If you own a manufacturing business and you have been thinking about selling, 2026 offers a valuation window that may not come around again for a decade. Reshoring, tariffs on Chinese goods, and over $1.5 trillion in committed domestic manufacturing investment have created a temporary boom in US manufacturing valuations that is already showing signs of peaking.

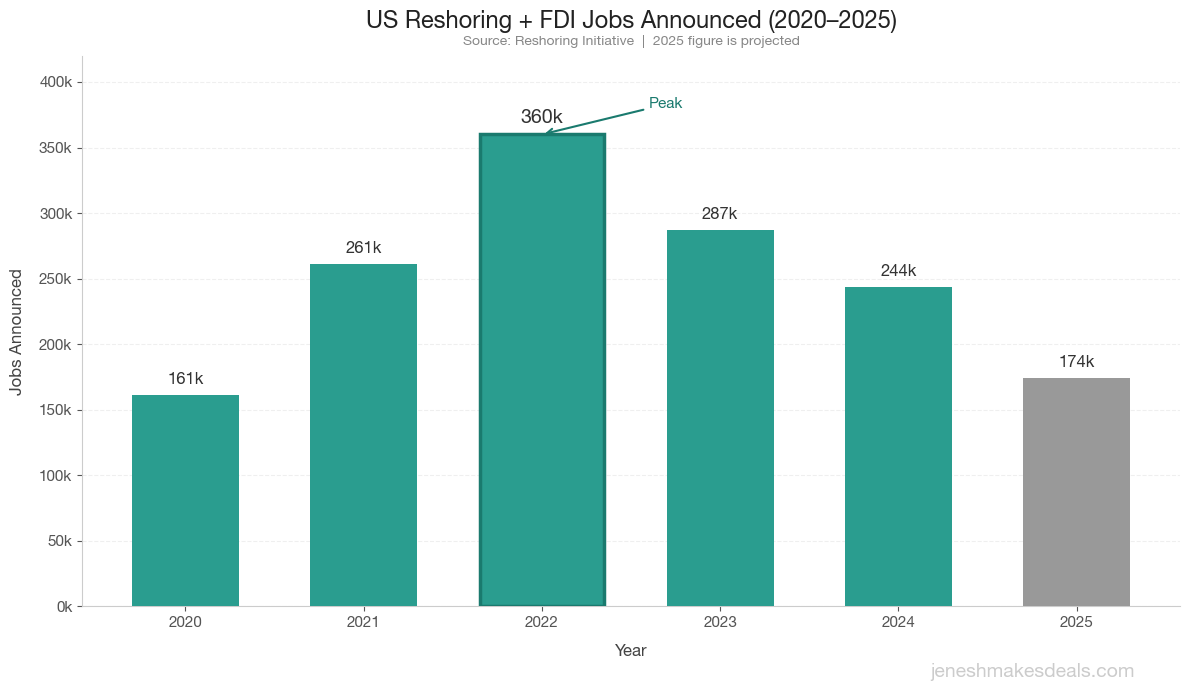

The numbers tell the story. Since 2010, over 2 million reshoring and FDI manufacturing jobs have been announced in the US. The CHIPS Act and IRA triggered a record 360,000 job announcements in 2022 alone. Average manufacturing deal multiples jumped 9% from the first half of 2024 to the first half of 2025, hitting 11.1x EBITDA. Deal values more than doubled in the same period.

But the signals of moderation are already appearing. Reshoring job announcements dropped from 360,000 in 2022 to a projected 174,000 in 2025. US manufacturing employment is actually down 108,000 in 2025 despite continued reshoring announcements. Automation and AI are projected to alter 60% of manufacturing jobs by 2030, which will reduce the premium buyers pay for labor dependent operations.

I work with manufacturing business owners who built their companies over 20 to 30 years and are now sitting on businesses worth significantly more than they were three years ago. The ones who understand why that premium exists, and how long it will last, are the ones making the best exit decisions.

Here is what every manufacturing business owner needs to know about selling in 2026.

