Selling a business is not a quick transaction. The average sale takes 6 to 12 months from listing to closing, and many deals take longer. That's a long time to stay focused on a business you've already mentally moved on from.

I've seen more deals lose value during the sale process than I'd like to admit. Not because the business wasn't good when it went to market, but because the owner checked out before the deal closed. Revenue dipped. Employees got nervous. Customers left. And the buyer, watching all of this, renegotiated the price downward.

This post is about how to prevent that from happening to you.

Why the Sale Process Takes So Long

If you've never sold a business before, the timeline can feel shocking. You're not just putting up a "for sale" sign and accepting offers. The process has multiple stages, and each one takes time.

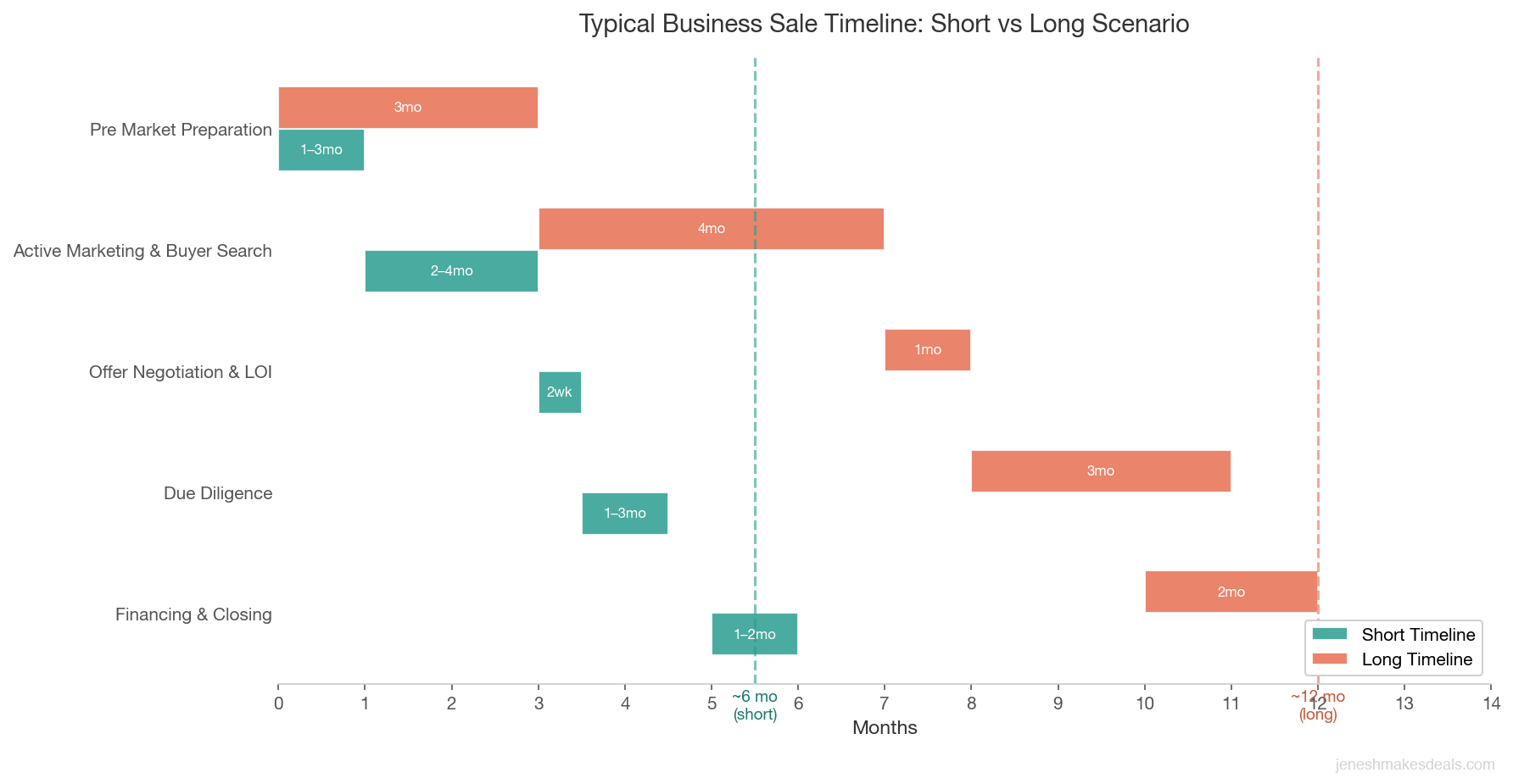

Here's what a typical timeline looks like:

| Stage | Typical Duration |

|---|---|

| Pre market preparation | 1 to 3 months |

| Active marketing and buyer search | 2 to 4 months |

| Offer negotiation and LOI | 2 to 4 weeks |

| Due diligence | 30 to 90 days |

| Financing and closing | 30 to 60 days |

Add those up and you're looking at 6 to 12 months on the short end. If the first buyer falls through, you're starting the buyer search again, and the clock resets on part of that timeline.

During all of this, the business needs to keep performing. Buyers aren't evaluating a snapshot of your business from the day you listed it. They're watching the trend. And if that trend is going downward, the price goes with it.

The "Mental Checkout" Problem

This is the number one threat to deal value that nobody talks about enough. The moment a business owner decides to sell, something shifts. You start thinking about what comes next. You stop caring about the small stuff. You don't invest the same energy into growth because, in your mind, it's someone else's business now.

I get it. It's human nature. But it's also the single most expensive mistake sellers make.

Here's what the mental checkout looks like in practice:

- You stop running marketing campaigns because "why spend the money?"

- You skip the annual price increase you normally would have done

- You postpone hiring a replacement for a key employee who left

- You stop attending industry events and networking

- You coast on existing customer relationships instead of building new ones

Each of these decisions feels rational in the moment. But they all have the same effect: they make the business worth less right when you need it to be worth more.

The moment you decide to sell, the business doesn't need less attention. It needs more. Every shortcut you take during the sale process gets priced into the deal.

Want to know what your business is worth before going to market? Use our valuation calculator to get a starting estimate.

Keep Marketing and Sales at Full Speed

This is the area where I see the most damage. Sellers cut marketing spend because they see it as money they won't benefit from. But here's the thing: buyers look at trailing 12 month revenue trends. If they see revenue declining over the last 6 to 9 months, they don't care that you used to be growing. They price the business based on what it's doing now and where it's headed.

One seller I worked with saw revenue drop 15% during a 9 month sale process because he stopped doing marketing. The buyer used that decline to renegotiate the price down by $180,000. The seller's "savings" on marketing cost him ten times what he saved.

What you should be doing instead:

- Keep all marketing campaigns running. If anything, increase your marketing effort during the sale. A business with growing revenue sells faster and for a higher price.

- Maintain your sales pipeline. Continue prospecting, following up on leads, and closing deals. A healthy pipeline shows buyers that the business has momentum.

- Don't skip seasonal promotions. If you normally run a holiday sale or spring campaign, run it. Buyers will compare year over year performance, and a missing campaign creates a gap.

- Track your numbers monthly. Keep detailed records of leads, conversions, and revenue so you can show buyers that the business maintained or improved its performance during the sale process.

The goal is simple: hand the buyer a business that's performing as well or better than it was when you listed it.

Managing Employees During the Sale

Employees are one of the trickiest parts of the sale process. They're critical to maintaining business value, but telling them too early can backfire. People get nervous when they hear the business is being sold. They start looking for other jobs. They worry about layoffs. Productivity drops.

Here's how I advise sellers to handle it:

Don't tell employees until you have to. In most cases, employees don't need to know until the deal is close to closing. Your broker should be managing confidentiality throughout the process, and most buyers understand the importance of keeping things quiet until the right time.

Identify your key people early. Before you go to market, figure out which employees are essential to the business. These are the people whose departure would hurt operations, customer relationships, or revenue.

Create retention incentives. For your most important employees, consider stay bonuses that pay out after the sale closes. This gives them a financial reason to stick around through the transition. A typical stay bonus might be 5% to 15% of their annual salary, payable 60 to 90 days after closing.

