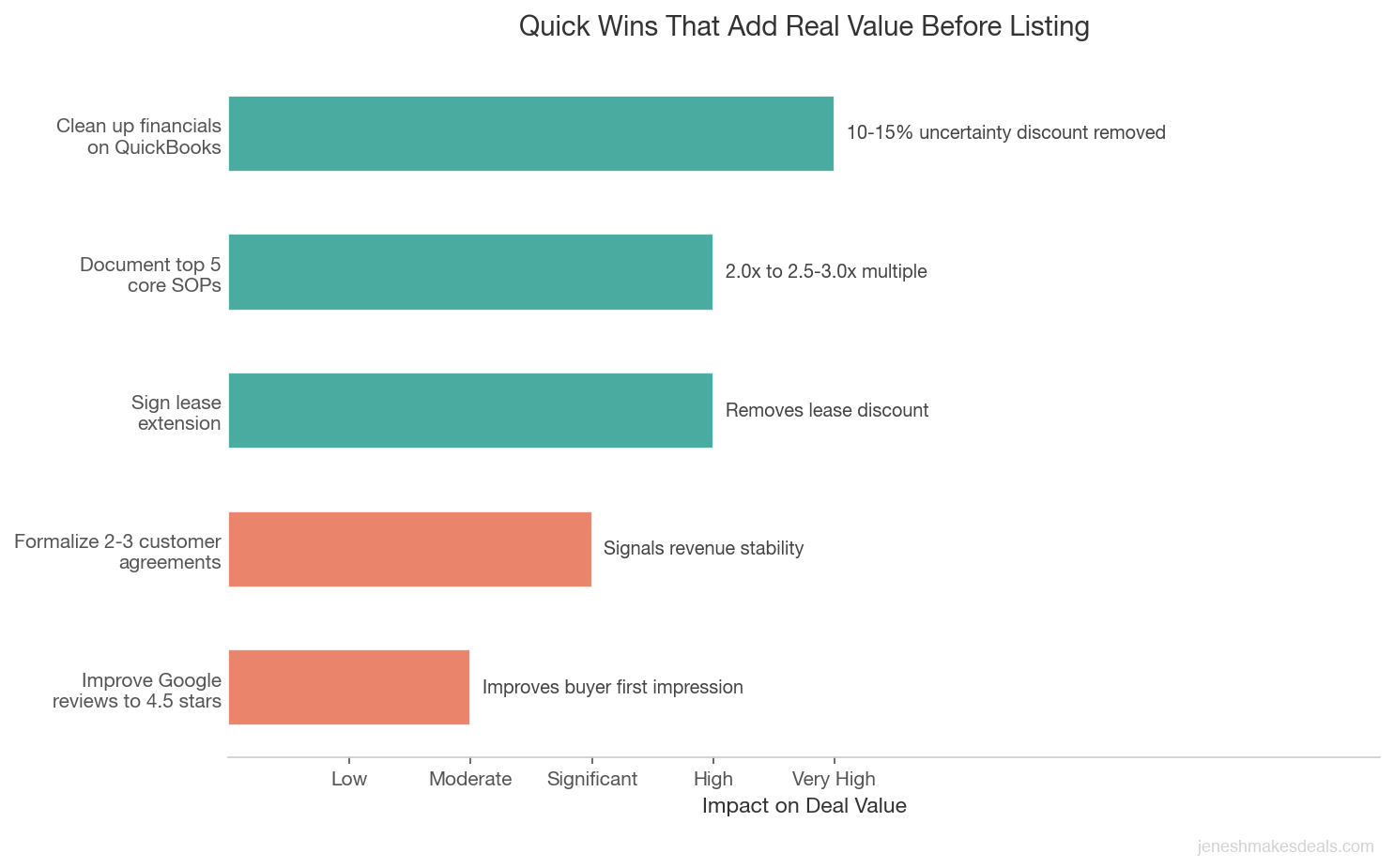

Quick Wins That Add Real Multiple Points

Not all preparation is equal. These specific moves have a consistent, documented history of improving valuation multiples without requiring months of effort.