The Reshoring Boom by the Numbers

US manufacturing reshoring has accelerated dramatically since 2020, driven by pandemic supply chain shocks, geopolitical risk with China, and massive federal incentive programs.

| Year | Jobs Announced (Reshoring + FDI) | Key Drivers |

|---|---|---|

| 2020 | 160,649 | Pandemic driven supply chain awareness |

| 2021 | ~261,000 | Post COVID recovery, demand surge |

| 2022 | 360,000+ | CHIPS Act and IRA passage, highest ever recorded |

| 2023 | ~287,000 | Moderation from record levels |

| 2024 | 244,000 | Sustained by tariff hedging and geopolitical risk |

| 2025 (proj.) | 174,000 | Lower due to policy uncertainty |

The investment scale is staggering. Over $1.5 trillion in committed manufacturing investments are now tracked across companies like Apple ($500B+ over four years), TSMC (Arizona semiconductor fabs), Micron (Idaho and Virginia), Johnson & Johnson ($55B through 2029), and Caterpillar ($725M Indiana facility). Construction spending on manufacturing facilities increased 40% in 2022 compared to 2021, and the construction boom has continued.

But here is the nuance most owners miss. The actual net employment picture tells a different story than the announcements. Between January 2020 and March 2025, there was only a slight net increase in manufacturing employment, with much of it attributed to pandemic rebound. US manufacturing employment was down 108,000 in 2025, suggesting that job announcements do not always translate to sustained net employment gains.

This gap between announcements and reality matters for valuations. The premium buyers are paying right now is partially built on the reshoring narrative. As that narrative moderates, so will the premium.

How Tariffs Created a Valuation Shield for Domestic Manufacturers

The current tariff regime on Chinese goods provides domestic manufacturers with meaningful cost protection, but the structure is complex and volatile.

The effective tariff rate on Chinese goods sits at 29.3% as of late 2025, down from 37.1% before the US China agreement reached in October 2025. The overall US average tariff rate on all imports rose from 2.6% to 13% over the course of 2025.

| Tariff Category | Rate | Target Products |

|---|---|---|

| Liberation Day (reduced) | 10% (was 34%) | All goods with exclusions |

| Section 232, Steel/Aluminum | 50% | Steel, aluminum, derivatives, appliances |

| Section 232, Autos | 25% | Passenger vehicles, auto parts |

| Section 232, Copper | 50% | Copper products, electrical components |

| Section 301, Lists 1 to 3 | 25% | Broad industrial/manufacturing goods |

| Section 301, 4 Year Review | 25% to 100% | EVs, batteries, semiconductors, solar, critical minerals |

Yale Budget Lab estimates that the 2025 to 2026 tariffs slow real GDP growth by 0.4 percentage points in 2026, with the economy persistently 0.3% smaller. However, US manufacturing output expands by 3.2% as a result.

For manufacturing business owners, tariffs create a temporary competitive moat. Your domestic production is worth more to buyers when imported alternatives face a 29% effective tax. But tariffs are policy decisions, not market fundamentals. They can change with an election, a trade deal, or a diplomatic shift. The protection is real today, but it is not guaranteed tomorrow.

Monthly tariff payments by midsize US firms have tripled compared to early 2025 levels, which means your raw material costs are also rising. Manufacturing revenues are expected to rise 4.4% in 2026, and 86% of manufacturers plan to pass on at least some tariff related costs. The question for sellers is whether to capture today's elevated valuation or absorb the ongoing cost uncertainty of operating in a volatile tariff environment.

Want to see what your manufacturing business is worth right now? Use our free manufacturing business valuation calculator to get an instant estimate.

What Manufacturing Multiples Look Like in 2026

Manufacturing valuation multiples vary enormously by subsector, size, and technology positioning. The dispersion is the widest it has been in years.