Have a communication plan ready. When it is time to tell employees, be prepared. Have answers for the obvious questions: Will I keep my job? Will my pay change? Will the new owner change how we do things? The more confident and prepared you are, the less panic you'll create.

| When to Tell Employees | Pros | Cons |

|---|---|---|

| Early (before listing) | Builds trust, avoids surprises | Risk of leaks, employee flight |

| Mid process (after LOI signed) | More certainty, less waiting | Still some uncertainty, rumor risk |

| Late (during closing) | Maximum confidentiality | Employees feel blindsided, less trust |

Most sellers land in the middle. They tell key managers after an LOI is signed and the rest of the team closer to closing. The exact timing depends on your industry, the size of your team, and how dependent the business is on specific people.

The number one regret I hear from sellers is telling employees too early. Once the word is out, you cannot take it back. Key people start interviewing, productivity drops, and the buyer notices. Keep the circle small until the deal is close enough to closing that certainty outweighs the risk of leaks.

Thinking about selling and not sure how to handle the employee conversation? Reach out for a confidential discussion about your situation.

Maintaining Customer Relationships

Customers are the revenue engine of your business. Losing key customers during the sale process doesn't just hurt current revenue. It changes the buyer's projection of future revenue, which directly impacts the purchase price.

Here's what to focus on:

- Stay visible and engaged with your top customers. If you normally meet with your biggest clients quarterly, keep doing that. Don't disappear.

- Deliver on your commitments. Nothing sends customers running faster than a drop in quality or missed deadlines. Maintain your service standards.

- Renew contracts proactively. If you have customers with contracts expiring during the sale process, get those renewed. A buyer values a business with locked in revenue far more than one with customers who could leave at any time.

- Don't make promises about the new owner. You can't guarantee what the buyer will do. If customers ask about changes, be honest about what you know and reassure them that continuity is a priority.

If your business has customer concentration risk (one client representing more than 15% to 20% of revenue), this becomes even more critical. Losing that customer during the sale could crater the deal entirely. If you're in this situation, work on diversifying your customer base before you go to market, not after.

Capital Expenditure Decisions: Invest or Save?

This question comes up in almost every sale I work on. Should you keep investing in the business while it's for sale, or should you conserve cash?

The answer depends on the type of expenditure.

Keep spending on maintenance and operations. If your delivery truck needs new tires, get new tires. If your equipment needs routine service, service it. Buyers will inspect the physical condition of your assets, and deferred maintenance is a red flag that leads to price reductions or repair credits at closing.

Be strategic about growth investments. A major renovation or new product launch that won't show returns for 12 to 18 months probably isn't the best use of capital during a sale. But investments that improve current performance, like a marketing campaign or a software upgrade that increases efficiency, can be worth it.

Don't starve the business to boost short term cash flow. Buyers and their advisors will notice if you've been cutting corners. Underspending on inventory, skipping equipment maintenance, or reducing staff to inflate the bottom line is called "running it lean for the sale," and experienced buyers know exactly what it looks like. It doesn't fool anyone. It just gives them negotiating ammunition.

| Expenditure Type | Recommendation | Why |

|---|---|---|

| Routine maintenance (equipment, vehicles) | Keep spending | Deferred maintenance is a red flag that leads to price reductions |

| Marketing and advertising | Keep spending or increase | Trailing revenue trends directly impact valuation |

| Staff replacements for key roles | Hire now | Unfilled critical positions signal instability to buyers |

| Major renovation or expansion | Pause | Returns won't materialize before closing |

| Software or efficiency upgrades | Invest selectively | Improvements to current performance strengthen the deal |

| Inventory restocking | Maintain normal levels | Thin inventory signals cost cutting and raises buyer concerns |

The general principle: run the business as if you plan to own it for five more years. That's what produces the best financial results during the sale and the highest purchase price at closing.

If a buyer's inspector finds a truck with bald tires and overdue maintenance, they don't just ask for a $2,000 tire credit. They start wondering what else you've been neglecting. Deferred maintenance is a trust issue that spreads to every part of the negotiation.

Keeping Clean Financials and Documentation Current

Your financials are the foundation of your business's valuation. During the sale process, buyers and their accountants will scrutinize every number. If your books are messy, incomplete, or out of date, it slows down due diligence, raises concerns, and can kill deals.

What "clean financials" means during a sale:

- Monthly financial statements ready within 15 days of month end. Buyers want to see current performance. If your most recent financials are four months old, that's a problem.