Getting your financials on QuickBooks and cleaned up consistently moves SDE presentations from confusing to credible. That alone can eliminate a buyer's uncertainty discount, which often runs 10% to 15% of deal value.

Documenting your top five SOPs proves operability without you. For businesses where the buyer was going to apply a 2x multiple due to owner dependence, documentation of solid processes can push that to 2.5x or 3x.

Signing a lease extension if you have less than three years remaining. A short lease is a buyer concern. A five to seven year term with an option gives buyers confidence and removes a negotiating lever from their side.

Formalizing even two or three major customer relationships with simple service agreements. Going from zero contracts to a few documented, recurring relationships signals stability.

Pulling your online reviews into shape. A 4.5 star average on Google with professional responses to any negative reviews takes about two hours and affects how every single buyer evaluates you during initial research.

Things Not to Do in the 90 Days

This is as important as the to do list. These are the mistakes I see regularly.

Do not cut marketing spend to show higher short term profitability. Buyers look at trailing trends. Cutting your marketing budget by $5,000 per month might improve this month's profitability number, but buyers see it in the trend and they'll ask why marketing dropped sharply right before the listing. The answer, that you were trying to inflate SDE, is exactly what they suspected.

Do not let key employees go to reduce payroll costs. Your employees are part of what a buyer is paying for. Cutting them right before a sale reduces the operational capacity a buyer is evaluating. It also creates instability on the team that buyers will sense during their visits.

Do not sign new long term vendor contracts without your broker's input. A five year contract with a supplier at a rate that isn't market rate becomes a buyer's problem. Get your broker's view before committing the business to anything that extends beyond the expected closing date.

Do not start a major new initiative. Launching a new product line, opening a second location, or pivoting the business model 60 days before you list creates uncertainty. Buyers want to see what the business is, not what it might become. Save new initiatives for after the sale or for the story of what a buyer could do with the business.

Do not neglect operations while you prepare. Some sellers mentally check out once they decide to exit. Revenue slips, customer service declines, and key employees pick up on the vibe. The business you go to market with needs to be performing at least as well as the trailing numbers you're showing buyers. Often better.

| Mistake | Why It Backfires |

|---|---|

| Cut marketing spend to inflate SDE | Buyers spot the trailing trend drop and question why |

| Let key employees go to reduce payroll | Reduces operational capacity buyers are evaluating |

| Sign long term vendor contracts without broker input | Bad rates become the buyer's problem |

| Launch major new initiatives before listing | Creates uncertainty instead of stability |

| Mentally check out of day to day operations | Revenue slips and employees sense the change |