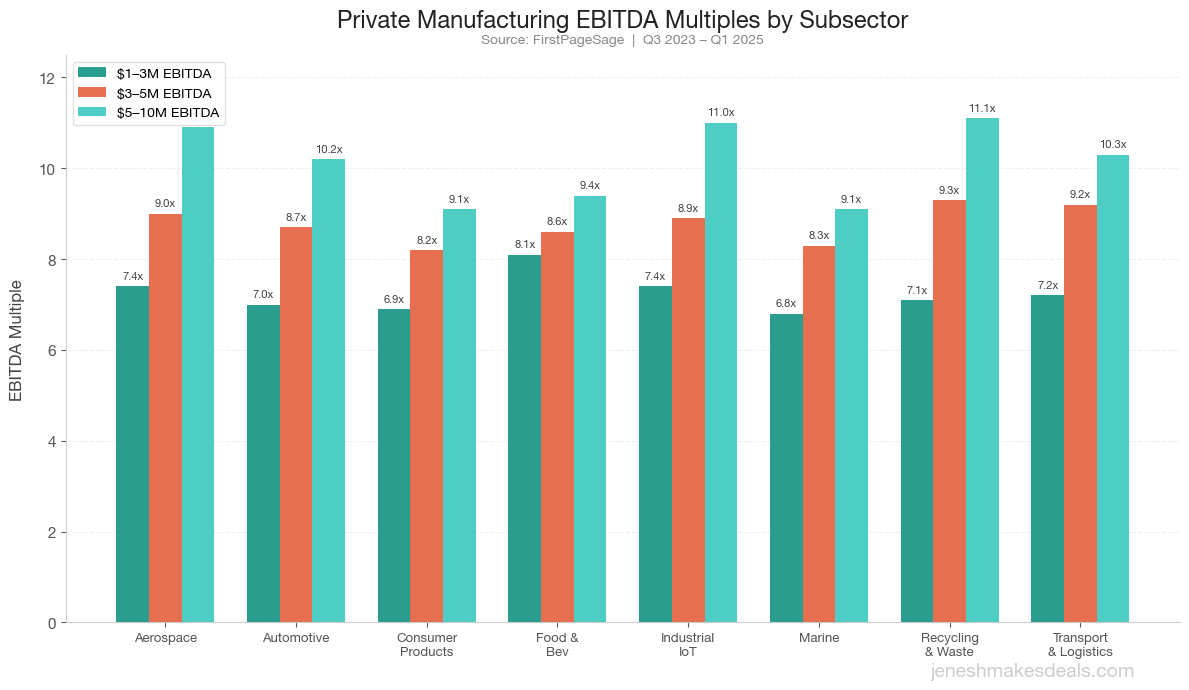

Private Market Multiples by Subsector and Size

| Subsector | $1 to 3M EBITDA | $3 to 5M EBITDA | $5 to 10M EBITDA |

|---|---|---|---|

| Aerospace | 7.4x | 9.0x | 10.9x |

| Automotive | 7.0x | 8.7x | 10.2x |

| Consumer Products | 6.9x | 8.2x | 9.1x |

| Food and Beverage | 8.1x | 8.6x | 9.4x |

| Industrial IoT | 7.4x | 8.9x | 11.0x |

| Marine and Maritime | 6.8x | 8.3x | 9.1x |

| Recycling and Waste | 7.1x | 9.3x | 11.1x |

| Transportation and Logistics | 7.2x | 9.2x | 10.3x |

The average manufacturing deal multiple increased approximately 9% from the first half of 2024 to the first half of 2025, from 10.2x to 11.1x EBITDA. Average deal values more than doubled in six months.

The median EBITDA multiple across private manufacturing firms hovers around 5.4x, with the 25th percentile at 3.2x and 75th percentile at 10.4x. Larger firms with revenue over $10M can achieve multiples as high as 9.0x.

The key insight is extreme valuation dispersion. Industrial IoT, recycling and waste management, and aerospace command 10x to 11x EBITDA at the $5M to $10M level. Traditional manufacturing subsectors like marine and consumer products trade at 9x. Technology adjacent industrial assets are increasingly being valued more like software companies.