- Tax returns filed and consistent with your financial statements. If there are differences between your tax returns and your P&L, be ready to explain them. Unexplained discrepancies are deal killers.

- Addbacks documented and supportable. Every personal expense, one time cost, or non recurring item that you're adding back to calculate SDE (seller's discretionary earnings) needs documentation. "Trust me" doesn't work in due diligence.

- Clean accounts receivable. Collect outstanding invoices. A business with $100,000 in receivables that are 120 days past due looks very different from one with $100,000 in receivables that are all current.

- Updated contracts and agreements. Leases, vendor agreements, customer contracts, employee agreements. All of these should be current and organized. A missing lease or expired contract can delay a closing by weeks.

I recommend keeping a data room (a secure digital folder with all your key documents) updated throughout the sale. When a buyer or their advisor asks for something, you want to be able to provide it within 24 hours, not scramble for a week looking for it.

Want to get organized before going to market? Contact us to discuss what buyers will want to see and how to prepare.

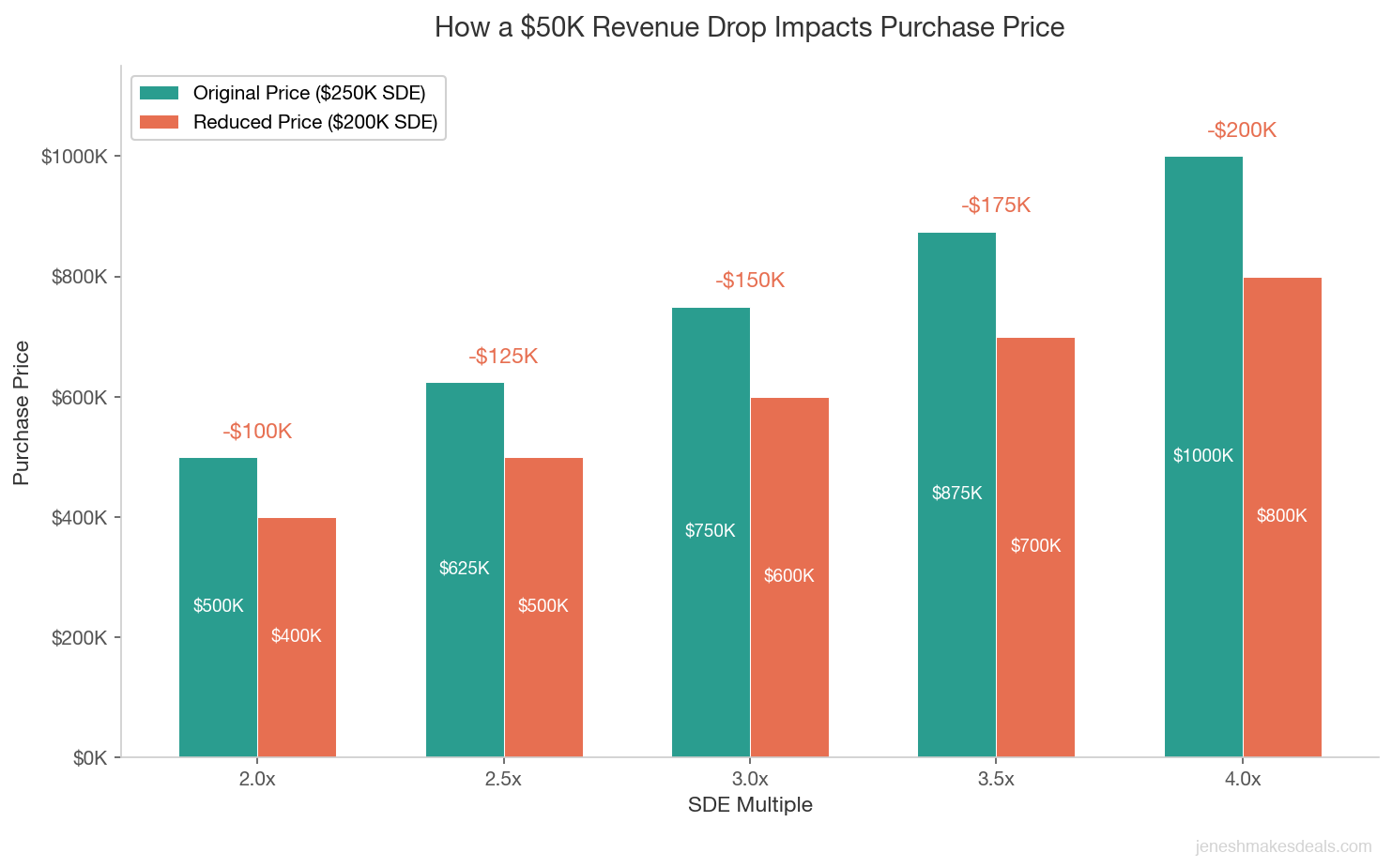

How a Revenue Dip Can Cost You Multiples of What You Lost

This is the math that surprises most sellers. A small revenue decline during the sale process has an outsized impact on the purchase price because of how businesses are valued.

Most small businesses sell for a multiple of SDE, typically 2.0x to 4.0x depending on the industry, size, and risk profile. That multiple means every dollar of SDE is worth $2 to $4 in purchase price.

Here's an example. Say your business has $500,000 in annual revenue and $250,000 in SDE, and a buyer is offering 3.0x, which puts the price at $750,000.

Now say revenue drops $50,000 during the sale process. That $50,000 in lost revenue flows through to SDE (assuming your costs stay roughly the same). Your SDE drops to roughly $200,000 to $225,000. At the same 3.0x multiple, the new price range is $600,000 to $675,000.

| Scenario | Revenue | SDE | Multiple | Purchase Price |

|---|---|---|---|---|

| Original | $500,000 | $250,000 | 3.0x | $750,000 |

| After $50K revenue drop | $450,000 | $200,000 to $225,000 | 3.0x | $600,000 to $675,000 |

| Difference | $75,000 to $150,000 |

A $50,000 revenue dip cost $75,000 to $150,000 off the purchase price. And that's if the buyer doesn't also lower the multiple, which they often do when they see a declining trend. If the multiple drops from 3.0x to 2.5x because of the trend, the damage is even worse.

This is why protecting revenue during the sale process is so important. Every dollar you let slip doesn't just cost you that dollar. It costs you that dollar multiplied by whatever your business's valuation multiple is.