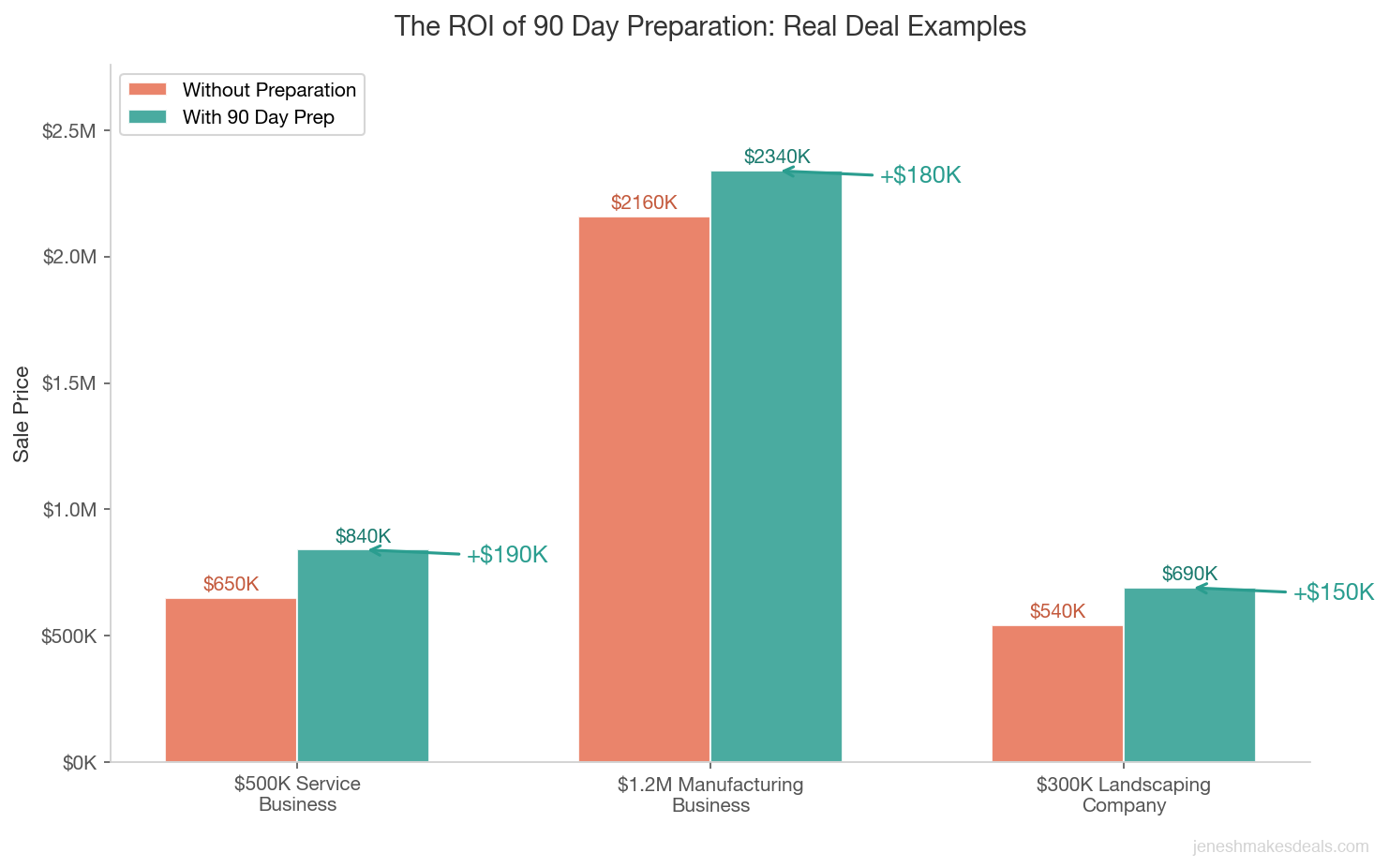

The ROI of Preparation: Real Examples

Let me give you three scenarios that show what this 90 day work actually returns.

A $500,000 service business with messy financials and no contracts gets listed without preparation. Buyers apply a 2x multiple and discount further for uncertainty. Final sale: $650,000. After 90 days of financial cleanup, SOP documentation, and two customer contracts signed, the same business sells with confidence at 2.8x clean SDE. Final sale: $840,000. The preparation added $190,000.

A $1.2M EBITDA manufacturing business has a lease expiring in 14 months and no lease extension in place. Buyers price this as a lease risk and offer at a discount. With a new five year lease extension signed before listing, the same business sells without a lease discount at full multiple. That lease conversation with the landlord, which took about three hours, was worth $180,000 in deal value.

A $300,000 SDE landscaping company has one customer who accounts for 35% of revenue. Without addressing this, buyers offer at 1.8x due to concentration risk: $540,000. The owner spends 90 days growing two other accounts from $20,000 per year to $45,000 per year each. The concentration drops from 35% to 27%, still high but trending down. With documented effort and a story, buyers accept a 2.3x: $690,000. The account development work added $150,000.

These aren't theoretical. They're the patterns I see across deals, year after year.

90 Day Pre-Listing Checklist

| Week | Focus Area | Key Tasks |

|---|---|---|

| 1-2 | Financial Cleanup | Recast P&L, document add backs, clean up books, pull 3 years of tax returns |

| 3-4 | Operational Docs | Write 5-10 core SOPs, create org chart, prepare transition training guide |

| 5-6 | Revenue Stabilization | Lock in key customer contracts, address concentration, audit recurring revenue |

| 7-8 | Physical and Digital Presence | Clean facility, update Google profile, fix website issues, check LinkedIn |

| 9-10 | Legal and Compliance | Audit licenses, resolve disputes, check lease terms, clear any tax issues |

| 11-12 | Listing Prep | Assemble seller document package, set pricing with broker, finalize CIM |

How a Broker Helps With Pre-Listing Prep

A good broker doesn't just list your business. They help you prepare it. When a seller comes to me 90 days before they want to list, here's what that engagement looks like.