Companies that sold through M&A advisory firms received, on average, 31% more than those who ran their own sale process. That statistic alone should make every manufacturing owner considering a sale think carefully about how they approach the process.

What Margins Look Like Across Manufacturing Subsectors

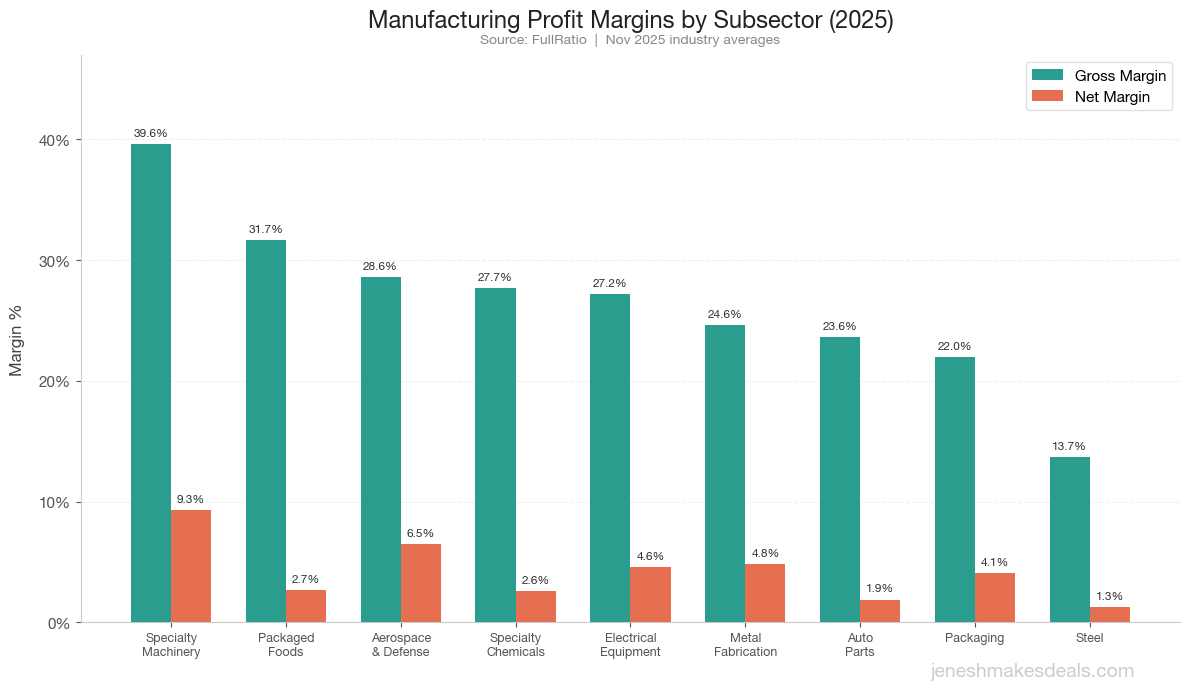

Understanding where your subsector falls on the margin spectrum directly affects your valuation.

| Subsector | Avg Gross Margin | Avg Net Margin |

|---|---|---|

| Specialty Industrial Machinery | 39.6% | 9.3% |

| Packaged Foods | 31.7% | 2.7% |

| Aerospace and Defense | 28.6% | 6.5% |

| Specialty Chemicals | 27.7% | 2.6% |

| Electrical Equipment and Parts | 27.2% | 4.6% |

| Metal Fabrication | 24.6% | 4.8% |

| Auto Parts | 23.6% | 1.9% |

| Packaging and Containers | 22.0% | 4.1% |

| Farm and Heavy Construction Machinery | 22.6% | 6.4% |

| Steel | 13.7% | 1.3% |

The lowest margin subsectors, steel, aluminum, and auto manufacturing, are most vulnerable to tariff driven input cost volatility. Raw material prices averaged a 5.4% increase in 2025. Automotive OEM margins continued to decline in Q3 2025, reaching 3.9%, down nearly 60% from their 2021 peak and now well below pre COVID levels.