A $50,000 revenue dip doesn't cost you $50,000. At a 3.0x multiple, it costs you $150,000. Every dollar of SDE you protect during the sale is worth $2 to $4 in purchase price.

What Happens When You Need to Renegotiate

If your business performance does decline during the sale process, expect the buyer to bring it up. Buyers and their advisors track your financial performance through due diligence. If the numbers from the trailing three to six months look worse than what was presented at listing, they have every right to renegotiate.

Here's how that usually plays out:

The buyer requests updated financials. This is standard during due diligence. If the numbers are down, the conversation starts here.

The buyer's advisor recalculates the valuation. They'll adjust SDE based on the more recent numbers and often apply a lower multiple because the declining trend increases perceived risk.

The buyer presents a revised offer. This might come as a formal price reduction request or as a series of "concerns" that lead to the same place.

You're stuck. At this point, your options are limited. You can accept the lower price, try to negotiate somewhere in the middle, or walk away from the deal entirely. None of these are good positions to be in, especially if you've already spent 6 to 9 months in the sale process.

The best way to avoid renegotiation is to prevent the decline in the first place. That means running the business at full capacity throughout the sale, not just until the LOI is signed.

Renegotiation is where sellers lose the most money, because you've already invested 6 to 9 months and feel pressure to close at almost any price. The best defense is simple: never give the buyer a reason to renegotiate. Keep your numbers flat or growing from listing day through closing day.

Working With Your Broker to Manage Timeline and Buyer Expectations

A good broker doesn't just find buyers. They manage the entire process to protect your interests, including keeping the timeline moving so the business doesn't sit on the market longer than necessary.

Here's what your broker should be doing:

- Setting realistic timelines with buyers. If a buyer is dragging their feet on due diligence, your broker should push them. Delays cost you money.

- Pre qualifying buyers. A buyer who can't get financing wastes months of your time. Your broker should verify a buyer's financial ability before you get deep into negotiations.

- Managing information flow. Sharing the right information at the right time keeps the process moving without giving away too much too early.

- Keeping you focused on operations. Your broker should handle the deal process so you can focus on running the business. If you're spending 20 hours a week on sale related activities, something is wrong.