First, I do a pre-listing review of your financials and identify everything that needs to be cleaned up or clarified before we go to market. I tell you what add backs are defensible and how to document them, and I tell you honestly where the numbers have problems a buyer will raise.

Then I look at the operational and structural issues: owner dependence, customer concentration, lease terms, key employee risk. I help you prioritize which ones can be meaningfully addressed in 90 days and which ones we'll need to disclose and manage during the sale.

Throughout the 90 days, I help you build the seller's package, the recast financials, the add back schedule, the process documentation, the customer contract summaries. This is the package that goes in front of buyers, and the quality of that package directly affects the quality of offers you receive.

By the time we list, buyers are seeing a well prepared business with clean materials. That reduces the time to offer, reduces the number of due diligence questions, and reduces the price reductions that come from buyers discovering problems they weren't warned about. The preparation that goes into those 90 days pays for itself many times over at the closing table.

Ready to start your 90 day sprint? Contact me for a free seller consultation and I'll give you an honest assessment of where to focus for your specific business. Or use our business valuation calculators to benchmark where you stand today before we talk.

FAQ

Is 90 days really enough time to meaningfully improve my sale price? Yes, for specific categories of preparation. Financial cleanup, operational documentation, minor revenue stabilization, legal and compliance review, and listing prep can all be done in 90 days and have a real impact on your price and the quality of your buyer pool. Structural changes like reducing owner dependence or rebuilding your customer base take longer.

What's the single most valuable thing I can do in 90 days? Clean up and recast your financials. Every dollar of SDE you can document and defend clearly gets multiplied by your industry multiple at closing. For most small businesses, the difference between messy financials and clean recast financials is $50,000 to $200,000 in deal value.

Should I hire a CPA to help with the financial cleanup? Yes, if your books are significantly behind or your financials are complex. A CPA who has experience with business sales, not just tax prep, can help you build a defensible add back schedule and reconcile any discrepancies between your reported income and actual cash flow. The cost is typically $2,000 to $8,000 and almost always pays back many times over in deal value.

What if I find legal or compliance issues I don't know how to fix? Disclose them to your broker immediately and get a qualified attorney's opinion on the path to resolution. Buyers who find undisclosed issues in due diligence are far more likely to walk or demand steep price reductions than buyers who are told about issues upfront with a clear resolution plan. Disclosure with a plan is almost always better than hoping no one notices.

Should I tell my employees I'm preparing to sell? Generally no, not during the 90 day preparation phase. You can make operational improvements and documentation work without disclosing your exit plans. See our post on what happens to employees when a business is sold for guidance on when and how to communicate with your team.

What if I have less than 90 days before I need to list? Focus on the financial cleanup first. It has the highest return and can be done in two to three weeks with the right help. Then prioritize legal and compliance issues that could kill a deal. Operational documentation and everything else comes after those two. Even 30 days of focused preparation is better than listing with no preparation at all.

Can I use financing to fund the preparation work? Yes. If improvements like hiring, equipment repair, or technology upgrades require capital, there are options. Explore funding resources for business owners who need capital for growth or pre-sale preparation. Just make sure the return on those improvements at the deal table exceeds their cost.

If you're within 90 days of wanting to list, tell us about your business and we'll help you prioritize what to tackle first.

Related Articles

March 19, 2026

How to Build a Business That Runs Without You

A business that depends on you has a ceiling on its value. Here's the step-by-step process for building real owner independence over 18-24 months.

March 2, 2026

First 90 Days After Buying a Business: Your Transition Playbook

The first 90 days after buying a business determine whether your acquisition succeeds. Here's exactly what to do each week, and what to avoid.

January 4, 2026

Live Social Selling Is Reshaping Ecommerce in 2026

Live social selling delivers 9 to 30% conversion rates vs 2 to 3% for standard ecommerce. Why brands are shifting to live commerce in 2026.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.