For sellers, the message is clear. If your margins are above your subsector average, that is a significant valuation premium waiting to be captured. If your margins are below average, improving them before going to market can add 1x to 2x turns to your multiple.

PE and Strategic Buyers Are Competing for Manufacturing Assets

2025 saw strong M&A momentum across industrials and manufacturing, with strategic buyers outbidding PE for the best assets.

The deal landscape is dominated by fewer but larger transactions, with strategic buyers paying premium multiples for technology differentiation, recurring revenue, and mission critical positioning.

| Buyer Type | Volume Share | Value Share | Strategy |

|---|---|---|---|

| Strategic acquirers | 51% to 57% | 62% to 69% | Capability and technology acquisitions |

| Private equity | 43% to 49% | 31% to 38% | Buy and build platforms, add on acquisitions |

Key numbers from 2025.

- Global PE deal value rebounded 19% to $2.6 trillion

- US industrial manufacturing saw 8,853 deals worth $303.7B in 2024, up 14.3% in value versus 2023

- 2025 is on track to be the second highest year in deal activity, up 40% in value to an estimated $4.9 trillion

- More than two thirds of total deal value in 2025 came from transactions above $5B

Hottest Subsectors for Buyers

- Specialty manufacturing (precision machining, metal fabrication with automation)

- Industrial services (maintenance, inspection, environmental)

- Energy transition (grid equipment, electrical components, battery supply chain)

- Defense and aerospace supply chain businesses

- Industrial software and automation (premium multiples, recurring revenue)

Companies with FDA approved materials, AI driven quality control, and proprietary processing technologies have commanded premium valuations in precision manufacturing.

Not sure how buyers would value your manufacturing business? Contact me for a free consultation to discuss what your business might be worth in today's market.

The CHIPS Act and IRA Created a Temporary Investment Floor

Two landmark pieces of legislation have directly inflated manufacturing valuations and activity since 2022.

CHIPS Act

- Total allocation of $52.7 billion to support US semiconductor manufacturing

- 25% Advanced Manufacturing Investment Tax Credit for property placed in service before December 2024, 35% for property after December 2025

- $33.7 billion in direct funding and $5.5 billion in loans awarded across 20 projects

Inflation Reduction Act

- $369 billion over the next decade to incentivize domestic green energy investment

- Section 45X advanced manufacturing production credit for solar components, wind components, inverters, battery components, and critical minerals

- The most significant post IRA investments have been in battery production facilities

The 2022 record of 360,000+ reshoring and FDI jobs was directly attributed to the passage of both laws. Semiconductor and clean energy manufacturing assets have seen significant valuation uplift. But political uncertainty around the IRA's future has created some deal hesitancy, which is another reason to consider selling while the incentive framework is still intact.

Why This Premium Is Temporary: Automation Changes Everything

This is the part most manufacturing owners do not want to hear. The same forces that are inflating valuations today, labor scarcity and supply chain risk, are being solved by automation and AI. When those solutions mature, the premium disappears.

| Source | Projection | Timeframe |

|---|---|---|

| McKinsey | 30% of US jobs automatable, 60% significantly altered | By 2030 |

| Forrester | 6.1% of US jobs lost (10.4M jobs), 20% strongly influenced | By 2030 |

| Wharton/Penn | 40% of labor income exposed to AI automation | Current |

| WEF | 170M new jobs created globally vs 92M displaced | By 2030 |

Current AI tools deliver average labor cost savings of approximately 25%, with studies showing gains ranging from 10% to 55%. These savings are projected to grow to 40% over coming decades.

For manufacturing specifically, automation is already the key enabler of competitive reshoring. The 2025 National Metalworking Reshoring Award winners, GE Appliance and Marlin Steel, both used automation to make domestic production cost competitive with offshore alternatives. 65% of surveyed manufacturers say attracting and retaining talent is their number one challenge, and automation addresses both the pricing gap versus offshore production and the skilled workforce shortage simultaneously.