- Communicating performance updates. If the business is doing well, your broker should make sure the buyer knows about it. Strong recent performance reinforces the value and protects your price.

One of the most important things your broker can do is keep the deal moving forward. Every month the sale drags on is another month where something could go wrong. Good brokers create urgency without being pushy, and they know how to handle buyers who stall or try to use time as a negotiating tool.

Looking for a broker who will protect your interests throughout the sale process? Let's talk about your situation.

Building a Management Team That Runs Without You

I've written about this topic in depth before (see how to build a business that runs without you), but it's worth repeating here because it directly impacts the sale process.

A business that depends on the owner for day to day operations has two problems during a sale:

- The owner is distracted by the sale process. Meetings with buyers, document requests, negotiations. All of this takes time and mental energy away from running the business.

- The buyer sees concentration risk. If the business can't function without you, the buyer knows that value could evaporate after you leave. They'll either reduce the price, demand a longer transition period, or structure an earnout that ties part of your payment to future performance.

The solution is the same whether you're selling in 3 months or 3 years: build a team that can run operations without your constant involvement.

This means:

- A strong second in command. Someone who can make day to day decisions, manage the team, and handle customer issues without calling you.

- Documented processes. Written SOPs for every major function in the business so knowledge isn't trapped in anyone's head, especially yours.

- Distributed customer relationships. If you're the only person who talks to your top 10 customers, start introducing account managers or key employees to those relationships now.

- Financial management systems. Automated reporting, regular financial reviews, and someone besides you who understands the numbers.

A management team that runs without you doesn't just protect value during the sale. It increases value. Buyers consistently pay higher multiples for businesses with strong management in place because they represent lower risk and an easier transition.

Buyers don't just buy what the business earns today. They buy how easy it is to keep earning that without the current owner. A team that runs without you is the single biggest value multiplier in any deal.

A Practical Checklist for Protecting Value During the Sale

Here's a summary of everything we've covered, organized as a checklist you can reference throughout the sale process.

Marketing and Sales:

- All marketing campaigns running at or above normal levels

- Sales team maintaining or exceeding targets

- Pipeline of new business development active

- Seasonal promotions and campaigns executed as planned

Employees:

- Key employee retention plan in place (stay bonuses if needed)

- Confidentiality maintained until appropriate disclosure time

- Communication plan prepared for when employees are told

- No critical positions left unfilled

Customers:

- Top customer relationships actively maintained

- Contracts renewed or extended where possible

- Service quality at or above standard

- Customer concentration risk addressed (no single customer above 15% to 20%)

Financials:

- Monthly statements produced within 15 days

- Tax returns current and consistent with financial statements

- Addbacks documented with supporting evidence

- Accounts receivable current

- Data room updated and organized

Operations:

- Equipment and assets maintained to normal standards

- No deferred maintenance

- Inventory at appropriate levels

- All licenses, permits, and certifications current

Management:

- Second in command capable of handling day to day operations

- SOPs documented for key processes

- Owner able to step back without immediate operational impact

The Bottom Line

The sale process is a marathon, not a sprint. The businesses that sell for the highest prices are the ones that maintain or improve their performance from listing day through closing day. Every dollar of revenue you protect during the sale is worth $2 to $4 in purchase price. Every customer you retain, every employee you keep, and every system you maintain is protecting the value you've spent years building.

Don't let the excitement of selling cause you to take your foot off the gas. The finish line isn't when you sign the listing agreement. It's when the wire transfer hits your account.

Ready to sell your business and want to make sure you protect its full value? Contact me for a confidential conversation about your timeline, your business, and how to get the best possible outcome.

Related Articles

March 19, 2026

How to Build a Business That Runs Without You

A business that depends on you has a ceiling on its value. Here's the step-by-step process for building real owner independence over 18-24 months.

March 2, 2026

First 90 Days After Buying a Business: Your Transition Playbook

The first 90 days after buying a business determine whether your acquisition succeeds. Here's exactly what to do each week, and what to avoid.

January 4, 2026

Live Social Selling Is Reshaping Ecommerce in 2026

Live social selling delivers 9 to 30% conversion rates vs 2 to 3% for standard ecommerce. Why brands are shifting to live commerce in 2026.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.