The net effect on valuations is already visible. Firms with high automation levels and AI integration are commanding premium multiples. Labor dependent operations face structural headwinds from both workforce shortages and margin compression. Job growth has stagnated in occupations with the most AI automation potential, with employment in fully automatable roles falling sharply in 2024.

If you sell your manufacturing business today, a buyer pays for your current revenue and margins. If you wait three to five years, that buyer will be comparing your labor dependent operation against competitors running AI driven production lines at 25% to 40% lower labor costs. Your valuation will reflect that comparison.

The Silver Tsunami: 40% of Manufacturing Owners Are Baby Boomers

The demographic wave hitting manufacturing is massive and creates both opportunity and urgency for sellers.

- 40% to 41% of all US small businesses are owned by baby boomers

- 2.3 to 3 million boomer owned businesses will change hands over the next decade

- Baby boomer owned businesses employ approximately 32 million people and generate nearly $6.5 trillion in revenue annually

- An estimated $10 trillion in business assets will change hands over the next two decades

- 10,000 baby boomers reach retirement age every single day, a trend continuing into the 2030s

- By 2030, every baby boomer will be 65 or older

- Only about 50% of retiring business owners have established formal succession plans

In manufacturing specifically, this is concerning because businesses are often closely tied to the owner's expertise, relationships, and institutional knowledge. Today's younger generations show less interest in taking over family manufacturing businesses. Only 4% of family businesses survive to the fourth generation.

This creates a dual dynamic. The sheer volume of businesses coming to market could depress valuations in some subsectors as supply outpaces qualified buyer demand. But PE firms are actively targeting this wave through buy and build platforms in fragmented manufacturing niches, recognizing that many well run businesses will be available at reasonable multiples.

The smart move is to sell ahead of the wave, not into it. Early sellers get premium multiples and competitive processes. Late sellers compete with thousands of other retiring owners for the same pool of buyers.

What Buyers Specifically Look For in a Manufacturing Acquisition

Manufacturing M&A due diligence is more operationally intensive than most sectors. Here is exactly what buyers prioritize.

1. Equipment Age and Condition

Buyers review age, maintenance records, downtime history, replacement timelines, and remaining useful life. Deferred maintenance or aging CNC equipment is a major red flag that can sink deals or compress multiples significantly.

2. Automation Level

Degree of manual intervention, scrap and rework rates. Highly automated operations command premium multiples. This is the single fastest growing valuation differentiator in manufacturing M&A.

3. Customer Concentration

Revenue dependence on one to three customers significantly increases perceived risk. Buyers heavily scrutinize this factor. Diversified customer bases with no single customer above 10% of revenue are ideal.

4. Contract Structure

Long term contracts with price escalation clauses are highly valued. Spot market dependent businesses trade at discounts because revenue is unpredictable.

5. Workforce Documentation

Employee tenure, turnover rates, I 9 compliance, training records, and safety records. Key person dependency leads to longer transitions, earnouts, and lower upfront consideration.

6. Plant Utilization

Current capacity versus maximum capacity. Buyers want to see room for growth without major capital expenditure. Production bottlenecks are identified and factored into pricing.

7. Quality Systems

Standard operating procedures, quality control processes, lean manufacturing practices, and customer return and refund trends. Systemic quality problems revealed during diligence can kill deals.

Ready to see where your manufacturing business stands? Use our free manufacturing valuation calculator to get a baseline estimate right now.

How to Position Your Manufacturing Business for Maximum Value

If you are considering selling in the next 12 to 24 months, here is what will move the needle on your multiple.

Invest in Automation Now

Even modest automation investments, a new CNC cell, automated inspection, robotic palletizing, signal to buyers that your operation is moving in the right direction. The valuation premium for automated operations versus manual ones is growing every quarter.

Diversify Your Customer Base

If one customer represents more than 20% of revenue, start actively pursuing new accounts. This is one of the most impactful changes you can make pre sale.

Document Everything

SOPs, maintenance logs, quality records, training programs. Buyers pay premiums for businesses with institutional knowledge captured in documentation rather than locked in the owner's head.

Clean Up Your Financials

Three to five years of organized P&Ls, tax returns, and balance sheets with clear addbacks. Companies that use M&A advisory firms to run their sale process receive on average 31% more than those who run the process independently.

Secure Long Term Contracts

Convert spot market customers to contracts with price escalation clauses wherever possible. Recurring, predictable revenue commands higher multiples.

Reduce Owner Dependency

If the business requires you to be on the floor every day, start building the management layer. Buyers discount heavily for owner dependency because it represents transition risk.

Common Mistakes Manufacturing Owners Make When Selling

After working with business owners across industries, here are the mistakes I see most often from manufacturing sellers.

Not understanding subsector valuation dispersion. Aerospace at 10.9x and marine at 9.1x for the same EBITDA size range is a meaningful difference. Know where your subsector trades before setting expectations.

Ignoring the automation premium. Buyers are explicitly paying more for automated operations. If you have invested in automation, make sure it is front and center in your marketing materials. If you have not, understand that you are competing against sellers who have.

Running the sale process yourself. The data is clear. Companies that use M&A advisory firms receive 31% more on average. On a $5M EBITDA manufacturing business at 7x, that is an additional $1.55M in value. The advisory fee pays for itself many times over. If you are on the fence, read my guide on whether you should use a broker to sell your business.

Waiting for reshoring premiums to grow further. The data shows reshoring job announcements peaked in 2022 and have declined every year since. The premium is at or near its peak. Waiting for it to grow further is a bet against the trend.

Deferring equipment maintenance. Buyers will conduct thorough equipment inspections. Deferred maintenance shows up as either a price reduction or a deal breaker. Spend the money now.

Not planning for the silver tsunami. If you wait until every 65 year old manufacturing owner tries to sell simultaneously, you are competing with thousands of sellers. Early movers get premium pricing.

What to Do Next

The manufacturing valuation environment in 2026 is the product of several temporary forces converging. Reshoring momentum from pandemic supply chain shocks. Tariff protection creating domestic cost advantages. $1.5 trillion in committed investment driven by CHIPS and IRA. PE and strategic buyers competing aggressively for quality assets. And a demographic wave of retiring owners creating urgency.

Not all of these forces will persist. Reshoring announcements are declining. Tariffs are politically dependent. Automation will reduce the labor premium. And the silver tsunami will eventually flood the market with supply.

If you own a manufacturing business and are considering an exit in the next one to three years, here is what I recommend.

-

Get a valuation. Use our free manufacturing business valuation calculator to get a baseline estimate right now.

-

Talk to someone who understands this market. Schedule a free consultation with me and I will give you an honest assessment of your business's attractiveness to buyers, what you could realistically expect in a sale, and what steps would increase your value.

-

Explore your financing options. If you are on the buying side and looking to acquire a manufacturing business during the reshoring window, check out our funding options for business acquisitions.

The window is open. The multiples reflect a once in a decade convergence of favorable forces. The question is whether you will capture that value or watch it normalize.

Sources

- Reshoring Initiative, 2024 Annual Report

- Reshoring Initiative, 2022 Data Report

- IndustrialSage, 10 Reshoring Stats 2025

- Progressive Policy Institute, US Manufacturing Employment 2025

- China Briefing, US China Tariff Rates 2025

- Yale Budget Lab, State of US Tariffs January 2026

- FirstPageSage, Manufacturing EBITDA Multiples 2025

- ClearlyAcquired, Manufacturing Valuation Multiples

- NYU Stern (Damodaran), EV/EBITDA Multiples by Sector

- MergersAndAcquisitions.net, Industrial Manufacturing M&A

- PwC, Industrial Manufacturing Deals 2026 Outlook

- McKinsey, Global Private Markets Report 2025

- Bain, Looking Back at M&A in 2025

- FullRatio, Profit Margins by Industry

- Manufacturing Dive, Manufacturers Plan Price Hikes

- Forbes, The Silver Tsunami Is Reshaping Small Business

- Hadley Capital, Business Succession Planning

- AMT, Reshoring and Future of US Manufacturing

- Capstone Partners, Precision Manufacturing Market Update

- Horizon MAA, What Buyers Look For in Manufacturing

Frequently Asked Questions

How much is my manufacturing business worth in 2026?

Manufacturing business valuations in 2026 vary enormously by subsector and size. Our business valuation calculator can give you a quick estimate based on your earnings. Private market EBITDA multiples range from 6.8x to 11.1x depending on your subsector and EBITDA level. Aerospace and Industrial IoT businesses with $5M to $10M EBITDA command 10.9x to 11.0x. Consumer products and marine businesses in the same size range trade at 9.1x. The median EBITDA multiple across all private manufacturing firms is 5.4x, with the 75th percentile at 10.4x. Companies that use M&A advisory firms to run their sale process receive on average 31% more than those who sell independently.

Are reshoring and tariffs actually boosting manufacturing valuations?

Yes, but the effect is nuanced. Tariffs create a 29.3% effective cost barrier on Chinese goods, which protects domestic manufacturers and supports premium valuations. US manufacturing output is expanding 3.2% due to tariffs. Over $1.5 trillion in domestic manufacturing investment has been committed. However, reshoring job announcements have declined from 360,000 in 2022 to a projected 174,000 in 2025, and US manufacturing employment is actually down 108,000 in 2025. The premium is real but showing signs of moderation.

Will automation reduce my manufacturing business valuation?

It depends on your automation level. Manufacturing businesses with high automation, AI driven quality control, and Industry 4.0 technologies are commanding premium multiples right now. Labor dependent operations face structural headwinds from both workforce shortages and margin compression. Current AI tools deliver average labor cost savings of 25%, projected to grow to 40%. The valuation gap between automated and manual operations is widening. If your business is labor dependent, selling before automation further widens this gap may be the best financial decision.

What do buyers look for in a manufacturing acquisition?

Buyers prioritize equipment age and condition, automation level, customer concentration (no single customer above 10% of revenue), contract structure (long term with price escalation clauses), workforce documentation and stability, plant utilization and capacity for growth, and quality systems. Highly automated operations with diversified customers, long term contracts, and documented processes command the highest multiples.

Is 2026 the peak for manufacturing business valuations?

The evidence suggests 2026 is at or near the peak of a reshoring driven valuation cycle. Average deal multiples increased 9% in the first half of 2025 and deal values more than doubled. However, reshoring announcements are declining, tariff protection is politically dependent, automation will reduce labor premiums over time, and the baby boomer retirement wave will increase the supply of businesses for sale. The structural forces supporting premiums (supply chain risk repricing, CHIPS and IRA incentives) appear durable, but the speculative component is already fading.

Related Articles

April 30, 2026

How Long Does It Really Take to Sell a Business

Most sellers are shocked by how long it takes. Here's the honest timeline from listing to closing, and what actually speeds things up.

April 26, 2026

How to Structure an Earnout That Works for Seller and Buyer

Most earnouts fail because they're poorly structured. Here's how to build earnout terms that protect both sides of the deal.

April 24, 2026

How to Value Intellectual Property in a Business Sale

Your IP could be worth more than your equipment. Learn how patents, trademarks, and trade secrets affect your business valuation.

About the Author

Jenesh Napit is an experienced business broker specializing in business acquisitions, valuations, and exit planning. With a Bachelor's degree in Economics and Finance and years of experience helping clients successfully buy and sell businesses, he provides expert guidance throughout the entire transaction process. As a verified business broker on BizBuySell and member of Hedgestone Business Advisors, he brings deep expertise in business valuation, SBA financing, due diligence, and negotiation strategies.

You might also be interested in

Free Business Calculators

Try our business valuation calculator and ROI calculator to estimate values and returns instantly.

How to Buy a Business Guide

Download our comprehensive free guide covering everything you need to know about buying a business.

Our Services

Explore our professional business brokerage services including valuations and buyer representation.

More Articles

Browse our complete collection of business brokerage insights and expertise.